Feed Premixes Market Report Scope & Overview:

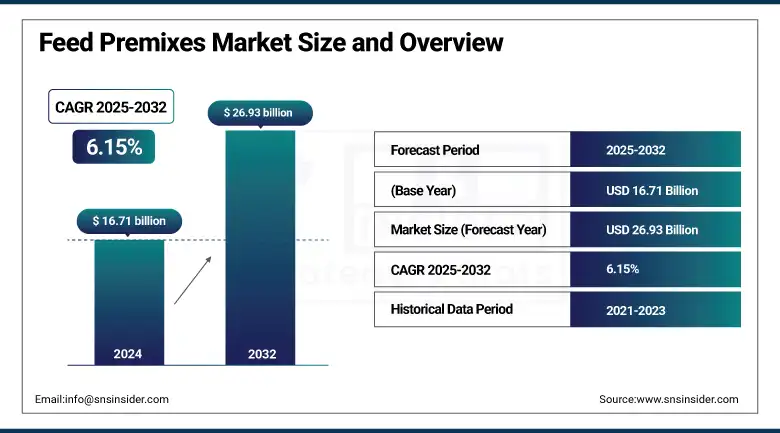

The Feed Premixes Market size was valued at USD 16.71 billion in 2024 and is expected to reach USD 26.93 billion by 2032, growing at a CAGR of 6.15% over the forecast period of 2025-2032.

The feed premix industry is increasingly dynamic with precision nutrition, digital dosing systems, and the sustainable nature of premix additive demand in play. The personalized vitamin premix is being driven by the growth of aquaculture, and the feed premix market is increasingly adapting to the clean-label trend. Stringent adherence to regulatory standards, including Morocco Order No. 2-23-557 and WTO notice G/SPS/N/MAR/106, is complementing the feed premixes industry expansion as well.

To Get more information On Feed Premixes Market - Request Free Sample Report

Feed premix producers such as Cargill are increasing capacity and have launched a new premix line in Mindanao in June 2025 to increase regional feed premix market share. The current USDA/NOP review is also impacting VPM and additive application. The very latest feed premix market trends are now focused on traceability, innovation, and animal health. Cumulatively, strategic investments, regulations, and custom formulations are driving robust feed premixes market trends with increasing focus on dry and liquid premixes, even as the feed premixes market trends tally to a wider spectrum across the global animal feed sectors.

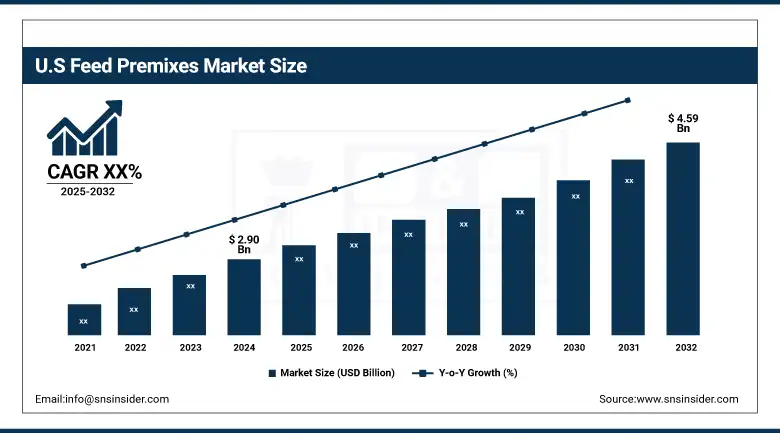

The U.S. leads the region with a market size of USD 2.90 billion in 2024 and is projected to reach a value of USD 4.59 billion by 2032 with a market share of around 79%, supported by USDA-backed research into nutrient-dense formulations and precision feeding technologies that elevate feed conversion efficiency.

Feed Premixes Market Dynamics:

Drivers:

-

Adoption of precision livestock farming enhances the Feed Premixes Market growth

Precision livestock farming leverages digital solutions and data analytics to customize nutrition to optimize feed efficiency and the health of the animals. This creates a demand for tailored premix additives and vitamin premix blends suited for various animal needs. The animal feed premix market is also modernized by the advanced livestock monitoring, which had 12% growth in the absolute number of the farms using it from 2020-2024, as agriculture on livestock monitoring adapted the USDA National Agricultural Statistics Service. In response, feed premixes companies are developing formulations that can be delivered through automated feeding systems, thus propelling the Feed Premixes Market size growth and increasing in overall market share.

-

Expansion of aquaculture drives demand for specialized Feed Premixes Market products

The booming growth of Aquaculture, with the Food and Agriculture Organization (FAO) documenting a global average annual growth rate of 5.8% from 2017 and 2023, has resulted in increased demand for species-specific vitamin premix and premix additive formulations that are unique to aquatic species. In this regard, the feed premixes companies are working on specialized products that help improve aquatic animal health and productivity, hence significantly influencing feed premixes market trends and size worldwide, over the forecast period.

Restraints:

-

Raw material supply chain disruptions impede Feed Premixes Market size expansion

Shortages in important raw materials, including vitamins and amino acids, compounded with continued global supply chain disruptions and slowdowns resulting from more stringent FDA traceability rules, create difficulties for feed premix manufacturers trying to ensure consistent output. In the years 2022-2024, the FDA reported vitamin shortages, with corresponding decreased availability of and formulation of vitamin premixes. This supply volatility adds cost and lead-time and further constrains the ability of the animal feed premix market to meet demand.

Feed Premixes Market Segmentation Analysis:

By Ingredient Type

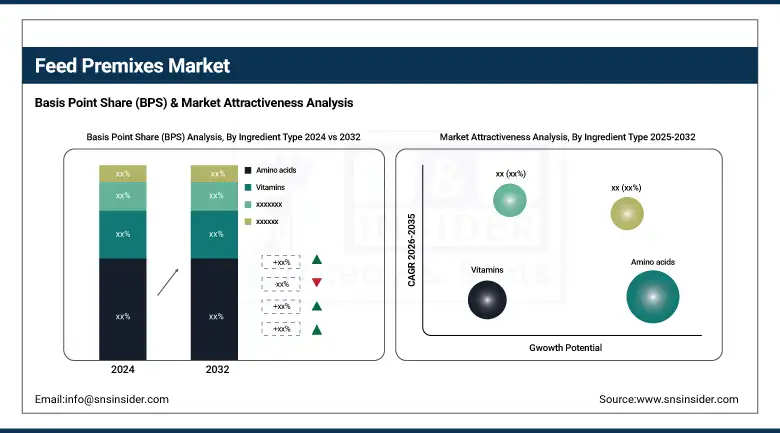

Amino acids dominated the feed premixes market in 2024 with a market share of 33.6%, led by lysine and methionine, which are critical in poultry and swine nutrition. Their efficacy is attributed to their established capability to improve growth rate and feed conversion. According to the US National Research Council (NRC), the balance of amino acids is essential to decrease nitrogen excretion, and therefore to reduce the environmental impact. USDA-funded nutrient optimization studies implemented to help decrease feed waste in commercial practices have had an impact on the incorporation of amino acid additives in practices such as precision feeding.

Vitamins are projected to be the fastest-growing segment from 2025 to 2032 with a CAGR of 6.69%, driven by increasing demand for immune-enhancing formulations such as Vitamin A, D3, and E in aquafeed. FAO aquaculture report (2023) emphasizes micronutrient deficiencies in worldwide aquatic culture and thus drives the requirement for vitamin-fortified premix solutions. The minor category of fat-soluble vitamins will be the leading segment owing to stability and bioavailability. This trend is also supported by regulatory activities related to the FDA’s CVM guidance for including vitamins in feed safely.

By Livestock

Poultry emerged as the dominant livestock segment in the feed premixes market in 2024, with an estimated market share of 35.2%, with broilers leading due to their shorter production cycles and high commercial demand. According to the USDA, the nation’s broiler production exceeded 9 billion heads in 2023, with overwhelming use of premix for weight gain enhancement. Dominant Players Feed premixes manufacturers are focusing on poultry-dedicated formulations such as amino acids and premix additives, driving feed cost and production efficiency, as well as compliance with the biosecurity laws.

Aquaculture is the fastest-growing segment during 2025–2032, with an estimated CAGR of 7.11%, led by the increasing use of fortified feed in farmed salmon and shrimp. In 2022, more than 56% of the fish consumed globally was cultivated through aquaculture demand for accurate nutrient input to ensure good fish condition and yield is therefore on the rise. Vitamin premix and mineral premix compounds are becoming popular with increased disease prevention requirements in intensive aquaculture. The sustained feed premixes market in this segment is being driven by technological advancements such as microencapsulation in aquatic premix additives.

By Form

Dry form dominated the feed premixes market in 2024 with a market share of 73.4%, attributed to longer shelf-life, cost-saving, and transportation of feed premixes. The use of dry premix formulations is common in both poultry and ruminant diets, particularly in large automated feed mills. More than 80% of compound feed produced in the U.S. is of dry origin, according to the American Feed Industry Association (AFIA). The reasons for the majority usage of dry form in feed premixes have been because of the blending flexibility and an even distribution of the nutrients in the feed batches.

Liquid form is expected to be the fastest-growing segment through 2032, with a CAGR of 6.35%, driven by adoption in precision livestock farming and automated liquid dosing systems. The National Animal Nutrition Program (NANP) supports studies on liquid nutrient delivery systems in swine and dairy farms to improve absorption rates. Liquid vitamin premix and amino acid concentrates are gaining traction for real-time customization of feed inputs, especially in high-value livestock production systems. Improved bioavailability and automation compatibility are fueling this shift toward liquid feed premix solutions.

Feed Premixes Market Regional Outlook:

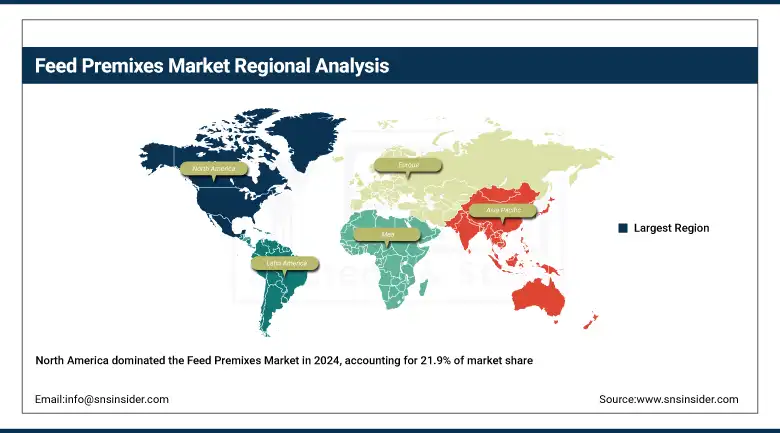

North America held the third-dominant feed premixes market share at 21.9% in 2024, driven by advanced livestock nutrition practices and widespread use of digital feeding systems. According to the American Feed Industry Association, over 75% of US feed facilities use pre-formulated vitamin premix and premix additive solutions. Canada is the fastest-growing contributor, with government initiatives to expand sustainable animal feed production. This structured adoption of fortified premixes continues to strengthen the region’s position in the animal feed premix market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe held 25.1% of the feed premixes market share in 2024, driven by strict feed safety laws and organic product demand. Germany and France led through certified additives, while EFSA regulations and the EU’s Green Deal supported standardized, sustainable formulations. Europe’s focus on compliance and clean-label vitamin premix solutions strengthened its position in high-quality premix manufacturing.

Asia Pacific dominated the feed premixes market in 2024, holding 34.7% of global share, due to rising meat consumption, growing aquaculture, and rapid industrialization of livestock farming. China leads in premix production volume, while India’s poultry sector relies heavily on amino acid and vitamin premix applications. The Ministry of Agriculture and Farmers Welfare in India supports premix innovation through feed policy modernization and subsidy programs. Growing consumer demand for protein-rich diets and tailored feed blends fuels ongoing Feed Premixes Market growth across the region.

Latin America is witnessing strong feed premixes market growth, led by Brazil’s poultry and swine sectors and government-backed feed quality initiatives. Argentina’s rising demand for sustainable vitamin premix formulations, driven by increased animal product exports, is also boosting regional market trends. Improved veterinary infrastructure and digitalization efforts are further enhancing feed premix adoption across the continent.

The Middle East & Africa region is the fastest-growing in the feed premixes market with the highest CAGR of 7.25%, owing to rapid urbanization, growing animal protein demand, and expanding commercial poultry production. South Africa leads with increased integration of vitamin premix solutions and feed automation systems. According to the South African Poultry Association, feed manufacturers are enhancing premix usage to meet national nutrition benchmarks. Additionally, Morocco’s new Order No. 2-23-557 on feed labeling and quality is encouraging the structured growth of premix additive use, further propelling the feed premixes market size in the region.

Key Players:

The major feed premixes market competitors include Cargill, Incorporated, Archer Daniels Midland Company (ADM), DSM-Firmenich, Nutreco N.V., Land O’Lakes, Inc. (Purina Animal Nutrition), Alltech, Inc., DLG Group, De Heus Animal Nutrition B.V., AB Agri Ltd., and BEC Feed Solutions Pty Ltd.

Recent Developments:

-

In October 2024, DSM‑Firmenich opened a new 10,000-ton capacity premix facility in Egypt to serve Egypt, the Middle East, and Africa, enhancing the supply of vitamins, minerals, and additives for sustainable animal nutrition.

-

In January 2024, Cargill launched a $28 million automated premix plant in Vietnam with 40,000-ton capacity, improving access to vitamin premixes and additives for livestock and aquaculture, boosting regional feed self-sufficiency.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 16.71 billion |

| Market Size by 2032 | USD 26.93 billion |

| CAGR | CAGR of 6.15% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Ingredient Type (Amino acids, Vitamins, Minerals, Antibiotics, Antioxidants, Others) •By Livestock (Pet, Poultry, Ruminant, Swine, Aquaculture, Others) •By Form (Dry, Liquid) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Cargill, Incorporated, Archer Daniels Midland Company (ADM), DSM-Firmenich, Nutreco N.V., Land O’Lakes, Inc. (Purina Animal Nutrition), Alltech, Inc., DLG Group, De Heus Animal Nutrition B.V., AB Agri Ltd., and BEC Feed Solutions Pty Ltd. |

Frequently Asked Questions

Traceability tech, automated dosing, and fortified premix additive innovations are key feed premixes market trends and opportunities.

Key feed premix companies include Cargill, ADM, DSM-Firmenich, Nutreco, Alltech, Land O’Lakes, and De Heus.

Rising aquaculture, precision livestock farming, and clean-label vitamin premix demand are boosting the global feed premixes market growth.

The feed premixes market is projected to grow at a CAGR of 6.15% from 2025 to 2032.

The global feed premixes market was valued at USD 16.71 billion in 2024 across all livestock and ingredient types.

Get in Touch