Pipe Insulation Market Report Scope & Overview:

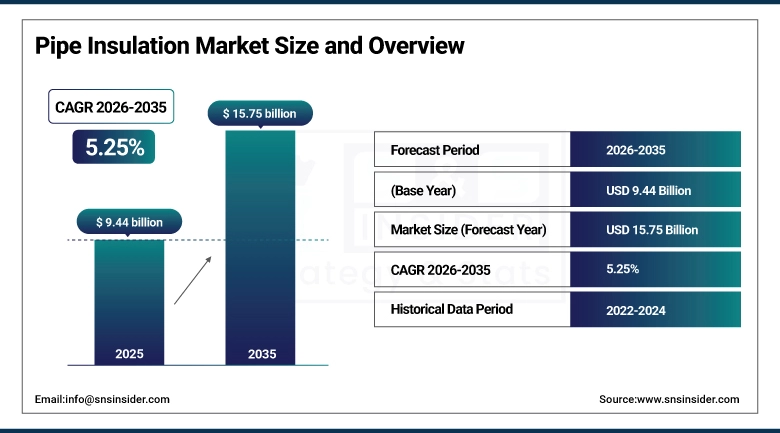

The Pipe Insulation Market size was valued at USD 9.44 billion in 2025 and is expected to reach USD 15.75 billion by 2035, growing at a CAGR of 5.25% over the forecast period of 2026-2035.

The global pipe insulation market trend is a growing demand for energy-efficient thermal management solutions such as pre-formed pipe insulation systems, polyurethane foam insulation, and elastomeric foam products as the growth of the market is driven by rising energy costs, tightening building energy codes, and increasing pressure on industrial operators to reduce heat losses across process piping networks. This trend is also driven by rapid expansion of district energy infrastructure and the accelerating pace of commercial building retrofits as construction developers and facility managers become more focused on achieving net-zero operational targets and are more willing to invest in high-performance insulation materials, resulting in growth in the domestic and international market for fiberglass, cellular glass, and foam-based pipe insulation solutions.

For instance, in April 2024, compliance requirements under the updated ASHRAE 90.1-2022 standard drove a 19% increase in pipe insulation product specifications for commercial HVAC piping systems across newly permitted construction projects in the United States, boosting demand for pre-formed fiberglass and elastomeric foam insulation products.

Pipe Insulation Market Size and Forecast:

-

Market Size in 2025: USD 9.44 billion

-

Market Size by 2035: USD 15.75 billion

-

CAGR: 5.25% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Pipe Insulation Market - Request Free Sample Report

Pipe Insulation Market Trends

-

Growing specification of pre-formed pipe insulation products across commercial HVAC and plumbing systems as contractors prioritize installation speed, dimensional consistency, and code-compliant thermal performance.

-

Increasing adoption of elastomeric foam insulation in refrigeration piping and chilled water systems driven by its closed-cell structure, low moisture vapor transmission rate, and suitability for below-ambient temperature applications.

-

Rising use of spray foam insulation for irregular pipe geometries and hard-to-access pipeline segments in industrial facilities where pre-formed sections cannot achieve seamless coverage.

-

Expanding procurement of pre-insulated pipe networks incorporating high-density polyurethane foam for district heating and cooling infrastructure projects across European and Asian smart city developments.

-

Strong demand from oil & gas refineries, petrochemical plants, and power generation facilities for high-temperature fiberglass and rock wool pipe insulation products rated for sustained operating temperatures above 500°C.

-

Growing enforcement of minimum insulation thickness requirements under ASHRAE 90.1, EN ISO 12241, and the EU Energy Performance of Buildings Directive pushing specification upgrades across new and existing mechanical piping systems.

-

Accelerated development of cellular glass pipe insulation products for cryogenic and sub-ambient piping in LNG terminals, cold storage warehouses, and pharmaceutical manufacturing environments where moisture ingress poses a direct process risk.

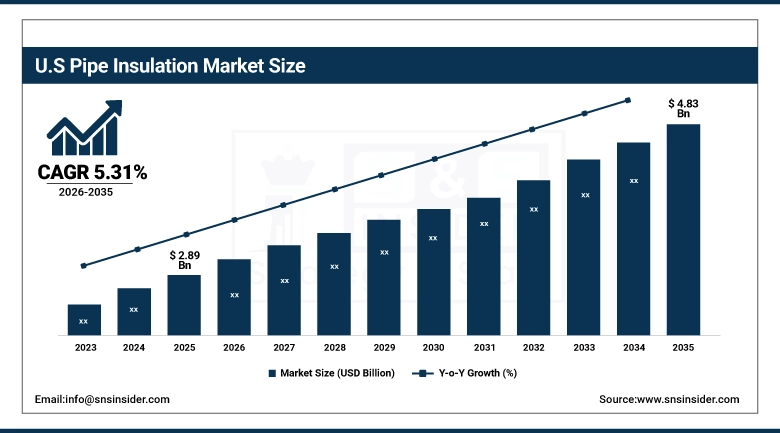

The U.S. Pipe Insulation Market was valued at USD 2.89 billion in 2025 and is expected to reach USD 4.83 billion by 2035, growing at a CAGR of 5.31% from 2026-2035. The United States represents the largest national market for pipe insulation products, primarily driven by the scale of its commercial construction sector, the geographic extent of oil and gas midstream pipeline infrastructure, and the mandatory energy efficiency retrofit requirements applicable to federally owned and financed buildings. Inflation Reduction Act tax incentives, high insurance penetration in industrial facilities, and increased capital allocation by mechanical contractors toward ASHRAE-compliant insulation upgrades help to drive growth in the market. Also, the U.S. is the largest national market in the world, due to the regulatory depth of its building energy codes and swift adoption of fiberglass and polyurethane foam-based pipe and mechanical insulation solutions.

Pipe Insulation Market Growth Drivers:

-

Tightening Building Energy Codes and Industrial Decarbonization Mandates are Driving the Pipe Insulation Market Growth

Tightening building energy codes and industrial decarbonization mandates take the center stage as a growth driver for the pipe insulation market share, and are driven by the implementation of ASHRAE 90.1-2022 compliance thresholds, Inflation Reduction Act energy efficiency provisions, and national net-zero emission targets compelling commercial building owners and industrial plant operators to invest in documented insulation performance upgrades. These requirements for thermal loss reduction across mechanical piping systems are driving the base of the market, the penetration of pre-formed and foam-based pipe insulation products, and adding to the overall market share globally.

For instance, in September 2024, updated industrial energy management requirements under ISO 50001 certification drove a ~23% increase in pipe insulation retrofit contracts across U.S. manufacturing facilities, with fiberglass and polyurethane foam insulation accounting for the majority of specified materials in audited energy improvement plans.

Pipe Insulation Market Restraints:

-

Volatile Petrochemical Feedstock Costs and Raw Material Price Instability are Hampering the Pipe Insulation Market Growth

Volatile petrochemical feedstock costs and raw material price instability of pipe insulation inputs also restrict the pipe insulation market growth, as a large share of polyurethane foam, polyisocyanurate, and elastomeric rubber compound costs moves directly with crude oil price cycles, exposing manufacturers to unpredictable margin compression and forcing procurement delays among cost-sensitive mechanical contractors. This results in specification downgrades, deferred retrofit projects, and reduced return on investment for insulation manufacturers in regions where project budgets are fixed at early design stages. As a result, market growth is stunted in price-sensitive construction segments and in regions where industrial maintenance spending is constrained by commodity revenue cycles.

Pipe Insulation Market Opportunities:

-

District Energy Network Expansion and Industrial Energy Audit Programs Create Future Growth Opportunities for the Pipe Insulation Market

The opportunity in district energy network expansion and industrial energy audit programs in the pipe insulation market is in the form of large-scale pre-insulated pipe procurement contracts, systematic insulation gap assessments in aging manufacturing facilities, and government-funded commercial building retrofit programs specifying minimum thermal resistance standards. These solutions provide for measurable energy loss reduction, compliance with increasingly stringent operational efficiency benchmarks, and real-time monitoring of insulation performance degradation. Through improved building energy ratings, industrial process efficiency gains, and regulatory compliance across sectors with chronic heat loss management needs, these programs improve lifecycle costs, reduce carbon reporting liabilities, and expand the market.

For instance, in June 2024, the European Commission reported that 76% of district energy operators across EU member states were actively procuring pre-insulated pipe systems with upgraded polyurethane foam cores, highlighting rising platform availability and increasing demand for thermally optimized pipe insulation products in urban energy infrastructure.

Pipe Insulation Market Segment Analysis

-

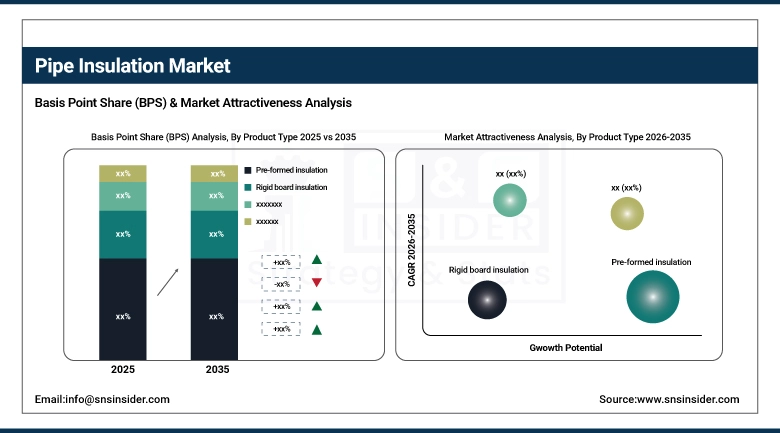

By product type, pre-formed insulation held the largest share of around 38.47% in 2025, and the spray foam insulation segment is expected to register the highest growth with a CAGR of 6.12%.

-

By material, the polyurethane & polyisocyanurate foam segment dominated the market with approximately 34.82% share in 2025, while the elastomeric foam segment is expected to register the highest growth with a CAGR of 6.38%.

-

By application, the industrial segment accounted for the leading share of nearly 47.63% in 2025, and the district energy system segment is expected to register the highest growth with a CAGR of 6.74%.

By Product Type, Pre-Formed Insulation Leads the Market, While Spray Foam Insulation Registers Fastest Growth

In 2025, the pre-formed insulation segment comprised the highest revenue share (38.47%) owing to its dimensional consistency for standard pipe diameters, faster field installation than cut-to-fit alternatives, and strong preference among mechanical contractors for ASHRAE-compliant commercial HVAC piping projects. Trends: Expansion of an exigency for with laboratory-certified thermal performance documenting for LEED & BREEM-rated building projects and increasing commercial building mechanical system retrofits On the other hand, spray foam insulation segment is projected to record the highest CAGR of nearly 6.12% over the 2026–2035 period, due to the high complexity of industrial pipeline configurations where pre-formed segments cannot offer seamless surface coverage, escalating use in underground pipeline thermal protection as well as growing utilization in offshore and marine piping applications. And the rise in demand for Corrosion-Inhibiting Spray Foam from petrochemical plant maintenance programs from new generations of industrial fittings, along with the technical preference for spray-applied closed-cell foam in CUI prevention applications, due to superior performance and long-term thermal cycling, is driving these trends.

By Material, the Polyurethane & Polyisocyanurate Foam Segment Dominates, while the Elastomeric Foam Segment Shows Rapid Growth

By 2025, the polyurethane & polyisocyanurate foam segment contributed the largest revenue share of 34.82% due to its low thermal conductivity values, high compressive strength, and broad applicability across district heating networks, industrial process piping, and commercial mechanical systems. Growing adoption of pre-insulated pipe systems in European district energy projects and continuous improvement of closed-cell foam thermal performance ratings are sustaining the material’s dominant market position. The elastomeric foam segment is projected to grow at the highest CAGR of about 6.38% between 2026 and 2035 due to the growing specification demand for closed-cell rubber insulation in chilled water systems, refrigeration piping, and food processing facilities. Some of the reasons include its zero-fiber composition preferred in clean manufacturing environments, superior moisture vapor resistance compared to fiberglass alternatives, and healthcare and pharmaceutical facility operators’ preference for antimicrobial-rated elastomeric foam products.

By Application, Industrial Leads, and District Energy System Registers Fastest Growth

The industrial segment accounted for the largest share of the pipe insulation market with about 47.63%, owing to the direct relationship between uninsulated process piping and measurable energy losses in oil & gas refineries, chemical processing plants, power generation facilities, and pharmaceutical manufacturing operations where heat conservation is a process-critical requirement. Reasons driving the industrial segment include increasing frequency of plant energy audits under ISO 50001 and aging pipe insulation replacement cycles in facilities built prior to current thermal performance standards. In addition, it is slated to grow at the fastest rate with a CAGR of around 6.74% throughout the forecast period of 2026–2035, as municipal energy authorities, real estate developers, and smart city planners accelerate the deployment of district heating and cooling networks whose operating economics depend directly on minimizing thermal losses across distribution pipe networks. Increased focus on urban carbon reduction targets and the proven lifecycle cost advantage of well-insulated district pipe systems over building-level HVAC drive continued investment.

Pipe Insulation Market Regional Highlights:

North America Pipe Insulation Market Insights:

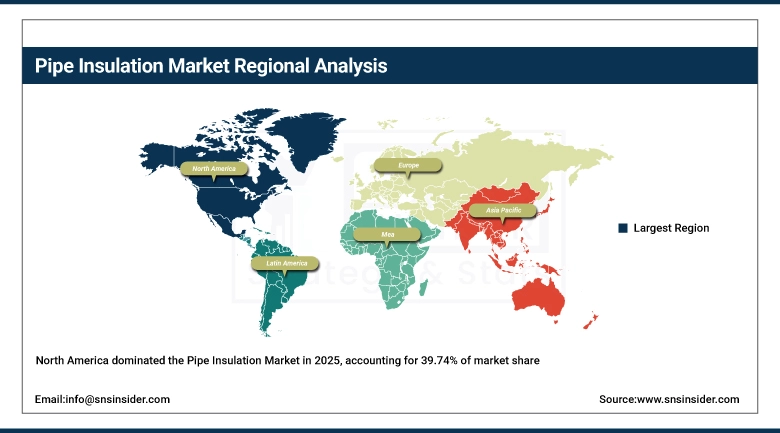

North America held the largest revenue share of over 39.74% in 2025 of the pipe insulation market due to a mature commercial construction sector, comprehensive enforcement of ASHRAE mechanical insulation requirements, and high industrial facility density generating consistent maintenance-driven demand for pipe insulation replacement products. Drivers include widespread EHR adoption of energy management certification, an established network of mechanical insulation contractors, growing data center construction requiring chilled water pipe insulation, and increased specification of fiberglass and polyurethane foam insulation products stemming from the Inflation Reduction Act’s building energy efficiency tax incentives. At the same time, federal infrastructure investment programs, mandatory building energy audit requirements, and capital allocation by large industrial operators toward pipe insulation upgrades are anchoring pipe insulation product and services demand in the market, and ensuring stable revenue streams across the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Pipe Insulation Market Insights:

Asia Pacific is the fastest-growing region in the pipe insulation market with a CAGR of 6.48%, as the volume of industrial construction, the pace of oil & gas infrastructure development, and the introduction of mandatory building energy efficiency codes in China, India, South Korea, and Southeast Asian markets are all growing. Factors including rapid urbanization, a rising volume of commercial construction requiring code-compliant mechanical insulation, and growing adoption of pre-insulated district cooling networks in Gulf and Southeast Asian smart city projects are stimulating the market growth. Government-backed energy efficiency programs and public-private infrastructure investment partnerships have been instrumental in raising pipe insulation specification standards, especially across newly commissioned industrial zones and large commercial developments. National procurement programs and government-funded building retrofit initiatives also help in advancing thermal insulation adoption and technical standards alignment with international codes. Increase in demand in Asia Pacific owing to rising industrial energy costs relative to historical levels and growing cost competitiveness of locally manufactured polyurethane foam and fiberglass pipe insulation products.

Europe Pipe Insulation Market Insights:

The pipe insulation market in Europe is the second-dominating region after North America on account of the EU Renovation Wave Strategy’s mandatory commercial building energy upgrade requirements, the rapid expansion of district heating networks in Germany, the Netherlands, Denmark, and Poland, and national net-zero building programs compelling specification upgrades across new and existing mechanical piping systems. Rising implementation of pre-insulated district pipe networks, advanced national building energy labeling programs, favorable EU Cohesion Fund allocations for building renovation, and cross-border district energy directives are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Pipe Insulation Market Insights:

In Latin America, and Middle East & Africa, the growing volume of oil & gas pipeline construction, expansion of petrochemical refining capacity in Brazil, Mexico, and GCC member states, and increasing mobile device penetration driving awareness of energy efficiency solutions support the pipe insulation market growth. The rising volume of district cooling procurement in UAE and Saudi Arabia smart city developments and growing adoption of pre-insulated pipe networks, along with public-sector energy cost reduction campaigns, will aid industrial and commercial pipe insulation adoption. The increasing scale of urban infrastructure investment and improving availability of locally distributed polyurethane foam and fiberglass insulation products in these regions are continuing to encourage market growth.

Pipe Insulation Market Competitive Landscape:

Owens Corning (est. 1938) is a global manufacturer of insulation, roofing, and composite materials with a broad portfolio of fiberglass pipe insulation products for commercial construction, industrial process, and HVAC applications. It uses its extensive North American and international manufacturing network and deep mechanical contractor relationships to maintain dominant specification share in commercial mechanical insulation across both new construction and retrofit project pipelines.

-

In March 2025, it extended its SOFTR® fiberglass pipe insulation product line with additional pipe diameter coverage and improved thermal resistance ratings targeting ASHRAE 90.1-2022 compliance, expanding product availability for commercial HVAC and plumbing piping specifications across its distributor network.

Armacell International S.A. (est. 1954) is the global leader in flexible elastomeric foam insulation materials, engineering foams, and technical nonwovens, and is the market leader in North America in the specification of its ArmaFlex® closed-cell foam pipe insulation for HVAC, refrigeration and chilled water piping applications worldwide. Strong competitive edge in mature commercial markets and high growth industrial and district cooling applications supported by continued R&D investment by the company into moisture vapor resistance formulations, fire rated product variants and sustainable foam chemistry.

-

In November 2024, Launched ArmaFlex® Ultima with a 30% reduction in thermal conductivity (relative to ArmaFlex®) and superior resistant to moisture vapor, aimed at chilled water and district cooling piping applications within high-humidity tropical key markets across Southeast Asia and the Middle East.

Rockwool International A/S (est. 1937) is a global leader in stone wool insulation with an industrial pipe insulation history serving petrochemical, marine, offshore and high-temperature process piping applications where fire protection, thermal stability over 500°C and acoustic performance are the conditions most often used to specify these materials. Company's established and lengthy relationships with EPC contractors and industrial facility operators throughout Europe, North America, and the Asia-Pacific region strengthens its competitive position in technologically challenging pipe insulation.

-

In January 2025, introduced an enhanced ProRox® pipe section series with improved compressive strength and an extended continuous operating temperature rating up to 750°C, targeting refinery scheduled turnaround projects and high-temperature steam distribution piping upgrades across European and Middle Eastern industrial markets.

Pipe Insulation Market Key Players:

-

Owens Corning

-

Armacell International S.A.

-

Rockwool International A/S

-

Knauf Insulation

-

Saint-Gobain (Isover)

-

Johns Manville (Berkshire Hathaway)

-

Kingspan Group plc

-

K-FLEX (L’Isolante K-Flex S.p.A.)

-

Cabot Corporation

-

Thermal Pipe Shields (TPS)

-

NMC S.A.

-

Aeroflex Industries

-

Thermaflex International

-

Rath Group

-

Wincell International

-

Kaimann GmbH

-

Steinbacher Insulation

-

Paroc Group

-

Megasorber Pty Ltd

-

Climatube (Logstor)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.44 billion |

| Market Size by 2035 | USD 15.75 billion |

| CAGR | CAGR of 5.25% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Pre-formed insulation, Rigid board insulation, Blanket insulation, Roll insulation, Spray Foam insulation, Others) •By Material (Cellular glass, Polyurethane & Polyisocyanurate Foam, Fiberglass, Elastomeric Foam, Water Rock Wool, Others) •By Application (Industrial, Building & Construction, District Energy System, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Owens Corning, Armacell International S.A., Rockwool International A/S, Knauf Insulation, Saint-Gobain (Isover), Johns Manville (Berkshire Hathaway), Kingspan Group plc, K-FLEX (L’Isolante K-Flex S.p.A.), Cabot Corporation, Thermal Pipe Shields (TPS), NMC S.A., Aeroflex Industries, Thermaflex International, Rath Group, Wincell International, Kaimann GmbH, Steinbacher Insulation, Paroc Group, Megasorber Pty Ltd. Climatube (Logstor), and Others. |

Frequently Asked Questions

Varying global regulations and certification standards limit expansion and slow new product launches in the pipe insulation market.

Key pipe insulation companies innovate with advanced materials like aerogel and elastomeric foams to strengthen market share.

North America leads with a 39.74% market share in the pipe insulation market.

Strict energy efficiency codes and rising retrofit demand significantly boost pipe insulation market growth worldwide.

The pipe insulation market size is USD 9.44 billion in 2025 and is expected to reach USD 15.75 billion by 2035.

Get in Touch