Coating Additives Market Report Scope & Overview:

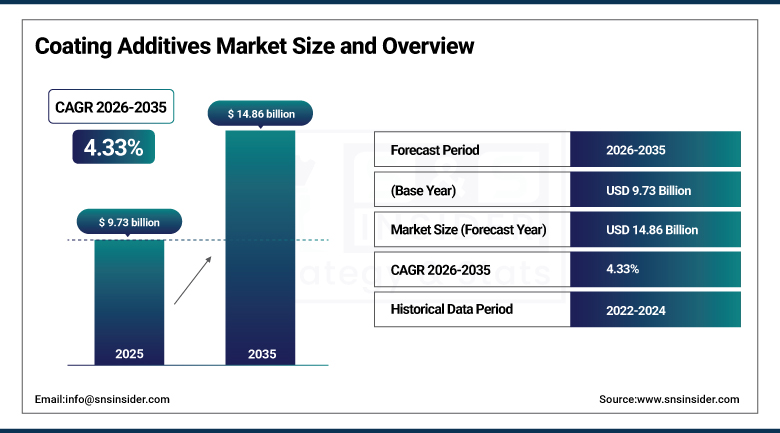

The Coating Additives Market was valued at USD 9.73 Billion in 2025 and is expected to reach USD 14.86 Billion by 2035, growing at a CAGR of 4.33% from 2026–2035.

The global coating additives market is experiencing significant expansion, fueled by growing demand in construction, automotive, and industrial applications. Coating additives are specialty chemical compounds added to paints, varnishes, lacquers, and protective coatings to modify or improve their performance, application properties, and final film characteristics, encompassing rheology modifiers, wetting and dispersing agents, defamers, biocides, levelling agents, and UV stabilizers. Stricter environmental regulations from agencies like the EPA and ECHA are prompting innovation in eco-friendly and low-VOC solutions, particularly in waterborne and powder coatings. Urbanization and infrastructure development are boosting architectural coatings, while the automotive sector is embracing self-healing and anti-corrosion coatings with nano-additives.

In March 2024, BASF introduced bio-based coating additives to enhance sustainability and performance, expanding its Ultradisperse and Larostat coating additive portfolio with renewably sourced raw material variants that deliver equivalent dispersing and anti-static performance to petroleum-derived alternatives. The bio-based product launches reflect BASF’s commercial response to customer sustainability procurement programmes whose bio-based content specification creates premium pricing opportunity that sustains R&D investment in renewable coating additive chemistry.

Market Size and Forecast

-

Market Size in 2026E: USD 10.15 Billion

-

Market Size by 2035: USD 14.86 Billion

-

CAGR: 4.33% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Coating Additives Market - Request Free Sample Report

Coating Additives Market Trends

-

Waterborne coating additive innovation is gaining traction as VOC regulations drive demand for environmentally compliant dispersants, rheology modifiers, and defoamers.

-

Nano-additives such as graphene, nano-silica, and nano-clay are enhancing coating performance through improved barrier properties, scratch resistance, and corrosion protection.

-

Self-healing coating additives are emerging in premium applications by enabling automatic repair of minor surface damage and extending coating lifespan.

-

Bio-based coating additives derived from renewable feedstocks are witnessing increased adoption due to sustainability goals and lower carbon footprints.

-

Powder coating additive advancements are supporting high-performance, zero-VOC coating solutions for industrial, automotive, and furniture applications.

The U.S. Coating Additives Market Outlook

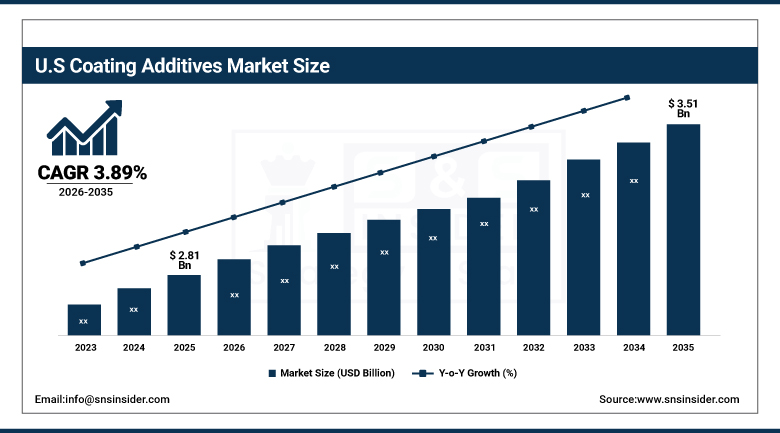

The U.S. Coating Additives Market was valued at USD 2.81 Billion in 2025 and is expected to reach USD 3.51 Billion by 2035, growing at a CAGR of 3.89%. The U.S. is the most commercially significant coating additives market within North America. Dow Chemical, BASF Corporation, Evonik Industries, Arkema, and Ashland collectively define the domestic coating additives commercial landscape. EPA’s VOC emission limits for architectural, industrial maintenance, and automotive refinish coatings create compliance investment motivation that drives waterborne and low-VOC additive adoption. The American Coatings Association’s documentation of rising adoption of low-VOC solutions and the construction sector’s architectural coating demand collectively sustain U.S. market growth.

Evonik Industries expanded its TEGO coating additives portfolio in 2024 with new waterborne wetting agents and flow additives specifically designed for high-solids and 100% solid UV-curable coating formulations, targeting the industrial wood, metal, and automotive refinish markets’ low-VOC transition whose performance requirement creates premium additive specification motivation. The portfolio expansion reflects TEGO’s commercial response to the North American coating industry’s progressive migration toward waterborne and radiation-curable coating formulations whose additive requirement differs fundamentally from conventional solvent-borne alternatives.

Coating Additives Market Segment Analysis

-

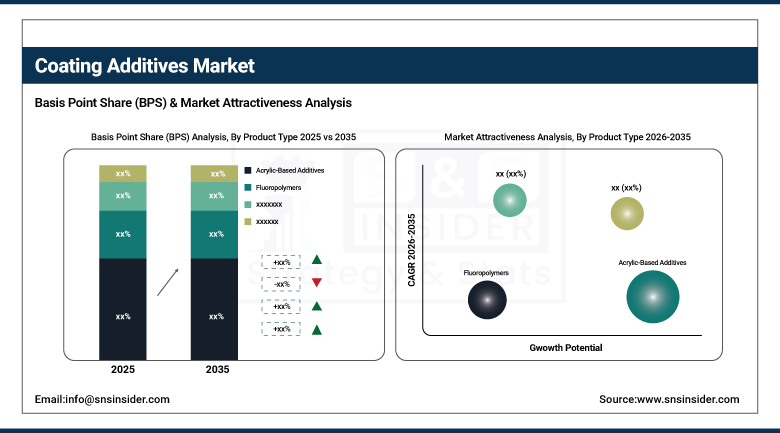

By Product Type, acrylic-based additives segment dominated the coating additives market with 38.5% share in 2025, while the fluoropolymers segment is the fastest growing.

-

By Application, rheology modification segment dominated the coating additives market with 32.8% share in 2025, while the wetting & dispersion segment is the fastest growing.

-

By End-Use Industry, architectural segment dominated the coating additives market, while the automotive segment is the fastest growing.

-

By Formulation, waterborne coatings segment dominated the coating additives market with the highest share in 2025, while the powder coatings segment is the fastest growing.

By Product Type, acrylic dominates, fluoropolymers grow fastest

Acrylic-based additives retained the dominant product position with 38.5% of the coating additives market in 2025. Acrylic additives’ commercial primacy reflects their exceptional versatility across the broadest range of coating formulations whose adhesion improvement, UV resistance, and compatibility with waterborne systems create specification preference in architectural, automotive, and industrial applications. Each architectural paint formulation that specifies acrylic dispersant, rheology modifier, or levelling agent creates procurement whose aggregate across the global architectural coating industry’s production volume creates commercial scale. The acrylic additive’s water-compatibility creates particular value in the waterborne coating transition whose low-VOC compliance creates progressive specification preference over solvent-borne alternatives.

Fluoropolymers are the fastest-growing product type because the aerospace industry’s chemical resistance requirement, industrial maintenance’s extreme environment durability demand, and premium architectural coating’s dirt-resistance specification create above-average fluoropolymer additive procurement. PTFE, PVDF, and fluoroethylene-vinyl ether copolymer additives’ unique chemical inertness and low surface energy create coating performance advantages that no other additive chemistry can replicate equivalently.

By Application, rheology modification dominates, wetting & dispersion grows fastest

Rheology modification retained the dominant application position with 32.8% of the coating additives market in 2025. Rheology modifier’s commercial primacy reflects its essential role in every coating formulation whose viscosity control, sag prevention, and levelling optimization create the process ability foundation that transforms raw coating ingredients into applicator-ready products. Each architectural paint whose brush, roller, or spray application characteristic creates viscosity specification creates rheology modifier procurement whose aggregate across the global coating industry’s extraordinary production volume creates commercial scale. HEUR, HASE, cellulose ether, and polyurethane associative thickener’s combined portfolio creates rheology solution breadth that sustains the application’s dominant commercial position.

Wetting and dispersing additives are the fastest-growing application because waterborne coating formulation’s pigment wetting challenge, nano-additive integration’s dispersion requirement, and sustainability-aligned waterborne coating transition create growing demand for premium dispersant technology. Each new waterborne coating formulation that specifies a wetting agent for substrate adhesion and a dispersant for pigment stability creates procurement whose technical requirement creates above-commodity commercial relationships with specialized dispersant chemistry providers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Coating Additives Market Insights

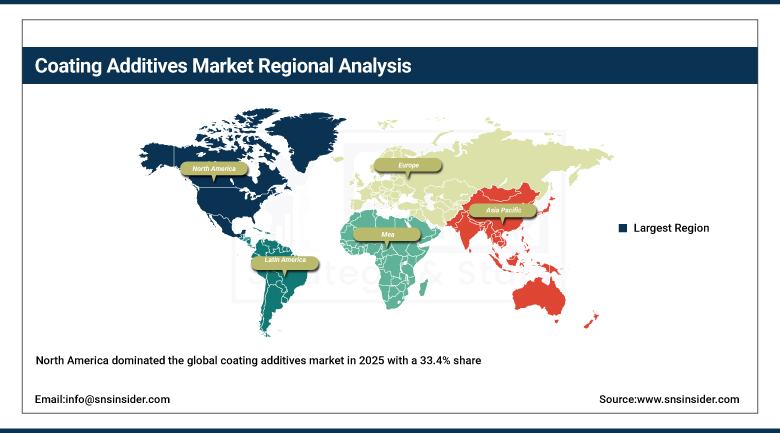

North America dominated the global coating additives market in 2025 with a 33.4% share, driven by strict environmental regulations, strong industrial demand, and the concentration of major coating additive manufacturers. The United States accounts for approximately 87.4% of North American revenues through Dow Chemical, BASF Corporation, Evonik, Arkema, and Ashland’s commercial operations sustained by EPA regulatory compliance creating non-discretionary waterborne additive adoption.

Canada contributes approximately 12.6% of North American revenues through its construction sector’s architectural coating demand, the automotive manufacturing sector’s coating specification, and the industrial maintenance coating market’s additive procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Coating Additives Market Insights

Europe is a technically sophisticated coating additives market where REACH regulation’s hazardous substance restriction, EU Paints Directive’s VOC limit, and BASF’s and Evonik’s German commercial leadership create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive OEM coating programme, the industrial maintenance sector’s corrosion protection investment, and BASF’s Ludwigshafen operations.

France, Italy, and the United Kingdom are significant secondary markets where architectural coating’s sustainability specification, automotive refinish, and industrial coating create consistent coating additive procurement.

Asia Pacific Coating Additives Market Insights

Asia Pacific is the fastest-growing regional coating additives market, driven by China’s extraordinary construction and automotive sectors, India’s rapidly growing infrastructure investment, Japan’s advanced industrial coating technology, and Southeast Asia’s expanding manufacturing base. China accounts for approximately 44.8% of Asia Pacific revenues through its world-leading architectural coating production, the automotive industry’s coating specification, and the progressive environmental regulation’s waterborne coating transition.

India’s infrastructure investment creating architectural coating demand, Japan’s advanced automotive and industrial coating technology, and South Korea’s electronics and automotive sectors create significant secondary markets.

MEA & Latin America Coating Additives Market Insights

Saudi Arabia leads MEA revenues through its extraordinary construction investment, NEOM and Vision 2030 infrastructure programme’s architectural coating demand, and the petrochemical sector’s industrial coating procurement. Brazil leads Latin American revenues through its construction sector’s architectural coating demand, the automotive manufacturing industry’s coating specification, and the industrial maintenance market’s corrosion protection investment.

Market Dynamics

Growth Drivers: EPA and ECHA environmental regulation driving low-VOC innovation and construction sector architectural coating demand

Stricter environmental regulations from agencies like the EPA and ECHA prompting innovation in eco-friendly and low-VOC solutions is the coating additives market’s most commercially transformative regulatory growth driver. The EPA’s architectural coating VOC standard creates compliance timeline whose systematic industry transition from solvent-borne to waterborne creates new waterborne additive formulation requirement whose technical complexity sustains premium commercial relationships with specialized additive chemistry providers. Each coating manufacturer’s waterborne reformulation programme creates additive specification that sustains R&D investment in waterborne-compatible rheology modifier, dispersant, and defoamer technology.

Urbanization and infrastructure development boosting architectural coatings is the market’s most commercially certain volume demand driver. The global construction sector’s annual output of USD 15+ trillion creates proportional architectural coating demand whose additive component sustains consistent market procurement. Each emerging market’s urbanization programme that creates new residential and commercial construction creates first-time architectural coating adoption that compounds with the global construction industry’s extraordinary scale.

Restraints: Raw material price volatility and compliance cost burden for smaller coating manufacturers

Coating additive raw material price volatility, driven by crude oil and petrochemical feedstock cycles affecting acrylic monomer, polyurethane intermediate, and fluoropolymer resin pricing, creates production cost uncertainty that limits additive manufacturer pricing predictability. Each raw material price spike creates coating additive cost pressure whose downstream impact on coating formulation cost creates procurement substitution motivation that moderates premium additive adoption.

Environmental regulation compliance investment, whose waterborne reformulation programme creates substantial R&D and process capital expenditure, creates competitive barrier for smaller coating manufacturers whose limited reformulation budget creates specification inertia that moderates market growth below the regulatory timeline’s technically available adoption opportunity.

Opportunities: Bio-based sustainable coating additives and nano-additive premium technology

Bio-based coating additive development from renewable feedstocks represents the most commercially differentiated innovation direction whose lifecycle carbon footprint advantage creates premium specification motivation in ESG-committed procurement programmes. Each bio-based coating additive that achieves performance parity with petroleum-derived alternatives at commercially accessible premium creates adoption momentum that compounds with corporate sustainability programme expansion.

Nano-additive technology’s integration into premium coating formulations creates the most commercially premium coating additive category whose graphene, nano-silica, and nano-clay’s extraordinary performance improvement creates above-commodity pricing that sustains innovation investment.

Recent Developments:

-

2024: BASF introduced bio-based coating additives in March 2024 to enhance sustainability and performance, expanding its Ultradisperse and Larostat portfolio with renewably sourced raw material variants delivering equivalent dispersing and anti-static performance to petroleum-derived alternatives.

-

2024: Evonik Industries expanded its TEGO coating additives portfolio in 2024 with new waterborne wetting agents and flow additives for high-solids and UV-curable coating formulations targeting industrial wood, metal, and automotive refinish markets’ low-VOC transition.

-

2024: Arkema expanded its Sartomer UV-curable coating additives division in 2024 with new bio-acrylate monomers and oligomers for radiation-curable coating formulations whose 100% solids, zero-VOC emission profile creates compliance advantage in industrial and architectural zero-emission coating applications.

Coating Additives Market Key Players are:

-

BASF SE

-

Evonik Industries AG (TEGO Coating Additives)

-

Dow Chemical Company

-

Arkema S.A. (Sartomer/Bostik)

-

Ashland Global Holdings Inc.

-

Clariant AG

-

Elementis PLC

-

Nuplex Industries Ltd. (Allnex)

-

BYK-Chemie GmbH (ALTANA AG)

-

Solvay S.A.

-

Munzing Chemie GmbH

-

Cabot Corporation

-

Wacker Chemie AG

-

Momentive Performance Materials Inc.

-

Azelis Group N.V.

-

Estron Chemical Inc.

-

Omnova Solutions Inc. (Synthomer)

-

Siltech Corporation

-

Harmony Additive Pvt. Ltd.

-

Michelman Inc.

Coating Additives Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.73 Billion |

| Market Size by 2035 | USD 14.86 Billion |

| CAGR | CAGR of 4.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Acrylic-Based Additives, Fluoropolymers, Urethane-Based Additives, Metallic Additives, Silicone-Based Additives, Others) • By Application (Rheology Modification, Wetting & Dispersion, Anti-Foaming, Biocides/Antimicrobials, Levelling & Flow Control, Impact Modification, Others) • By Formulation (Waterborne Coatings, Solvent-Borne Coatings, Powder Coatings, Radiation-Curable/UV-Cured Coatings) • By End-Use Industry (Architectural, Automotive, Industrial, Wood & Furniture, Marine, Aerospace, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Evonik Industries AG (TEGO Coating Additives), Dow Chemical Company, Arkema S.A. (Sartomer/Bostik), Ashland Global Holdings Inc., Clariant AG, Elementis PLC, Nuplex Industries Ltd. (Allnex), BYK-Chemie GmbH (ALTANA AG), Solvay S.A., Munzing Chemie GmbH, Cabot Corporation, Wacker Chemie AG, Momentive Performance Materials Inc., Azelis Group N.V., Estron Chemical Inc., Omnova Solutions Inc. (Synthomer), Siltech Corporation, Harmony Additive Pvt. Ltd., and Michelman Inc. |

Frequently Asked Questions

The Coating Additives Market is expected to grow at a CAGR of 4.33% from 2026 to 2035.

The Coating Additives Market was valued at USD 9.73 Billion in 2025.

Stricter environmental regulations from EPA and ECHA prompting innovation in eco-friendly and low-VOC solutions, particularly in waterborne and powder coatings, alongside growing demand from construction, automotive, and industrial applications.

Acrylic-Based Additives dominated the Coating Additives Market with 38.5% share in 2025.

North America dominated the global coating additives market in 2025 with a 33.4% share.

Get in Touch