Flow Meter Market Report Scope & Overview:

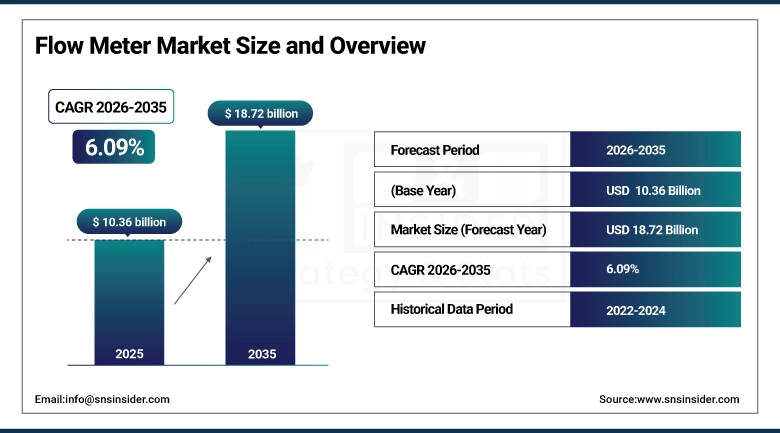

The Flow Meter Market was estimated at USD 10.36 Billion in 2025 and is expected to reach USD 18.72 Billion by 2035 and grow at a CAGR of 6.09% over the forecast period of 2026-2035.

The Growth of the Flow Meter Market can be attributed to the increasing automation in various industries, increasing need for precise measurements of fluids, and investment in water and wastewater treatment, oil and gas, chemicals, and power generation sectors. The adoption of smart meters, industry 4.0 technology, and stringent regulation of processes and resource management systems has propelled the growth of the market.

The International Energy Agency's energy sector data documents that global primary energy consumption grew 2.1% in the most recently reported year, sustaining demand for the fuel gas, liquid petroleum, and steam flow measurement infrastructure that energy production and distribution require.

Market Size and Forecast

-

Market Size in 2025: USD 10.36 Billion

-

Market Size by 2035: USD 18.72 Billion

-

CAGR: 6.09% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Flow Meter Market - Request Free Sample Report

Flow Meter Market Trends

-

Smart flow meter adoption where meters with integral microprocessors, wireless communication, and on-board diagnostics transmit flow data, diagnostic alerts, and calibration status to plant SCADA and cloud analytics platforms is replacing conventional analog output meters in industrial process automation upgrade programs.

-

IoT-connected water utility meter networks where residential and commercial water meters with low-power wireless communication transmit consumption data continuously to utility billing systems are replacing manual-read meters in smart metering rollout programs globally.

-

Hydrogen flow measurement development where calibrated flow meters for gaseous and liquid hydrogen are required for the emerging hydrogen economy's production, distribution, and dispensing infrastructure is creating a new specialty flow measurement market segment whose growth tracks hydrogen infrastructure investment.

-

Non-invasive clamp-on ultrasonic flow meters are expanding from their traditional large-bore pipe maintenance and troubleshooting applications into permanent installation monitoring roles where their installation without process interruption creates application advantages in high-availability process environments.

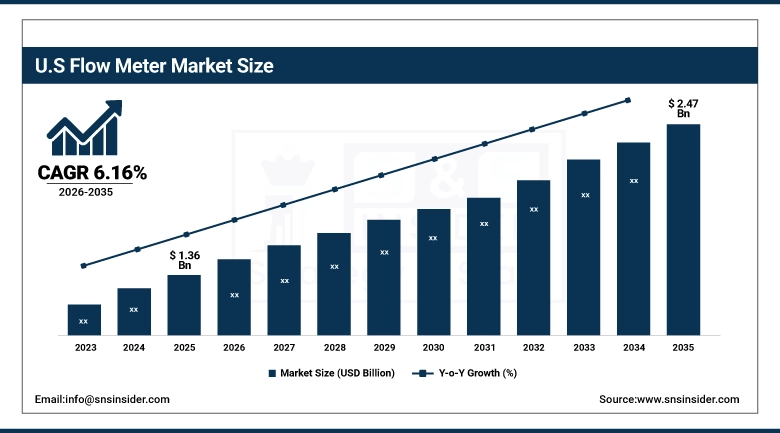

The U.S. Flow Meter Market was valued at USD 1.36 billion in 2025 and is expected to reach USD 2.47 billion by 2035, growing at a CAGR of 6.16%.

The Growth of the U.S. Flow Meter Market can be attributed to the increasing investment in water infrastructure, shale oil and gas production, and industrial automation in manufacturing industries. The increased adoption of smart meters, stringent environmental regulation, and the need for accurate monitoring of energy and chemical industries' processes has fueled the growth of the market.

The U.S. Geological Survey's water use data documents that the United States withdraws approximately 322 billion gallons per day from surface and ground water sources for agricultural, industrial, and municipal purposes sustaining flow measurement infrastructure investment across every water use sector.

Flow Meter Market Segment Analysis

-

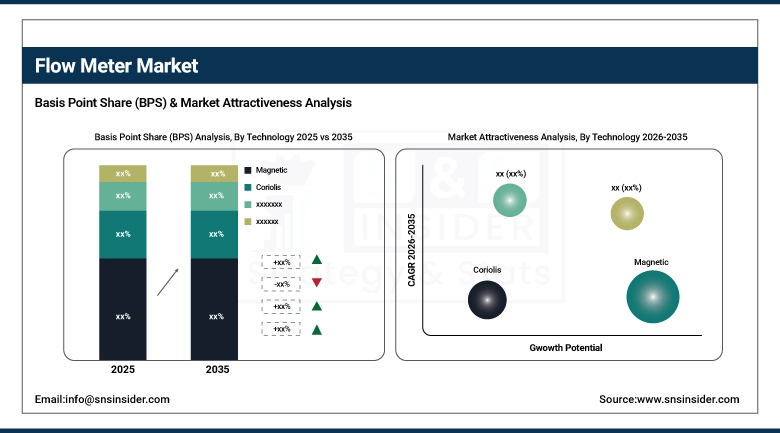

By Technology, Magnetic dominated with ~32% share in 2025; Ultrasonic growing at the fastest CAGR.

-

By Power Source, Battery-Powered dominated with ~48% share in 2025 due to remote installation advantages.

-

By End-Use Industry, Power Generation dominated with ~34% share in 2025; Water & Wastewater and Oil & Gas significant.

By Technology: Magnetic dominates at 32%, Ultrasonic fastest CAGR

Magnetic Flow Meters held approximately 32% of the Flow Meter Market in 2025, reflecting their dominant position across the large volume applications water treatment, chemical processing, food and beverage, and wastewater where the measurement of conductive fluid volume flow in pipelines requires the accuracy, low maintenance, and non-intrusive measurement that electromagnetic flow meters provide without moving parts, pressure drop, or calibration-affecting deposits. Magnetic meters' advantages zero pressure drop, self-cleaning design compatible with slurry service, and bidirectional measurement in a single instrument sustain their specification across municipal water systems, mining slurry pipelines, and food processing applications where alternative meter technologies create operational disadvantages. Ultrasonic Flow Meters are growing at the fastest technology CAGR, driven by the expanding adoption of clamp-on ultrasonic meters for non-invasive flow measurement where the ability to install transit-time ultrasonic transducers on the external surface of existing pipes without shutting down the process creates retrofit measurement access in operating plants where inline meter installation would require process interruption.

By Power Source: Battery-Powered dominant, Wired growing for smart integration

Battery-Powered flow meters held approximately 48% of the Flow Meter Market in 2025, reflecting the large population of remote metering applications remote wellhead production monitoring, distribution pipeline monitoring, isolated water supply systems where the absence of AC power makes battery operation essential. Battery-powered meters' adoption has grown with battery technology improvement where lithium thionyl chloride cells sustaining 10-15 year operational life eliminate the maintenance cost of battery replacement that sustained preference for wired power in remote applications and wireless communication integration whose low power consumption is compatible with battery-only power budgets.

By End-Use: Power Generation dominant, all sectors significant

Power Generation held approximately 34% of the Flow Meter Market in 2025, reflecting the measurement-intensive nature of power plant operation where every fuel, steam, water, and cooling fluid stream requires continuous flow measurement for energy balance calculation, efficiency optimization, and regulatory emission reporting. Coal, natural gas, nuclear, and renewable power plants each sustain comprehensive flow measurement programs that create per-plant instrument populations whose aggregate represents the largest single end-use segment. Water and Wastewater is a large and growing end-use where both the enormous global volume of treated water distribution and the progressive smart meter rollout in water utilities are sustaining consistent growth. Oil and Gas sustains significant market share through its custody transfer measurement precision requirements and the ongoing investment in new production, processing, and distribution infrastructure.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

86% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

Saudi Arabia |

42% |

|

Latin America |

Brazil |

50% |

North America Flow Meter Market Insights

North America holds a substantial Flow Meter Market position driven by the United States' dominant oil and gas, power generation, and water treatment industries. The U.S. EPA's effluent monitoring requirements which mandate continuous flow measurement at industrial wastewater discharge points sustain regulatory-driven flow meter procurement across the manufacturing sector. The shale oil and gas production renaissance where unconventional well production requires wellhead measurement and gathering pipeline flow monitoring creates ongoing flow meter procurement that sustains U.S. oil and gas flow measurement market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Flow Meter Market Insights

Europe's Flow Meter Market is driven by the EU's regulatory environment — including the Industrial Emissions Directive's continuous measurement requirements for flow-dependent emission calculations, the Water Framework Directive's water use monitoring requirements, and the Renewable Energy Directive's energy measurement requirements for renewable heat metering that creates compliance-driven flow meter procurement across European industry. Germany's process industry leadership where BASF, Bayer, and LANXESS operate the world's most sophisticated chemical production complexes sustains Germany's position as Europe's largest flow measurement market by industrial consumption.

Asia Pacific Flow Meter Market Insights

Asia Pacific is the fastest-growing regional Flow Meter Market, driven by China's massive industrial investment whose continued expansion of chemical, petrochemical, power generation, and water treatment capacity creates new flow meter installation demand at the world's highest pace of industrial capital deployment India's growing industrial infrastructure, and the region's water utility smart meter rollout programs. China's domestic flow meter manufacturers including Endress+Hauser China operations, Yokogawa China, and domestic producers including Guanghua Measurement sustain a competitive domestic market whose pricing sustains adoption across China's price-sensitive mid-tier industrial customers.

MEA and Latin America Flow Meter Market Insights

The Middle East's Flow Meter Market is growing with the Gulf states' oil and gas infrastructure where Saudi Aramco, ADNOC, and Kuwait Oil Company each operate some of the world's largest single-site flow measurement networks at their production, processing, and export facilities and the region's ambitious water infrastructure investment in desalination and distribution. Latin America's market concentrates in Brazil's oil production from the subsalt offshore fields where precision multiphase flow metering at wellheads sustains specialist flow meter procurement and the region's water utility infrastructure expansion.

Flow Meter Market Growth Drivers:

-

Industrial automation and water infrastructure investment driving sustained flow meter market growth globally

Both industrial automation and investments in water infrastructure are spurring on the growth of the Flow Meter Market in terms of value and volume due to the increasing need for measuring fluid flow rates accurately and in real time to ensure efficient operations, reduced energy consumption, and compliance with regulations. The rising deployment of process control automation in industries such as oil & gas, chemicals, power generation, food & beverages, and pharmaceuticals is boosting the demand for sophisticated flow meters. At the same time, growing investments in water and wastewater infrastructure are driving up the demand for flow meters.

Flow Meter Market Restraints:

-

High replacement costs and installation disruption creating flow meter market adoption challenges in retrofit applications globally

The flow meter market's growth is constrained by the installation cost of inline meter types where replacing an existing flow meter in an operating pipeline requires process shutdown, pipe cutting, and flange installation that generates labor cost and production loss disproportionate to the meter's hardware cost creating lifecycle replacement resistance that sustains aging meter fleets beyond their optimal service lives. The cost of calibration and maintenance required to sustain measurement accuracy over 10-20 year service lives creates total cost of ownership considerations that influence initial meter selection toward the lowest-maintenance alternatives.

Flow Meter Market Opportunities:

-

Hydrogen infrastructure metering and smart water network integration creating significant flow meter market growth opportunities globally

Hydrogen flow measurement represents the flow meter market's most commercially novel emerging application where the planned construction of hydrogen production, distribution, and dispensing infrastructure creates new meter installation demand for a fluid whose measurement challenges differ fundamentally from conventional process fluids. Hydrogen's extremely low molecular weight, high diffusivity, and wide flammability range create measurement constraints that existing flow meter technologies must overcome through specific adaptations creating development investment opportunity for meter manufacturers who establish technical leadership in hydrogen measurement. Smart water network integration where flow meters with cellular or LPWAN wireless communication continuously transmit consumption and pressure data to utility analytics platforms is creating value-added digital service revenue above hardware procurement for meter manufacturers who develop data platform capabilities.

Recent Developments:

-

2026: Endress+Hauser launched the Proline Promag W 400 electromagnetic flow meter achieving IP69 full submersibility for installation in flood-prone locations, Bluetooth commissioning via the SmartBlue app, and integrated self-diagnostics detecting liner abrasion, electrode coating, and ground fault conditions with NB-IoT wireless communication enabling autonomous data transmission in smart water network applications without requiring site power infrastructure, reporting deployment in 200 smart water district metering area pilots across 15 countries in its first year of availability.

-

2025: Emerson Electric launched the Micro Motion G-Series Coriolis flow meter the first Coriolis meter achieving OIML R117 custody transfer accuracy certification for liquid hydrogen measurement enabling custody transfer billing of liquid hydrogen at LH2 fueling stations and hydrogen production facility loading terminals, completing the metrological validation framework required for commercial hydrogen market custody transfer measurement that previous-generation Coriolis meters' test limitations at hydrogen's cryogenic operating temperatures could not satisfy.

Flow Meter Market Key Players

-

Emerson Electric Co. (Micro Motion, Rosemount)

-

Endress+Hauser Group

-

ABB Ltd.

-

Yokogawa Electric Corporation

-

Honeywell International Inc.

-

Siemens AG (SITRANS)

-

KROHNE Group

-

Badger Meter Inc.

-

Brooks Instrument (Emerson)

-

Roper Technologies Inc.

-

Omega Engineering Inc. (Spectris)

-

Azbil Corporation

-

Magnetrol International Inc.

-

Kobold Instruments Inc.

-

Sierra Instruments Inc.

-

Bronkhorst High-Tech BV

-

Spirax Sarco Engineering plc

-

McCrometer Inc.

-

Keyence Corporation

-

GE Sensing & Inspection Technologies

Flow Meter Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.36 Billion |

| Market Size by 2035 | USD 18.72 Billion |

| CAGR | CAGR of 6.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Magnetic, Coriolis, Ultrasonic, Differential Pressure, Positive Displacement, Vortex, Others) • By Power Source (Battery-Powered, Wired/Externally Powered) • By End-Use Industry (Power Generation, Oil & Gas, Water & Wastewater, Chemical, Food & Beverage, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Emerson Electric Co. (Micro Motion, Rosemount); Endress+Hauser Group; ABB Ltd.; Yokogawa Electric Corporation; Honeywell International Inc.; Siemens AG (SITRANS); KROHNE Group; Badger Meter Inc.; Brooks Instrument (Emerson); Roper Technologies Inc.; Omega Engineering Inc. (Spectris); Azbil Corporation; Magnetrol International Inc.; Kobold Instruments Inc.; Sierra Instruments Inc.; Bronkhorst High-Tech BV; Spirax Sarco Engineering plc; McCrometer Inc.; Keyence Corporation; GE Sensing & Inspection Technologies. |

Frequently Asked Questions

Ans: The Flow Meter Market was valued at USD 10.36 billion in 2025.

Ans: Power Generation dominated with approximately 34% share; Water & Wastewater and Oil & Gas also significant.

Ans: Battery-Powered dominated with approximately 48% share in 2025.

Ans: Magnetic flow meters dominated with approximately 32% share; Ultrasonic is growing at the fastest CAGR.

Ans: The Flow Meter Market is expected to grow at a CAGR of 6.09% from 2026 to 2035.

Get in Touch