Copper Tubes Market Report Scope & Overview:

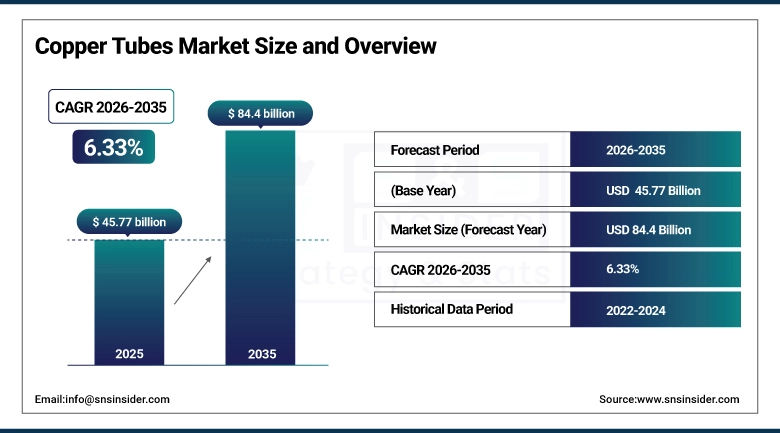

The Copper Tubes Market was valued at USD 45.77 billion in 2025 and is expected to reach USD 84.4 billion by 2035, growing at a CAGR of 6.33% from 2026–2035.

The Copper tubes are an indispensable industry and construction section material for heating, ventilation, air circulation refrigeration, plumbing system structure and medical gas delivery methods. Naturally Copper is already suited for these applications it has very good thermal conductivity, making it excellent for heat exchanging purposes, together with a high corrosion resistance and finally, after the USD 40 million research carried out by 'Antimicrobial copper project' company suggests that metals like copper are among a few alloys known as this type of material. Market Dynamics Construction activity drives the HVAC demand, especially in warming climates which is fuelling the overall market. Although copper prices are rising, and competing materials such as plastic are undercutting its market share in some applications, the intrinsic performance advantages that copper has over competing materials means there will always be a pivotal place for it to play.

The thermal conductivity of copper is 30 times greater than stainless steel and about 700 times that of common plastic piping. The tremendous thermal conductivity lead copper tubes to out perform everything else in heat transfer applications such as HVAC and refrigeration in the systems for which thermal efficiency is the important design criteria.

This warming trend is in turn feeding into structural demand for copper tubes, as air conditioning demand increases globally; including the emerging economies of South and South-East Asia where rising-income levels allow mass market uptake of wholesale residential and commercial cooling systems for the first time.

Market Size and Forecast:

-

Market Size in 2025: USD 45.77 Billion

-

Market Size by 2035: USD 84.4 Billion

-

CAGR: 6.33% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Copper Tubes Market - Request Free Sample Report

Copper Tubes Market Trends:

-

Global warming and rising temperatures in previously cool regions are driving first-time air conditioning adoption that creates strong new demand for refrigerant copper tubes.

-

Heat pump adoption for space heating is accelerating as governments subsidize electric heating alternatives, driving demand for high-efficiency copper refrigerant circuits.

-

Construction activity in Asia Pacific, particularly India and Southeast Asia, is a primary driver of copper tube demand for plumbing and HVAC applications.

-

Medical gas distribution systems in hospitals require copper tubes for oxygen and other medical gases, growing with hospital construction.

-

Copper tube manufacturers are developing thinner-walled, higher-strength products that reduce material use while maintaining performance.

-

The transition to low-GWP refrigerants requires compatible copper tube specifications, creating product development opportunities.

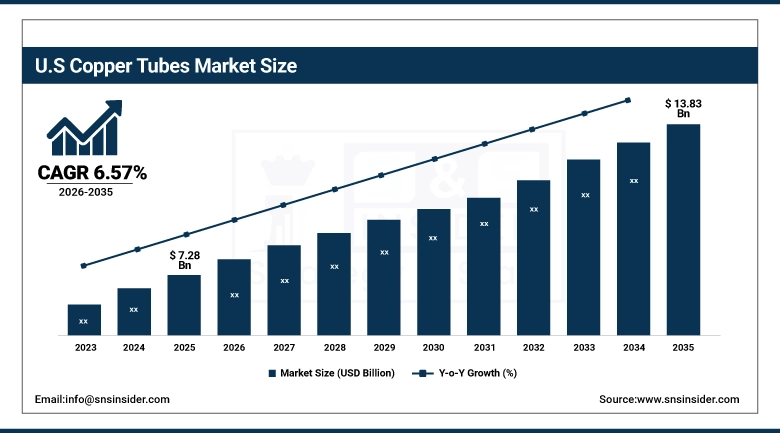

U.S. Copper Tubes Market was valued at USD 7.28 billion in 2025 and is expected to reach USD 13.83 billion by 2035, growing at a CAGR of 6.57% from 2026 to 2035.

The USA is one of the largest markets worldwide for Copper Tubes American demand is dictated by the booming HVAC and refrigeration market, active construction sector, as well as plumbing applications in both new builds and renovations. Part of the momentum relates to the move toward higher-efficiency HVAC systems driven in part by federal efficiency standards as well as incentives for heat pumps arising from the Inflation Reduction Act, which is in turn driving demand for superior quality copper tube components that enable this shift of using electricity-powered heating instead of natural gas.

Public buildings, school systems and municipal facilities will be renewed with the support of U.S. $1 trillion Infrastructure Investment and Jobs Act funding that supports much more than just infrastructure improvements but includes HVAC upgrades and plumbing system replacement that will translate into rivets of copper tube over the next 10 years.

Copper Tubes Market Segment Insights:

-

Based on Type, Coils dominated the copper tubes market in 2025,; Straight lengths are preferred for plumbing.

-

Based on Thickness, Standard Gauge accounted for the largest market share due to widespread use in plumbing and HVAC systems; Capillary Tubes are witnessing faster growth driven by refrigeration and precision industrial applications.

-

Based on Application, HVAC & Refrigeration is the largest end-use segment; Medical Gas applications are growing with hospital construction.

Copper Tubes Market Segment Analysis:

By Type, Coils Lead for HVAC, Straight for Plumbing

The primary product form in the market is coiled copper tube, which refers to a long continuous length of material that can be shaped into the form of a coil and cut into shorter sections. Coils allow for complex heat exchanger geometries to be manufactured because it allows the ventricles to bend during construction, making them ideal for applications like HVAC and refrigeration systems. HVAC and refrigeration is the largest end-use application, giving coils their largest share of market revenue. Coil — The coil product form allows for more efficient manufacturing and reduces in-field scrap for factory-assembled systems.

Copper tubing in its straight-length form is most often used for plumbing where the pipe sections are cut to sizes and assembled using fittings at the construction site. This specific formulation is also applicable for medical gas systems and certain industrial uses. Straight sections are losing market share to PEX plastic piping in home plumbing, but they continue to be a site for commercial and high-temperature plumbing where plastics have limited ability.

By Thickness : Standard Gauge Dominates, Capillary Tubes Growing

Standard gauge copper tubing is the largest and most commonly used thickness category of its kind in terms of market roll, also because they are extensively used for plumbing systems, HVAC refrigerant line systems, low-pressure and positive pressure compressed gases or compressed air (should not use as a hydraulic fluid transport system), cryogenic fluids or gaseous oxygen lines, alternatively industrial & commercial fluid transportation apparatus. These tubes are recommended in determining and developing an uncompromised indicated balance among durability, corrosiveness-resistance, strength, cost-effective coefficient etc. hence most of the residential, commercial as well as industrial infrastructural projects can be compiled through using steel pipes/tubes bodies for production though offered to suit accordance with standard technical specifications. Extra heavy gauge tubes are primarily used in pressure and heavy-duty industrial applications, such as power plants, marine systems, and large commercial climate control systems, where additional strength and durability to ensure an extended service life is paramount.

The fastest-growing segment is because of the increasing demand for refrigeration systems, air conditioners, precision cooling applications, and medical devices are the capillary tubes. As key components of the latest cooling technologies and energy-efficient appliances, their small footprint and capacity to control refrigerant flow with precision are important factors. Thin wall gauge tubes are also enticing in lightweight and cost-sensitive applications from ease of installation to less material usage amid higher adoption within compact HVAC and automotive systems..

By Application : HVAC Dominates, Medical Gas Growing

HVAC and refrigeration is the biggest and most strategically important end use for copper tubes. Copper tubes are utilized in the heat exchangers and refrigerant circuits of every air conditioner, heat pump, refrigerator, commercial refrigeration system. This segment keeps representing a strong growth with the increase of global temperatures and the domestication of AC adoption in markets where it used to be rare. The phasing out of traditional refrigerants in favor of next-generation low-GWP refrigerants is another area fueling demand for new tube specifications and premium quality products.

Factors such as corrosion resistance, cleanliness, and reliability make copper tubes to be preferred in most medical gas delivery systems. Any hospital, clinic and surgical center that supplies oxygen, nitrous oxide or medical air through piping systems needs to have an infrastructure of piping containing copper tube. This niche, high-market potential segment is supported by growing construction of hospitals across Asia and Middle East.

Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

76% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

55% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

52% |

Copper Tubes Market North America Insights:

North America is a lucrative region for copper tube owing to high HVAC demand, continuous commercial and residential construction activity & plumbing infrastructure. The U.S. has a large number of HVAC in-place and almost all needs to have the equipment replaced every 15-20 years. Based on product, the growing demand for heat pump systems as a gas alternative is particularly driving demand in high efficiency copper refrigerant circuits.

Get Customized Report as per Your Business Requirement - Enquiry Now

Copper Tubes Market Europe Insights:

The European market for copper tubes is already well developed, with large contributions from the HVAC, plumbing and industrial-related applications. The main market is Germany, Italy, France and the UK. Copper was favored for plumbing in many European construction codes—the installed base is large. Europe is experiencing booming heat pump market because of government measures to phase out gas boilers which are driving strong demand for the copper tubes and pipes surrounding those heat exchangers.

Copper Tubes Market Asia Pacific Insights:

The Asia Pacific copper tube market is the largest due to the manufacturing and construction sectors are driven by China. Considered the leading global copper tube manufacturer and consumer, China remains the biggest copper tube producer. As incomes rise and temperatures increase, air conditioning is becoming an explosive phenomenon in India, Vietnam, Thailand and other emerging Asian economies. Japan and South Korea are mature markets with steady replacement demand..

Copper Tubes Market Middle East & Africa Insights:

the Middle East and strong demand for air conditioning, this region is a stable market with high potential for refrigerant copper tubes up to now. Demand for HVAC and plumbing in big commercial or residential buildings will focus on huge amounts of copper tubes for the critical development tasks in Saudi Arabia, UAE and Qatar. In particular, investment in infrastructure drives Africa's market growth and the potential for AC adoption facilitated by power infrastructure improvements in sub-Saharan African countries allows the market to open wider.

Copper Tubes Market Latin America Insights:

Latin America is a growing copper tube market, led by Brazil, Mexico, Colombia, and Chile. Brazil's large construction market and growing AC penetration drive consistent demand. The sizeable construction market in Brazil and rising AC penetration will mean steady demand. Latin American copper tube manufacturers will benefit from their privileged access to raw materials considering the prominent domestic copper production capacity in the region, chiefly Chile—the leading regional and global producer of copper. Widespread first-time adoption of residential air conditioning is being propelled by a burgeoning middle class throughout the region..

Copper Tubes Market Growth Drivers:

-

Expanding HVAC demand in warming climates and growing construction in developing markets

There are two parallel trends that support the copper tube market First, the world is warming up and living standards are rising in developing countries, which together creates massive first-time demand for air conditioning. It turns out that in India, Southeast Asia, Africa and Latin America hundreds of millions of households are buying their first air conditioners — one each needs a number of copper refrigerant tubes. Second, infrastructure and construction investment in developing markets is creating the hospitals, offices, factories and homes all of which need copper plumbing and HVAC systems. These trends help maintain the markets growth outlook during our forecasted period.

The changeover to global heat pumps is a concrete and robust driver of copper tube demand The gradual phase-out of fossil fuel heating systems in favour of electric heat pumps has required copper refrigerant circuits for each installation, as governments in Europe, North America and increasingly Asia have shown commitment to this infrastructure. Due to government subsidies, heat pump installations rapidly accelerated, growing over 50% yoy in some European markets.

Copper Tubes Market Restraints

-

High copper prices and competition from plastic piping alternatives

Copper metal price fluctuations constitute the biggest limitation regarding copper tube market expansion. Copper is a tradable global commodity that tends to be driven by the level of demand exhibited by China, interruptions in supply and certain macroeconomic factors. With a spike in pricing of copper, alternatives are sought by end users. Cross-linked polyethylene piping (PEX), which rose rapidly in residential plumbing to take over most of the market share from copper, is cheaper and easier to install, although it also resists freezing. This substitution pressure particularly restricts the growth of copper tube in the segment of residential plumbing.

Copper Tubes Market Opportunities

-

Next-generation refrigerant transition and heat pump boom create premium product demand

The global transition from high-GWP refrigerants like R-410A to next-generation refrigerants including HFOs and natural refrigerants like R-290 (propane) and R-744 (CO2) requires new HVAC system designs with different operating pressures and temperature ranges. These new systems need higher quality, tighter-tolerance copper tubes than today. Gunther Walther (Walther, 2001) also discusses how manufacturers that make copper products specifically for next generation refrigerants and high efficiency heat pumps will gain a substantial premium price in an expanding market. Heavy metal wire for ego wiring has the highest technical performance requirement, while copper exhibits better properties than plastic based alternatives which will further strengthens copper's portfolio in the most demanding applications.

Recent Developments:

-

2025: Wieland Group announced the opening of a new copper tube production facility in the United States specifically designed to serve the growing heat pump market, with capacity for 30,000 tonnes annually of precision refrigerant-grade copper tubes optimized for next-generation low-GWP refrigerant systems.

-

2024: Daikin Industries and Mitsubishi Electric jointly announced they would standardize on a new copper tube specification for their next-generation inverter heat pump product lines, requiring suppliers to develop ultra-clean, tight-tolerance tubes that support their efficiency target of exceeding energy factor 5.0.

-

2023: Mueller Industries reported record revenue driven by strong North American HVAC replacement demand and initial heat pump market adoption, with its copper tube and fittings divisions both achieving double-digit revenue growth as homeowners upgraded to high-efficiency cooling and heating systems.

Copper Tubes Market Key Players:

-

Wieland Group

-

Mueller Industries Inc.

-

KME Group

-

Metalcorp Group

-

Kobelco & Materials Copper Tube Ltd.

-

Hutmen S.A.

-

UACJ Corporation

-

Zhejiang Hailiang Co., Ltd.

-

Golden Dragon Precise Copper Tube Group Inc.

-

Luvata Oy

-

KGHM Polska Miedz S.A.

-

Cerro Flow Products LLC

-

Triangle Brass Manufacturing

-

Yorkshire Copper Tube Ltd.

-

Mehta Tubes Ltd.

-

Cambridge-Lee Industries LLC

-

MM Kembla

-

Shanghai Metal Corporation

-

Qingdao Hongtai Copper Co., Ltd.

-

Uniflow Copper Tubes

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 45.77 Billion |

| Market Size by 2035 | USD 84.4 Billion |

| CAGR | CAGR of 6.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Straight lengths, Coils, Pancake or flattened tubes, U-Bends, Drawn tubes, Others) • By Thickness (Standard gauge, Extra heavy gauge, Thin wall gauge, Capillary tubes, Others) • By Application (Plumbing, HVACR, Industrial, Medical gas system, Fire sprinkler system, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Wieland Group; Mueller Industries Inc.; KME Group; Metalcorp Group; Kobelco & Materials Copper Tube Ltd.; Hutmen S.A.; UACJ Corporation; Zhejiang Hailiang Co., Ltd.; Golden Dragon Precise Copper Tube Group Inc.; Luvata Oy; KGHM Polska Miedz S.A.; Cerro Flow Products LLC; Triangle Brass Manufacturing; Yorkshire Copper Tube Ltd.; Mehta Tubes Ltd.; Cambridge-Lee Industries LLC; MM Kembla; Shanghai Metal Corporation; Qingdao Hongtai Copper Co., Ltd.; Uniflow Copper Tubes. |

Frequently Asked Questions

Expanding HVAC demand driven by rising global temperatures and the heat pump transition for building heating are the primary growth drivers.

Asia Pacific dominates, with China as the world's largest producer and consumer of copper tubes.

HVAC & Refrigeration is the largest end-use segment due to copper's superior thermal conductivity in heat exchange applications.

The market was valued at USD 45.77 billion in 2025.

The market is expected to grow at a CAGR of 6.33% from 2026 to 2035.

Get in Touch