Food Packaging Market Report Scope & Overview:

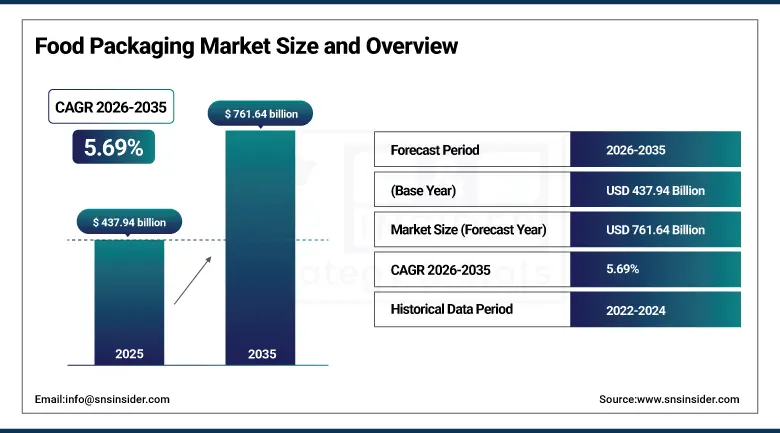

The Food Packaging Market was valued at USD 437.94 billion in 2025 and is expected to reach USD 761.64 billion by 2035, growing at a CAGR of 5.69% from 2026–2035.

The food packaging market provides essential protection, preservation, storage, and transportation solutions across the food supply chain. It includes flexible packaging, rigid plastics, glass containers, metal cans, and bulk logistics packaging used by food manufacturers, retailers, and food service providers. The market is evolving through growing demand for sustainable and recyclable materials, adoption of smart packaging technologies, and rising consumption of convenience and packaged foods worldwide.

It exemplifies the most advanced food packaging innovation ecosystem in the world, further underscored by two major sustainable packaging innovation investment confirmations; the October 2024 launch of Amcor's AmLite Ultra Recycle platform for mono-material polyethylene food packaging in February 2025 and Sealed Air's Cryovac OptiDure high-barrier recyclable film.

Market Size and Forecast

-

Market Size in 2026E: USD 462.86 Billion

-

Market Size by 2035: USD 761.64 Billion

-

CAGR (2026-2035): 5.69% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia-Pacific

To Get more information on Food Packaging Market - Request Free Sample Report

Food Packaging Market Trends

-

Brand owners are adopting recyclable flexible packaging solutions driven by retailer and regulatory pressure, with Amcor and Sealed Air leading innovation in recyclable film technologies.

-

Smart packaging is growing with QR-code digital product passports, freshness indicators, and tamper-evident features improving transparency and safety.

-

Modified atmosphere packaging is widely used in fresh food categories to extend shelf life by controlling internal gas composition and reducing food waste.

-

Active packaging systems using oxygen scavengers and antimicrobial agents are gaining traction to enhance shelf life and support clean-label products.

-

Fiber-based packaging adoption is increasing due to PFAS restrictions, driving a shift toward sustainable paper and paperboard alternatives.

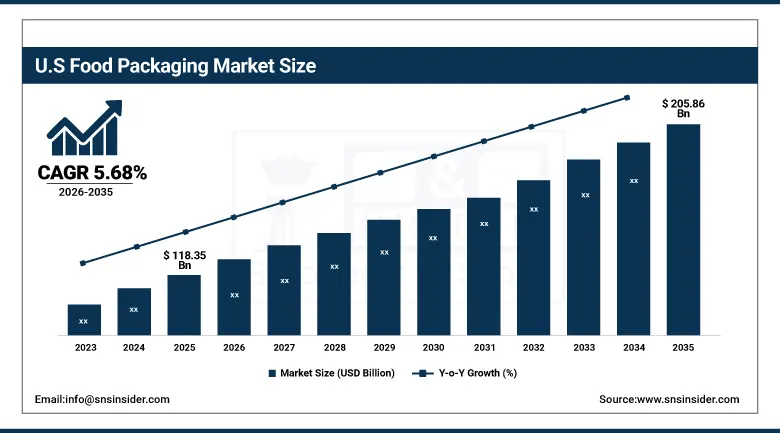

The U.S. Food Packaging Market Size Outlook

The U.S. Food Packaging Market was valued at USD 118.35 billion in 2025 and is expected to reach USD 205.86 billion by 2035, growing at a CAGR of 5.68% during 2026–2035.

The US is the largest and most commercially sophisticated food packaging market in the world, with per-capita packaged food consumption higher than any other country and a demanding cold chain/fresh/chilled specification that exists due to the best developed cold chain/food distribution infrastructure on earth, as well as being home to international companies dominating QSRs and Food Delivery services. With the FDA setting the broadest regulatory and brand owner sustainability commitments for grease-proofing agents at either end along with national market-leading packaging material development ecosystem of over hundreds of innovative packaging material and technology companies headquartered across the U.S. in addition to Amcor, Sealed Air, Berry Global -clearly this position creates both scale unmatched and perhaps unprecedented sustainable packaging innovation pull on American firms.

Food Packaging Market Segment Analysis

-

By Packaging Type, Flexible dominated with approximately 46.83% of revenues in 2025, reflecting its adoption across snack, bakery, dairy, and frozen food categories; Semi-rigid is the fastest-growing packaging type at approximately 6.14% CAGR from 2026 to 2035, driven by thermoformed tray and clamshell demand from fresh produce, dairy, and prepared meal categories.

-

By Material, Plastic dominated with approximately 38.57% of revenues in 2025 due to its established barrier performance, low material cost, and food manufacturer preference for lightweight formats; Paper and Paperboard is the fastest-growing material at approximately 6.72% CAGR from 2026 to 2035, driven by regulatory PFAS bans, clean-label brand commitments, and e-commerce packaging demand.

-

By Food Type, Meat and Seafood held the highest revenue share of approximately 24.63% in 2025 due to high packaging intensity of fresh, chilled, and processed protein categories; Fruits and Vegetables is the fastest-growing food type at approximately 6.54% CAGR, driven by increasing fresh produce consumption and growing demand for breathable and anti-fog packaging films.

-

By End-User, Quick Service Restaurants accounted for approximately 34.72% of revenues in 2025 and is simultaneously the fastest-growing end-user at approximately 6.89% CAGR, reflecting the high per-outlet food packaging consumption intensity of global QSR chains and the extraordinary expansion of food delivery platforms creating packaging volume growth.

By Packaging Type,flexible dominates the food packaging market, semi-rigid grows fastest

Flexible packaging dominated the food packaging market with an estimated 46.83% market share in 2025, driven by its material efficiency, cost-effectiveness, lightweight design, and versatility across food categories such as snacks, bakery products, frozen foods, dairy products, condiments, and pet food. Its ability to provide strong product protection, convenient sealing options, and reduced transportation costs continues to support widespread adoption, while ongoing innovations in lightweight and high-performance packaging solutions further strengthen its market position.

Semi-rigid packaging is projected to be the fastest-growing packaging type in the Food Packaging Market, expanding at a CAGR of approximately 6.14% through 2035, supported by rising demand for prepared meals, ready-to-eat foods, and fresh produce. Its ability to provide attractive product presentation, modified atmosphere preservation, and microwave-ready convenience makes it increasingly preferred across premium chilled food applications.

By Material,plastic dominates the food packaging market, paper and paperboard grows fastest

Plastic dominated the food packaging market with an estimated 38.57% market share in 2025, owing to its superior barrier protection, lightweight properties, flexibility, scalability, and cost-effectiveness. Despite increasing sustainability concerns, plastic remains widely used across flexible and semi-rigid packaging applications due to its ability to extend shelf life and reduce food waste through effective moisture and oxygen barrier performance.

Paper and Paperboard is projected to be the fastest-growing material segment, expanding at a CAGR of approximately 6.72% during 2026–2035, driven by increasing sustainability regulations, growing consumer preference for fiber-based packaging, and advancements in high-barrier paper technologies that enable replacement of conventional plastic packaging across a wider range of food applications.

By Food Type,meat and seafood dominates the food packaging market, fruits and vegetables grows fastest

The meat & seafood segment dominated the food packaging market with approximately 24.63% of market revenue in 2025, driven by its high packaging intensity and reliance on advanced packaging solutions such as modified atmosphere packaging (MAP), vacuum skin packaging, and high-barrier films to maintain product freshness, safety, and shelf life.

The fruits & vegetables segment is projected to be the fastest-growing food type in the food packaging market, expanding at a CAGR of approximately 6.54% through 2035, driven by rising fresh produce consumption, increasing adoption of advanced breathable packaging solutions, and growing demand for e-commerce-ready produce packaging.

By End-User,quick service restaurants dominate the food packaging market and grow fastest

The quick service restaurants (QSRs) segment dominated the food packaging market with approximately 34.72% market share in 2025 and is also projected to be the fastest-growing end-user segment, expanding at a CAGR of around 6.89% through 2035, driven by the continued expansion of fast-food chains, food delivery services, and increasing demand for sustainable packaging solutions.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83% |

|

Europe |

Germany |

28% |

|

Asia Pacific |

China |

46% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

43% |

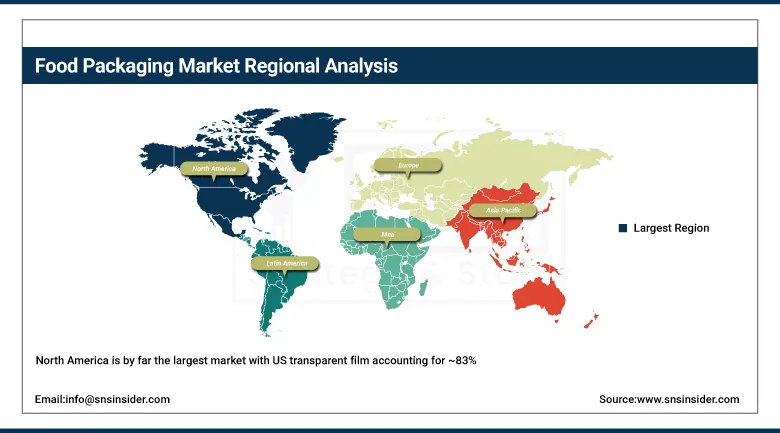

North America Food Packaging Market Insights

North America is by far the largest market with US transparent film accounting for ~83% of. Combined, the FDA PFAS ban, U.S. Plastics Pact 2025 commitments and California packaging extended producer responsibility legislation make the U.S. market home to the most sophisticated sustainable packaging regulatory environment, and therefore one with by far the broadest compliance-driven sustainable packaging transition in any national food market. Canada also adds through its high food processing sector and the matching regulatory framework around sustainable packaging requirements with U.S.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Food Packaging Market Insights

Europe is the most regulatory-driven food packaging market worldwide, having been influenced by a revision of the EU's Packaging and Packaging Waste Regulation (which has mandated recycled content minimums, recyclability criteria, and extended producer responsibility), coupled with an increasingly robust set of regulations from the Single-Use Plastics Directive that restrict or ban certain particular food contact plastic items. The largest food manufacturing and retail sectors in Europe drive Europe to consume the most packaged food on the continent, which is reflected in innovation by packaging type: barrier paper for flexible packaging; compostable flexible packaging formats mainly for food service applications; reusable packaging formats largely geared toward the grocery retail channel.

Asia Pacific Food Packaging Market Insights

In 2025, the food packaging market accounted for one-third of global revenues in Asia Pacific as among the fastest growing markets worldwide for processed food consumption and India, China, Japan and South Korea spearheading unprecedented urbanization changes along with disposable income growth and transformation of dietary patterns transitioning towards packaged or convenience pressure and ready-to-eat formats from bulk and loose food purchase systems. As the largest economy for food manufacturing in the world, China dominates Asia Pacific food packaging volumes; The rapid expansion of India's packaged food market and increasing modern retail infrastructure across Southeast Asian countries create a trajectory of fastest regional market growth worldwide.

Latin America and MEA Food Packaging Market Insights

Food packaging markets of Latin America and MEA impacted by booming urbanization, modern retail space development and increase in packaged food consumption Oct 2025. Brazil is the largest country in Latin America from an extensive food and beverage manufacturing sector and growing QSR. Octofrost is really having great business acceleration with their Innovative solutions available at different package size, and region following MEA food packaging avenues from Gulf cooperation council modern retail expansion, Sub Saharan Africa packaged food consumption growth along with yet growing global pre-formed pouch demand for sustainable future against the backdrop of external pressures in this countries on the lip of 500 million equal partnered population.

Market Dynamics

Growth Drivers: Global expansion of packaged food consumption and QSR food delivery growth creating structural volume demand, combined with sustainable packaging transition creating pricing premiums that sustain value growth above volume growth

The primary structural growth drivers for the food packaging market are the irreversible global expansion of processed, packaged, and convenience food consumption driven by urbanization, household income growth, and changing food preparation behaviors that makes packaged food the default meal solution for an expanding share of the world's population, combined with the sustainable packaging transition that is adding value to each unit of packaging through the premium material costs and innovation investment that recyclable, compostable, and smart packaging formats command relative to the conventional formats they replace.

The combination of Amcor's Alite Ultra Recycle mono-material PE platform, Tetra Pak's fiber-based beverage cartons replacing aluminum layers, and Sealed Air's Cryovac OptiDure recyclable flexible film for meat packaging, each launched within months of each other in late 2024 and early 2025, confirm that the food packaging industry's sustainable innovation pipeline is producing commercial products at a pace that will systematically raise the average packaging material cost per unit across every food category and end-user segment, sustaining the Food Packaging Market's 5.69% CAGR value growth above the underlying volume growth driven by global food consumption expansion through the 2026 to 2035 forecast period.

Restraints: High sustainability transition costs, regulatory complexity, and performance limitations of eco-friendly packaging are slowing adoption in demanding applications.

Food packaging market faces challenges from the higher costs of sustainable packaging materials, which can be 20–50% more expensive than conventional plastic alternatives. Diverse regulatory requirements across regions increase compliance complexity for multinational manufacturers. Additionally, many recyclable, paper-based, and biodegradable packaging materials still face technical limitations in moisture, oxygen, and barrier protection performance compared to traditional plastics. These cost, regulatory, and performance challenges can slow the adoption of sustainable packaging solutions, particularly in demanding food preservation applications.

Opportunities: Smart packaging digital connectivity, active and intelligent packaging for food waste reduction, and e-commerce food packaging specialization

Smart packaging technologies, including digital product passports, NFC-enabled freshness monitoring, and blockchain-based traceability, are creating significant growth opportunities by enhancing transparency, consumer engagement, and anti-counterfeiting capabilities. Rising concerns over food waste are driving demand for active packaging solutions such as oxygen scavengers and antimicrobial materials that extend shelf life and improve distribution efficiency. Additionally, the rapid growth of e-commerce food delivery is increasing demand for specialized packaging formats designed to withstand transportation, handling, and last-mile delivery conditions.

Recent Developments:

-

March 2025: Amcor launched a new line of fully recyclable flexible pouches for snacks and beverages, designed to enter established film recycling streams at end of life while maintaining the barrier performance and processing compatibility that food manufacturer packaging lines require.

-

February 2025: Amcor expanded its AmLite Ultra Recycle flexible food packaging platform with new high-barrier mono-material polyethylene structures for dry food and dairy applications, targeting brand owner sustainable packaging commitments across North American and European retail markets.

-

January 2025: Tetra Pak introduced fiber-based beverage cartons with improved barrier properties as an alternative to aluminum layers, maintaining food safety and shelf life performance while supporting package recyclability improvements that reduce the carton's material complexity and environmental footprint.

-

October 2024: Sealed Air Corporation launched its Cryovac Brand OptiDure high-barrier recyclable flexible film for fresh and processed meat packaging applications, providing food safety packaging performance equivalent to conventional multi-layer laminates within a recyclable mono-material structure.

-

2025: Klockner Pentaplast introduced a new lightweight MAP tray design exhibiting high performance with material reduction for chilled prepared meal packaging, demonstrating the material efficiency innovation sustaining plastic packaging's cost competitiveness against emerging sustainable alternatives.

Food Packaging Market Key Players are:

-

Amcor plc

-

Sealed Air Corporation

-

Berry Global Group Inc.

-

Tetra Pak International SA

-

Smurfit Kappa Group plc

-

Mondi plc

-

Sonoco Products Company

-

WestRock Company

-

DS Smith plc

-

Huhtamaki Oyj

-

Constantia Flexibles Group GmbH

-

Bemis Company Inc. (Amcor)

-

Coveris Group

-

CCL Industries Inc.

-

Silgan Holdings Inc.

-

Graphic Packaging Holding Company

-

Ardagh Group SA

-

Crown Holdings Inc.

-

Ball Corporation

-

AptarGroup Inc.

Food Packaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 437.94 Billion |

| Market Size by 2035 | USD 761.64 Billion |

| CAGR | CAGR of 5.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Packaging Type (Flexible, Rigid, Semi-rigid), • By Material (Plastic, Paper and Paperboard, Glass, Metal, Biopolymers, Others), • By Food Type (Bakery and Confectionery, Meat and Seafood, Fruits and Vegetables, Dairy, Beverages, Ready Meals, Others), • By End-User (Quick Service Restaurants, Food Manufacturers, Retail, Institutional Catering, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amcor plc, Sealed Air Corporation, Berry Global Group Inc., Tetra Pak International SA, Smurfit Kappa Group plc, Mondi plc, Sonoco Products Company, WestRock Company, DS Smith plc, Huhtamaki Oyj, Constantia Flexibles Group GmbH, Bemis Company Inc. (Amcor), Coveris Group, CCL Industries Inc., Silgan Holdings Inc., Graphic Packaging Holding Company, Ardagh Group SA, Crown Holdings Inc., Ball Corporation, AptarGroup Inc. |

Frequently Asked Questions

Paper and Paperboard is the fastest-growing material at approximately 6.72% CAGR from 2026 to 2035,

Flexible packaging dominated with approximately 46.83% of revenues in 2025, reflecting its unmatched combination of material efficiency,

The irreversible global expansion of processed, packaged, and convenience food consumption driven by urbanisation and changing food behaviour creating structural volume demand

The Food Packaging Market was valued at USD 437.94 billion in 2025.

The Food Packaging Market is expected to grow at a CAGR of 5.69% from 2026 to 2035.

Get in Touch