Geosynthetic Clay Liner (GCL) Market Report Scope & Overview:

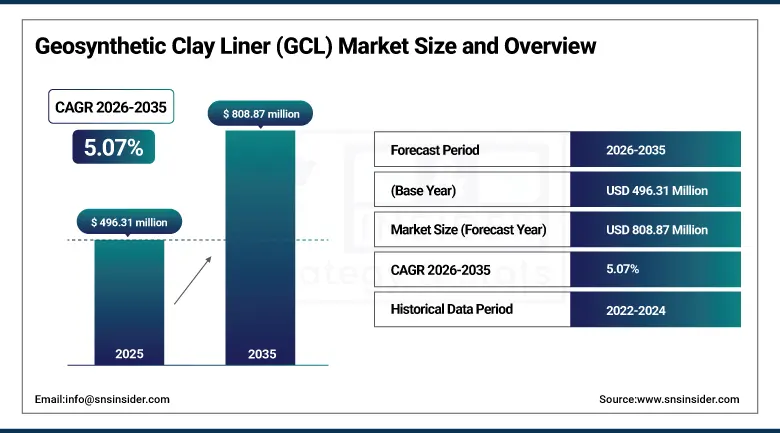

The Geosynthetic Clay Liner (GCL) Market was valued at USD 496.31 Million in 2025 and is expected to reach USD 808.87 Million by 2035, growing at a CAGR of 5.07% from 2026 to 2035.

Geosynthetic clay liners represent an essential category of the geosynthetics industry, featuring engineered composite liners that comprise the granular form of sodium or calcium bentonite clay sandwiched between two geotextile carrier layers, offering superior performance in terms of containment and protection. These geosynthetic clay liners have been used in a diverse array of applications such as municipal solid waste landfills, hazardous waste facilities, mining tailings ponds, water reservoirs, canal systems, and wastewater lagoons. They provide an efficient and economical alternative to compacted clay liners due to their ability to seal themselves upon hydration and resist leakage due to percolation of contaminated water.

CETCO (Minerals Technologies Inc.) operates manufacturing and distribution facilities across more than 30 countries and supports environmental containment projects in over 100 countries worldwide. Its Bentomat® geosynthetic clay liner portfolio is widely deployed in landfill, mining, wastewater, and infrastructure containment applications, with the company maintaining one of the industry's largest technical support networks dedicated to geosynthetic barrier system design and installation assistance.

Market Size and Forecast

-

Market Size in 2026E: USD 518.49 Million

-

Market Size by 2035: USD 808.87 Million

-

CAGR (2026–2035): 5.07%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Geosynthetic Clay Liner (GCL) Market - Request Free Sample Report

Geosynthetic Clay Liner (GCL) Market Trends

-

Stringent landfill and hazardous waste regulations worldwide are driving steady demand for GCLs in containment liner systems.

-

Expanding mining activities across Asia Pacific, Latin America, and Africa are increasing GCL adoption in tailings and heap leach containment applications.

-

Rising water scarcity and investments in irrigation and water storage infrastructure are boosting GCL deployment in water containment projects.

-

Advances in polymer-modified bentonite technologies are enhancing GCL performance and expanding use in industrial and hazardous waste containment.

-

Growing infrastructure and environmental remediation projects in emerging economies are creating new opportunities for GCL adoption.

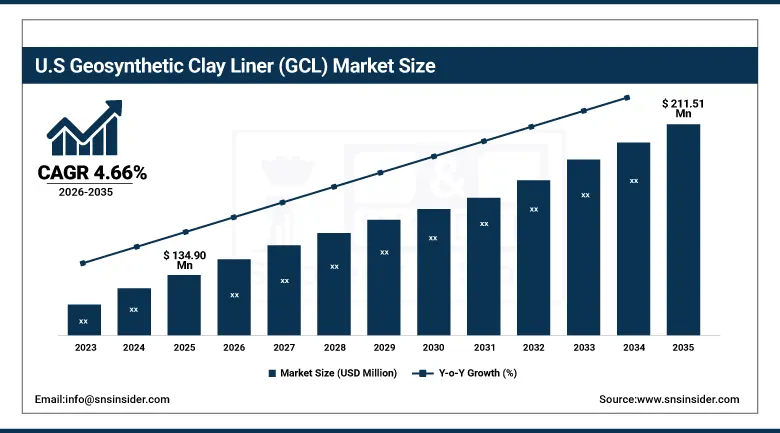

The U.S. Geosynthetic Clay Liner (GCL) Market Outlook

The U.S. Geosynthetic Clay Liner (GCL) Market was valued at USD 134.90 Million in 2025 and is expected to reach USD 211.51 Million by 2035, growing at a CAGR of 4.66%.

The USA is the largest national market for GCL products due to its one of the most advanced regulations on waste containment systems. Requirements for both municipal solid waste and hazardous waste landfills by EPA Subtitle D and Subtitle C involve construction of composite liners, which incorporate geosynthetic clay liners. This forms an ongoing pattern in purchasing these materials for construction of numerous authorized landfills in the country. Moreover, the U.S. mining industry creates additional demand through use of GCL in heap leach pads, tailing facilities, and processing ponds. Such applications can be frequently found in western mining regions in connection with precious and base metals.

In 2025, U.S. GCL demand benefited from continued capital expenditure in landfill expansion and cell development projects, as municipalities and waste management operators responded to growing solid waste volumes. Federal infrastructure funding appropriations supporting water quality and environmental remediation projects provided additional tailwinds for GCL procurement by public sector engineering and environmental contractors.

Geosynthetic Clay Liner (GCL) Market Segment Analysis

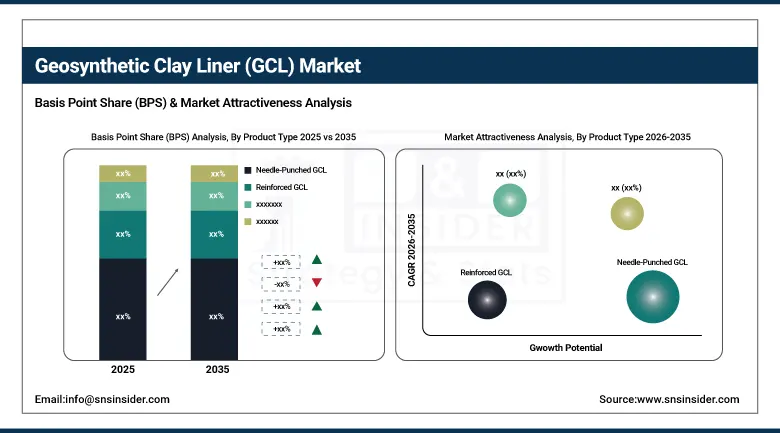

By Product Type, needle-punched GCL dominated the geosynthetic clay liner (GCL) market with 37.12% share in 2025, while stitch-bonded GCL is the fastest-growing product type with the highest CAGR of 6.68% from 2026 to 2035.

By Raw Material, sodium bentonite GCL dominated the geosynthetic clay liner (GCL) market with 66.45% share in 2025, while polymer-modified bentonite GCL is the fastest-growing raw material type with the highest CAGR of 6.98% from 2026 to 2035.

By End-Use Industry, waste management dominated the geosynthetic clay liner (GCL) market with 34.24% share in 2025, while mining is the fastest-growing end-use industry with the highest CAGR of 5.83% from 2026 to 2035.

By Application, landfill liners & caps dominated the geosynthetic clay liner (GCL) market with 36.24% share in 2025, while mining containment is the fastest-growing application with the highest CAGR of 5.74% from 2026 to 2035.

By Product Type, needle-punched GCL dominates the geosynthetic clay liner (GCL) market, while stitch-bonded GCL is the fastest-growing segment.

Needle-Punched GCL segment dominated the market with the highest revenue share of 37.12% in 2025, due to its ability to withstand high levels of internal shearing, prevent migration of the bentonite, and exhibit excellent performance in various containment applications, such as landfills, mining sites, and water-related projects. The mechanical binding of geotextile material and bentonite filling via fiber entanglement through the needling method results in superior stability and hydraulic characteristics under confining pressure. Such characteristics explain why the needle-punched type of GCL is usually specified in challenging containment projects in which the integrity of the lining systems is crucial.

The Stitch-Bonded GCLs segment is anticipated to hold the highest CAGR among all other segments during the assessment period (2026-2035), owing to increasing preference for GCLs, especially when bentonite layer thickness consistency and high-seam strength are required in their respective applications. Stitching-bonded type of construction helps in controlling the thickness consistency and seam strength of bentonite layers. Increasing investments in mining infrastructure in regions like APAC and Latin America, where stitching-bonded type of GCLs are increasingly being used as liners in tailings and leach pad containment operations, are contributing significantly to the growth of this global segment.

By Raw Material, sodium bentonite (GCL) dominates the geosynthetic clay liner (GCL) market, while polymer-modified bentonite GCL is the fastest-growing segment.

Sodium Bentonite GCL segment dominated the geosynthetic clay liner (GCL) market with the highest revenue share of 66.45% in 2025, accordance with the proven track record of sodium bentonite as the core hydraulic barrier material for geosynthetic liners. The ability of sodium bentonite to swell upon being hydrated, the very low permeability of this material, together with its self-healing properties under confinement pressure have made sodium bentonite the standard used for liner systems as required by regulation for landfill, mining, and environmental containment applications across the globe. Its widespread availability and performance history make sodium bentonite the preferred material for the manufacture of GCLs.

Polymer Modified Bentonite GCL Segment will witness the highest CAGR during the forecast period from 2026 to 2035 due to increasing demand for performance of GCLs in chemically aggressive leachate conditions, in which sodium bentonite may exhibit deterioration in hydraulic conductivity properties. The polymers modify bentonite either through ionic polymers or by blending them into bentonites, which improve the chemical resistance of bentonite while ensuring that hydraulic conductivity remains low in conditions of high ionic strength or multivalent cations.

By End-Use Industry, waste management dominates the geosynthetic clay liner (GCL) market, while mining is the fastest-growing segment.

Waste Management segment dominated the market with the highest revenue share of 34.24% in 2025, motivated by the necessity to use engineered lining systems in landfills for municipal solid waste and hazardous waste disposal sites around the world. Regulations in North America, Europe, and more recently Asia Pacific and Latin America compel composite lining systems design using a geomembrane on top of a GCL lining for landfill cells and closures at existing waste disposal facilities. The continued growth of landfill capacity due to increasing solid waste generation from urban centers, along with the significant market for rehabilitation and landfill closures, keeps demand for GCLs at high levels.

The mining segment is anticipated to experience the fastest CAGR between 2026 and 2035 due to the growth in mineral extraction worldwide and, therefore, the demand for mining containment solutions. The application of GCLs is widespread in the construction of heap leach pads, base liners and caps of tailings storage facilities, and process solution ponds, which are applications experiencing rapid growth amid increasing global investments in the mining industry. The increasingly strict liner specifications demanded during the permitting process for mines in South America, Africa, and Asia Pacific are leading to the use of composite liners incorporating GCLs.

By Application, landfill liners & caps dominates the geosynthetic clay liner (GCL) market, while mining containment is the fastest-growing segment.

Landfill Liners & Caps segment dominated the market with the highest revenue share of 36.24% in 2025, highlighting the importance of GCLs as integral parts of the composite liner system which is required to be used in all municipal and industrial waste disposal facilities that conform to relevant regulations. As an alternative material, GCLs act as a cost-effective clay liner that can perform equally well compared to the equivalent hydraulic performance of a well-compact native clay liner but with far less material thickness and lower cost and time of construction. There will be increased demand coming from this key market sector due to the expansion and construction of landfill facilities across the globe.

The Mining Containment segment is expected to grow at the highest rate among all segments, driven by the worldwide growth of infrastructure for mineral processing and extraction in areas where there is considerable development of mineral resources taking place. The factors responsible for fast growth include investments made in mining for precious metals and battery materials, strict regulations on environmental permits related to containment systems, and the realization by mine operators about the superiority of GCLs over conventional liners.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.54% |

|

Europe |

Germany |

30.45% |

|

Asia Pacific |

China |

41.26% |

|

Middle East & Africa |

UAE |

37.36% |

|

Latin America |

Brazil |

44.87% |

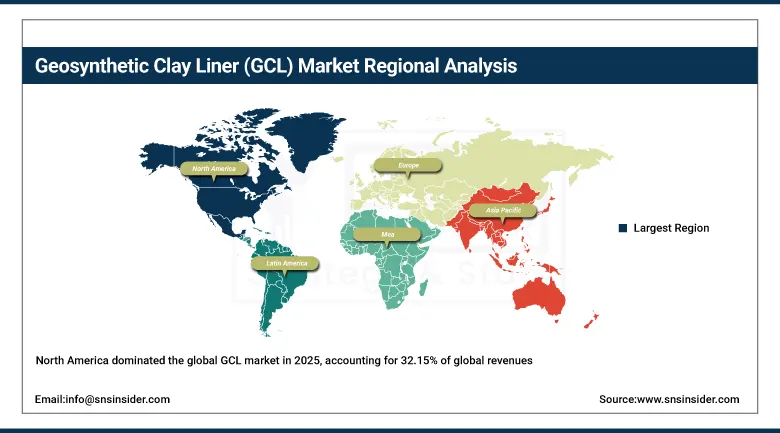

North America Geosynthetic Clay Liner (GCL) Market Insights

North America dominated the global GCL market in 2025, accounting for 32.15% of global revenues, with the United States representing 84.54% of regional revenue. Market leadership in North America is ensured by the presence of an extensive and strict regulatory regime governing the design of landfill liner systems, containment of hazardous waste, and environmental restoration, leading to continuous demand for GCL from a sizeable number of containment facilities currently operating. The United States GCL market will be supported by the presence of a well-developed technical specification process where the use of GCL is made mandatory under the composite liner design system requirements of the Subtitle D and Subtitle C regulations.

The growing demand for GCL in North America will be supplemented by Canada, which has an increasing number of contributions from its mining industry in terms of GCL adoption within its operations involving tailings and heap leach ponds due to increasing environmental permits within the provinces. The active participation of Canada in water and environmental site remediation creates additional demand for GCL.

More than 2,600 active municipal solid waste landfills utilize engineered containment systems, making the region the largest installed base for GCL applications. The U.S. and Canada collectively account for over 15,000 operating and abandoned mine sites requiring containment, closure, and environmental remediation solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Geosynthetic Clay Liner (GCL) Market Insights

The continent of Europe, aided by the forward-thinking environmental regulations of the region, an active landfill building and closing industry, and increased investments in water management facilities in Western and Eastern Europe, is a leader in GCLs. The regulations of the EU Landfill Directive, which require the use of GCLs or their equivalents in newly built landfill liners in all member nations, ensure steady demand from regulation-induced sources. Germany accounts for of regional sales due to its technologically advanced waste management industry and significant industrial needs for GCLs. The remaining significant GCL markets in Europe include the UK, France, Italy, and Spain. Eastern Europe offers strong growth potential, driven by rising waste management investments and increasing alignment with EU environmental regulations.

Over 500 million tonnes of waste are processed annually under stringent environmental regulations, supporting widespread adoption of advanced geosynthetic barrier systems. More than 25 countries enforce landfill directives requiring engineered lining and capping systems for hazardous and non-hazardous waste facilities. Increasing national water conservation programs across Southern and Eastern Europe are creating new demand for GCLs in reservoir and canal lining applications beyond the traditional landfill containment sector.

Asia Pacific Geosynthetic Clay Liner (GCL) Market Insights

Asia Pacific segment is expected to grow at the fastest CAGR of about 5.02% from 2026-2035. A double-sided market environment exists within the region, whereby the mature markets of Japan and Australia show developed regulatory environments and advanced GCL specification procedures, but the rapidly developing markets of China, India, and Southeast Asian countries demonstrate growth markets, fueled by increased investment into environmental infrastructure and progressive regulations. China is the dominant market within the region when it comes to consumption of GCLs, due to a large pipeline for landfill construction, as well as developments within its industrial waste industry and mining containment sector. India demonstrates itself to be one of the fastest-growing markets within the region.

The region develops hundreds of new landfill, mining, and water infrastructure projects annually, making it the fastest-growing GCL consumption hub globally. China, India, and Australia collectively contribute over 50% of global mining project investments, creating substantial demand for containment liner solutions. China's progressive tightening of solid waste disposal regulations is compelling adoption of GCL-inclusive liner systems in new landfill projects, expanding the country's addressable market beyond historically dominant compacted clay liner practices.

MEA & Latin America Geosynthetic Clay Liner (GCL) Market Insights

The regions of the Middle East and Africa along with Latin America make up an important part of the GCL revenue in the global market, constituting percent of the total value of the market by 2025. In the Middle East, the requirement for the use of GCL arises because of the need for containment in industries in the oil and gas industry, building waste management infrastructure facilities in GCC countries, and lining of reservoirs and canals due to lack of water resources. UAE and Saudi Arabia make two important markets for GCLs as there is a rise in investments for sustainable infrastructure in waste management and water conservation.

More than 150 million cubic meters of water storage capacity is supported by reservoirs, canals, and water conservation projects requiring seepage control solutions. GCC countries invest tens of Millions of dollars annually in water security, wastewater treatment, and environmental infrastructure projects where GCLs are increasingly utilized. Rising lithium and copper mining investments in Latin America are boosting demand for GCL-based containment infrastructure.

Market Dynamics

Growth Drivers: Stringent environmental regulations and expanding containment infrastructure globally

The growth in the GCL market is ultimately dependent upon the global increase in regulation surrounding waste management, mining operations, water treatment, and containment facilities a regulatory trend which invariably necessitates the need for liner systems using GCLs. In the area of landfilling, mandatory regulations under the EPA Subtitle regime in North America, the Landfill Directive in Europe, and increasingly stringent equivalent regimes in Asia Pacific and Latin America ensure that liner system designs utilizing GCL products are an absolute necessity in hundreds of new and expanding disposal sites each year. In the mining industry, increased expenditure on mineral extraction around the world, especially those used in batteries and precious metals, is ensuring a pipeline of containment facilities utilizing liner systems.

Restraints: Competition from alternative liner systems and installation complexity in challenging environments

GCLs encounter continual competition from other types of liner systems such as CCLs in places where there is sufficient availability of locally abundant clay and cheap labor, as well as from HDPE and other geomembrane-only liners for applications where regulatory requirements regarding minimum level of performance of the liner are achievable using only geomembranes without the use of a clay layer. In economically challenging environments, the higher cost of installation of GCL compared to that of locally produced clay liners may pose difficulties for adoption of such liners. GCLs’ vulnerability to interactions with site-specific leachate chemicals may be another engineering challenge for some industrial and mining sites where customized or chemically altered polymer liners must be used.

Opportunities: Mining sector expansion and water management infrastructure investment in emerging markets

This is especially true for the GCL market because the market is set to benefit from the following two opportunity drivers during the forecast period of 2026-2035. Firstly, the worldwide increase in the mining of critical minerals and precious metals due to the demand for such minerals such as lithium, cobalt, and copper as part of the energy transition is generating a substantial pipeline of mining containment infrastructure, in which the deployment of GCLs is being encouraged in Latin America, Africa, and the Asia-Pacific region. Secondly, there has been an increase in water scarcity around the world, leading to investment into reservoirs, lined canals, and water storage infrastructure in the Middle East, South Asia, and Sub-Saharan Africa regions.

Recent Developments:

-

2025: CETCO (Minerals Technologies Inc.) launched an enhanced polymer-modified bentonite GCL range for hazardous waste and mining containment applications, strengthening its presence across North America and Europe.

-

2025: Solmax acquired a regional geosynthetics manufacturer in South America, expanding its distribution network and technical support capabilities in key mining markets including Brazil, Chile, and Peru.

-

2026: NAUE GmbH & Co. KG introduced its next-generation Bentofix NSP reinforced GCL series featuring advanced needle-punch technology for landfill, mining, and water management projects.

-

2026: HUESKER Synthetic GmbH expanded European production capacity for its GCL solutions to address rising demand from landfill and waste containment infrastructure projects.

Geosynthetic Clay Liner (GCL) Market Key Players are:

-

CETCO (Minerals Technologies Inc.)

-

Solmax

-

NAUE GmbH & Co. KG

-

HUESKER Synthetic GmbH

-

Officine Maccaferri S.p.A.

-

AGRU America Inc.

-

TenCate Geosynthetics

-

Thrace Group

-

Layfield Group Ltd.

-

Terrafix Geosynthetics Inc.

-

ABG Ltd.

-

Carthage Mills Inc.

-

GeoSolutions Inc.

-

Geofabrics Australasia Pty Ltd.

-

Global Synthetics Pty Ltd.

-

Polyfabrics Australasia Pty Ltd.

-

Titan Environmental Containment Ltd.

-

ACE Geosynthetics Enterprise Co. Ltd.

-

Atarfil S.L.

-

BPM Geosynthetics

Geosynthetic Clay Liner (GCL) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 496.31 Million |

| Market Size by 2035 | USD 808.87 Million |

| CAGR | CAGR of 5.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Needle-Punched GCL, Reinforced GCL, Unreinforced GCL, Adhesive-Bonded GCL, Stitch-Bonded GCL) • By Raw Material (Sodium Bentonite GCL, Calcium Bentonite GCL, Polymer-Modified Bentonite GCL, Others) • By End-Use Industry (Waste Management, Mining, Water Management, Construction & Infrastructure, Oil & Gas, Energy & Power) • By Application (Landfill Liners & Caps, Mining Containment, Water Containment Reservoirs & Canals, Wastewater Treatment Facilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CETCO (Minerals Technologies Inc.), Solmax, NAUE GmbH & Co. KG, HUESKER Synthetic GmbH, Officine Maccaferri S.p.A., AGRU America Inc., TenCate Geosynthetics, Thrace Group, Layfield Group Ltd., Terrafix Geosynthetics Inc., ABG Ltd., Carthage Mills Inc., GeoSolutions Inc., Geofabrics Australasia Pty Ltd., Global Synthetics Pty Ltd., Polyfabrics Australasia Pty Ltd., Titan Environmental Containment Ltd., ACE Geosynthetics Enterprise Co. Ltd., Atarfil S.L., BPM Geosynthetics. |

Frequently Asked Questions

The geosynthetic clay liner (GCL) market is expected to grow at a CAGR of 5.07% from 2026 to 2035.

The geosynthetic clay liner (GCL) market was valued at USD 496.31 Million in 2025.

Key growth drivers include stricter environmental regulations, expanding mining containment projects, and rising investments in water management infrastructure worldwide.

Stitch-Bonded GCL is the fastest-growing product type in the geosynthetic clay liner (GCL) market.

North America dominated the Geosynthetic Clay Liner Market in 2025, accounting for 32.15% of global revenues, with the United States representing 84.54% of North American revenues.

Get in Touch