Golf Simulators Market Report Scope & Overview:

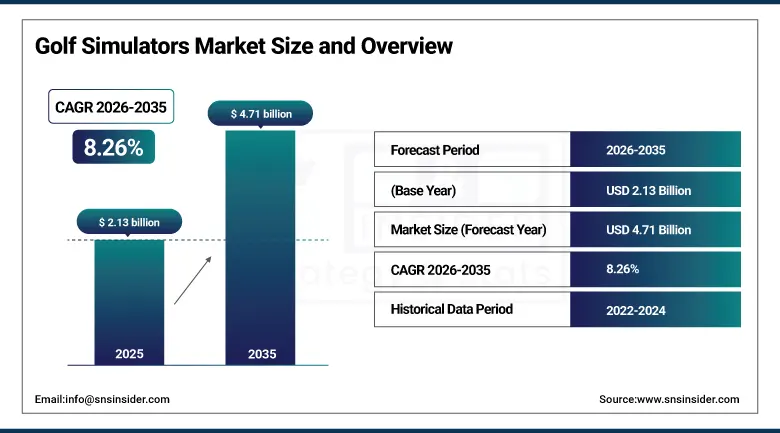

The Golf Simulators Market was valued at USD 2.13 Billion in 2025 and is expected to reach USD 4.71 Billion by 2035, growing at a CAGR of 8.26% from 2026 to 2035.

The Golf Simulators market is witnessing tremendous growth, driven by the increasing consumer desire for engaging in sports activities indoors throughout the year, the increasing trend of building recreational facilities at home, and technological advancements in simulators. The development of VR technologies, artificial intelligence, and sensor technology has enhanced the experience of simulators to an extent that makes them attractive for not only recreational use but also training purposes.

Golf Simulators Market Size and Forecast

-

Market Size in 2025: USD 2.13 Billion

-

Market Size by 2035: USD 4.71 Billion

-

CAGR: 8.26% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Golf Simulators Market - Request Free Sample Report

Golf Simulators Market Trends

-

Strong growth in residential installations as homeowners invest in dedicated indoor golf practice environments.

-

Rising adoption of VR-integrated simulators that offer immersive, multi-course virtual golf experiences to consumers.

-

Increasing use of AI-based swing analysis and performance coaching tools embedded within simulator platforms.

-

Cloud-based multiplayer features gaining traction, with approximately 25% of simulator systems now enabling online competitive play.

-

Commercial venues such as sports bars, golf academies, and hospitality properties adding simulators as premium service offerings.

-

Declining hardware costs broadening market accessibility beyond high-income consumer segments and premium clubs.

-

Corporate event organizers increasingly incorporating simulator experiences into team-building and entertainment packages.

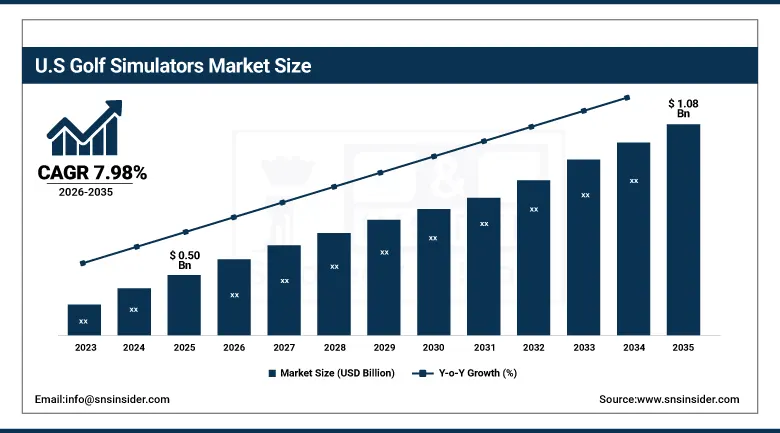

U.S. Golf Simulators Market was valued at USD 0.50 Billion in 2025 and is expected to reach USD 1.08 Billion by 2035, registering a CAGR of 7.98% during 2026–2035.

The United States is by far the biggest national market for golf simulators worldwide, making up an unusually high proportion of both commercial and home-based golf simulators. It has a rich culture of playing golf, with more than 25 million active golf players who constitute a ready market for golf simulators. The extremely cold winters in some parts of the country limit year-round playing outdoors, thus necessitating indoor golf simulators throughout the year.

Golf Simulators Market Segment Insights

-

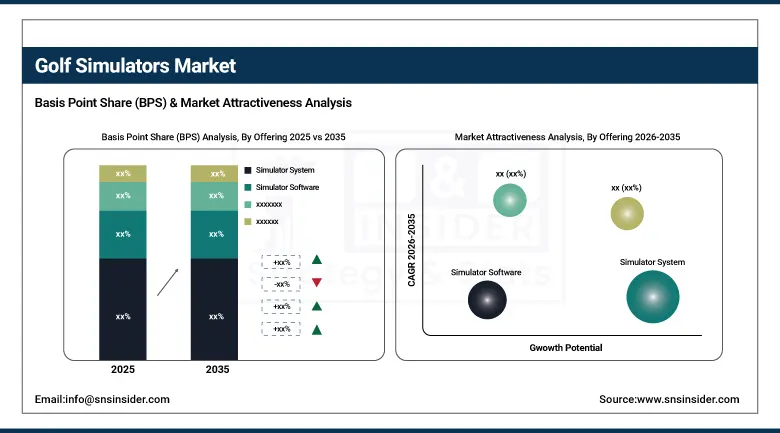

Based on Offering, Simulator System accounted for the largest market share at 53.10% in 2025; Simulator Services expected to be the fastest-growing segment with a CAGR of 13.5%.

-

Based on Product, Portable Simulators held a dominant share of 64.8% in 2025; Built-in Simulators expected to be the fastest-growing segment at a CAGR of 12.3%.

-

Based on Simulator Type, Full Swing Simulators accounted for 70.7% share in 2025; VR Golf Simulators expected to be the fastest-growing segment at a CAGR of 12.2%.

-

Based on Application, Commercial Spaces held 51.6% market share in 2025; Residential segment expected to grow at the highest CAGR of 12.0%.

-

Based on Distribution Channel, Direct Sales held more than 62.4% share in 2025 and is also projected to be the fastest-growing channel.

Golf Simulators Market Segment Analysis

By Offering, Simulator System dominates the Golf Simulators Market, Simulator Services expected to grow fastest

Among the segments, the Simulator Systems category occupied the highest share in the Golf Simulators Market in 2025. The market share of the Simulator Systems segment is estimated to be about 53.10%. These refer to the basic hardware components that make up a golf simulator such as screens, sensors, projectors, launch monitors, computing unit, etc. Such an important position of the segment stems from the nature of transactions that take place in the golf simulators market. In particular, buying equipment is the main deal in the discussed niche. Therefore, given further improvements of the quality of hardware and reduced prices due to intensified competition among producers, the leader position will not change during the forecasted period.

The segment growing at the highest rate from 2026 to 2035 is that related to the provision of Simulator Services. This includes installation, maintenance, software updates, and other services offered by suppliers. The growth rate for this segment is predicted to reach the value of 13.5%. It correlates with the overall trends in the hardware technology industry when vendors focus on gaining revenues from providing services rather than from the sales of products.

By Product, Portable Simulators dominate the Golf Simulators Market, Built-in Simulators expected to grow fastest

The Portable Simulators have gained the lion’s share in the product type segment and accounted for 64.8% share of total volume in 2025. The ease of usage, easy installation, as well as affordable initial cost when compared to other permanently built systems are some of the attributes which make portable simulators attractive for a large number of users. Such devices are particularly preferred by individual golfers since they allow practicing without investing in an elaborate set-up of the infrastructure. They can be also moved to a different place where they will be utilized depending on the event.

Meanwhile, the Built-in Simulators have been forecast to post the fastest growth rate with the CAGR of 12.3% up to 2035. With more players focusing on developing highly immersive and advanced environments as a way to increase prices and justify investments in expensive infrastructure, the demand for professionally made simulator installations becomes higher. In terms of the end-users, Hotels & Entertainment Venues and Sports Clubs are anticipated to account for the lion’s share of the Built-in Simulators sales volume.

By Simulator Type, Full Swing Simulators dominate the Golf Simulators Market, VR Golf Simulators expected to grow fastest

Full Swing Simulators dominated the market, accounting for 70.7% of sales in 2025 due to their status as the predominant standard format for consumer and commercial golf simulation. Full swing systems employ high-speed cameras or infrared sensors to capture a variety of data on ball flight trajectories, launch angles, spin speeds, and swing patterns, all of which can be used to analyze and improve golfing skills. Full swing systems' credibility within the golfing community, as well as their affordable price range, make them the default purchase for new entrants into the market.

The market's VR Golf Simulators category will record the highest CAGR during the forecast period, at 12.2% from 2026 to 2035. Unlike traditional simulators that project images of courses and other golf elements onto screens, VR-based systems allow players to experience simulated golf in fully immersive digital environments. VR-based simulators appeal to technologically savvy individuals and entertainment venues where the novelty factor plays a role in attracting customers. As VR headset technology advances and virtual reality course content expands, VR Golf Simulators will likely gain an increasing market share due to their unique offerings.

By Application, Commercial Spaces dominate the Golf Simulators Market, Residential segment expected to grow fastest

Application-wise, Commercial Spaces was the leading segment with a market share of 51.6% in 2025. Golf clubs, sports academies, entertainment centers, sports bars, and other corporate hospitality facilities are becoming increasingly important customers for simulator systems as they seek to use simulators as a tool for attracting members, increasing visitor flows, and offering top-notch recreational services. The commercial category enjoys advantages related to the bulk buying process, demand for professional installation, and ongoing maintenance agreements, which allow for raising transaction values. In addition, the emergence of new entertainment golf formats that involve playing golf with meals and drinks makes a considerable contribution.

The Residential segment is forecast to show the strongest growth rate out of all application categories, reaching CAGR of 12.0% through 2035. Homeowners who possess recreation zones in their houses are seeing a home golf simulator as something worthy of being invested into. Changes brought by the pandemic in the form of the rise in telecommuting hours increase free time people spend at home, leading to a shift in discretionary expenditures in favor of home entertainment equipment. Improvements in hardware and affordability also make it easier for companies to sell products to homeowners.

By Distribution Channel, Direct Sales dominate the Golf Simulators Market

The share of Direct Sales was higher than 62.4% of the distribution channel segment in 2025, and this segment is also expected to exhibit the highest CAGR during the forecast period. With direct sales channels such as websites of the manufacturers, authorized dealers, and demonstration centers, brands can have control over the entire purchase process, convey technical details, and establish contact directly with business buyers. In cases of customized products with installation and service agreements, direct involvement of the buyer and the manufacturer is the best method for procurement.

The Indirect Channel, which comprises online stores and specialized sport equipment shops, is witnessing growth because of the rising penetration of cost-effective portable devices among first-time users who choose to buy on their own. With the rise in e-commerce in the sport equipment industry, there is an increase in demand for budget-conscious households that buy basic models online without face-to-face interactions.

Golf Simulators Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

67% |

|

Europe |

United Kingdom |

34% |

|

Asia Pacific |

South Korea |

38% |

|

Middle East & Africa |

UAE |

30% |

|

Latin America |

Brazil |

48% |

North America Golf Simulators Market Insights

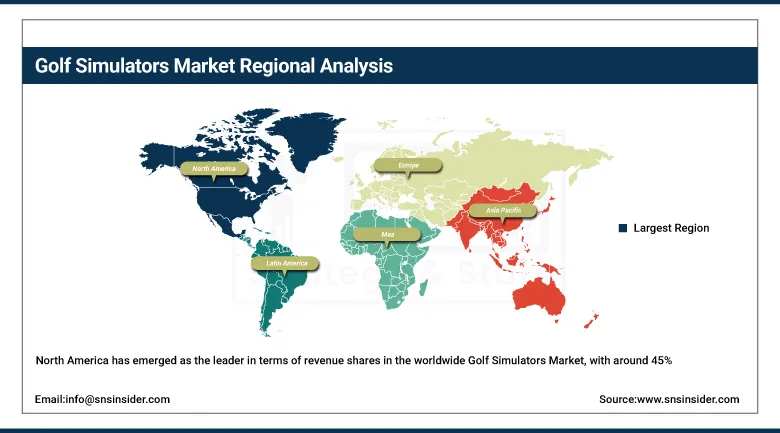

North America has emerged as the leader in terms of revenue shares in the worldwide Golf Simulators Market, with around 45% of global market share accounted for by North America in 2025. This is driven mainly due to the USA, which hosts one of the largest populations of golf players in the world alongside an active recreational sector that favors luxury leisure services. Availability of advanced technologies provided by major simulator vendors such as Full Swing Golf, TrackMan, and SkyTrak, which have operations in North America, is one of the key driving factors.

Colder climate during winters in northern states of the US as well as Canada creates a demand for indoor golfing activities independent of any trends in terms of purchases. The commercial and residential markets are well developed with thousands of units installed each year. Enterprise application is increasingly gaining ground via corporate events, hotels, and entertainment centers, and it is forecasted that North America will remain the topmost performer until 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Golf Simulators Market Insights

Asia-Pacific is set to exhibit the largest CAGR in the Global Golf Simulators Market during 2028-2035, fueled by the increasing popularity of golf in countries such as South Korea, Japan, China, and Southeast Asia. South Korea is particularly notable within the region because, for example, Golfzon alone runs most of the indoor golf simulators in the country while exporting their technologies to other countries as well. The densely urbanized cities in Asia coupled with limited land availability have favored the uptake of smaller and superior indoor golf simulation options.

Increased disposable income levels among the rising middle class in China and Southeast Asian countries have expanded the target market for premium recreational technology products. Growing investments in sports infrastructure by governments and corporate spending on hospitality in some countries are further driving installations. Asia-Pacific is anticipated to witness an intensifying competition in local production as well as adoption of foreign simulators looking to expand into fast-growing national markets.

Europe Golf Simulators Market Insights

Europe constitutes a well-established market for golf simulators with a share of around 29% in terms of revenues across the globe in 2025. There is notable activity in the UK and Germany as the countries actively invest in the development of golf academies, facilities offering training services year-round, as well as entertainment establishments where golf simulators are installed to attract more visitors. Consumers in Europe are interested in employing simulators in a training capacity, meaning the demand for professional-grade simulators capable of producing reliable performance analysis data will increase.

There is also an important niche created by the European golf tourism market valued at several billions. It provides another source of demand, creating the need for installations in hotels and resorts enabling guests to play golf despite adverse climatic conditions. Countries of Northern Europe as well as other continental markets where the climate features wet or cold seasons have demonstrated increased adoption rates of simulation technologies in such circumstances. The region will experience steady growth until 2035.

Middle East & Africa and Latin America Golf Simulators Market Insights

The Middle East & Africa and Latin America segments will serve as developing markets for golf simulation products driven by increasing expenditures on urban leisure entertainment, growing engagement in high-end leisure activities, and booming commercial hospitality businesses. Within the Middle East region, the UAE will spearhead market development in terms of premium leisure installations within hotels and golf resorts that cater to the demands of wealthy tourists and local residents who are engaging in premium sports activities. Investment into expansive leisure and entertainment infrastructures in GCC nations will present numerous commercial prospects for simulator suppliers.

In Latin America, Brazil will be the leading country in terms of the market, where the majority of growth will be derived from upscale commercial establishments, private clubs, and corporate event centers. Both market segments remain at an earlier stage of development, which suggests that the market base remains small and percentage growth figures during the period between 2026 and 2035 will be significant. As awareness regarding simulator technologies increases and more cost-effective products become available within these markets, domestic installations will contribute to regional revenues.

Golf Simulators Market Growth Drivers:

-

Rising demand for year-round indoor sports recreation and home-based entertainment

The primary factor driving the Golf Simulators Market is the rising demand for affordable sports activities that are independent of weather conditions and can be pursued throughout the year. Many golf enthusiasts find themselves unable to frequently attend actual courses owing to factors such as urbanization, tight schedules, and geographical constraints; the availability of simulators offers them an alternative solution for indoor activities. In recent years, the rise in expenditure on leisure at home has made consumers more receptive to high-end sports equipment indoors.

Commercial operators across the hospitality, entertainment, and fitness sectors are also recognizing the revenue potential of simulator installations, which attract new customers, extend visit durations, and generate premium pricing opportunities. The convergence of entertainment and sports in hybrid venues is creating a structural new demand channel that was not meaningfully present a decade ago. This dual growth from both individual consumers and commercial operators gives the market a broad and resilient demand foundation going into the 2026 to 2035 forecast period.

Golf Simulators Market Restraints

-

High upfront equipment and installation costs limiting mass-market accessibility

One of the major factors restraining the growth of this market on a global basis would be the large amount of money that is needed to create high-performance simulation systems. Commercial grade simulators may cost much more than USD 50,000 once all expenses related to hardware installation, screens installation, and necessary room preparations are taken into account. As a result, such simulators will be available for purchase only by those consumers who have sufficient income and are ready to make expensive investments, along with commercial enterprises having large financial budgets. Thus, the cost factor will prevent any substantial expansion of this market towards middle and low-cost consumers. At the same time, residential customers face certain limitations associated with the necessity to find a place with sufficient size, height, and lighting conditions. In turn, this prevents them from using portable systems, which tend to be significantly cheaper and occupy less space. Nevertheless, it should be noted that portable simulators do not guarantee a similar level of accuracy compared to fixed ones.

Golf Simulators Market Opportunities

-

Expansion of VR-integrated and AI-powered simulation platforms for personalized training and entertainment

With such fast-moving development of both VR technology and AI analytics, there exists an excellent business opportunity for simulator producers to launch unique products that cannot be offered by conventional golf training equipment. Indeed, AI coaching applications capable of analyzing the user's swing, body posture, club trajectory, and ball flight can transform simulators into highly valuable tools for improving player performance. Such positioning will greatly expand the attractiveness of this market from recreational golfers to competitive amateurs, professional players, and even athletes taking part in various coaching programs. Virtual reality can help manufacturers extend their reach even further, capturing the attention of customers who may not necessarily consider themselves golfers yet can be attracted to a virtual golf game through VR technology. Cloud connectivity allowing for multiplayer virtual tournaments is one of the ways for adding value to the offering of manufacturers and creating additional sources of revenue. Companies that will be able to create a complete digital ecosystem around their hardware, along with paid subscriptions for its users, will enjoy strong retention and steady income generation well beyond 2035.

Recent Developments:

-

2026: Several major simulator manufacturers accelerated integration of real-time AI swing coaching features into their platforms, with cloud-based analytics dashboards allowing golfers to track performance improvement over time and access instructor feedback remotely.

-

2025 (Q2): Golfzon secured a USD 50 million Series B funding round aimed at accelerating global market expansion and investing in next-generation simulator technologies, reinforcing the company's ambition to grow its already dominant position in Asia and expand into Western markets.

-

2025 (Q2): Foresight Sports entered a formal partnership with the PGA Tour to develop and commercially launch official PGA Tour-branded simulator experiences targeting both commercial venues and high-end residential buyers, significantly raising the profile of simulator-based entertainment.

Golf Simulators Market Key Players

Some of the Golf Simulators Market Companies

-

TrackMan – TrackMan Golf Simulator

-

Full Swing Golf – Full Swing Pro Series

-

Foresight Sports – GCHawk Simulator System

-

Golfzon – Golfzon Vision Series

-

SkyTrak – SkyTrak+ Launch Monitor

-

OptiShot Golf – OptiShot 2 Simulator

-

TruGolf – APX Series Simulator

-

AboutGolf – aG Series Simulators

-

Ernest Sports – ES16 Tour Simulator

-

Uneekor (Creatz) – QED Simulator System

-

Flightscope – Mevo+ Launch Monitor System

-

Garmin – Approach R10 Launch Monitor

-

Rapsodo – MLM2PRO Launch Monitor

-

X-Golf – Commercial X-Golf Simulator

-

ProTee United – ProTee Play System

Golf Simulators Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.13 Billion |

| Market Size by 2035 | USD 4.71 Billion |

| CAGR | CAGR of 8.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Offering (Simulator System, Simulator Software, Simulator Services) • By Product (Portable Simulators, Built-in Simulators) • By Simulator Type (Full Swing Simulators, VR Golf Simulators) • By Application (Commercial Spaces, Residential, Colleges and Universities, Corporate Events) • By Distribution Channel (Direct Sales, Indirect Channels) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | TrackMan, Full Swing Golf, Foresight Sports, Golfzon, SkyTrak, OptiShot Golf, TruGolf, AboutGolf, Ernest Sports, Uneekor (Creatz), Flightscope, Garmin, Rapsodo, X-Golf, ProTee United |

Frequently Asked Questions

North America dominated the Golf Simulators Market in 2025, accounting for approximately 40 to 45% of global revenue share.

The Simulator System segment dominated the Golf Simulators Market in 2025, accounting for 53.10% of market share.

The major growth factor is the rising demand for year-round indoor sports recreation and home-based entertainment, combined with technological advancements in simulation software, VR integration, and AI-powered swing analytics.

The Golf Simulators Market was valued at USD 2.13 Billion in 2025.

The Golf Simulators Market is expected to grow at a CAGR of 8.26% from 2026 to 2035.

Get in Touch