Guidewires Market Report Scope & Overview:

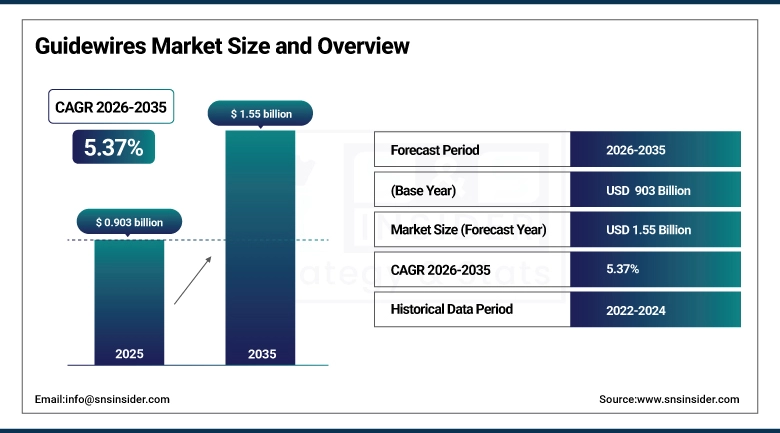

The Guidewires Market was valued at USD 0.903 billion in 2025 and is expected to reach USD 1.55 billion by 2035, growing at a CAGR of 5.37% from 2026-2035.

In interventional medicine, access is everything the ability to navigate a catheter, stent, or therapeutic device to a precise anatomical destination through tortuous vessels, narrow passages, and complex lesion architectures. The guidewire is the first thing that enters the body and the last thing that leaves during most minimally invasive vascular and endoluminal procedures, functioning as the navigator that all subsequent devices follow into position. Getting this access right on the first attempt, without vessel injury, wire perforation, or the time-consuming exchanges that complicate multi-lesion cases, is the procedural goal that guidewire engineering is relentlessly pursuing. Hydrophilic polymer coatings that virtually eliminate friction in tortuous vessels, nitinol cores that provide superelastic kink resistance while maintaining the tactile feedback interventionalists rely on to feel what the wire is doing, variable stiffness designs that are floppy at the tip but firm in the shaft for pushability each of these is a technical solution to a specific procedural challenge, and each has created market categories where premium guidewires command price premiums that justify continued investment in materials science and coating technology.

The World Health Organization's cardiovascular disease statistics document that coronary artery disease the primary application for coronary guidewires accounts for approximately 9 million deaths annually, making it the world's leading cause of death. The American College of Cardiology documents that over 900,000 percutaneous coronary intervention (PCI) procedures are performed in the U.S. annually, each requiring at least one coronary guidewire.

Guidewires Market Size and Forecast

-

Market Size in 2025: USD 0.903 billion

-

Market Size by 2035: USD 1.55 Billion

-

CAGR: 5.37% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Guidewires Market - Request Free Sample Report

Guidewires Market Trends

-

Robotic-assisted coronary intervention systems including Corindus CorPath GRX are creating demand for guidewire designs compatible with remote robotic manipulation that must maintain performance characteristics under mechanical actuation different from manual wire handling.

-

Chronic Total Occlusion (CTO) guidewire technology is advancing with new polymer jacket designs, tapered micro-tip configurations, and stiffness profiles optimized for retrograde and antegrade crossing approaches in complex calcified lesions.

-

Neurovascular guidewires are reaching new anatomical destinations as neurointerventionalists advance catheter-based stroke treatment, mechanical thrombectomy, and flow diverter placement into increasingly distal cerebral vasculature.

-

Hydrophilic coating formulation improvements are reducing thrombus formation on guidewire surfaces during prolonged procedural dwell times, addressing a safety concern that has affected complex multi-vessel and multi-access interventional cases.

-

Biodegradable polymer coating development is addressing the embolic risk of hydrophilic coating particle shedding in critical vessels, with several manufacturers advancing clinical validation of next-generation bioresorbable coating systems.

-

Microcatheter and guidewire combination systems for the most challenging access targets including tiny coronary collaterals, spinal artery feeders, and distal pulmonary vessels are expanding interventional capabilities while creating premium market segments.

-

Pressure-sensing guidewires that measure fractional flow reserve at the same time as providing mechanical wire function are simplifying coronary physiology measurement workflows by eliminating the need for adenosine infusion in IVUS-guided PCI.

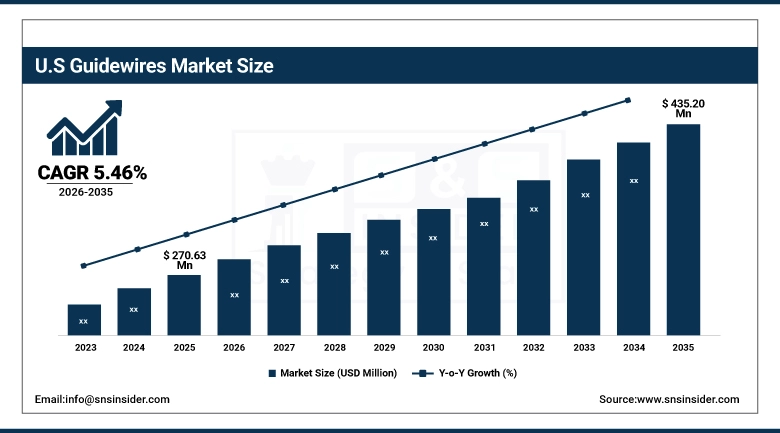

U.S. Guidewires Market was valued at USD 270.63 million in 2025 and is expected to reach USD 435.20 million by 2035, growing at a CAGR of 5.46%.

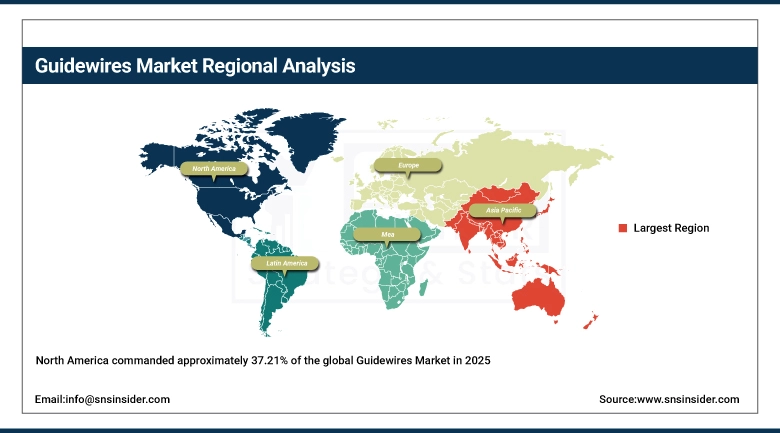

North America dominated the Guidewires Market with approximately 37.21% revenue share in 2025, driven by the United States' combination of the world's highest percutaneous coronary intervention procedure volumes, advanced healthcare infrastructure, favorable reimbursement for interventional procedures, and the headquarters of leading guidewire manufacturers including Boston Scientific, Abbott, and Teleflex. The U.S. market's commercial sophistication is reflected in its rapid adoption of premium guidewire technologies CTO-specific guidewires, pressure-sensing guidewires, and advanced hydrophilic-coated designs are adopted in the U.S. market with shorter lag times from clinical validation to commercial uptake than any other national market. U.S. cardiovascular disease demographics with baby boomer aging creating growing volumes of elderly patients requiring coronary intervention sustain the procedure volume foundation that makes guidewire market growth reliable.

The Society for Cardiovascular Angiography and Interventions 2024 data shows that U.S. PCI volumes recovered to 98% of pre-pandemic levels by 2023 and have been trending upward through 2024, driven by aging demographics and expanded reimbursement for complex PCI including CTO procedures. Abbott's Vascular division, Boston Scientific's Interventional Cardiology division, and Asahi Intecc collectively hold an estimated 65% of the U.S. coronary guidewire market by revenue.

Guidewires Market Segment Analysis

-

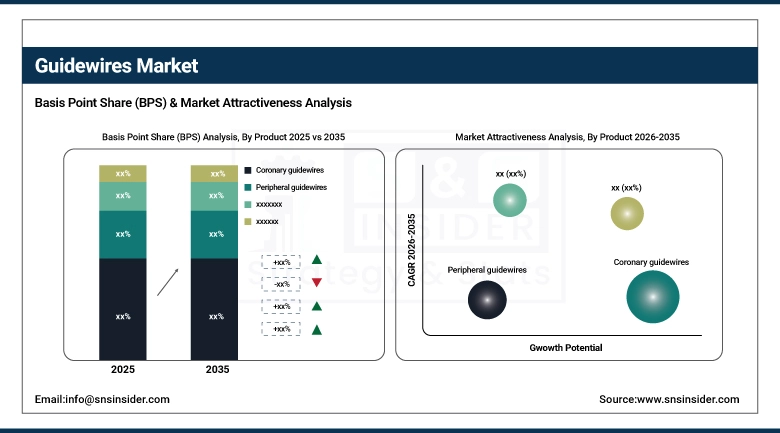

By Product, Coronary Guidewires dominated with 42.56% share in 2025; Peripheral and Neurovascular growing fastest.

-

By Material, Stainless Steel dominated the Guidewires Market in 2025; Nitinol fastest growing (CAGR).

-

By Application, Cardiology dominated the Guidewires Market in 2025; Neurology growing at fastest CAGR.

-

By End-User, Hospitals dominated the Guidewires Market in 2025; ASCs and Research Institutes growing.

By Product: Coronary Guidewires dominate at 42.56%, Peripheral and Neurovascular growing

Coronary Guidewires held approximately 42.56% of the Guidewires Market in 2025, reflecting the global burden of coronary artery disease as the world's leading cause of death and the established standard of care for PCI as the primary treatment for obstructive coronary artery disease. Every percutaneous coronary intervention balloon angioplasty, stent implantation, rotational atherectomy, intravascular lithotripsy begins with a coronary guidewire crossing the lesion to provide the access track over which all subsequent devices are delivered. The coronary guidewire market spans a wide performance spectrum: workhorse guidewires used in the majority of straightforward lesions, soft floppy-tip wires for fragile or tortuous vessels, intermediate support wires for lesions requiring device delivery force, and dedicated CTO guidewires with progressively aggressive tip designs for crossing the organized fibrous tissue of chronic total occlusions.

Peripheral Guidewires serving lower extremity arterial intervention, renal and mesenteric artery procedures, deep venous interventions, and structural heart disease access are growing as peripheral arterial disease's prevalence grows with the aging of populations in developed markets and as endovascular treatment displaces open surgical bypass for an expanding range of peripheral vascular lesion types. The BEST-CLI and BASIL-2 trials comparing endovascular versus surgical strategies in peripheral arterial disease have influenced practice patterns in ways that sustain endovascular approach adoption, creating consistent guidewire procedure volume growth. Neurovascular Guidewires used in cerebral aneurysm coiling, arteriovenous malformation embolization, mechanical thrombectomy for acute ischemic stroke, and carotid stenting are the fastest-growing product type, driven by acute stroke's emergence as one of the most actively treated time-sensitive emergencies in modern medicine.

The American Heart Association's 2023 Heart Disease and Stroke Statistics document that approximately 795,000 Americans suffer a stroke annually, with mechanical thrombectomy which uses specialized neurovascular guidewires, aspiration catheters, and stent retrievers now the standard of care for large vessel occlusion stroke presenting within 24 hours, creating growing neurovascular guidewire procedure volumes at comprehensive stroke centers.

By Material: Stainless Steel dominates, Nitinol growing fastest

Stainless Steel maintained the dominant material position in the Guidewires Market in 2025, driven by its established performance profile high tensile strength, excellent torque transmission, reliable kink resistance at moderate curvatures, and predictable tip behavior under fluoroscopic visualization that has made stainless steel the material specification for a large proportion of workhorse guidewires used in routine interventional procedures. Stainless steel's cost advantage over nitinol reflecting the simpler metallurgy and manufacturing processes of steel versus the precise thermal processing required for nitinol's shape memory properties sustains its commercial position in price-sensitive market segments. Standard 0.014-inch coronary workhorse guidewires in stainless steel are high-volume commodity products where manufacturing scale determines competitive position more than material specification.

Nitinol is the fastest-growing material, driven by its unique superelastic properties that deliver kink resistance and shape recovery advantages that stainless steel cannot match in the most technically challenging anatomical territories. Nitinol's ability to undergo large elastic deformation up to 8% recoverable strain versus 0.2% for stainless steel means that a nitinol guidewire traversing a severely tortuous coronary segment recovers its designed shape as it exits the bend, while a stainless-steel wire of equivalent diameter would plastically deform and become unusable. In neurovascular applications where cerebral vessels have much smaller diameters and tighter tortuosity than coronary vessels nitinol’s superelastic advantages make it the material of choice for the most demanding access challenges. Asahi Intec one of the world's leading nitinol guidewire manufacturers has built its market position around superior nitinol wire drawing expertise that produces guidewires with tighter dimensional tolerances and more consistent mechanical properties than competitors achieve with the same material.

By Application: Cardiology dominates, Neurology growing fastest

Cardiology held the dominant application position in the Guidewires Market in 2025, encompassing the coronary, structural heart, and peripheral vascular interventional procedures that collectively generate the majority of global guidewire consumption. Interventional cardiology's broad reach treating angina with PCI, correcting valvular heart disease with TAVR and MitraClip, occluding left atrial appendages to prevent stroke in atrial fibrillation patients, closing patent foramen ovale defects creates diverse guidewire demand across a wide range of wire diameters, stiffnesses, and tip configurations. The expansion of structural heart disease interventions has been particularly significant, creating demand for specific guidewires and wires optimized for transapical and transseptal access routes that did not exist as major commercial categories a decade ago.

Neurology is expected to grow at the fastest application CAGR, driven by the acute ischemic stroke treatment revolution that mechanical thrombectomy represents and the expanding neurointerventional treatment options for previously untreatable cerebrovascular diseases. The 2015 publication of five major randomized controlled trials demonstrating mechanical thrombectomy's superiority over medical management alone for large vessel occlusion stroke transformed stroke care essentially creating the acute neurointerventional subspecialty at scale rather than as a rare tertiary center activity. Each thrombectomy procedure consumes multiple neurovascular guidewires along with aspiration catheters and stent retrievers, creating a high per-procedure device cost that generates premium revenue for guidewire manufacturers in this application.

By Application, Cardiology dominated the Guidewires Market in 2025, driven by extensive use in coronary, structural heart, and peripheral vascular interventions including PCI, TAVR, MitraClip, and LAA closure procedures, which collectively generate the highest global guidewire consumption; Neurology is emerging as the fastest-growing segment, fueled by the rapid expansion of mechanical thrombectomy for acute ischemic stroke, increasing adoption of neurointerventional therapies, and rising treatment of complex cerebrovascular disorders requiring multiple specialized guidewires per procedure.

By End-User: Hospitals dominate, ASCs and Research Institutes expanding rapidly

Hospitals dominated the Guidewires Market in 2025 due to their central role as primary care centers for complex cardiovascular, neurovascular, and peripheral interventional procedures. They are equipped with advanced imaging systems, catheterization laboratories, and specialized clinical teams that enable the performance of a wide range of high-acuity procedures such as PCI, mechanical thrombectomy, structural heart interventions, and endovascular repairs. This extensive procedural capability leads to consistent and large-scale usage of guidewires across diagnostic and therapeutic applications, making hospitals the most significant end-user segment in the market.

Ambulatory Surgical Centers (ASCs) are emerging as the fastest-growing end-user segment, supported by the increasing shift toward minimally invasive, cost-effective outpatient procedures that allow quicker patient recovery and reduced healthcare burden on hospitals. ASCs are gradually expanding their role in performing selected cardiovascular and peripheral vascular interventions, particularly for lower-complexity cases. Research Institutes are also witnessing steady growth, driven by ongoing clinical research activities, technological advancements, and the development of next-generation guidewire technologies focused on improving navigation, flexibility, and precision in complex anatomical conditions.

Guidewires Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

North America Guidewires Market Insights

North America commanded approximately 37.21% of the global Guidewires Market in 2023 and maintained its dominant position in 2025, sustained by the U.S. healthcare system's extraordinary investment in cardiovascular and neurovascular interventional infrastructure. The concentration of leading guidewire manufacturers Boston Scientific in Marlborough, Massachusetts; Abbott Vascular in Santa Clara, California; Teleflex in Wayne, Pennsylvania; and Cook Medical in Bloomington, Indiana sustains both strong domestic product development and the commercial relationships with hospital systems and group purchasing organizations that make U.S. adoption of innovative guidewire designs commercially efficient. Favorable U.S. reimbursement for complex PCI, including CTO procedures and structural heart disease interventions, sustains procedure volumes that are accessible to guidewire technology innovation in ways that cost-controlled health systems in other countries cannot easily match.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Guidewires Market Insights

Asia Pacific is the fastest-growing regional Guidewires Market with an expected CAGR of 6.45%, driven by Japan's world-class interventional cardiology program Asahi Intecc, a Japanese company, is among the world's leaders in premium coronary guidewire technology China’s enormous and growing cardiac catheterization program, India's expanding interventional cardiology capacity, and South Korea's sophisticated healthcare system with high PCI procedure volumes. Japan contributes uniquely to the guidewire market in both supplier and consumer dimensions: it hosts Asahi Intecc and Terumo Corporation two of the world's most technically sophisticated guidewire manufacturers and its domestic interventional cardiology community is among the world's most demanding in its guidewire performance specifications, driving technical innovation that subsequently spreads globally.

Japan's Cardiovascular Intervention Society data shows that Japan performs approximately 250,000 PCI procedures annually one of the world's highest rates per capita creating a premium guidewire demand that has supported Asahi Intecc's development of the world's most technically advanced CTO guidewire portfolio.

Europe Guidewires Market Insights

Europe holds a significant Guidewires Market position, with Germany, France, the UK, and the Nordic countries as the primary markets. European interventional cardiology and neuroradiology communities are among the world's most technically sophisticated, with active catheterization laboratory networks at major hospitals driving consistent guidewire procurement. The EU Medical Device Regulation (EU MDR 2017/745) compliance requirements which have imposed significant regulatory burdens on guidewire manufacturers have affected product availability in Europe by pushing some smaller manufacturers to exit the European market rather than bear CE marking reapproval costs, creating commercial opportunities for established manufacturers with the regulatory resources to maintain EU MDR compliance across their full product portfolios.

Middle East & Africa and Latin America Guidewires Market Insights

The Middle East's guidewire market is growing with the Gulf states' healthcare infrastructure investment dedicated cardiac centers in Saudi Arabia, UAE, and Kuwait are seeing increasing PCI procedure volumes as cardiovascular disease prevalence in these high-income, high-obesity markets grows. The region's willingness to procure premium medical technology at international prices makes it commercially attractive for guidewire manufacturers despite its modest volume relative to North America and Asia. Latin America's guidewire market concentrates in Brazil, Mexico, and Argentina, where private healthcare sectors maintain PCI programs using premium guidewires while public health system programs use more cost-sensitive products.

Guidewires Market Growth Drivers:

Rising cardiovascular disease burden and minimally invasive procedure preference driving sustained guidewires market growth globally

Guidewire market growth follows two converging demand curves that are each independently growing. Cardiovascular disease incidence is increasing with the aging of global populations coronary artery disease, peripheral arterial disease, and valvular heart disease all predominantly affect patients over 65, and the world has more people over 65 than at any time in history. Simultaneously, the clinical preference for percutaneous catheter-based treatment over open surgical revascularization keeps expanding as clinical evidence demonstrates that minimally invasive approaches achieve equivalent or superior outcomes at lower patient morbidity in an ever-widening range of cardiovascular conditions. Each expansion of minimally invasive treatment indication transcatheter aortic valve replacement, left atrial appendage occlusion, chronic total occlusion PCI adds a new category of guidewire-consuming procedures that sustains market growth beyond the underlying cardiovascular disease incidence trend.

Guidewires Market Restraints:

High product costs and stringent regulatory requirements creating guidewires market access challenges in cost-sensitive markets

Premium guidewires CTO-specific, nitinol-based, or hydrophilic-coated specialty designs command per-unit prices of USD 200-400 that create procurement cost challenges for public hospital systems in developing countries where cardiology programs operate on per-procedure budgets that leave minimal margin for premium device selection. Price-sensitive procurement in developing markets sustains generic and lower-specification guidewire competition from Asian manufacturers whose products meet basic technical specifications at substantially lower price points than branded premium designs. Regulatory clearance requirements FDA 510(k) in the U.S., EU MDR CE marking in Europe, CDSCO approval in India, NMPA registration in China create time-to-market barriers that slow innovative product deployment and add development cost to the economics of guidewire innovation.

Guidewires Market Opportunities:

AI-guided navigation technology and CTO crossing innovation creating significant guidewires market growth opportunities globally

AI integration into interventional procedure guidance represents an emerging opportunity for guidewire technology that blends the physical device with digital intelligence. Robotic-assisted PCI systems including Corindus CorPath already enable guidewire manipulation with robotic precision from a radiation-protected position outside the catheterization laboratory, reducing operator radiation exposure while enabling more precise wire movements than the natural hand tremor inherent in manual manipulation allows. As AI guidance algorithms develop that can interpret real-time fluoroscopic images to suggest optimal wire trajectory adjustments, the combination of AI guidance with precision robotic manipulation could significantly reduce CTO procedure complexity and improve success rates the commercial opportunity being that AI-guided CTO success rates would expand the population of operators comfortable attempting complex procedures, growing the market for CTO-specific guidewires.

Recent Developments:

-

2025: Asahi Intecc launched its Filder XT coronary guidewire with a new proprietary polymer jacket coating providing 35% lower crossing resistance versus its Fielder FC predecessor in quantitative bench testing simulating tortuous coronary anatomy targeting the significant proportion of coronary interventions where wire crossing resistance in complex anatomy is the primary procedural challenge.

-

2025: Boston Scientific received FDA clearance for its ROTAPRO rotational atherectomy system compatible upgrade enabling the use of its Rotawire Extra Support guidewire in combination with the new turbine-free motor design, offering 45% lower guidewire bias force during burr rotation for improved wire position stability during heavily calcified lesion atherectomy.

-

2026: Teleflex Incorporated launched the TrapLiner Microcatheter system with an integrated 0.014-inch nitinol guidewire featuring a novel atraumatic spring coil tip design rated for 45 degrees of tip angulation without loss of torque response, specifically targeting the subset of tortuous peripheral artery disease interventions where conventional guidewires' tip angulation compromises their ability to negotiate complex iliac and femoral arterial anatomy.

Guidewires Market Key Players

Some of the Guidewires Market Companies

-

Boston Scientific Corporation

-

Medtronic plc

-

Abbott Laboratories

-

Terumo Corporation

-

B. Braun Melsungen AG

-

Cardinal Health Inc.

-

Cook Medical LLC

-

Teleflex Incorporated

-

Asahi Intecc Co., Ltd.

-

C.R. Bard Inc. (BD)

-

Stryker Corporation

-

Johnson & Johnson MedTech (Cordis)

-

Nitinol Devices & Components Inc.

-

Lake Region Medical

-

Angiodynamics Inc.

-

Acrostak Corp.

-

OptiMed GmbH

-

Biotronik SE & Co. KG

-

IHT Co. (Interventional Therapies)

-

EPflex Feinwerktechnik GmbH

Guidewires Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.903 Billion |

| Market Size by 2035 | USD 1.55 Billion |

| CAGR | CAGR of 5.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Nitinol Guidewire, Stainless Steel Guidewire, Hybrid Guidewire) • By Product (Coronary Guidewires, Peripheral Guidewires, Urology Guidewires, Neurovascular Guidewires) • By Application (Cardiology, Vascular, Neurology, Urology, Gastroenterology, Oncology, Otolaryngology) • By End-User (Hospitals, Diagnostic Centers, Ambulatory Care Centers, Research Laboratories & Academic Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Terumo Corporation, B. Braun Melsungen AG, Cardinal Health Inc., Cook Medical LLC, Teleflex Incorporated, Asahi Intecc Co., Ltd., C.R. Bard Inc. (BD), Stryker Corporation, Johnson & Johnson MedTech (Cordis), Nitinol Devices & Components Inc., Lake Region Medical, Angiodynamics Inc., Acrostak Corp., OptiMed GmbH, Biotronik SE & Co. KG, IHT Co. (Interventional Therapies), EPflex Feinwerktechnik GmbH |

Frequently Asked Questions

North America dominated with 37.21% share; Asia Pacific is the fastest growing at 6.45% CAGR.

Nitinol is the fastest growing material segment in the Guidewires Market.

Coronary Guidewires dominated with approximately 42.56% share in 2025.

The Guidewires Market was valued at USD 903 million in 2025.

The Guidewires Market is expected to grow at a CAGR of 5.37% from 2026 to 2035.

Get in Touch