Healthcare IT Services Market Report Scope & Overview:

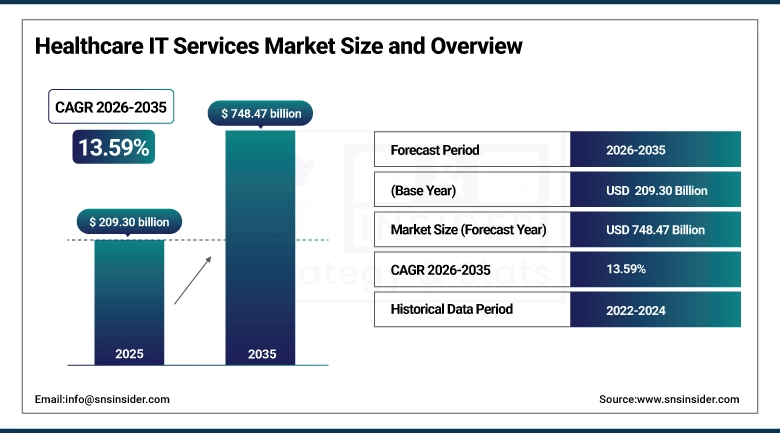

The Healthcare IT Services Market was estimated at USD 209.30 billion in 2025 and is expected to reach USD 748.47 billion by 2035 and grow at a CAGR of 13.59% over the forecast period of 2026-2035.

Factors contributing to the Healthcare IT Services Market include the rapid digitalization of the healthcare sector, increased use of electronic health records, and growing need for telehealth services. The increasing emphasis on better patient outcomes, operational efficiency, and evidence-based decision-making will contribute to increased adoption. Increasing usage of artificial intelligence, cloud computing, and big data analytics in the sector will further enhance the infrastructure of the healthcare industry. The government initiatives towards digital health coupled with increased investment in healthcare modernization will drive the market globally.

The U.S. Office of the National Coordinator for Health IT (ONC) reports that approximately 96% of non-federal acute care hospitals use certified electronic health record (EHR) systems, reflecting near-universal adoption of digital patient record infrastructure in hospital settings. Among office-based physicians, around 78% utilize certified EHR systems, indicating strong but still evolving penetration in outpatient care environments.

The U.S. Food and Drug Administration (FDA) further confirms that hundreds of AI/ML-based medical devices are now authorized, with many applications supporting diagnostics and clinical decision-making, underscoring the growing integration of artificial intelligence into regulated healthcare technologies.

Market Size and Forecast

-

Market Size in 2025: USD 209.30 Billion

-

Market Size by 2035: USD 748.47 Billion

-

CAGR: 13.59% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Healthcare IT Services Market - Request Free Sample Report

Healthcare IT Services Market Trends

-

Rising demand for digital transformation in healthcare delivery is driving the healthcare IT services market.

-

Growing adoption of electronic health records (EHR), telehealth, and hospital information systems is boosting market growth.

-

Expansion of connected healthcare infrastructure and interoperability initiatives is fueling service deployment.

-

Increasing focus on improving patient outcomes, operational efficiency, and data-driven decision-making is shaping adoption trends.

-

Advancements in cloud computing, AI-powered diagnostics, cybersecurity, and health analytics are enhancing service capabilities.

-

Rising healthcare costs and the need for efficient resource management are supporting market expansion.

-

Collaborations between healthcare providers, IT service vendors, and technology firms are accelerating innovation and global adoption.

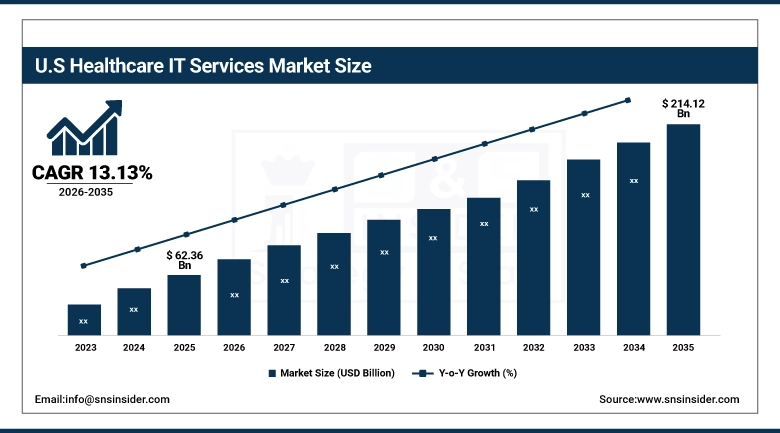

The U.S. Healthcare IT Services Market was valued at USD 62.36 billion in 2025 and is expected to reach USD 214.12 billion by 2035, growing at a CAGR of 13.13% from 2026-2035.

U.S. Healthcare IT Services Market growth is propelled by fast adoption of electronic health records, high demand for telemedicine services, and robust use of AI and cloud-based healthcare solutions. Increased emphasis on enhancing quality of patient care, efficiency, and data interoperability is also aiding market growth.

Healthcare IT Services Market Segment Highlights

-

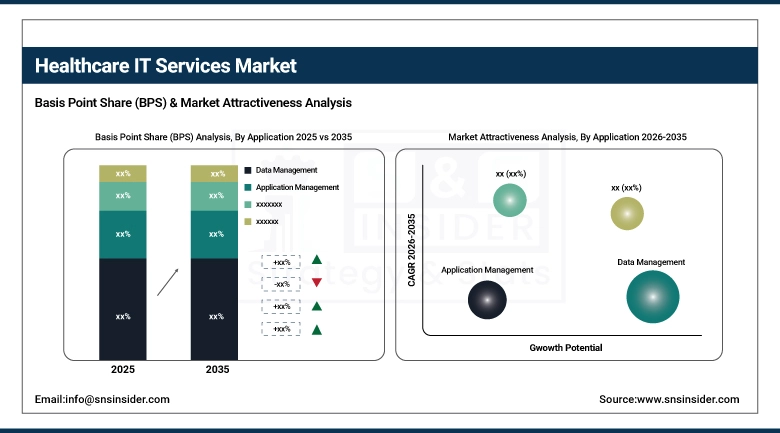

By Application, Data Management segment dominated the Healthcare IT Services Market in 2025 with approximately 32% share; Security & Compliance Management segment fastest growing (CAGR).

-

By Technology, Big Data Analytics segment dominated the Healthcare IT Services Market in 2025 with approximately 38% share; AI & Machine Learning segment fastest growing (CAGR).

-

By Deployment Mode, On-premises segment dominated the Healthcare IT Services Market in 2025 with approximately 56% share; Cloud segment fastest growing (CAGR).

-

By Service, HCIT Integration Systems segment dominated the Healthcare IT Services Market in 2025 with approximately 28% share; Telehealth Solutions segment fastest growing (CAGR).

Healthcare IT Services Market Segment Analysis

By Application, Data Management segment dominates the Healthcare IT Services Market, Security & Compliance Management segment expected to grow fastest

Data Management segment dominated the Healthcare IT Services Market in 2025 due to the growing need for centralized storage, organization, and retrieval of vast volumes of patient and clinical data across healthcare systems. Hospitals and providers rely on data management solutions to improve care coordination, reduce errors, and enhance operational efficiency. Increasing digitization of health records and interoperability requirements further strengthen adoption, making data management the backbone of healthcare IT infrastructure.

The Security & Compliance Management segment is the fastest-growing (CAGR). There are many reasons why healthcare providers are focused on increasing their investments in a security framework. In particular, there is an ever-growing number of cyber-attacks and ransomware attacks in healthcare. Also, there are stricter regulations concerning data protection in healthcare, which forces healthcare providers to invest in compliance monitoring, encryption, and identity management systems.

By Technology, Big Data Analytics segment dominates the Healthcare IT Services Market, AI & Machine Learning segment expected to grow fastest

The Big Data Analytics segment dominated the Healthcare IT Services Market in 2025 owing to its capability to analyze huge amounts of both structured and unstructured healthcare data to provide clinical and operational insights. The use of analytics in healthcare enables organizations to deliver improved patient outcomes, better resource utilization, and make evidence-based decisions. The adoption of predictive analytics in disease management and operations makes the segment dominant in the healthcare IT market.

The AI & Machine Learning segment is expected to grow at the highest CAGR during the forecast period because of the increasing usage of intelligent algorithms in the field of diagnostics, treatment planning, and operational optimization. The use of artificial intelligence in healthcare helps in enhancing the accuracy of medical imaging, predictive diagnostics, and personalized treatments. Growing investments in digital health innovations and adoption of smart healthcare applications are driving the segment's growth.

By Deployment Mode, On-premises segment dominates the Healthcare IT Services Market, Cloud segment expected to grow fastest

The on-premises segment will dominate the Healthcare IT Services Market in 2025 owing to high levels of data security requirements, regulatory compliances, and control over patients' sensitive information. Most healthcare organizations rely on on-premises infrastructure to avoid any cybersecurity threats and maintain data sovereignty. Existing IT infrastructure in hospitals and vulnerability concerns regarding cloud will further drive the adoption of on-premises solutions in large hospitals and governmental healthcare organizations.

The cloud segment is projected to be the fastest-growing segment in terms of CAGR owing to rising demands for scalable and cost-effective IT solutions in healthcare. The cloud-based infrastructure will facilitate real-time data availability, remote collaboration, and integration of electronic health records among different hospitals. Growing adoption of telemedicine applications, digital health platforms, and AI in healthcare will further drive the growth of the cloud segment in healthcare IT services market.

By Service, HCIT Integration Systems segment dominates the Healthcare IT Services Market, Telehealth Solutions segment expected to grow fastest

HCIT Integration Systems segment accounted for the largest share in the Healthcare IT Services Market in 2025 owing to the necessity for seamless integration between different healthcare software and systems. Hospitals need integration platforms that can facilitate connections between various electronic health records, laboratory management system, and imaging software. Increased focus on integration of patient data and better clinical decisions is another factor that is expected to fuel its adoption.

Telehealth Solutions segment is expected to register the fastest growth in CAGR due to rising need for remote patient consultation, virtual visits, and increased accessibility through digital health services. Increasing usage of smartphones, internet, and wearable technology devices is another reason for the rise in popularity of telehealth services. With the onset of post-pandemic behavioral changes and favorable government policies, there has been an increased adoption of telehealth services across the globe.

Healthcare IT Services Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

94.1% |

|

Europe |

United Kingdom |

28.6% |

|

Asia Pacific |

Australia |

10.4% |

|

Middle East & Africa |

UAE |

16.2% |

|

Latin America |

Brazil |

53.9% |

North America Healthcare IT Services Market Insights

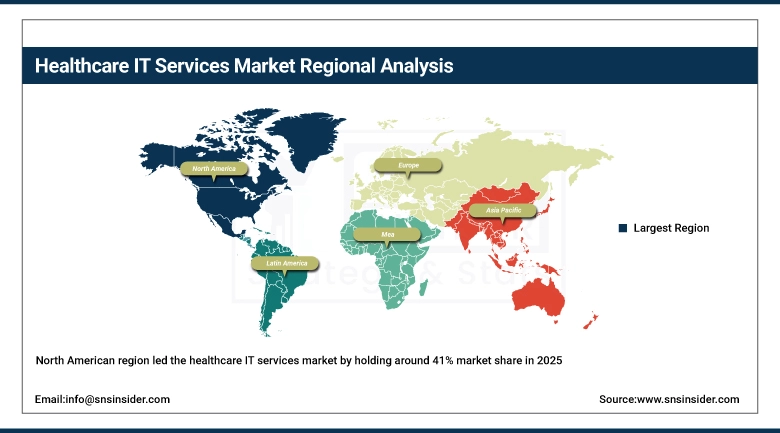

The North American region led the healthcare IT services market by holding around 41% market share in 2025. The prominent availability of advanced healthcare infrastructure, high rate of electronic health record adoption, and the integration of digital healthcare solutions were among the key factors driving regional growth. Moreover, the rising investments in healthcare analytics powered by artificial intelligence, cloud-based services, and interoperable systems contributed positively to the market growth. In addition, the presence of leading healthcare IT service providers and increased efforts toward improving patient outcomes and operational efficiency were driving the market dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Healthcare IT Services Market Insights

The Asia Pacific region is the fastest-growing region in terms of CAGR in the healthcare IT services market owing to the fast-paced digital transformation in the healthcare sector and the growing use of advanced healthcare IT technology. Growth in investment in hospital infrastructure, the increasing need for telehealth services, and rising adoption of electronic health records are contributing to the growth in the market. Increased awareness about healthcare, government involvement in digital health, and increased adoption of cloud-based healthcare solutions are also adding to market growth.

Europe Healthcare IT Services Market Insights

Europe possesses a considerable share in the market for healthcare IT services owing to robust healthcare infrastructures, advanced digitalization, and stringent regulations that enable evidence-based care. The adoption of electronic health records, telehealth solutions, and hospital information systems is contributing to the growth of the market. The emphasis on interoperability, privacy of patient data, and clinical efficiencies is helping fuel adoption rates. Investments made in AI-enabled healthcare analytics, cloud computing technologies, and digital health transformation programs are bolstering the healthcare IT landscape in Europe.

Middle East & Africa and Latin America Healthcare IT Services Market Insights

The Middle East & Africa and Latin America represent the developing market for healthcare IT services, due to the growing trend towards the healthcare digitization process and increasing investment in the development of medical infrastructure. Telemedicine systems, electronic health records, and hospital management systems become more widely used, which enhances the efficiency of healthcare services delivery. The governmental programs aimed at modernizing healthcare systems and providing citizens with digital care contribute to market growth. At the same time, the shortage of IT infrastructure and budgets remain the existing limitations.

Market Growth Drivers: Rising digital transformation across healthcare systems and increasing adoption of electronic health records and interoperable platforms globally

Healthcare organizations are increasingly utilizing digital technology to enhance their operations and delivery of patient care. The increasing adoption of electronic health records, health information exchange, and hospital management systems is creating robust demand for healthcare IT services. The growing requirement for real-time patient information exchange among healthcare providers is promoting the use of interoperability solutions. Automation of tasks and processes to reduce administrative workload is currently gaining momentum at hospitals and clinics. Cloud infrastructure and analysis services for the healthcare industry are receiving investments, thus adding to growth. Modernization of healthcare IT systems is fueling market growth around the world.

Market Restraints: Data security concerns and strict regulatory compliance requirements restricting seamless adoption of digital healthcare solutions

The information technology systems for healthcare deal with extremely sensitive health data, which is why cybersecurity and privacy protection are crucial aspects that need to be taken into account by the healthcare organizations. The rise in the number of data breaches and cyber attacks on the healthcare institutions results in growing security threats. Compliance with certain requirements related to data protection laws and healthcare regulations makes the process of implementing healthcare information technology systems even more difficult. The proper data storage, transmission, and access control necessitate advanced security measures. Different legal requirements in different regions pose an additional challenge.

Market Opportunities: Expanding adoption of artificial intelligence and machine learning in healthcare systems creating new opportunities for predictive and personalized care solutions

Integration of artificial intelligence and machine learning within healthcare IT services is presenting numerous opportunities for innovations in diagnosis, treatment planning, and patient monitoring. AI technology allows for predictive analytics, early detection of diseases, and customized treatment options. The increasing demand for healthcare solutions based on data is prompting more rapid development of intelligent clinical decision support systems. Hospitals and research organizations are increasingly adopting AI-based healthcare systems. Constant progress in big data analytics and automation technologies is improving the efficiency and accuracy of healthcare services. It is expected that such developments will generate considerable growth opportunities for healthcare IT services.

Recent Developments:

-

2026: Optum expanded AI-powered payer-provider integration, improving claims automation, fraud detection, and real-time healthcare data exchange across large-scale insurance and provider networks.

-

2026: Oracle Health expanded autonomous EHR capabilities using generative AI to automate clinical documentation, coding, and patient record summarization, enabling reduced administrative burden for healthcare providers.

-

2025: IBM expanded hybrid cloud and AI healthcare services following Watson Health restructuring, focusing on data interoperability, clinical analytics, and population health management solutions.

-

2025: Cognizant expanded its TriZetto healthcare platform, improving payer-provider interoperability, claims processing automation, and cloud-based healthcare administration solutions.

Healthcare IT Services Market Key Players

-

Epic Systems

-

Oracle Health

-

McKesson Corporation

-

Optum

-

Cognizant

-

Accenture

-

IBM

-

Philips Healthcare

-

Siemens Healthineers

-

GE HealthCare

-

Tata Consultancy Services

-

Wipro

-

Infosys

-

HCLTech

-

Cerner Corporation

-

athenahealth

-

Teladoc Health

-

Amwell

-

Change Healthcare

-

InterSystems

Healthcare IT Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 209.30 Billion |

| Market Size by 2035 | USD 748.47 Billion |

| CAGR | CAGR of 13.59% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Systems & Network Management, Data Management, Application Management, Security & Compliance Management, Others) • By Technology (AI & Machine Learning, Big Data Analytics, Threat Intelligence, Others) • By Deployment (On-premises, Cloud) • By Service (Population Health Management Services, HCIT Integration Systems, Telehealth Solutions, Laboratory Information Systems, Clinical Decision Support Systems, Infection Surveillance Solutions, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Epic Systems, Oracle Health, McKesson Corporation, Optum, Cognizant, Accenture, IBM, Philips Healthcare, Siemens Healthineers, GE HealthCare, Tata Consultancy Services, Wipro, Infosys, HCLTech, Cerner Corporation, athenahealth, Teladoc Health, Amwell, Change Healthcare, InterSystems |

Frequently Asked Questions

Ans: The Healthcare IT Services Market is expected to grow at a CAGR of 13.59% from 2026 to 2035.

Ans: The Healthcare IT Services Market was valued at USD 209.30 billion in 2025.

Ans: Rising digital transformation across healthcare systems and increasing adoption of electronic health records and interoperable platforms globally.

Ans: The Big Data Analytics segment dominated the Healthcare IT Services Market in 2025.

Ans: North America dominated the Healthcare IT Services Market in 2025.

Get in Touch