Biopharmaceutical Manufacturing Consumables Testing Market Report Scope & Overview:

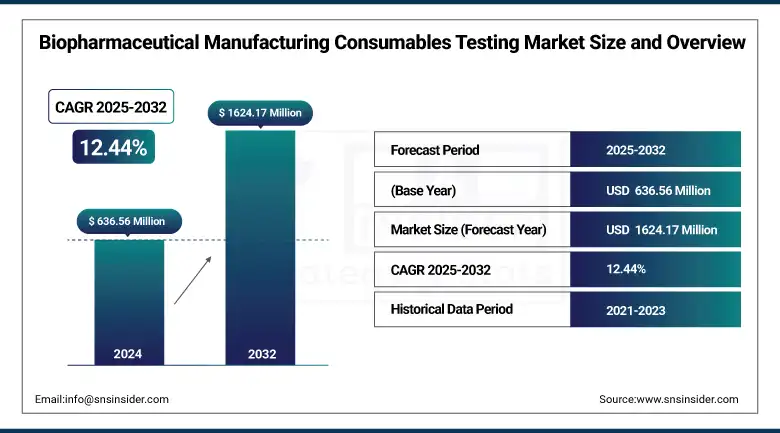

The biopharmaceutical manufacturing consumables testing market size was valued at USD 636.56 million in 2024 and is expected to reach USD 1624.17 million by 2032, growing at a CAGR of 12.44% over 2025-2032.

The biopharmaceutical manufacturing consumables testing market is receiving substantial momentum from the growing complexity of biologics, increasing concern for regulatory-compliant consumables in manufacturing settings.

As the industry continues to move toward more sophisticated therapies such as monoclonal antibodies, cell and gene therapies, and biosimilars, manufacturers are also depending more heavily on more robust compendial and microbial testing of inputs, including filters and tubing, excipients, chromatography resins, and APIs. Such demand is also supported by increasingly strict FDA and EMA regulations requiring validated testing procedures of single-use systems and cleanroom consumables to ensure product safety and purity.

Charles River Laboratories added rapid compendial methods for single-use bioprocessing systems to its endotoxin and microbial testing services in February 2024 to meet increasing demand in the Biopharmaceutical manufacturing consumables testing market.

To Get more information On Biopharmaceutical Manufacturing Consumables Testing Market - Request Free Sample Report

With the increasing biopharmaceutical manufacturing consumables testing market trends, with outsourcing, CDMOs and biopharma companies are collaborating with companies that conduct testing of biopharmaceutical manufacturing consumables for GMP standards, thereby fueling the global biopharmaceutical manufacturing consumables testing market. The steady increase in R&D investment over USD 240 billion globally in 2023 has fuelled growth in new biologics pipelines and demand for testing within the industry. Furthermore, increasing drug approvals and quality standards support, such as USP / have also influenced the growth of the biopharmaceutical manufacturing consumables testing market, especially in the U.S. biopharmaceutical manufacturing consumables testing market.

In May 2024, Eurofins Scientific introduced a cloud-enabled data analytics platform for real-time tracking of consumables testing, marking shifts toward digital transformation in the biopharmaceutical manufacturing consumables testing market analysis.

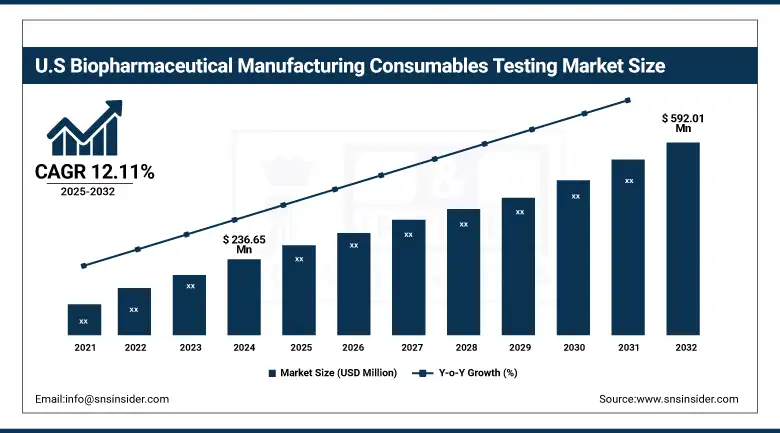

The U.S. biopharmaceutical manufacturing consumables testing market size was valued at USD 236.65 million in 2024 and is expected to reach USD 592.01 million by 2032, growing at a CAGR of 12.11% over 2025-2032. The U.S. dominates in this domain due to the presence of leading market participants such as Charles River Laboratories, Thermo Fisher Scientific, Catalent, and others. The US biopharmaceutical manufacturing consumables testing market is further influenced by the implementation of the USP / procedure and the emergence of the enhanced single-use system validation strategy. Canada is becoming a supportive environment due to government grants in the biotech space and partnerships with global CDMOs.

Market Dynamics:

Drivers:

-

Rising Biologics Pipeline and Regulatory Scrutiny Fuel Testing Demand, Also Propels Market Growth

The biopharmaceutical manufacturing consumables testing market growth is fueled by the development of biologics, such as monoclonal antibodies, cell therapies, and mRNA-based products, that require rigorous raw material and consumables testing. With more than 22,000 biologics currently in the development pipeline worldwide (as of 2024, according to PhRMA), demand for testing has skyrocketed to meet compliance with USP and requirements. Anything that touches a product in ultrapurification, like excipients, filters, tubing, and resins, is all validated for extractables/leachables, endotoxins, and microbiological contamination.

Moreover, supply chain complexity is driving manufacturers towards vendor qualification programs with the help of third-party labs. The investment by the top pharma companies in R&D was more than USD 260 billion in 2023, leading to an increase in product pipelines and an increased reliance on validated and traceable inputs. Rising regulatory pressure from the FDA, EMA, and PMDA is also encouraging the use of validated testing procedures, thus further driving the biopharmaceutical manufacturing consumables testing market growth in all therapeutic modalities.

Restraints:

-

High Testing Costs and Infrastructure Gaps Limit Wider Adoption of Market

Although the market is growing, the biopharmaceutical manufacturing consumables testing market is limited by the expensive nature of advanced analytical testing, as well as the scarcity of specialized infrastructure in developing countries. Repeated tests for a variety of impurities, such as extractables/leachables and particulate matter, are costly and could involve significant capital equipment, such as mass spectrometry and high-performance chromatography systems, which many smaller manufacturers or startups don’t have or cannot afford. Moreover, the need to adhere to new pharmacopeial standards (e.g., USP for plastics packaging) has added further complexity and time to operations, placing pressure on batch release times.

A shortage of harmonized global regulatory standards also creates a bottleneck for international suppliers, adding weight to global validation programs. In addition, despite increasing R&D investments, many firms still are underfunding quality testing programs, which can lead to audit delays or failures. These impediments restrict the universal adoption of testing services, which in turn affects the scalability and responsiveness of companies operating in the biopharmaceutical manufacturing consumables testing market in cost-sensitive scenarios.

Segmentation Analysis:

By Service Type

Laboratory testing dominated the market in 2024, with a share of 34.2%, owing to its widespread usage in GMP compliance, raw material quality assurance, and batch release testing. Its need is driven by the application as a quality control in the regular verification of APIs, excipients, and packaging as they are critical for product safety and regulatory compliance.

Compendial & multi-compendial grows the fastest, as they also align with enhanced pharmacopeial test requirements (USP, EP, JP) and the demand for standardized methods in the world markets are increasing. It is also boosted by increased control by the FDA over USP and for packaging and plastic systems.

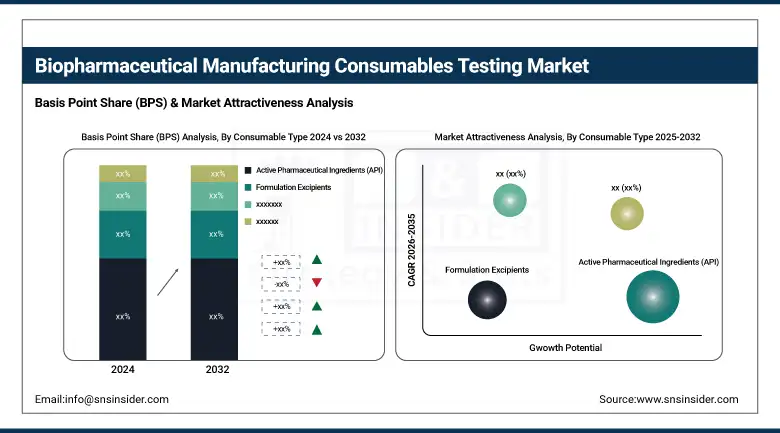

By Consumable Type

APIs generated the highest revenue of 31.7% in 2024, as they are exceedingly important for determining product efficacy and safety. APIs need to have a thorough impurity profile, microbe, and endotoxin profile; they represent the center of action in terms of consumable testing.

Single-use bioprocessing consumables are experiencing the highest demand growth as biopharma increasingly adopts disposable and modular manufacturing systems. This end-market is being supported by growing requests for extractables/leachables testing and filter integrity validation, notably in cell and gene therapy manufacturing.

By Testing Technology

Physicochemical testing was the leading test with 29.4% biopharmaceutical manufacturing consumables testing market share in 2024 due to its essential requirement to determine the identification, purity, and concentration of the inputs, such as excipients, buffers, and chromatography media, specifically through HPLC and FTIR.

Biological and microbiological testing segment is expected to witness fastest growth as microbial limit, endotoxin, and sterility testing are critical for biopharmaceutical safety. The development of injectable biologics and personalised medicines has also increased the testing requirements in this area.

By End-user

Biopharmaceutical & biotechnology companies dominated the highest biopharmaceutical manufacturing consumables testing market share of 43.6% in 2024 on account of internal quality assurance policies and rising product pipelines for strong input validation.

CDMOs are experiencing the most rapid growth as pharma companies are outsourcing more consumables testing as part of their efforts to optimize operations. Growing international collaborations and demand for fast scale-up have increased the number of testing volumes coming into CDMOs.

Regional Analysis:

The biopharmaceutical manufacturing consumables testing market in North America held the largest share based on region in 2024, which was attributed to the large number of biopharmaceutical companies, the stringent regulatory scenario of the FDA, and high investment in biologics R&D.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe was the second major market for the global biopharmaceutical manufacturing consumables testing market in 2024, and its biologics manufacturing infrastructure leaders include Germany and the UK. Germany continues to lead with a well-developed pharma R&D centre and compliance with EU GMP. There is also an increasing number of outsourcing to testing-led contract establishments from France and Italy. The star performer among the country group is Poland, supported by the growth of in-country CDMOs and EU-based pharma investments.

The biopharmaceutical manufacturing consumables testing market in Asia Pacific is projected to register the highest CAGR during the forecast period, driven by the growing number of biologics manufacturing facilities, rising clinical research, and increasing regulatory harmonization. China holds the largest share in the region, supported by government initiatives such as “Made in China 2025” and the surge in local testing labs. India appeared as the second most dynamic country, given the increasing harmonisation with USP/EP standards and significant CDMO investments by international biopharma companies. Japan and South Korea are also witnessing resilient growth, driven by strong innovation pipelines and a focus on high-quality manufacturing.

Key Players:

Leading biopharmaceutical manufacturing consumables testing companies driving the market include Charles River Laboratories, Eurofins Scientific, Merck KGaA (MilliporeSigma), Agilent Technologies, Inc., Catalent, Inc., Alcami Corporation, Pace Analytical Services, LLC, Nelson Laboratories, LLC (Gibraltar Laboratories), Element Materials Technology (Avomeen Analytical Services), BioSpectra Inc., Thermo Fisher Scientific Inc., SGS SA, Intertek Group plc, Lonza Group AG, WuXi AppTec, Boston Analytical, Microbac Laboratories, Inc., PPD Inc. (Part of Thermo Fisher Scientific), West Pharmaceutical Services, Inc., Pharmalex GmbH, Envigo (now part of Inotiv, Inc.), Labcorp Drug Development (formerly Covance), Ajinomoto Bio-Pharma Services, Toxikon Corporation, and Biologics Consulting Group Inc.

Recent Developments:

In June 2025, Charles River initiated the Endosafe Cartridge Recycling Program in partnership with TerraCycle. This initiative enables the recycling of used endotoxin testing cartridges, particularly those used in routine water testing, helping labs reduce plastic waste and meet sustainability goals in consumables testing operations.

In June 2024, MilliporeSigma opened a state-of-the-art quality control building at its Darmstadt site, boosting analytical and microbial testing capacity supported by GMP-compliant labs and sustainable infrastructure to support global demand.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 636.56 million |

| Market Size by 2032 | USD 1624.17 million |

| CAGR | CAGR of 12.44% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Laboratory Testing, Custom / Proprietary Testing Services, Compendial & Multi-Compendial Testing (USP, EP, JP, etc.), Method Development & Validation, Stability & Compatibility Testing, Microbial Limit & Endotoxin Testing) • By Consumable Type (Formulation Excipients, Active Pharmaceutical Ingredients (API), Single-use Bioprocessing Consumables (tubing, bags, filters), Chromatography Resins & Filters, Buffer Solutions & Culture Media, Packaging Components (vials, stoppers, containers)) • By Testing Technology (Compendial Testing (USP/EP/JP Standards), Non-compendial Testing (Client-Specific Protocols), Physicochemical Testing, Biological and Microbiological Testing, Spectroscopy and Chromatography Techniques) • By End-user (Biopharmaceutical and Biotech Companies, Contract Development and Manufacturing Organizations (CDMOs), Raw Material and Excipient Suppliers, Academic and Research Institutions, Regulatory & Quality Assurance Agencies) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Charles River Laboratories, Eurofins Scientific, Merck KGaA (MilliporeSigma), Agilent Technologies, Inc., Catalent, Inc., Alcami Corporation, Pace Analytical Services, LLC, Nelson Laboratories, LLC (Gibraltar Laboratories), Element Materials Technology (Avomeen Analytical Services), BioSpectra Inc., Thermo Fisher Scientific Inc., SGS SA, Intertek Group plc, Lonza Group AG, WuXi AppTec, Boston Analytical, Microbac Laboratories, Inc., PPD Inc. (Part of Thermo Fisher Scientific), West Pharmaceutical Services, Inc., Pharmalex GmbH, Envigo (now part of Inotiv, Inc.), Labcorp Drug Development (formerly Covance), Ajinomoto Bio-Pharma Services, Toxikon Corporation, and Biologics Consulting Group Inc. |

Frequently Asked Questions

Ans: Trends include automation in microbial and particulate testing, AI-based data analytics, and increased adoption of compendial and rapid testing methods.

Ans: Major players include Charles River Laboratories, Eurofins Scientific, Merck KGaA, Agilent Technologies, Catalent, Pace Analytical, and SGS SA.

Ans: Fastest-growing segments include endotoxin testing, filter integrity testing, and cleanroom consumables validation, particularly within biologics and cell therapy manufacturing workflows.

Ans: Key drivers include growing regulatory scrutiny (FDA/EMA), rising use of single-use technologies, and increased outsourcing of endotoxin and validation testing by CDMOs and pharma firms.

Ans: It refers to analytical and quality assurance services used to test materials like excipients, APIs, filters, and single-use systems used in biopharma manufacturing. These tests ensure regulatory compliance, product safety, and manufacturing consistency.

Get in Touch