Neonatal Critical Care Equipment Market Report Scope & Overview:

To Get More Information on Neonatal Critical Care Equipment Market - Request Sample Report

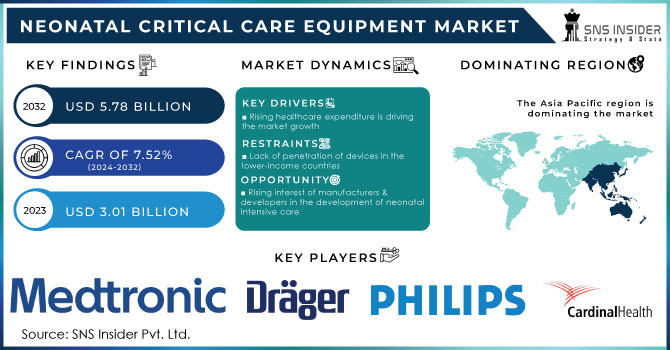

The Neonatal Critical Care Equipment Market size was estimated at USD 3.01 billion in 2023 and is expected to reach USD 5.78 billion by 2032 with a growing CAGR of 7.52% during the forecast period of 2024-2032.

Neonates are cared for using specialized equipment due to prenatal abnormalities or premature births, neonates are cared for using specialized equipment. For the neonates born prematurely, incubators are in high demand in the NICU facilities. The WHO estimates that 15 million babies are born prematurely each year around the world. Neonatal admissions to the NICU have increased as a result of this larger number. Additionally, if neonatal diseases become more prevalent, end users may need more care equipment. Additionally, it is projected that increased R&D by medical device businesses and the introduction of cutting-edge products will raise market potential throughout the forecast period.

MARKET DYNAMICS

DRIVERS

- Rising healthcare expenditure is driving the market growth

Because of the rising expense of healthcare, the market for neonatal intensive care is expanding significantly. Due to increased funding for healthcare, particularly in developing countries, new care facilities can now be expanded and improved. As a result, there is a greater need for goods and services connected to neonatal intensive care. A rise in healthcare funding has made it possible to build neonatal intensive care units (NICUs) with modern amenities and additional beds. These facilities require large infrastructure, medical equipment, and staffing investments. When there are more NICU beds available, a greater number of neonates in need of intensive care can be admitted and treated. This growth is a response to the growing need for neonatal intensive care services, particularly in regions with a higher incidence of preterm births and neonatal diseases.

RESTRAIN

- Lack of penetration of devices in the lower-income countries

OPPORTUNITY

- Rising interest of manufacturers & developers in the development of neonatal intensive care

The Neonatal Intensive Care Industry is expanding as a result of manufacturers and developers increased interest in the development of neonatal intensive care equipment and the newest product launches. For instance, following the U.S. Food and Drug Administration's (FDA) marketing permission, Medtronic plc, a multinational medical technology company, announced the U.S. commercial launch of the Carpediem Cardio-Renal Pediatric Dialysis Emergency Machine in November 2021. The joint efforts of manufacturers to establish a presence in new markets also help to the expansion of the Neonatal Intensive Care Market.

CHALLENGES

- Lack of regulatory approval and critical care equipment

The rise of neonatal intensive care is likely to be constrained by factors such as a lack of awareness, economic restraints, and declining birth rates in industrialized countries. The biggest and most important challenge to market expansion will be the absence of regulatory approval for critical care equipment.

IMPACT OF RUSSIA-UKRAINE WAR

According to the United Nations Population Fund (UNPFA), an estimated 265,000 pregnant women who were unable to get maternal care when the violence started. This is corroborated by the fact that several hospitals have been hastily moved into bomb shelters and underground metro stations as they become inoperable or inaccessible. Numerous infants are delivered in bomb shelters without a stable power source. The risk of difficulties, illness, and death for mothers and newborns will rise due to filthy circumstances during deliveries underground caused by attacks on hospitals and healthcare institutions, according to the WHO external status report. According to UNICEF, the medical staff at the subpar underground medical center is working under extreme strain and filling various responsibilities because to a labor shortage. The likelihood of premature deliveries has been observed in recent reports. Preterm infants need specialized care, which is probably not available at such crucial times.

IMPACT OF ONGOING RECESSION

As a result of COVID-19, economic recession has happened in practically all nations. Previous studies have shown that these financial crises have a disproportionately negative impact on children's health and mortality in low- and middle-income countries (but not in high-income ones), and that these impacts are probably independent of whether or not children have COVID-19 disease. The cumulative impacts of environmental contamination, nutrient inadequacy, maternal factors, injury, and personal sickness control are thought to be the mechanisms linking social health variables like GDP per capita to child mortality in low- and middle-income nations. For instance, as households attempt to overcome poverty by moving to less-than-ideal housing with poorer sanitation and greater crowding, as well as by changing their diets away from expensive sources of protein and micronutrients, reductions in household income can unleash dual effects of environmental contamination and nutrient deficiency.

KEY MARKET SEGMENTATION

By Type

-

Thermoregulation Equipment

-

Infant Warmers

-

Incubators

-

-

Phototherapy Equipment

-

Neonatal Monitoring Devices

-

Cardiac Monitors

-

Capnographs

-

Integrated Monitoring Devices

-

-

Respiratory Devices

-

Neonatal Ventilators

-

Continuous Positive Airway Pressure (CPAP) Devices

-

Oxygen Analyzers and Monitors

-

Resuscitators

-

Others

-

-

Others

In 2022, thermoregulation equipment segment is accounted the largest market share of 33.2% during the forecast period. The demand for thermoregulation equipment is anticipated to rise throughout the projected period due to the rising prevalence of newborn hypothermia and greater awareness of the high mortality and morbidity associated with it. The prevalence of hypothermia is higher in developing nations, where it affects between 34% and 87% of neonates born in hospitals and between 13% and 94% of those born at home, according to a research article published in the National Library of Medicine in September 2021.

By End User

-

Hospitals

-

Clinics

-

Others

In 2022, the hospitals segment is expected to held the highest market share of 58.1% during the forecast period, the segment is anticipated to develop the fastest by opening new centers and collaborating with other groups, hospitals that offer newborn critical care are increasing their treatment options. For instance, the Motherhood Hospitals network opened five virtual Neonatal Intensive Care Units (NICUs) in India in April 2023. The addition of cutting-edge treatments to a hospital's service portfolio helps it to gain market share.

REGIONAL ANALYSIS:

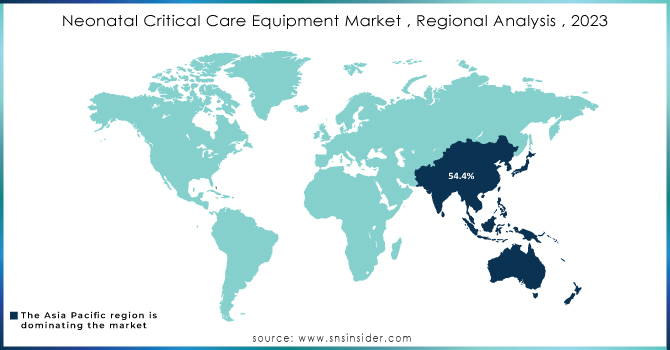

Asia Pacific held a significant market share of 54.4% in 2022 owing to the technological developments in neonatal critical care equipment and an increase in preterm deliveries. A UNICEF database shows that in South Asia, the newborn mortality rate was 22.993 per 1,002 live births in 2021, which resulted in 801,695 neonatal fatalities in this region. Therefore, growth throughout the forecast period is likely to be driven by the availability of a sizable patient pool, rising awareness regarding neonatal care, and the expanding presence of global players.

Middle East & Africa is witness to expand fastest market share during the forecast due to preterm births are becoming more common in Africa. Infections and illnesses are known to be more contagious in preterm babies. According to a JAMA Network article, the majority of preterm births (approximately 60%) take place in Africa and South Asia. Therefore, fetal incubators and fetal monitors must be used to keep an eye on these neonates. The demand for monitoring tools and equipment is predicted to rise as a result of these causes, accelerating technical development.

Do You Need any Customization Research on Neonatal Critical Care Equipment Market - Enquire Now

REGIONAL COVERAGE

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

Key Players

The major players are Drägerwerk AG & Co. KGaA, Cardinal Health, Koninklijke Philips N.V., Medtronic, GE Healthcare, Fisher & Paykel Healthcare Limited, Masimo, Phoenix Medical Systems (P) Ltd., Natus Medical Incorporated, Utah Medical Products, Inc., Inspiration Healthcare Group plc, Atom Medical Corp, and Others.

RECENT DEVELOPMENTS

-

In July 2023, Evita V800, V600, and Babylog VN800 ventilators made by Drägerwerk AG & Co. KGaA have been given FDA 510(k) approval for use on both adults and newborns.

-

In May 2023, Sibel Health's Anne One platform for newborn and baby monitoring has gained U.S. FDA 510(k) clearance. It is an adult, infant, and neonate-specific wireless, clinical-grade, continuous monitoring solution

| Report Attributes | Details |

| Market Size in 2023 | US$ 3.01 billion |

| Market Size by 2032 | US$ 5.78 billion |

| CAGR | CAGR of 7.52% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Thermoregulation Equipment, Phototherapy Equipment, Neonatal Monitoring Devices, Respiratory Devices, Others) • By End User (Hospitals, Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Texas Instruments (US), Skyworks Solutions, Inc. (US), Analog Devices (US), Broadcom Inc. (US), and Infineon Technologies (Germany), ON Semiconductor (U.S.), Murata Manufacturing Company Ltd (Japan), STMicroelectronics N.V. (Switzerland), NXP Semiconductors N.V. (the Netherlands), Vicor Corporation (U.S.) |

| Key Drivers | • Rising healthcare expenditure is driving the market growth |

| Market Challenges | • Lack of penetration of devices in the lower-income countries |

Frequently Asked Questions

Ans: Lack of penetration of devices in the lower-income countries.

Ans: Asia Pacific segment is expected to held the highest market share in 2023.

Ans: Neonatal critical care equipment market size was valued at USD 3.01 billion in 2023.

Ans: Neonatal critical care equipment market is anticipated to expand by 7.52% from 2024 to 2032.

Ans: The growth rate of the neonatal critical care equipment market is expected to grow USD 5.78 billion by 2032.

Get in Touch