Hyaluronidase Market Report Scope & Overview:

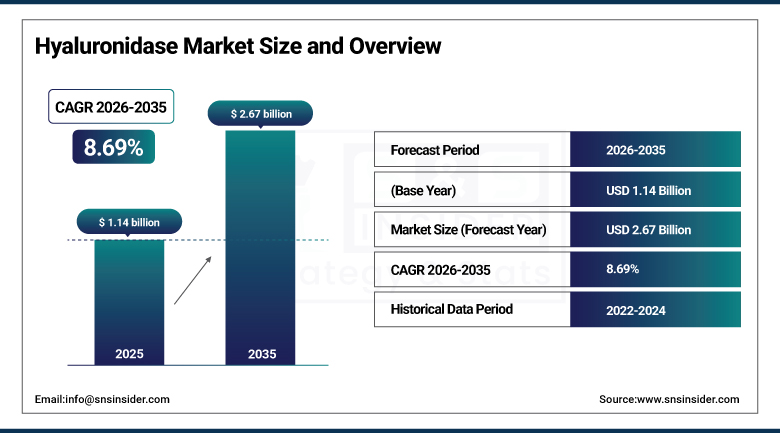

The Hyaluronidase Market was valued at USD 1.14 billion in 2025 and is expected to reach USD 2.67 billion by 2035, growing at a CAGR of 8.69% from 2026–2035.

Hyaluronidase is an enzyme that hydrolyzes hyaluronic acid, which occurs naturally in the body. The use of this enzyme in the healthcare industry is primarily for two purposes: facilitating the dispersion of drugs within tissues following injection, and also reversing the action of hyaluronic acid fillers in cosmetic surgeries. The increasing popularity of minimally invasive cosmetic treatments globally has been a primary market impetus.

Halozyme Therapeutics has commercialized hyaluronidase as a drug delivery platform through its ENHANZE technology. This platform is licensed to major pharmaceutical companies including Roche, Pfizer, and Janssen to convert intravenous biologics into subcutaneous formulations, dramatically reducing treatment time for patients.

Market Size and Forecast

-

Market Size in 2025: USD 1.14 Billion

-

Market Size by 2035: USD 2.67 Billion

-

CAGR: 8.69% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Hyaluronidase Market - Request Free Sample Report

Market Trends

-

Growing popularity of minimally invasive aesthetic procedures is driving parallel demand for hyaluronidase as a reversal and safety agent.

-

Pharmaceutical companies are increasingly converting IV biologic therapies to subcutaneous delivery using recombinant hyaluronidase.

-

FDA approvals for new combination biologic therapies using ENHANZE drug delivery technology are expanding clinical applications.

-

Rising aesthetic consciousness in Asia Pacific, particularly in South Korea, China, and Japan, is creating major new regional markets.

-

Recombinant human hyaluronidase products are gradually replacing animal-derived versions due to superior consistency and purity.

-

Telemedicine and virtual consultations are expanding access to aesthetic treatments, which in turn drives demand for correction products.

-

Post-filler vascular complications requiring emergency hyaluronidase treatment are driving education and product stocking in aesthetic clinics.

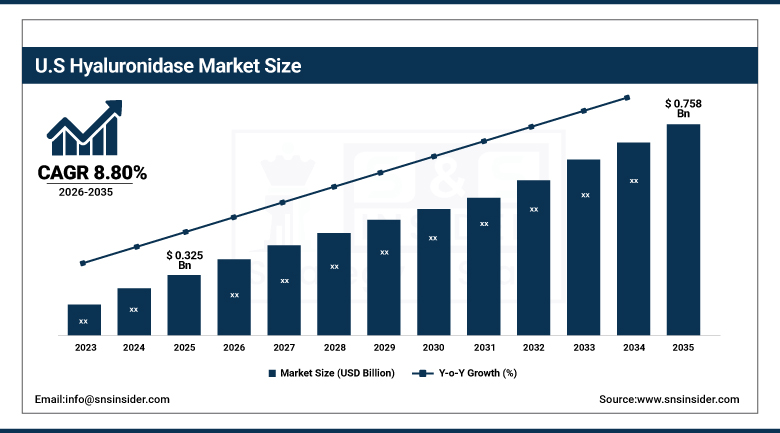

U.S. Hyaluronidase Market was valued at USD 0.325 billion in 2025 and is expected to reach USD 0.758 billion by 2035, growing at a CAGR of 8.80% from 2026 to 2035.

The US dominates the global hyaluronidase market because of its massive aesthetic industry, superior oncology programs, and solid research & development pipeline for drugs administered subcutaneously. The recent FDA approvals of SKINVIVE by JUVÉDERM in 2023 and Tecentriq Hybreza in 2024 have enhanced the clinical application of hyaluronic acid and reversal agents. Some of the most innovative applications of hyaluronidase are being developed by American pharma giants such as Halozyme Therapeutics.

The U.S. aesthetics market is the largest in the world, with millions of hyaluronic acid filler procedures performed each year by dermatologists and plastic surgeons. This creates a consistent baseline demand for hyaluronidase as both a safety precaution and a correction tool in aesthetic practices.

Market Segment Insights

-

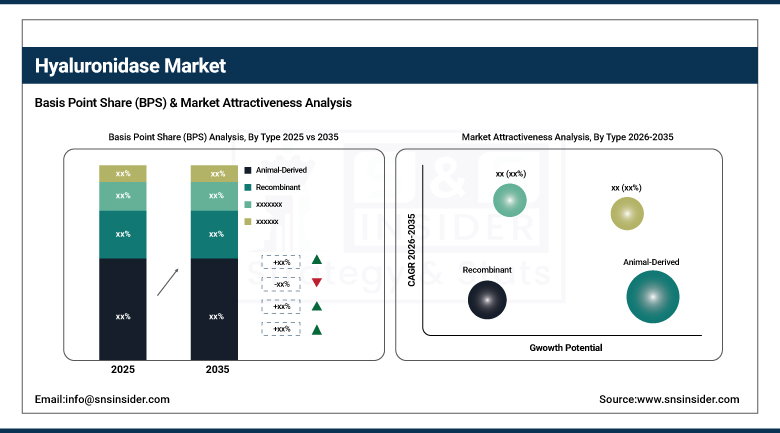

Based on Type, Animal-Derived Hyaluronidase dominated with 68.45% market share in 2025; Recombinant products are expected to grow at a faster CAGR.

-

Based on Application, Drug Delivery Enhancement and Dermal Filler Reversal are the two largest application segments.

-

Based on End-Use, Hospitals and Aesthetic Clinics are the two primary end-users; Ambulatory Surgical Centers are a growing segment.

-

Oncology applications are seeing increased use as new biologic cancer therapies are reformulated for subcutaneous delivery using hyaluronidase.

Market Segment Analysis

By Type: Animal-Derived Leads, Recombinant Growing Faster

Hydrolyzing enzymes that come from animal tissues, including the testes of cattle or sheep, have been utilized in the clinical setting for several decades now. These enzymes are quite easy to understand, easily available, and much less expensive compared to the recombinant alternatives. This accounts for why they occupy a major 68.45% of the market share until 2025. Clinical procedures, as well as training sessions for doctors, are mostly developed on the basis of animal products. The cost of changing an already established procedure is considerable.

Recombinant enzymes are humanized via genetic manipulation. The most important benefit associated with them is high uniformity and low chances of allergies compared to animal products. Halozyme is one of the manufacturers producing HYLENEX recombinant enzymes. Nowadays, pharmaceutical companies favor hyaluronidase for drug delivery, making recombinant enzymes the priority choice due to their advanced character. Recombinant products will be growing faster than animal-derived between 2015 and 2035.

By Application: Drug Delivery and Filler Reversal Both Strong

Enhancing drug delivery is the primary, most strategic use case for hyaluronidase. In combination with a drug, hyaluronidase creates temporary pores within the connective tissue through which the drug can diffuse quickly and achieve peak levels in the blood. As a consequence, subcutaneous infusion can be turned into subcutaneous injections, saving significant time for the patient. Subcutaneous injection of Herceptin and MabThera by Roche works on this principle, decreasing treatment time from 90 minutes via intravenous administration to only 5 minutes subcutaneously.

Dermal filler removal is the consumer healthcare application most commonly associated with hyaluronidase. The use of hyaluronidase allows the rapid degradation of a hyaluronic acid filler in cases of adverse events like vascular occlusions or poor patient satisfaction with the cosmetic result achieved. This application is developing along with the expansion of the global aesthetic market. Hyaluronidase must be available at clinics performing dermal fillers for the sake of safety regulations in multiple jurisdictions. Another medical area using hyaluronidase is ophthalmic surgery where it increases diffusion rates of the anesthetic administered locally into the eye. This is a solid but slowly growing niche application developing in correlation with cataract surgery volumes.

By End-Use: Hospitals Largest, Aesthetic Clinics Growing Fast

Hospitals remain the largest purchasers of hyaluronidase, mainly due to their use in drug delivery within the oncology infusions department and operating rooms. Patients who require subcutaneous biological treatment in the oncology department of hospitals provide a consistent revenue source.

The aesthetics sector remains the fastest-growing market. With the increasing popularity of non-invasive facial procedures, the number of clinics that offer fillers has increased significantly. Each clinic requires hyaluronidase both as a therapeutic agent and as an emergency kit. Hyaluronidase training remains a fundamental aspect of aesthetic medicine training globally.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

80% |

|

Europe |

United Kingdom |

29% |

|

Asia Pacific |

South Korea |

30% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

52% |

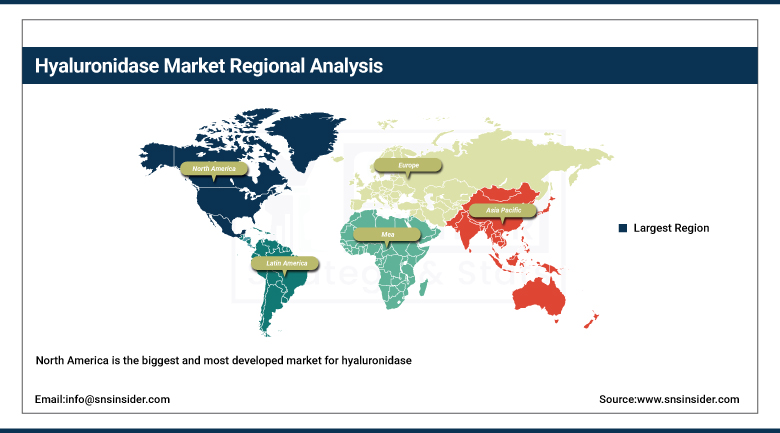

North America

North America is the biggest and most developed market for hyaluronidase. There is a significant growth in aesthetics business in the United States as well as in oncological treatments and the favorable regulatory policies of FDA for hyaluronidase-based drugs. In addition, there is an increasing aesthetic medicine market in Canada. American companies like Halozyme are driving worldwide marketing of hyaluronidase-based drugs.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe

Europe represents a key market due to the existing aesthetics industry in addition to the presence of its robust pharmaceutical industry. The UK, France, Germany, and Italy represent key markets for both the aesthetic filler products and the biologic anticancer medications. Several subcutaneous forms of biologics using hyaluronidase are already approved by the European Medicine Agency (EMA).

Asia Pacific

Asia-Pacific is the fastest-growing region for the development of hyaluronidase due to the rapid expansion of the aesthetic industry in South Korea, China, and Japan. South Korea is considered the leading country in aesthetic medicine globally, with highly per-capita usage of fillers. In China, the expanding middle class leads to quick adoption of minimally-invasive aesthetic treatments. Japan’s aging demographics fuel the need for subcutaneous biological medicines.

Middle East & Africa

The field of aesthetic medicine is flourishing in the Middle Eastern countries such as the UAE, Saudi Arabia, and Lebanon due to social acceptance and a big consumer base willing to afford expensive procedures. In parallel with the rise of the use of hyaluronic acid fillers, there is a gradual adoption of hyaluronidase in the region. The influx of patients traveling for medical purposes has contributed to the increase in the number of procedures.

Latin America

Brazil is the world's second-largest market for cosmetic procedures and a significant regional driver of hyaluronidase demand. The Brazilian aesthetics market is well-regulated and professionally organized, which supports quality product adoption. Mexico, Colombia, and Argentina also have growing aesthetics markets. The region's biopharmaceutical sector is developing, which will eventually drive demand for drug delivery applications of hyaluronidase in oncology and other therapeutic areas.

Market Growth Drivers

-

Growth of the global aesthetics market and subcutaneous drug delivery innovation

Two parallel trends are driving hyaluronidase market growth. First, the global aesthetics industry is growing at a high rate as non-surgical treatments become more socially accepted, affordable, and accessible. More filler procedures mean more demand for the reversal agent. Second, major pharmaceutical companies are using hyaluronidase as a platform to improve their drug delivery, turning slow IV infusions into quick subcutaneous injections. This second driver is particularly powerful because it links hyaluronidase to the blockbuster biologic drug market.

Halozyme's ENHANZE technology partnerships with Roche, Pfizer, Janssen, and others represent a franchise model that generates royalty revenue across multiple drug programs. Each new approval of a subcutaneous biologic using this technology expands the total addressable market for recombinant hyaluronidase without requiring Halozyme to develop or sell the drug itself.

Market Restraints

-

Limited regulatory approvals in developing markets and supply concentration risks

In many developing countries, hyaluronidase products are not yet formally approved or are difficult to source reliably. This creates gaps in patient care, particularly in aesthetic medicine where unregulated filler procedures are common but emergency reversal products may not be available. For the drug delivery market, the concentration of recombinant hyaluronidase manufacturing in a small number of facilities creates supply chain risk, and any disruption could affect multiple biologic drug supply chains simultaneously.

Market Opportunities

-

New oncology applications and expanding biologic subcutaneous conversion pipeline

The pipeline of biologics being converted from IV to subcutaneous delivery using recombinant hyaluronidase is substantial and growing. Multiple cancer immunotherapies, anti-coagulants, and chronic disease treatments are in development or regulatory review as subcutaneous formulations. Each approval adds a new recurring revenue stream. The success of subcutaneous checkpoint inhibitors like atezolizumab (Tecentriq Hybreza) in 2024 demonstrates that even complex biologic antibodies can be delivered this way, opening a large new market segment.

Recent Developments

-

2024 (September): Roche received FDA approval for Tecentriq Hybreza, a subcutaneous formulation of atezolizumab combined with recombinant hyaluronidase using Halozyme's ENHANZE technology, allowing cancer patients to receive a treatment in minutes that previously required 30-60 minute IV infusions.

-

2023 (May): The FDA approved SKINVIVE by JUVÉDERM, a new intradermal microinjection product for cheek skin quality improvement, expanding the hyaluronic acid injectable market that creates parallel demand for hyaluronidase reversal products.

Key Players

Leading companies in the Hyaluronidase Market:

-

Halozyme Therapeutics Inc. – HYLENEX Recombinant

-

Sun Pharmaceutical Industries – Hyaluronidase Injection

-

PriMed Pharma – Hyaluronidase Products

-

CoLucid Pharmaceuticals – Ophthalmic Hyaluronidase

-

Amphastar Pharmaceuticals – Hyaluronidase Injection

-

Ethex Corporation – Hyaluronidase Injectable

-

Anika Therapeutics Inc. – Hyaluronic Acid Solutions

-

Bioregen Biomedical – Hyaluronidase Formulations

-

VWR International – Laboratory Grade Hyaluronidase

-

Merz Aesthetics – Belotero Filler and Reversal Support

-

Galderma S.A. – Restylane Filler and Hyaluronidase

-

Allergan Aesthetics (AbbVie) – Juvederm and HYLENEX

-

Roche Holding AG – Subcutaneous Biologic Formulations

-

Pfizer Inc. – ENHANZE-Based Subcutaneous Medicines

-

Johnson & Johnson – Janssen ENHANZE Collaboration

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.14 Billion |

| Market Size by 2035 | USD 2.67 Billion |

| CAGR | CAGR of 8.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Animal-Derived, Recombinant) • By Application (Drug Delivery Enhancement, Ophthalmic Surgery, Dermal Filler Reversal, Subcutaneous Fluid Administration, Oncology, Others) • By End-Use (Hospitals, Aesthetic Clinics, Ambulatory Surgical Centers, Research Labs, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Halozyme Therapeutics Inc., Sun Pharmaceutical Industries, PriMed Pharma, CoLucid Pharmaceuticals, Amphastar Pharmaceuticals, Ethex Corporation, Anika Therapeutics Inc., Bioregen Biomedical, VWR International, Merz Aesthetics, Galderma S.A., Allergan Aesthetics (AbbVie), Roche Holding AG, Pfizer Inc., Johnson & Johnson |

Frequently Asked Questions

North America leads, driven by the large U.S. aesthetics market and Halozyme's commercial drug delivery platform.

Animal-derived hyaluronidase holds the largest share at about 68.45%, though recombinant products are growing faster.

The main applications are drug delivery enhancement (subcutaneous biologic therapies), dermal filler reversal in aesthetics, and ophthalmic surgery.

The market was valued at USD 1.14 billion in 2025.

The market is expected to grow at a CAGR of 8.69% from 2026 to 2035.

Get in Touch