Hyperloop Technology Market Report Scope & Overview:

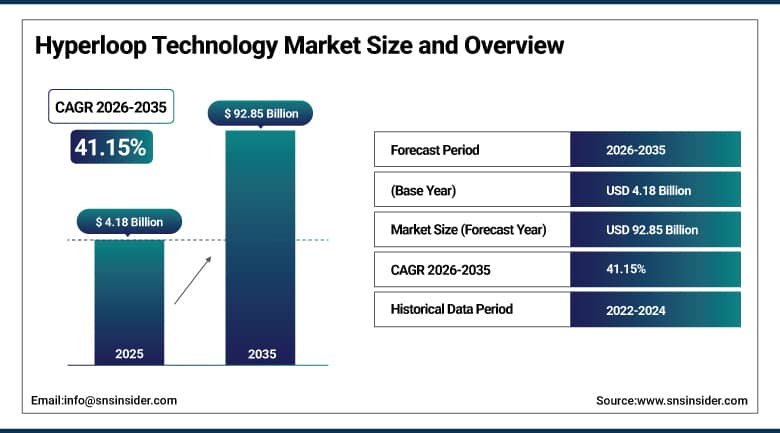

The Hyperloop Technology Market was valued at USD 4.18 Billion in 2025 and is expected to reach USD 92.85 Billion by 2035, growing at a CAGR of 41.15% from 2026 to 2035.

From a statistical perspective, there is clearly a buildup in terms of hype for the hyperloop technology market, where major route development is expected in the coming years by 2035 in regions such as North America, Europe, and the Asia Pacific region. There is clear government and private sector investment in infrastructure projects from 2020 to 2024, especially in the US, the UAE, and India. Travel times through hyperloop can be reduced up to 70% compared to conventional modes of travel. Hyperloop utilizes the principle of maglev and low-pressure tubes to provide ultra-high speed travel at speeds of up to 760 mph and close to zero emissions through the utilization of vacuum tube infrastructures and advancements in the propulsion system.

In October 2023, Hyperloop TT announced the completion of feasibility studies for a proposed hyperloop corridor connecting major metropolitan centres, demonstrating continued progress toward commercial route development despite the technology's early-stage status. The feasibility study completion represents an important project milestone whose successful technical and economic validation creates the foundation for subsequent government approval, private investment commitment, and eventual construction phase initiation that the hyperloop industry's commercial viability ultimately depends upon.

Market Size and Forecast

-

Market Size in 2026E: USD 5.90 Billion

-

Market Size by 2035: USD 92.85 Billion

-

CAGR: 41.15% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Hyperloop Technology Market - Request Free Sample Report

Hyperloop Technology Market Trends

-

Rising government and private sector investments are accelerating hyperloop infrastructure development, with pilot projects and feasibility studies advancing across key regions including the U.S., UAE, and India

-

Increasing public-private partnerships are supporting technology innovation, funding, and commercialization efforts for next-generation high-speed transportation systems

-

Continuous advancements in magnetic levitation and propulsion technologies are improving system efficiency, reliability, and operational performance for future hyperloop networks

-

Growing interest in cargo and freight transportation applications is expanding hyperloop opportunities beyond passenger mobility by enabling faster and more efficient long-distance logistics

-

Integration of hyperloop corridors into smart city and regional development plans is positioning the technology as a strategic component of future interconnected transportation and economic infrastructure systems

U.S. Hyperloop Technology Market Outlook

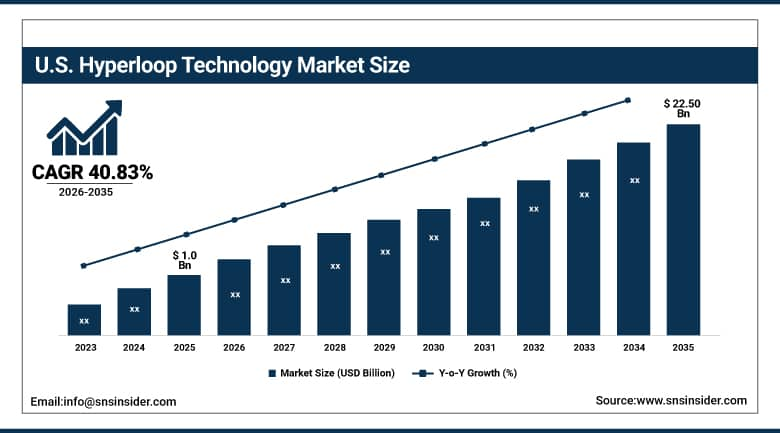

The U.S. Hyperloop Technology Market was valued at approximately USD 1.0 Billion in 2025 and is expected to reach approximately USD 22.50 Billion by 2035, growing at a CAGR of approximately 40.83%.

This rapid growth is driven by increasing demand for sustainable and efficient transportation solutions, with hyperloop technology offering ultra-fast, energy efficient, and low impact transit options that significantly reduce carbon emissions and alleviate traffic congestion. Pilot projects are underway across multiple U.S. states to demonstrate commercial viability, further accelerating interest and funding in the market. The Boring Company, Hyperloop TT, and various university research partnerships collectively define the domestic commercial and research landscape, with federal infrastructure investment programmes creating supportive policy conditions for continued hyperloop development and testing.

In January 2024, a major steel manufacturer partnered with IIT Madras and IIT Madras associated start up TuTr Hyperloop to advance hyperloop infrastructure component development and testing capability. The partnership demonstrates the cross-border collaborative ecosystem developing around hyperloop technology, where materials science expertise, academic research capability, and specialised engineering startups combine to accelerate the technical validation that commercial hyperloop deployment requires before route construction can proceed at meaningful scale.

Hyperloop Technology Market Segment Analysis

-

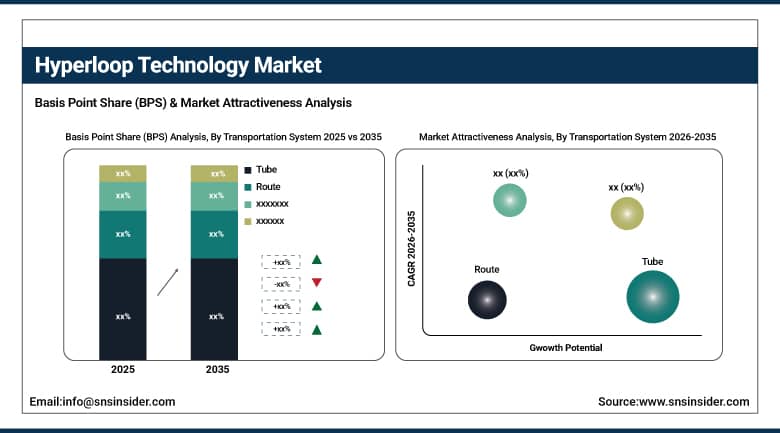

By Transportation System, the Tube segment dominated the Hyperloop Technology Market with approximately 38% share in 2025, while the Route segment is the fastest growing.

-

By Carriage Type, the Passenger segment dominated the Hyperloop Technology Market with approximately 55% share in 2025, while the Cargo/Freight segment is the fastest growing.

By Transportation System, tube dominates, route grows fastest

The tube segment retained the dominant transportation system position with approximately 38% of the hyperloop technology market in 2025. Hyperloop systems, which utilise low pressure tubes to shoot pods through a near vacuum environment at high speeds, offer an exciting alternative to traditional forms of transportation including cars, trains, and airplanes. Hyperloop can also withstand natural disasters and extreme weather events that would significantly disrupt all other modes of transportation. Because hyperloop tubes are located in controlled, sealed environments, these systems are less vulnerable to the destructive forces of natural disasters including floods, earthquakes, and hurricanes, allowing for uninterrupted service and greater reliability in adverse circumstances. The tube infrastructure represents the most capital-intensive single component of any hyperloop system, sustaining its commanding commercial position across the technology's overall component value chain.

The route segment is expected to register the fastest growth during the forecast period. Hyperloop connections mean they connect not only cities but also regions while incorporating economic development and integration between different geographical areas. Hyperloop routes reduce travel times between major urban centres, which enables business and leisure travel, sparks investment in neglected areas, and supports the growth of smaller cities and satellite communities along route corridors as hyperloop networks expand. Each new route feasibility study completed and each corridor advancing from planning to construction phase creates structured procurement growth that compounds with the broader hyperloop ecosystem's commercial maturation throughout the forecast period.

By Carriage Type, passenger dominates, cargo/freight grows fastest

The passenger segment retained the dominant carriage type position with approximately 55% of the hyperloop technology market in 2025. This dominance reflects the rapid growth of this segment with faster, more efficient, and sustainable modes of transportation in urban and intercity settings, supported by government assistance and technological development. Passenger transportation applications represent the most commercially visible and publicly discussed hyperloop use case, sustaining substantial pilot project investment and feasibility study activity across multiple global markets. Each metropolitan corridor whose passenger transportation demand creates structured business case justification for hyperloop investment sustains the passenger segment's commanding commercial position throughout the technology's early commercialisation phase.

The cargo and freight segment is projected to have the highest growth rate during the forecast period. There is an increasing call for more incredible and economic logistics solutions to expedite the shipment of goods over long distances as worldwide commerce and online shopping have expanded. Many corporations and research organisations have teams working with prototyping and testing hyperloop infrastructure components specifically optimised for freight applications, where the absence of passenger comfort and safety certification requirements creates a potentially faster commercial deployment pathway than passenger oriented hyperloop systems require before achieving regulatory approval for operational service.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

India |

38.4% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Hyperloop Technology Market Insights

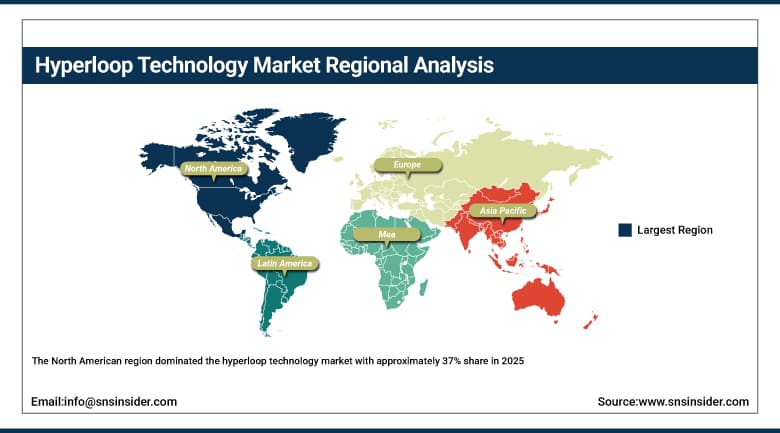

The North American region dominated the hyperloop technology market with approximately 37% share in 2025, owing to the rising demand for eco friendly transport solutions. With increasing concern about climate change and environmental impacts, the demand for hyperloop technology to help reduce carbon emissions and support green transportation has skyrocketed. The United States accounts for approximately 87.4% of North American revenues through The Boring Company, Hyperloop TT, and academic research partnerships' combined technology development and pilot project activity.

Canada contributes complementary North American revenue through its growing interest in sustainable intercity transportation alternatives, with feasibility studies exploring potential hyperloop corridors connecting major Canadian metropolitan centres to support the region's broader green transportation infrastructure objectives.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Hyperloop Technology Market Insights

Asia Pacific is the fastest growing regional hyperloop technology market, driven by significant infrastructure investment commitment and pilot project advancement across India and other rapidly developing economies. India accounts for approximately 38.4% of Asia Pacific revenues through its partnership ecosystem including major steel manufacturers, IIT Madras, and TuTr Hyperloop's collaborative infrastructure component development and testing programmes.

China and other emerging Asian economies represent additional commercial opportunity as smart city development initiatives and government backed transportation modernisation programmes create structured demand for next generation transit infrastructure investment that hyperloop technology development can address as the technology matures toward commercial deployment readiness.

Europe Hyperloop Technology Market Insights

Europe is a technically sophisticated hyperloop technology market where Hardt Hyperloop's domestic technology development and the European Union's sustainable transportation policy framework create supportive conditions for continued pilot project investment. Germany accounts for approximately 22.3% of European revenues through its strong engineering and infrastructure development capability supporting hyperloop component testing and validation activities.

The Netherlands and other Western European markets are significant secondary markets where Hardt Hyperloop's headquarters presence and the European Hyperloop Centre's testing infrastructure create consistent commercial activity. France and the United Kingdom's growing interest in sustainable high speed transportation alternatives sustains regional commercial momentum across the continent's hyperloop development ecosystem.

MEA & Latin America Hyperloop Technology Market Insights

The UAE leads MEA revenues through its commitment to next generation transportation infrastructure under national vision programmes, with feasibility studies exploring hyperloop corridors connecting major Gulf metropolitan centres and supporting Dubai's broader smart mobility ambitions. Saudi Arabia's Vision 2030 infrastructure modernisation programme and NEOM's futuristic city planning add complementary regional demand. Brazil leads Latin American revenues through its growing interest in sustainable intercity transportation alternatives that could address the region's infrastructure development challenges. Mexico's expanding transportation infrastructure investment and Argentina's growing sustainability focus collectively sustain growing regional market engagement through 2035.

Market Dynamics

Growth Drivers: Eco-friendly transportation demand and government-private collaboration acceleration

Global demand for transportation methods that are eco-friendly and save time is contributing to the rise of hyperloop technology adoption. Hyperloops offer super-fast travel speeds of up to 760mph with almost zero carbon footprint due to its ability to use magnetic levitation as well as tubes with low pressure. It meets climate change objectives of nations worldwide in addition to their development objectives. It is seen as an option by both governments and private investors to help overcome traffic congestion and fuel prices, thus making it increasingly popular. Pilot projects in the USA, India, UAE and other countries make it more interesting and financially feasible.

There is a rise in collaboration among governments, startups and technology companies in order to innovate in the field of hyperloop technology. Collaboration allows innovating and sharing expenses, thus becoming beneficial for all partners. Some examples of collaborations include Hyperloop TT, Hardt Hyperloop and other infrastructure firms partnering with infrastructure and mobility agencies to launch pilot projects. Many countries have already conducted studies with financial assistance aimed at integrating routes into transit network with growth potential especially in developing countries due to necessity of next generation transportation technology.

Restraints: Massive capital requirements and complex engineering challenges

Despite its futuristic appearance, the price of constructing hyperloop systems continues to be one of the most significant barriers. Creating vacuum tubes, special railway tracks, and unique propulsion systems is very expensive and requires billions of dollars to be invested. The necessity of conducting a lot of tests, obtaining permissions and buying land complicates this process greatly. Also, there are worries regarding the amount of energy required for creating low-pressure environments and maintaining the magnetic system. Such financial and technological barriers often prevent interested parties from implementing their plans, especially in the case of regions that do not have enough budgetary resources. Absence of profitability models and international standards often prevents countries from investing into such projects.

Absence of regulations and safety standards also complicates large scale implementation of this technology. As a unique mode of transportation, hyperloop is not regulated by existing laws and rules, and that creates many difficulties in legislation and safety evaluation. Issues related to travelling in closed vacuum tubes at a great speed, passengers' safety and comfort, and emergency measures also need to be evaluated carefully.

Opportunities: Public-private partnership expansion and cargo logistics applications

Collaborations between governments and technology firms are unlocking funding and innovation opportunities. The hyperloop market is witnessing a surge in collaborative efforts between governments, startups, and established technology companies, fostering innovation and reducing the financial burden on individual entities. Several countries have initiated feasibility studies with funding support to explore route integration into existing transit networks, creating new growth opportunities especially in emerging economies where there is a need for next generation transport to support smart city development and industrial growth.

Cargo and freight logistics applications represent the fastest growing commercial opportunity as worldwide commerce and online shopping expansion creates demand for more economic logistics solutions to expedite shipment of goods over long distances. Each freight focused hyperloop pilot project that demonstrates technical viability without the additional passenger safety certification burden creates a potentially faster commercial deployment pathway whose success could accelerate broader hyperloop technology validation and subsequent passenger application investment confidence.

Recent Developments:

-

2023: Hyperloop TT announced the completion of feasibility studies in October 2023 for a proposed hyperloop corridor connecting major metropolitan centres, demonstrating continued progress toward commercial route development.

-

2024: A major steel manufacturer partnered with IIT Madras and IIT Madras associated start up TuTr Hyperloop in January 2024 to advance hyperloop infrastructure component development and testing capability for the Indian market.

-

2023: Hardt Hyperloop announced the opening of the European Hyperloop Centre testing facility in the Netherlands in 2023, providing dedicated infrastructure for propulsion system and tube technology validation under controlled testing conditions.

-

2024: The Boring Company advanced its tunnel boring technology applications in 2024 with new contracts supporting underground transportation infrastructure development that shares technical synergies with hyperloop tube construction methodology.

-

2023: Virgin Hyperloop transitioned its technology development focus toward cargo and freight applications in 2023, recognising the potentially faster commercial deployment pathway that freight focused systems offer relative to passenger certified hyperloop infrastructure.

Hyperloop Technology Market Key Players

-

Hyperloop Transportation Technologies Inc.

-

Hardt Hyperloop B.V.

-

The Boring Company

-

Virgin Hyperloop

-

TransPod Inc.

-

Zeleros Hyperloop S.L.

-

TuTr Hyperloop

-

Nevomo Sp. z o.o.

-

DP World (Cargospeed)

-

Hyperloop One Global Inc.

-

SpaceX (Tunnel Technology)

-

Swisspod Technologies SA

-

Eurotube Foundation

-

China Aerospace Science and Industry Corporation

-

Siemens Mobility GmbH

-

Alstom SA

-

Bombardier Transportation

-

Larsen & Toubro Limited

-

Tata Steel Limited

-

Indian Institute of Technology Madras

Hyperloop Technology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.18 Billion |

| Market Size by 2035 | USD 92.85 Billion |

| CAGR | CAGR of 41.15% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Transportation System (Capsule, Tube, Propulsion System, Route) • by Carriage Type (Passenger, Cargo/Freight) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Hyperloop Transportation Technologies Inc., Hardt Hyperloop B.V., The Boring Company, Virgin Hyperloop, TransPod Inc., Zeleros Hyperloop S.L., TuTr Hyperloop, Nevomo Sp. z o.o., DP World (Cargospeed), Hyperloop One Global Inc., SpaceX (Tunnel Technology), Swisspod Technologies SA, Eurotube Foundation, China Aerospace Science and Industry Corporation, Siemens Mobility GmbH, Alstom SA, Bombardier Transportation, Larsen & Toubro Limited, Tata Steel Limited, Indian Institute of Technology Madras |

Frequently Asked Questions

The Hyperloop Technology Market is expected to grow at a CAGR of 41.15% from 2026 to 2035.

The global push for eco friendly and time efficient transportation systems offering ultra high speed travel with near zero emissions, and growing collaborations between governments, startups, and established technology companies that are fostering innovation and reducing the financial burden of pilot project development on individual entities.

The Hyperloop Technology Market was valued at USD 4.18 Billion in 2025.

North America dominated the Hyperloop Technology Market with approximately 37% share in 2025, while Asia Pacific is the fastest growing region driven by India's infrastructure investment commitment.

Get in Touch