Hysteroscopy Procedures Market Report Scope & Overview:

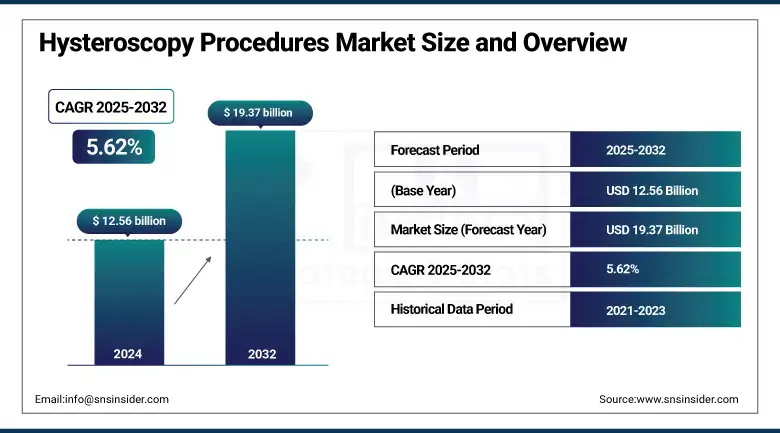

The hysteroscopy procedures market size was valued at USD 12.56 billion in 2024 and is expected to reach USD 19.37 billion by 2032, growing at a CAGR of 5.62% over the forecast period of 2025-2032.

The global hysteroscopy procedures market is growing at a steady rate, owing to an increase in the cases of gynaecological problems, such as fibroids, polyps, and abnormal uterine bleeding. Growing demand for minimally invasive diagnostic and operative procedures, technological advancements in the field of hysteroscopy devices, and rising focus of women on genital-related issues are other factors driving the hysteroscopy procedures market growth. The market is also driven by the increasing availability of outpatient surgical centers and better reimbursement policies. Developing countries and fertility clinics also heavily influence the increasing procedures globally.

To Get more information On Hysteroscopy Procedures Market - Request Free Sample Report

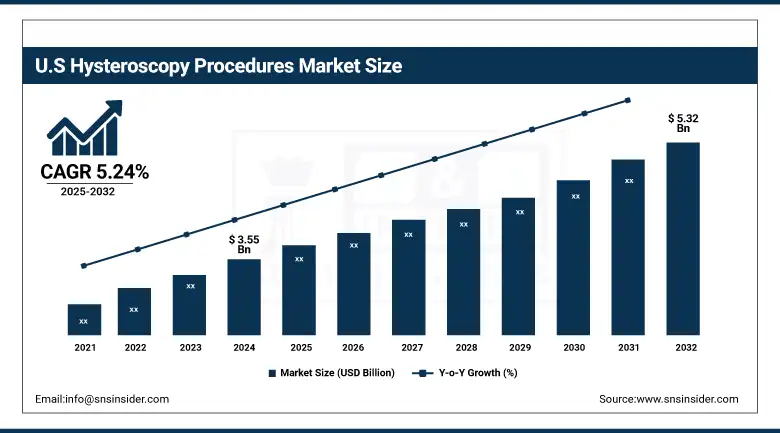

The U.S. hysteroscopy procedures market size was valued at USD 3.55 billion in 2024 and is expected to reach USD 5.32 billion by 2032, growing at a CAGR of 5.24% over the forecast period of 2025-2032.

The U.S. is the leading contributor to the hysteroscopy procedures market in North America, owing to a high prevalence of gynecological disorders, high adoption rates for minimally invasive surgeries, and a well-established healthcare system. This superiority is also reinforced by the strong presence of the dominant companies and reimbursement policies.

In 2024, it is projected that 116,930 women in the U.S. will be diagnosed with cancers of the reproductive system, and 33,850 will die from the disease. Endometrial cancer, or the lining of the uterus, is the most frequent gynecologic cancer. Ovarian cancer is the fifth leading cause of cancer death in women, and also kills more women than any other cancer of the female reproductive system.

Market Dynamics:

Drivers:

-

Increase in the Incidence of Gynecological Diseases is Boosting the Growth of the Market

The rising prevalence of gynecological diseases, including abnormal uterine bleeding, endometrial polyps, submucosal fibroids, and endometrial cancer, is playing a key role in the huge demand for hysteroscopy procedures. These conditions frequently necessitate diagnostic and therapeutic (therapeutic hysteroscopy) approaches that invasive hysteroscopic procedures can perform with high efficacy. Also, the increasing knowledge of women on early detection and prompt intervention of reproductive health problems is among the reasons that have led to the increase in the number of these procedures. Furthermore, lifestyle choices and later pregnancies, and hormonal imbalance have all seen an increase in such cases globally, and this has driven the need for hospitals and clinics to take up hysteroscopy as the norm in excellent patient care.

Global increase in fibroids: The number of incident cases of uterine fibroids increased from 5.77 million in 1990 to 9.64 million in 2019, representing an increase of 67% according to the NHI.

AUB-Abnormal Uterine Bleeding: In India, 17% of women are affected with AUB, 45% of which are polyps and 38% are submucosal fibroids, leading to growth in office hysteroscopy.

-

Technological Development in Hysteroscopic Devices Driving the Market

Advances in hysteroscopic technology, including the availability of smaller and more flexible hysteroscopes, three-dimensional high-definition imaging systems, and digital integration, have increased the accuracy and safety of procedures. Device miniaturization allows for office-based hysteroscopy without anaesthesia, which is a more patient-friendly option. Moreover, the introduction of novel equipment, such as bipolar electrosurgery, fluid management systems, and robotic assistance has improved procedural effectiveness. These advancements not only shorten procedures and decrease complications but also promote a transition to an office-based or same-day care environment, driving market expansion.

Single-use Minerva Surgical launched the HERizon Hysto‑Kit for single-use office hysteroscopy in May 2025 to expedite outpatient treatment.

Restraints:

-

Expensive Advanced Hysteroscopic Equipment and Procedures are Acting as a Restraint for the Market Segments

The expenses of conducting hysteroscopy procedures can be an important constraint, in particular in low-resource settings. Modern-day hysteroscopy systems, especially those with HD imaging, fluid management systems, and combined operative capabilities, are capital-intensive. Recurring expenses, including single-use hysteroscopes, maintenance, and exchange of visualization system units, should also be accounted for by hospitals and clinics.

These treatments may not be affordable for patients, especially in countries where insurance is limited or reimbursement is insufficient. In countries, where healthcare is heavily out-of-pocket, the cost of full diagnostic or surgical hysteroscopy can be a deterrent to women seeking this minimally invasive surgery, leading them to choose cheaper but poorer diagnostic and surgical procedures, such as blind D&C.

Therefore, despite the clinical advantages, the cost to perform hysteroscopy procedures remains a barrier to wider usage, particularly, in low- and middle-income countries.

Segmentation Analysis:

By CPT Code

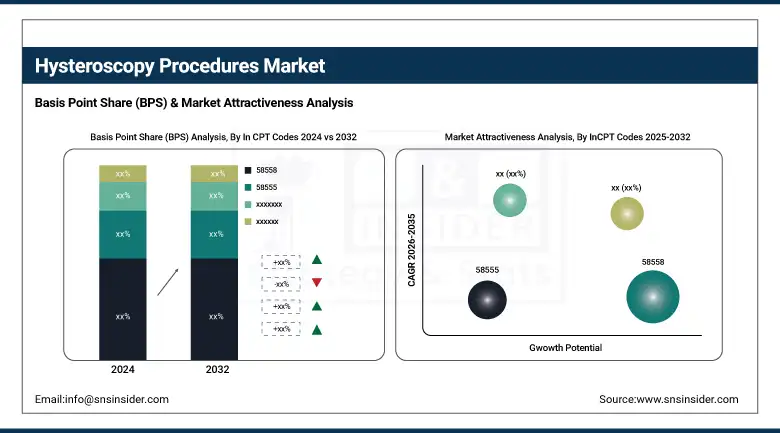

The CPT code 58558 segment led the hysteroscopy procedures market share in 2024 with a 33.12%, due to its versatile application in clinics and regular procedures. This code applies to hysteroscopy with sampling (endometrial biopsy or polypectomy), which is one of the most common gynecologic procedures. Due to the increasing prevalence of endometrial polyps and abnormal uterine bleeding (AUB), there is an increase in diagnostic and therapeutic hysteroscopic procedures. This would result in further penetration of 58558 as the lead procedure code in the market, including hospitals, in addition to the clinic volume.

The CPT code 58562 segment is anticipated to grow at the fastest CAGR over the forecast period due to high traction for hysteroscopic myomectomy procedures. This code is for hysteroscopy with removal of leiomyomata (fibroids), which are a major source of infertility, pelvic pain, and abnormal bleeding among women of reproductive age. Technological developments, along with a growing trend for minimally invasive surgery and increasing demand for uterus-sparing treatments, are likely to boost the demand for the removal of fibroids through a hysteroscopic approach. However, the increasing prevalence and diagnosis of uterine fibroids globally are driving the adoption of 58562-coded procedures, and making it the fastest-growing segment.

By Type of Procedure

The operative hysteroscopy segment held the largest share of the hysteroscopy procedures market in 2024, with a 76.31%, due to its wide application in the treatment of intrauterine pathology (including fibroids, polyps, adhesions, and septa). In contrast to diagnostic hysteroscopy, which visualizes and diagnoses, operative hysteroscopy allows direct therapeutic intervention in the same session. This two-in-one feature minimizes the necessity of repetition, accelerates healing and resolution times, and increases clinical effectiveness. The growing word of mouth among gynecologists for minimally invasive treatment methods also contributed to the supremacy of operative hysteroscopy in 2024.

The operative hysteroscopy segment is anticipated to witness the fastest growth during the forecast period on account of technological advancements in surgical devices, imaging, and outpatient procedure capabilities. Awareness and early diagnosis of uterine pathology, and patient demand for less invasive alternatives to hysterectomy, have led to more operative interventions. Growth in the number of ambulatory surgical centers and an increase in healthcare penetration in developing regions are also expected to be key drivers for the high adoption rate of the operative hysteroscopy market, thereby propelling its growth throughout the forecast period.

By Application

The endometrial ablation segment held the largest share of the market in 2024 due to the adoption of endometrial ablation as an alternative to hysterectomy for the treatment of abnormal uterine bleeding (AUB), especially in women who prefer minimally invasive procedures, which has driven the growth of this market. This treatment is efficacious, with a quick recovery time and usually an outpatient type procedure, and therefore, both patients and providers find it attractive. Increasing incidence of AUB, particularly in women under perimenopausal age, and increasing easy accessibility of advanced hysteroscopic ablation devices were some of the other factors driving the segment to its leading position in 2024.

The myomectomy (removal of fibroids) segment is expected to register the highest growth during the forecast period, owing to the rising global prevalence of uterine fibroids, especially among women of reproductive age. Advancements in hysteroscopic methods and instruments are providing safer, more effective methods for removing fibroids, and an increasing number of women are choosing this uterus-preserving procedure. Moreover, increased consciousness about fertility preservation and the preference for minimally invasive treatment options of fibroid-induced symptoms are propelling the demand for hysteroscopic myomectomy, thereby driving the market growth during the forecast years.

By End-User

The hospitals segment held the largest share for the hysteroscopy procedures market in 2024, with a 51.14%, with its well-established healthcare infrastructure, availability of advanced hysteroscopic instruments, and skilled workforce for carrying out both diagnostic and advanced operative procedures. Hospitals remain the preferred choice of patients with comorbidities and patients who need multidisciplinary care under a single roof. Moreover, a greater number of patient admissions, insurance, and treatment of post-operative complications also boosted the prominence of the segment in 2024.

The ambulatory surgical centers (ASCs) are anticipated to witness the fastest growth over the forecast period on account of the rising preference for outpatient minimally invasive surgeries. ASCs provide a cost-effective, convenient, and faster alternative to hospital-based procedures, with shorter waiting periods and patient turnover. The increasing need for same-day procedures and the rise in payment policies for outpatient care are acting as high-impact drivers in the rapid growth of ASCs in the hysteroscopy procedures market.

Regional Analysis:

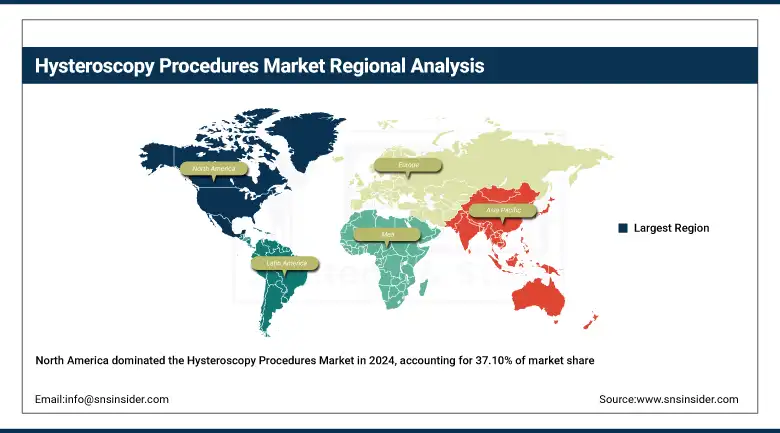

North America dominated the hysteroscopy procedures market growth in 2024, with a 37.10% market share, is significantly driven by the presence of well-established healthcare infrastructure in the region, along with early adoption of minimally invasive procedures, high level of awareness among patients, and healthcare professionals about gynecological disorders. The popularity of the procedure in the region is attributed to the high penetration of the major medical device manufacturers, regular product releases, and reimbursement policies that support the use of diagnostic and operative hysteroscopy. Moreover, the increasing prevalence of uterine diseases and an aging female population drive the demand for hysteroscopic procedures in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region in the hysteroscopy procedures market analysis, owing to the rising funds for improving the health care infrastructure and operations, and a surge in awareness of minimally invasive procedures for treatment. Fast-growing urbanization, higher levels of discretionary spending, and growing government efforts to enhance accessibility to gynecological care are driving procedural numbers. Another factor contributing to market growth is the increasing incidence of uterine anomalies and a large pool of target patient population in countries, such as China, India, and Japan, thereby positioning the region as a prolific growth pocket.

The European hysteroscopy procedures market trend is growing at a steady pace owing to the growing awareness of minimally invasive gynecological procedures and the surging number of uterine disorders, including fibroids and polyps. The market in the region is propelled by a well-established healthcare infrastructure, the presence of major market players, and increasing uptake of advanced hysteroscopic devices in public and private hospitals. Moreover, increasing government campaigns for early diagnosis and treatment of infertility are also contributing to the growth of the market in most of the developed European nations.

The hysteroscopy procedures market is growing at a moderate pace in Latin America and the Middle East & Africa (MEA). An increasing awareness of women’s healthcare and the development of healthcare infrastructure, and the availability of skilled gynecologists in Latin America, are driving the hysteroscopic procedures. Nevertheless, reimbursement issues and economic restrictions remain a major obstacle to general acceptance.

Market growth in MEA is being bolstered by the ongoing healthcare systems, especially in GCC countries. Efforts from governments to promote quality and maternal & reproductive health are, in turn, bolstering market growth as a surge in spending is witnessed in the minimally invasive sector.

Key Players:

The hysteroscopy procedures market companies are Olympus Corporation, Hologic, Inc., Stryker Corporation, Karl Storz SE & Co. KG, Richard Wolf GmbH, Medtronic plc, CooperSurgical, Inc., Boston Scientific Corporation, Cook Medical, Inc., MedGyn Products, Inc., B. Braun Melsungen AG, Johnson & Johnson (Ethicon Inc.), LiNA Medical ApS, Maxer Endoscopy GmbH, Smith & Nephew plc, WISAP Medical Technology GmbH, EndoMed Systems GmbH, Rudolf Medical GmbH + Co. KG, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Henke-Sass, Wolf GmbH, and other players.

Recent Developments:

-

November 2024 – Olympus Corporation of the Americas shared its attendance at the American Association of Gynecological Laparoscopists (AAGL) global Congress, where it presented its wide-ranging portfolio of gynecologic solutions, highlighting innovation in minimally invasive techniques.

-

May 2023 – B. Braun unveiled its innovation, the AESCULAP EinsteinVision 3.0 FI laparoscopic system, at the International Society for Gynecologic Endoscopy (ISGE), marking its focus on better visualization and surgical accuracy.

-

October 2023 – Hologic, Inc. said it had formed a strategic collaboration with the American Association of Gynecologic Laparoscopists (AAGL) and Inovus Medical to further training and education in gynecologic laparoscopy using advanced simulation technologies.

Hysteroscopy Procedures Market Report Scope:

Report Attributes Details Market Size in 2024 USD 12.56 Billion Market Size by 2032 USD 19.37 Billion CAGR CAGR of 5.62% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By CPT Codes (58555, 58558, 58562, 58340, 58563, 58565, 58353, 58561, 74740, and Others)

• By Type of Procedure (Diagnostic Hysteroscopy, Operative Hysteroscopy)

• By Application (Myomectomy, Polypectomy, Endometrial Ablation, Adhesiolysis, Tubal Sterilization, Others)

• By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Gynecology Clinics, Fertility Centers)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles The hysteroscopy procedures market companies are Olympus Corporation, Hologic, Inc., Stryker Corporation, Karl Storz SE & Co. KG, Richard Wolf GmbH, Medtronic plc, CooperSurgical, Inc., Boston Scientific Corporation, Cook Medical, Inc., MedGyn Products, Inc., B. Braun Melsungen AG, Johnson & Johnson (Ethicon Inc.), LiNA Medical ApS, Maxer Endoscopy GmbH, Smith & Nephew plc, WISAP Medical Technology GmbH, EndoMed Systems GmbH, Rudolf Medical GmbH + Co. KG, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Henke-Sass, Wolf GmbH, and other players.

Frequently Asked Questions

Ans: North America dominated the Hysteroscopy Procedures Market in 2024.

Ans: The “58558” segment dominated the Hysteroscopy Procedures Market.

Ans: The hysteroscopy procedures market companies are Olympus Corporation, Hologic, Inc., Stryker Corporation, Karl Storz SE & Co. KG, Richard Wolf GmbH, Medtronic plc, CooperSurgical, Inc., Boston Scientific Corporation, Cook Medical, Inc., MedGyn Products, Inc., B. Braun Melsungen AG, Johnson & Johnson (Ethicon Inc.), LiNA Medical ApS, Maxer Endoscopy GmbH, Smith & Nephew plc, WISAP Medical Technology GmbH, EndoMed Systems GmbH, Rudolf Medical GmbH + Co. KG, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Henke-Sass, Wolf GmbH, and other players.

Ans: The Hysteroscopy Procedures Market was USD 12.56 billion in 2024 and is expected to reach USD 19.37 billion by 2032.

Ans: The Hysteroscopy Procedures Market is expected to grow at a CAGR of 5.62% during 2025-2032.

Get in Touch