Immersive Training Market Report Scope & Overview:

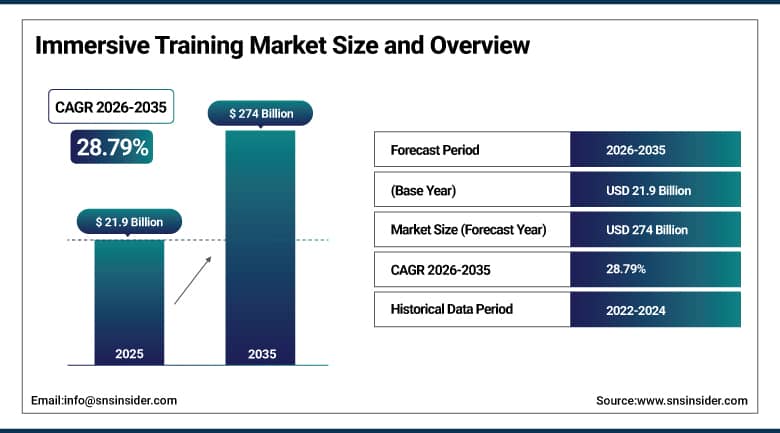

Immersive Training Market was valued at USD 21.9 billion in 2025 and is expected to reach USD 274 billion by 2035, growing at a CAGR of 28.79% from 2026-2035.

The Immersive Training Market is showing signs of growth due to the growing use of AR and VR technologies, the rising demand for simulation-based training, increased focus on workforce upskilling, and improved performance of training programs, which in turn help organizations boost their efficiency and productivity levels.

PwC's VR training effectiveness study across 10,000 participants found that VR-trained employees were 275% more confident in applying skills learned versus classroom training, with 4x faster training completion and 3.75x higher emotional connection to the content. The U.S. Department of Defense has invested over USD 2 billion in simulation-based training systems across service branches, citing documented improvements in mission readiness and trainee retention.

Immersive Training Market Size and Forecast

-

Market Size in 2025: USD 21.9 Billion

-

Market Size by 2035: USD 274 Billion

-

CAGR: 28.79% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Immersive Training Market - Request Free Sample Report

Immersive Training Market Trends

- AI-powered adaptive simulation is moving beyond scripted training scenarios toward dynamically generated challenges that respond to individual trainee decisions in real time, creating genuinely unique training experiences.

- Cloud-based immersive training delivery is enabling multi-site training cohorts to share the same virtual environment simultaneously, making collaborative training exercises practical for geographically distributed organizations.

- Haptic feedback integration into VR training systems is adding tactile realism to surgical simulation, industrial equipment training, and physical therapy rehabilitation in ways that pure visual-audio simulation cannot achieve.

- Eye-tracking integration in AR/VR headsets is generating granular trainee attention data that training managers can use to identify where learners lose focus, look in the wrong direction, or miss critical visual cues.

- 5G network infrastructure is enabling high-fidelity AR training overlay delivery to industrial facilities without the latency that wired-only setups previously required for real-time holographic instruction.

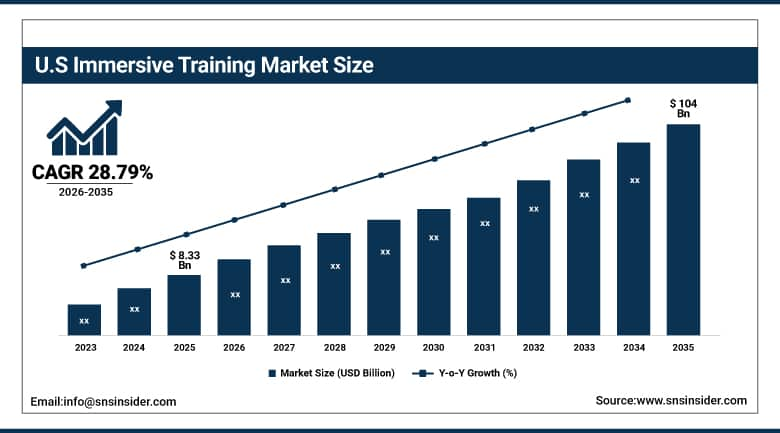

U.S. Immersive Training Market was valued at USD 8.33 billion in 2025 and is expected to reach USD 104 billion by 2035, growing at a CAGR of 28.79% from 2026-2035.

U.S. Immersive Training Market will witness growth owing to increased adoption rates of AR & VR technology in the defense sector, healthcare sector, and enterprises. Factors that drive growth in the market include increased adoption rates of simulation-based technology, increased focus on workforce training, better training outcomes, and investments in learning solutions.

The U.S. Army's Synthetic Training Environment program a USD 2.7 billion contract to create a globally scalable immersive training platform is one of the largest single military simulation procurements in history and reflects the DoD's commitment to simulation-based readiness as a strategic military capability. The Association of American Medical Colleges documents that surgical simulation training is now integrated into 85% of U.S. general surgery residency programs.

Immersive Training Market Segment Analysis

-

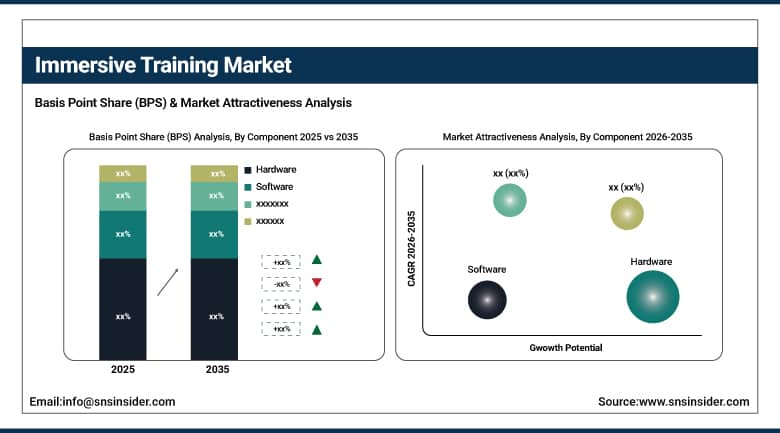

By Component, Hardware segment dominated with ~47% share in 2025; Software segment expected to grow fastest (CAGR).

-

By Technology, Virtual Reality (VR) segment dominated the Immersive Training Market in 2025; Mixed Reality (MR) segment expected to grow fastest (CAGR).

-

By Industry, Gaming segment dominated the Immersive Training Market in 2025; Healthcare segment expected to grow fastest (CAGR).

By Component: Hardware dominates, Software growing fastest

Hardware commanded approximately 47% of the Immersive Training Market's revenue in 2025, a position reflecting the capital-intensive nature of establishing immersive training infrastructure. The physical devices VR headsets, AR glasses, motion controllers, haptic vests, omnidirectional treadmills, tracking sensors, and the computing infrastructure that drives them represent the primary cost item in any immersive training deployment. Organizations that commit to immersive training must first make substantial hardware investments before their first trainee enters a simulation. Meta Quest Pro, Microsoft HoloLens 2, Varjo's enterprise VR headsets, and Apple Vision Pro each represent different price points and capability profiles in a commercial hardware market that serves everything from USD 400 consumer-grade deployment to USD 10,000+ enterprise-grade headsets with precision optics and extended battery life designed for professional use.

Software is the fastest-growing component segment, and the shift reflects the market's maturation from hardware-centric deployment to content-centric value creation. Organizations that already own VR hardware are asking which training content will deliver the best outcomes for their next investment dollar. Simulation authoring platforms including Unity-based training content tools, purpose-built simulation environments from companies like Mursion, Talespin, and STRIVR are becoming the primary value-add layer.

By Technology: VR dominates, Mixed Reality growing fastest

Virtual Reality held the dominant technology position in the Immersive Training Market in 2025, driven by its ability to create fully controlled, distraction-free training environments where trainees have complete immersion in the simulated scenario without visual or auditory interruptions from their physical surroundings. VR's total environmental substitution you see nothing except what the simulation presents is uniquely valuable for high-stakes training scenarios where incomplete presence or divided attention would undermine the training goal. Surgical simulation requires the trainee's complete visual field to be the operative site. Firefighting simulation requires the trainee to experience smoke, heat indicators, and structural uncertainty that can only be simulated if nothing else is visible.

Mixed Reality which combines real-world visual perception with overlaid digital information, instruction, and simulation elements is growing at the fastest technology CAGR because it enables training in the actual context where work occurs rather than in an isolated simulation chamber. An MR-equipped technician learning to maintain industrial machinery sees their actual machine, with digital overlays highlighting which fasteners to loosen, showing X-ray views of internal components, and flagging safety hazards in real time. A surgeon using an AR overlay during a procedure sees the patient with anatomical reference information integrated into their visual field rather than requiring them to look away at a separate screen.

By Industry: Gaming dominates, Healthcare growing fastest

The Gaming industry held the dominant position in the Immersive Training Market's revenue breakdown in 2025 which requires a moment of explanation given that the market is defined around training rather than entertainment. The reason is that gaming companies were the earliest, heaviest, and most technically sophisticated investors in VR/AR content production and deployment infrastructure, meaning that gaming-adjacent content game design training, esports coaching platforms, VR game engine development education sits alongside the market's more traditional training applications in the same commercial category. Game development schools using VR to train future game designers, esports academies using VR simulation for competitive skill development, and VR content studios training their own staff in immersive production represent gaming industry training demand that is genuinely substantial.

Healthcare is positioned to grow at the fastest CAGR through the forecast period, and the reasons are compelling from both clinical and commercial perspectives. Patient safety outcomes are directly linked to trainee preparation quality in medicine, and immersive simulation is demonstrably better than conventional training methods at preparing practitioners for the procedural, cognitive, and emotional demands of clinical work. Medical schools are building simulation centers with surgical simulators, emergency response scenarios, and patient communication practice environments that allow students to fail safely — developing the pattern recognition and procedural fluency that clinical experience builds, without the patient risk that comes with learning on real patients. The military medicine training sector adds additional healthcare demand: combat medic, flight surgeon, and military nurse training programs across multiple countries are deploying VR simulation at scale for trauma management, battlefield triage, and medevac scenario practice.

Immersive Training Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

89% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

South Korea |

35% |

|

Middle East & Africa |

UAE |

40% |

|

Latin America |

Brazil |

50% |

North America Immersive Training Market Insights

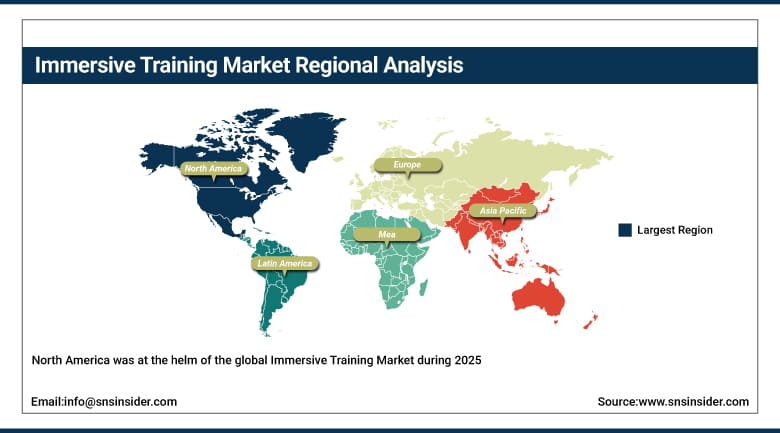

North America was at the helm of the global Immersive Training Market during 2025, buoyed by exceptional government defense training investments, a robust corporate learning technologies ecosystem, and high-density presence of VR and AR technology firms globally. The utilization of simulation training in the U.S. military pre-dated the advent of VR by decades, and the programs include the F-35 aircraft flight simulator system, the gaming-driven training system used in the army, and the virtual shipboard systems used by the navy, forming the bedrock of immersive training in the U.S. military that went on to define corporate and healthcare frameworks for adopting immersive training systems. In the corporate world, HR technology investments among Fortune 500 companies that consider training and development as a competitive edge drives demand for premium immersive training services from Walmart, JPMorgan Chase, and Boeing, among others.

Meta's Reality Labs division has invested over USD 36 billion in VR/AR hardware and software development since 2014, creating the consumer-grade hardware ecosystem that makes enterprise VR training deployment economically viable. The U.S. National Science Foundation's Future of Work program has funded immersive training research at over 40 universities, sustaining the academic research-to-commercial pipeline.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Immersive Training Market Insights

Asia Pacific is the fastest-growing regional Immersive Training Market, propelled by South Korea's advanced technology manufacturing ecosystem, Japan's precision industrial training culture, China's industrial expansion and military modernization, and India's growing IT and manufacturing training demand. South Korea's chaebols Samsung, LG, Hyundai, and SK have been among the earliest industrial companies globally to implement factory-floor AR training overlays for manufacturing quality control and equipment maintenance, driven by Korea's position as an advanced manufacturing export economy where workforce precision is a competitive differentiator. China's People's Liberation Army has publicized extensive simulation-based training programs, and the country's domestic VR hardware and content industry companies including ByteDance's Pico, iQIYI VR, and Nreal is building a supply-side ecosystem that supports military and civilian training deployment.

South Korea's Ministry of Science and ICT has dedicated KRW 500 billion to immersive technology industrial application programs through 2027, with manufacturing training identified as a priority application under the Digital New Deal initiative. Japan's Ministry of Economy, Trade and Industry has funded immersive training pilot programs in manufacturing, logistics, and construction through the Society 5.0 framework.

Europe Immersive Training Market Insights

Europe holds a significant share of the global Immersive Training Market, with the United Kingdom, Germany, France, and the Nordic countries as the primary adoption markets. Europe's strength in this market is concentrated in industrial training Airbus uses VR extensively for aircraft maintenance training, Siemens deploys AR overlays for industrial equipment service, and Volkswagen has built virtual reality training centers at its major production facilities. The UK's National Health Service has been one of the world's most active public healthcare systems in evaluating and deploying VR training for clinical staff, with documented programs in surgical training, mental health care simulation, and emergency response preparation at multiple NHS trusts. European defense programs NATO's simulation training networks and bilateral defense simulation investments by Germany, France, and the UK add public sector immersive training demand that sustains premium hardware and content procurement.

Airbus has documented that its VR-based A320 maintenance training program reduces qualification time by 30% and delivers 92% of the learning outcomes achieved by conventional hands-on training at 60% of the cost per trainee completion. The UK's NHS Digital has committed to deploying VR mental health training to 40,000 clinical staff across NHS trusts by 2027 as part of its mental health workforce development strategy.

Middle East & Africa and Latin America Immersive Training Market Insights

The Middle East is investing in immersive training primarily through oil and gas sector workforce development, military training modernization, and the ambitious smart city and tourism sector development programs of the UAE and Saudi Arabia. Saudi Aramco has deployed VR training simulators for oil refinery operations, pipeline maintenance, and safety emergency response at its major facilities, motivated by both workforce safety outcomes and the operational efficiency of training without disrupting production processes. The UAE's EDGE defense group has announced immersive military simulation programs aligned with the country's defense technology nationalization goals. Africa's immersive training market is in its earliest stages, with limited deployment outside South Africa's mining and manufacturing sectors, though mobile-accessible AR training approaches that do not require full VR headsets are beginning to find application in agricultural extension and healthcare worker training programs.

Immersive Training Market Growth Drivers:

-

High-risk industry skill gaps and proven training effectiveness driving sustained global immersive training market growth

Training outcomes research consistently delivers a finding that justifies the investment case for immersive training in high-stakes sectors: VR and AR-based training produces better skill retention, faster competency development, and lower error rates in real-world application than conventional training methods in physically complex, dangerous, or high-consequence skill domains. When a hospital can demonstrate that VR surgical simulation reduces residents' operative errors, or when a military can demonstrate that flight simulator hours translate directly to combat mission readiness, the argument for immersive training investment becomes straightforward organizational risk management rather than technology enthusiasm. The global shortage of experienced professionals in trades including aircraft maintenance, industrial welding, surgical practice, and emergency medicine creates additional urgency immersive simulation enables faster qualification of the people who are entering these fields to replace retiring workers, compressing training timelines that conventional methods require.

Oxford Economics and the World Economic Forum jointly estimate that skills shortages in technical trades will cost global economies over USD 8.5 trillion in unrealized productivity by 2030 a figure that makes accelerated, outcome-effective immersive training not a luxury but an economic necessity.

Immersive Training Market Restraints:

-

High hardware costs and content development complexity limiting immersive training adoption among SMEs and developing markets

The economics of immersive training deployment still work most favorably for large organizations with significant training budgets and substantial learner populations to amortize content development costs across. A bespoke VR training module covering a complex industrial maintenance procedure can cost USD 50,000-500,000 to develop, depending on the fidelity of simulation, the range of scenarios, and the integration with enterprise LMS platforms. When that content investment is spread across 10,000 trained employees, the per-learner cost is modest. When it must be absorbed across 100 employees, it is difficult to justify relative to conventional training alternatives. This cost structure inherently favors large enterprises, leaving SMEs which collectively employ the majority of workers globally dependent on generic off-the-shelf immersive training content that may not adequately address their specific operational contexts.

Immersive Training Market Opportunities:

-

AI-driven simulation personalization and enterprise metaverse adoption creating transformative immersive training market opportunities

Generative AI applied to simulation content creation represents the most commercially significant cost-reduction opportunity for immersive training at scale. If AI can generate realistic, contextually appropriate training scenarios from a brief specification rather than requiring months of 3D modeling, scripting, and testing by a development team, the cost-per-module economics of immersive training change dramatically in favor of broader adoption. Several companies including Mursion, Bodyswaps, and Oxford Medical Simulation are actively developing AI-generated scenario systems that allow training managers to specify the learning objectives they want to achieve and receive simulation environments built automatically around those objectives. As these systems mature, the content development cost barrier that currently prices SMEs out of bespoke immersive training will diminish, expanding the accessible market by an order of magnitude.

Recent Developments:

-

2026: Meta launched its Business Suite for Quest enterprise VR training, an integrated platform combining content management, multi-user session management, performance analytics, and LMS integration in a single subscription offering targeting Fortune 500 HR and L&D departments deploying VR training at scale across thousands of headsets with centralized content administration.

-

2025: Microsoft HoloLens 2 Industrial Edition received IEC 60068 environmental certification for dust, vibration, and temperature resistance, enabling AR training overlay deployment in active factory floor, construction, and offshore oil and gas environments where previous generation hardware could not reliably operate.

Immersive Training Market Key Players

Some of the Immersive Training Market Companies

-

Meta Platforms Inc. (Quest)

-

Microsoft Corporation (HoloLens)

-

Sony Interactive Entertainment

-

Oculus VR (Meta)

-

STRIVR Labs Inc.

-

Mursion Inc.

-

Talespin Reality Labs

-

Oxford Medical Simulation

-

Bodyswaps Ltd.

-

SimX Inc.

-

Pixo VR

-

Prisms of Reality

-

Osso VR Inc.

-

Virti Ltd.

-

Varjo Technologies

-

Immerse Inc.

-

Learn Brands Inc.

-

Walmart Academy

-

Labster ApS

-

Uptale SAS

Immersive Training Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.9 Billion |

| Market Size by 2035 | USD 274 Billion |

| CAGR | CAGR of 28.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Technology (Virtual Reality, Augmented Reality, Mixed Reality, Others) • By Industry (Gaming, Healthcare, Military & Defense, Manufacturing, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Meta Platforms Inc. (Quest), Microsoft Corporation (HoloLens), Sony Interactive Entertainment, Oculus VR (Meta), STRIVR Labs Inc., Mursion Inc., Talespin Reality Labs, Oxford Medical Simulation, Bodyswaps Ltd., SimX Inc., Pixo VR, Prisms of Reality, Osso VR Inc., Virti Ltd., Varjo Technologies, Immerse Inc., Learn Brands Inc., Walmart Academy, Labster ApS, Uptale SAS |

Frequently Asked Questions

Ans: The Mixed Reality segment is expected to register the fastest CAGR in the Immersive Training Market through 2035.

Ans: The Hardware segment dominated with approximately 47% share in 2025; Software is the fastest growing.

Ans: The Immersive Training Market was valued at USD 21.9 billion in 2025.

Ans: The Immersive Training Market is expected to grow at a CAGR of 28.79% from 2026 to 2035.

Ans: North America dominated the Immersive Training Market in 2025.

Get in Touch