In Vitro Fertilization (IVF) Market Report Scope & Overview:

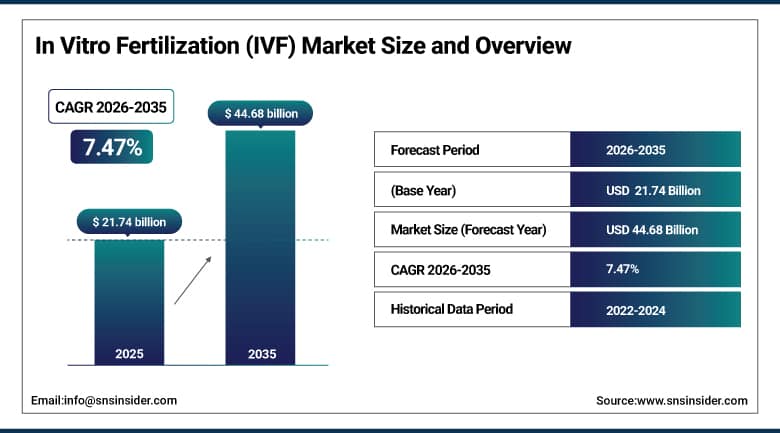

The In Vitro Fertilization (IVF) Market size was valued at USD 21.74 Billion in 2025 and is projected to reach USD 44.68 Billion by 2035, growing at a CAGR of 7.47% during 2026–2035.

The In Vitro Fertilization (IVF) market is growing rapidly owing to the high incidence of infertility among people, the high degree of awareness about IVF procedures, and the developments in the field of infertility treatments. The developments in IVF procedures, the high success rates of IVF treatments, and the adoption of minimally invasive techniques are the major growth drivers for the In Vitro Fertilization market. The high degree of accessibility to IVF treatments, along with the supportive government policies towards healthcare, is also driving the market. The preference for personalization in IVF treatments is also influencing the market.

In Vitro Fertilization (IVF) Market Size and Forecast:

-

Market Size in 2025: USD 21.74 Billion

-

Market Size by 2035: USD 44.68 Billion

-

CAGR: 7.47% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On In Vitro Fertilization (IVF) Market - Request Free Sample Report

In Vitro Fertilization (IVF) Market Key Trends:

-

Increasing adoption of advanced reproductive technologies like ICSI and preimplantation genetic testing.

-

Rising preference for fertility preservation and egg/sperm freezing.

-

Integration of digital tools and AI for personalized IVF treatment planning.

-

Growing demand for minimally invasive and high-success-rate IVF procedures.

-

Expansion of fertility clinics offering comprehensive and patient-centric services.

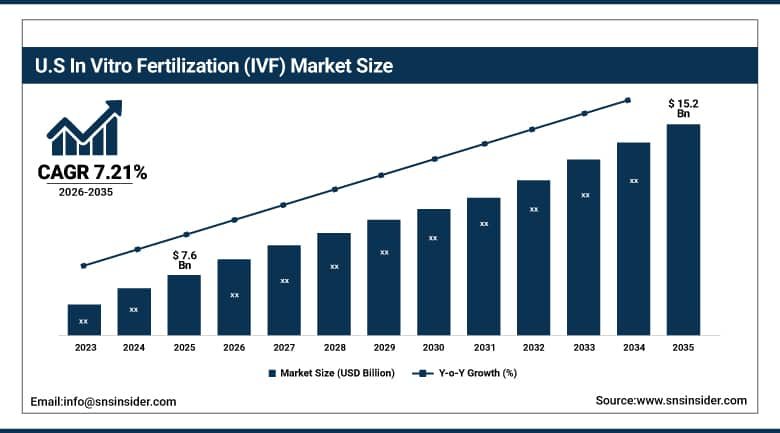

The U.S. In Vitro Fertilization (IVF) Market has been valued at USD 7.6 Billion in 2025 and is expected to reach USD 15.2 Billion in 2035, growing at a CAGR of 7.21% from 2026 to 2035. Growth is driven by rising infertility rates, advancements in reproductive technologies, increased awareness, greater accessibility to fertility treatments, supportive healthcare policies, and growing demand for personalized assisted reproductive solutions.

In Vitro Fertilization (IVF) Market Drivers:

-

Rising infertility rates and advancements in assisted reproductive technologies drive IVF market growth.

The major factor that is contributing to the growth of the IVF market is the rise in the number of infertile people due to the change in lifestyle. Technological advancements in IVF procedures such as intracytoplasmic sperm injection, preimplantation genetic testing, culture media, etc., are also contributing to the growth of the IVF market. In addition, awareness about ART procedures, as well as government initiatives, is also contributing to the growth of the IVF market.

In Vitro Fertilization (IVF) Market Restraints:

-

High treatment costs and ethical concerns limit market adoption.

The IVF industry is affected by various challenges, including the high cost of IVF services, which may limit access in low- and middle-income regions. Ethical concerns regarding embryo culture, religious beliefs, and regulatory hurdles in some countries may also limit IVF services in these regions. Furthermore, the stress associated with undergoing multiple cycles of IVF may limit access to these services in some regions.

In Vitro Fertilization (IVF) Market Opportunities:

-

Technological innovations and fertility preservation trends create growth opportunities.

The development of new technologies such as artificial intelligence for embryo selection, robotic IVF procedures, and telemedicine for patient consultations is opening new opportunities for growth. The growing demand for fertility preservation techniques such as egg and sperm freezing and the increasing number of IVF clinics in developing countries are also providing opportunities for growth. The partnership of healthcare providers, biotech companies, and research organizations to improve IVF outcomes is also increasing market opportunities.

In Vitro Fertilization (IVF) Market Segments:

-

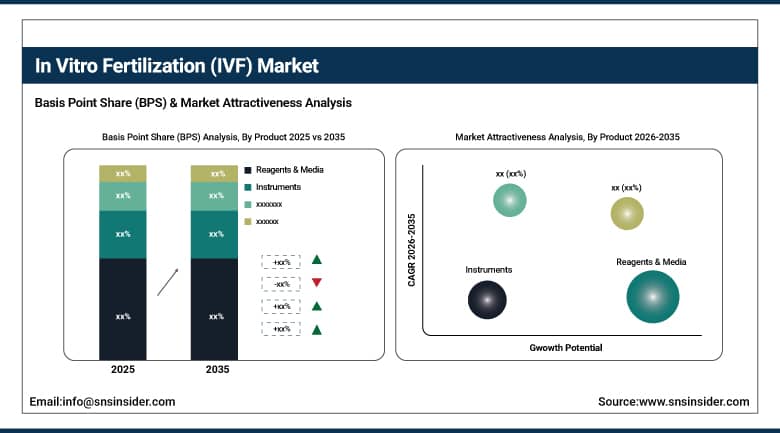

By Product: In 2025, Reagents & Media dominated with 45% share; Instruments fastest-growing segment during 2026-2035

-

By Cycle Type: In 2025, Fresh IVF Cycles dominated with 50% share; Frozen IVF Cycles fastest-growing segment during 2026-2035

-

By Application: In 2025, Female Infertility dominated with 60% share; Male Infertility fastest-growing segment during 2026-2035

-

By End User: In 2025, Fertility Clinics dominated with 55% share; Hospitals fastest-growing segment during 2026–2035.

In Vitro Fertilization (IVF) Market Segment Analysis:

By Product: Reagents & Media Dominate, Instruments Fastest-Growing

Reagents & Media lead the product segment in the IVF market, owing to their critical role in ensuring optimal embryo culture and high treatment success rates. Reagents and culture media are essential for every IVF procedure, from fertilization to embryo transfer, making them indispensable in fertility clinics and hospitals worldwide. High adoption of standardized and advanced media formulations has further reinforced their dominance.

Instruments segment is growing at a rapid pace due to technological advancements in IVF lab instruments. The acceptance of automated embryo management systems, incubators, and micromanipulators is increasing in IVF treatments, thus encouraging more investment in instruments. R&D activities and new product introductions are contributing significantly to the growth of the instruments segment

By Cycle Type: Fresh IVF Cycles Dominate, Frozen IVF Cycles Fastest-Growing

Fresh IVF Cycles dominate the market, due to their established clinical protocols, higher adoption rates, and proven success in assisted reproduction. Many fertility clinics prefer fresh cycles for first-time patients, contributing to their market leadership.

Frozen IVF Cycles is growing rapidly, and this is because there is a growing trend in fertility preservation. Moreover, the chances to preserve embryos for future use, as well as the high success rates associated with frozen embryo transfer, are the main factors that contribute to the rapid growth of this cycle.

By Application: Female Infertility Dominates, Male Infertility Fastest-Growing

Female Infertility treatments dominate the application segment, driven by higher prevalence of conditions such as polycystic ovary syndrome (PCOS), endometriosis, and age-related fertility decline. Women are more likely to seek IVF treatment due to societal awareness, medical guidance, and the success rates of modern reproductive technologies.

Male Infertility is the fastest-growing segment, supported by advancements in sperm retrieval techniques, assisted reproductive procedures like ICSI, and increasing awareness about male reproductive health. Growing focus on male factor infertility diagnostics and treatment is contributing to accelerated adoption in this segment.

By End User: Fertility Clinics Dominate, Hospitals Fastest-Growing

Fertility Clinics dominate the end-user segment due to their specialization in assisted reproductive technologies, higher patient volume, and tailored treatment plans. Clinics also provide comprehensive IVF solutions with advanced lab facilities, making them the preferred choice for patients.

Hospitals are the fastest-growing segment, as more healthcare centers integrate fertility services into their offerings. Rising collaborations between hospitals and IVF specialists, coupled with increasing patient awareness and insurance coverage for fertility treatments, are driving growth in hospital-based IVF services.

In Vitro Fertilization (IVF) Market Regional Analysis:

North America In Vitro Fertilization (IVF) Market Insights:

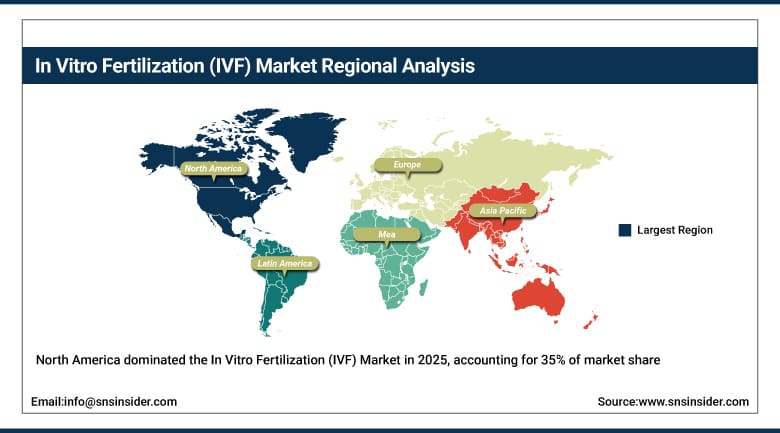

North America has a strong hold in the IVF market, covering 35% of the global market share. The strong hold of North America is due to better health infrastructure, high acceptance of ART techniques, and well-established fertility clinics in the region. Moreover, better insurance facilities and growing awareness of fertility treatments among people, along with government initiatives towards reproductive health, are some of the key factors contributing to the strong hold of North America in the IVF market. Additionally, technological advancements in IVF and patients’ willingness to spend on IVF treatments are some of the contributing factors.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe In Vitro Fertilization (IVF) Market Insights:

Europe is an important market for the global IVF market due to the presence of established fertility clinics and high awareness of assisted reproductive technologies. The government is also supporting the IVF market in Europe by providing insurance cover for fertility treatments. The focus of European countries is also on research and development in the field of reproductive medicine. The demand for personalized IVF treatments is also increasing in Europe. The use of technology in IVF treatments is also increasing in Europe.

Asia-Pacific In Vitro Fertilization (IVF) Market Insights:

Asia-Pacific is the fastest-growing IVF market. Rapid growth is driven by rising infertility rates, increasing awareness of assisted reproductive technologies, and expanding healthcare infrastructure. Growing investments in fertility clinics, improving access to advanced IVF procedures, and rising disposable incomes in countries like India, China, and Japan are further fueling adoption. Supportive government initiatives and the rising trend of medical tourism also contribute to the region’s accelerated market growth.

Latin America In Vitro Fertilization (IVF) Market Insights:

Latin American IVF market is growing steadily due to increasing awareness of infertility problems and better health care infrastructure. The increasing number of fertility clinics and better IVF techniques are also contributing to the growth of the IVF market in Latin America. Government support for health care and increasing disposable income are also contributing to the growth of the IVF market in Latin America. Medical tourism is also a growing phenomenon in countries such as Brazil and Mexico.

Middle East & Africa (MEA) In Vitro Fertilization (IVF) Market Insights:

The MEA IVF market is witnessing steady growth, and this can be attributed to the rising awareness about infertility treatments, healthcare infrastructure, and increasing investment in fertility clinics. The advancements in assisted reproductive technologies and the increasing adoption of IVF procedures in urban areas are contributing to the growth of the market. The positive government initiatives, rise in medical tourism, and increasing focus on reproductive health are contributing to the steady growth of the market in the major countries in the MEA region.

In Vitro Fertilization (IVF) Market Competitive Landscape:

Vitrolife AB was founded in 1994 and is a global life sciences company headquartered in Gothenburg, Sweden. Vitrolife specializes in assisted reproductive technologies (ART) and provides a range of products and solutions, including culture media, instruments, and consumables for in vitro fertilization (IVF) procedures. The company supports fertility clinics worldwide by enhancing embryo culture, handling, and transfer processes. Vitrolife AB has operations in over 30 countries and employs thousands of professionals globally.

-

In 2025, Vitrolife AB advanced IVF procedures by launching innovative embryo culture media and automated laboratory instruments, improving treatment success rates and workflow efficiency for fertility clinics globally.

Cook Medical was established in 1963 and is a leading global medical device company headquartered in Bloomington, Indiana, USA. Cook Medical develops and manufactures a wide range of medical devices, including products for reproductive health, minimally invasive procedures, and assisted reproductive technologies. The company’s IVF portfolio includes instruments, catheters, and consumables used in fertility treatments. Cook Medical operates in more than 135 countries with thousands of employees worldwide.

-

In 2025, Cook Medical contributed to the IVF market by introducing advanced instruments and devices for egg retrieval and embryo transfer, enhancing procedural precision and success rates for fertility clinics globally.

In Vitro Fertilization (IVF) Market Key Players:

-

Vitrolife AB

-

Cook Medical

-

Merck KGaA

-

Thermo Fisher Scientific, Inc.

-

CooperSurgical, Inc.

-

Ferring Pharmaceuticals

-

GC Biotech

-

Genea Biomedx

-

Origio (MediTech A/S)

-

Irvine Scientific (Becton Dickinson)

-

Hamilton Thorne Ltd.

-

SAGE IVF

-

Esco Micro Pte Ltd.

-

Lifecodexx GmbH

-

Vitrolife AB

-

Gynemed GmbH & Co. KG

-

Zhejiang Hisun Pharmaceuticals

-

Gynemed Laboratories

-

CooperSurgical Fertility & Genomic Solutions

-

KARL STORZ SE & Co. KG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.74 Billion |

| Market Size by 2035 | USD 44.68 Billion |

| CAGR | CAGR of 7.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product: (Reagents & Media, Instruments, Accessories) • By Cycle Type: (Fresh IVF Cycles, Frozen IVF Cycles, Donor Egg IVF Cycles) • By Application: (Female Infertility, Male Infertility, Others) • By End User: (Fertility Clinics, Hospitals, Surgical Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Vitrolife AB, Cook Medical, Merck KGaA, Thermo Fisher Scientific, Inc., CooperSurgical, Inc., Ferring Pharmaceuticals, GC Biotech, Genea Biomedx, Origio (MediTech A/S), Irvine Scientific (Becton Dickinson), Hamilton Thorne Ltd., SAGE IVF, Esco Micro Pte Ltd., Lifecodexx GmbH, Gynemed GmbH & Co. KG, Zhejiang Hisun Pharmaceuticals, Gynemed Laboratories, CooperSurgical Fertility & Genomic Solutions, KARL STORZ SE & Co. KG. |

Frequently Asked Questions

Ans: The In Vitro Fertilization (IVF) Market is expected to grow at a CAGR of 7.47% during 2026–2035.

Ans: The market was valued at USD 21.74 Billion in 2025 and is projected to reach USD 44.68 Billion by 2035.

Ans: The key drivers of the In Vitro Fertilization (IVF) Market include rising infertility, advanced reproductive technologies, increasing awareness, better healthcare access, supportive policies, and demand for personalized fertility treatments.

Ans: The Fresh IVF Cycles segment dominated during the projected period.

Ans: North America dominated the In Vitro Fertilization (IVF) Market in 2025.

Get in Touch