Retinal Vein Occlusion Treatment Disease Market Report Scope & Overview:

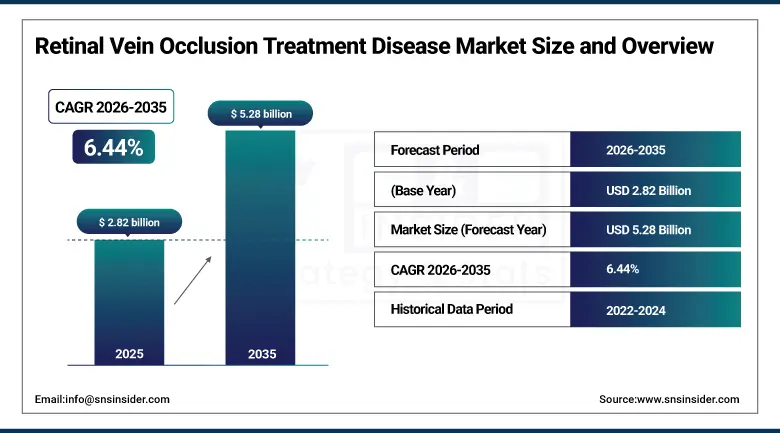

The Retinal Vein Occlusion Treatment Disease Market was valued at USD 2.82 Billion in 2025 and is expected to reach USD 5.28 Billion by 2035, growing at a CAGR of 6.44% from 2026–2035.

The global retinal vein occlusion treatment disease market is growing at a sustained pace. Retinal vein occlusion (RVO) is the second most common cause of retinal vascular disease after diabetic retinopathy, caused by blockage of the retinal vein due to thrombosis that results in elevated venous pressure, retinal oedema, hemorrhage, and vision loss. The market is driven by the rising prevalence of RVO associated with systemic risk factors including hypertension, diabetes, hyperlipidemia, and glaucoma in an aging global population, alongside the progressive adoption of intravitreal anti-VEGF therapy whose superior visual outcome evidence relative to laser and corticosteroid alternatives sustains structured clinical procurement.

In 2023, Roche and Genentech received FDA approval for faricimab (Vabysmo) for the treatment of macular oedema following retinal vein occlusion. Faricimab’s dual inhibition of VEGF-A and angiopoietin-2 creates a mechanistic advantage over conventional anti-VEGF monotherapy whose combined vascular stabilisation and anti-permeability effect creates durable macular oedema resolution that may reduce intravitreal injection frequency burden for RVO patients whose quarterly treatment schedule creates clinical management challenges.

Market Size and Forecast

-

Market Size in 2026E: USD 3.00 Billion

-

Market Size by 2035: USD 5.28 Billion

-

CAGR: 6.44% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Retinal Vein Occlusion Treatment Disease Market - Request Free Sample Report

Retinal Vein Occlusion Treatment Disease Market Trends

-

Faricimab’s dual anti-VEGF/Ang-2 mechanism is driving higher adoption due to improved durability and reduced treatment burden compared to earlier anti-VEGF therapies.

-

Extended-release corticosteroid implants such as dexamethasone (Ozurdex) are gaining traction in pseudophakic and vitrectomised RVO patients to reduce injection frequency and complications.

-

Sustained-release drug delivery systems are under development to extend dosing intervals from monthly injections toward quarterly or annual regimens.

-

Teleophthalmology and AI-assisted retinal imaging are improving RVO monitoring through remote OCT analysis and early detection of disease recurrence.

-

Combination therapy approaches integrating anti-VEGF with anti-inflammatory or neuroprotective agents are emerging in clinical research to enhance treatment outcomes beyond monotherapy.

The U.S. Retinal Vein Occlusion Treatment Disease Market Outlook

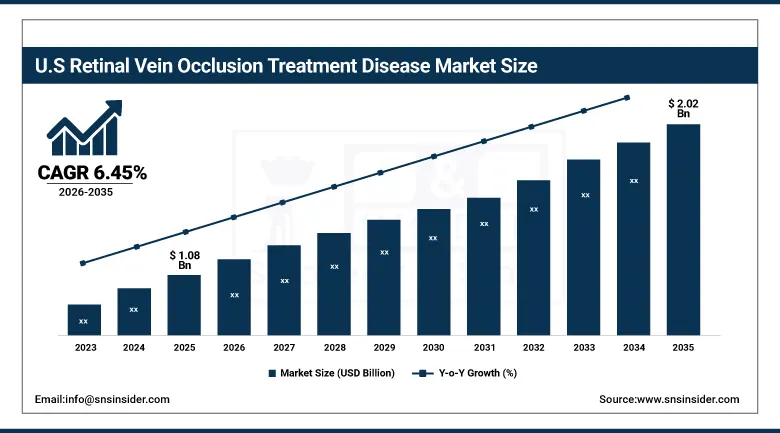

The U.S. Retinal Vein Occlusion Treatment Disease Market was valued at approximately USD 1.08 Billion in 2025 and is expected to reach approximately USD 2.02 Billion by 2035, growing at a CAGR of approximately 6.45%.

The U.S. is the most commercially sophisticated RVO treatment market within North America’s dominant revenue position. Regeneron’s Eylea (aflibercept), Genentech/Roche’s Lucentis (ranibizumab) and Vabysmo (faricimab), and Allergan/AbbVie’s Ozurdex collectively define the commercial U.S. RVO treatment landscape. The FDA’s approved treatment pathway for BRVO and CRVO macular oedema, CMS’ J-code reimbursement infrastructure for intravitreal anti-VEGF, and the large retinal specialist practice community’s established treatment infrastructure create the world’s most commercially mature RVO treatment procurement environment. The aging U.S. population’s growing RVO incidence and the increasing prevalence of hypertension and diabetes as RVO risk factors sustain consistent market growth.

Regeneron Pharmaceuticals filed a supplemental BLA for high-dose aflibercept (Eylea HD, 8 mg) for RVO-associated macular oedema in 2024, seeking to expand the approved indication for the higher-dose formulation that demonstrates extended treatment durability relative to standard 2 mg Eylea whose 4–8-week injection interval requirement creates patient burden that high-dose quarterly dosing could substantially reduce. The regulatory submission reflects Regeneron’s commercial strategy of maintaining Eylea’s market position against faricimab competition through durability improvement whose successful approval creates differentiation in the anti-VEGF RVO treatment market.

Retinal Vein Occlusion Treatment Disease Market Segment Analysis

-

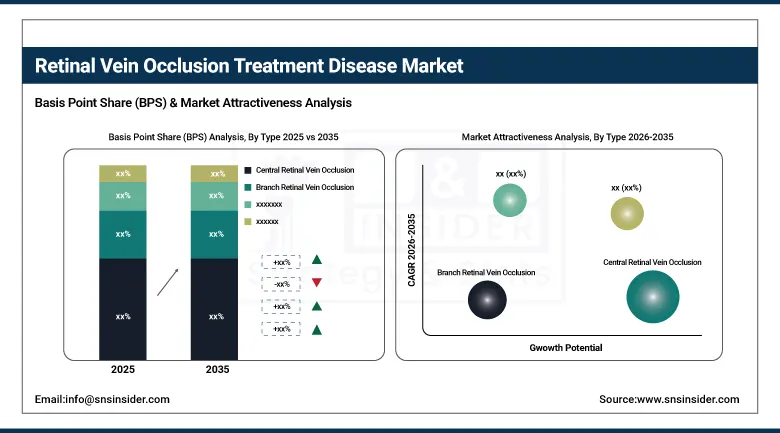

By Type, the Central Retinal Vein Occlusion (CRVO) segment dominated the market with approximately 58% share in 2025, while the Branch Retinal Vein Occlusion (BRVO) segment represents the larger epidemiological burden and is the fastest growing.

-

By Treatment, the Anti-VEGF agents segment dominated the market with approximately 65% share in 2025, while the Corticosteroid Medications segment is the fastest growing.

-

By Route of Administration, the intravitreal injection segment dominated the market with approximately 82% share in, while the oral/systemic segment maintains relevance for antiplatelet, anticoagulant, and systemic risk factor management whose adjunctive treatment role creates consistent pharmaceutical procurement alongside intravitreal injection primary treatment.

-

By End User, the hospitals & clinics segment dominated the market with approximately 52% share in 2025, while the retail pharmacy segment is the fastest growing.

By Type, CRVO dominates, BRVO grows fastest

CRVO retained the dominant type position with approximately 58% of the retinal vein occlusion treatment disease market in 2025. CRVO’s commercial primacy despite its lower epidemiological prevalence relative to BRVO reflects its more severe clinical course whose higher rate of ischemic progression, more frequent neovascular complications, and greater macular oedema severity create above-average per-patient treatment intensity and commercial value. Each CRVO patient’s treatment programme requires more frequent intravitreal injections, longer treatment duration, and more intensive ophthalmological monitoring than the average BRVO patient, creating disproportionate commercial volume relative to epidemiological incidence.

BRVO is the fastest-growing type because its higher absolute prevalence representing approximately 75% of all RVO cases creates a larger total patient population whose treatment penetration is progressively improving with ophthalmologist awareness and screening programme expansion. Each general ophthalmologist that establishes capability to diagnose and initiate BRVO treatment before retinal specialist referral creates treatment volume expansion beyond the specialist practice setting.

By Treatment, anti-VEGF dominates, corticosteroids grow fastest

Anti-VEGF agents retained the dominant treatment position with approximately 65% of the retinal vein occlusion treatment disease market in 2025. Anti-VEGF therapy’s clinical leadership in RVO treatment reflects the compelling evidence base demonstrating superior visual acuity outcomes relative to observation, laser photocoagulation, and corticosteroid alternatives in both BRVO and CRVO macular oedema randomized controlled trials. BRAVO and CRUISE trials’ ranibizumab data, VIBRANT trial’s aflibercept evidence, and SHORE and BALATON trial’s faricimab results collectively define a robust anti-VEGF efficacy dataset that sustains first-line treatment specification in clinical practice guidelines globally.

Corticosteroid medications are the fastest-growing treatment because the dexamethasone intravitreal implant’s distinct mechanism, favorable profile in pseudophakic patients and vitrectomised eyes, and reduced injection frequency relative to anti-VEGF create above-average adoption in specific patient subpopulations whose treatment characteristics create clinical motivation for corticosteroid specification.

By End User, hospitals dominate, retail pharmacy grows fastest

Hospitals and clinics retained the dominant end-user position with approximately 52% of the retinal vein occlusion treatment disease market in 2025. The intravitreal injection procedure’s clinical environment requirement creates inherent procurement concentration in specialist ophthalmological outpatient facilities whose sterile injection suite, slit-lamp examination capability, and optical coherence tomography monitoring infrastructure create the standard of care setting for RVO treatment.

Retail pharmacy is the fastest-growing end user because the oral and topical adjunctive medication market’s expansion, combined with the progressive pharmacy role in specialty medication dispensing programme, creates growing retail procurement contribution to the RVO treatment market. Each new RVO patient whose systemic risk factor management requires antiplatelet therapy, blood pressure medication, or anticoagulant management creates retail pharmacy procurement whose aggregate across the RVO patient population creates consistent commercial volume.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Retinal Vein Occlusion Treatment Disease Market Insights

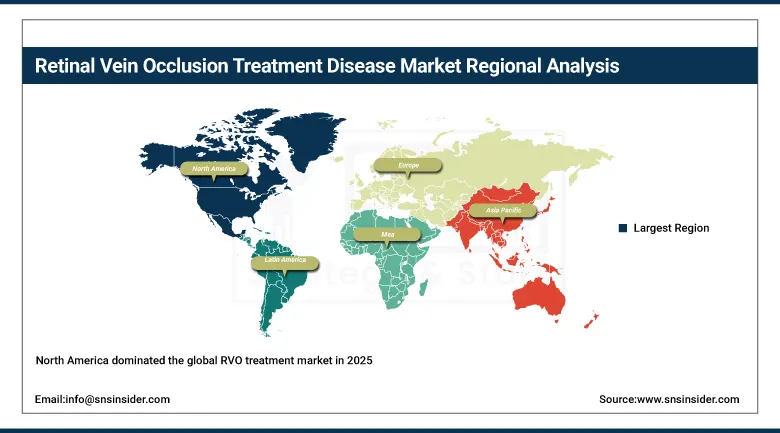

North America dominated the global RVO treatment market in 2025 as the highest per-capita healthcare expenditure region with advanced ophthalmic care infrastructure. The United States accounts for approximately 87.4% of North American revenues through Regeneron’s Eylea, Genentech’s Lucentis and Vabysmo, and AbbVie’s Ozurdex’s commercial procurement in a well-established retinal specialist practice network whose intravitreal injection infrastructure creates consistent treatment volume.

Canada contributes approximately 12.6% of North American revenues through its provincial healthcare system’s retinal specialist network, the growing anti-VEGF reimbursement infrastructure, and the aging population’s growing RVO incidence creating consistent treatment demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Retinal Vein Occlusion Treatment Disease Market Insights

Europe is a technically sophisticated RVO treatment market where EMA’s approved treatment indications, national reimbursement systems’ anti-VEGF coverage, and the ophthalmology specialty’s advanced clinical training create structured institutional procurement. Germany accounts for approximately 22.3% of European revenues through its advanced ophthalmic clinic network, Bayer’s Eylea commercial partnership, and the statutory health insurance’s anti-VEGF reimbursement.

The United Kingdom, France, and Spain are significant secondary markets where NHS and equivalent national healthcare system’s retinal treatment programme creates institutional-scale RVO treatment procurement whose NICE and HAS guideline endorsement of anti-VEGF therapy sustained consistent clinical adoption.

Asia Pacific Retinal Vein Occlusion Treatment Disease Market Insights

Asia Pacific is the fastest-growing regional RVO treatment market, driven by the rapidly aging population in China, Japan, South Korea, and India whose RVO incidence grows with age, the increasing prevalence of hypertension and diabetes as RVO risk factors, and the expanding retinal specialist care infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through its large RVO patient population, the government’s healthcare expansion, and the growing retinal specialist practice network whose anti-VEGF adoption is increasing with clinical guideline awareness.

Japan’s advanced ophthalmic care infrastructure, South Korea’s sophisticated healthcare system, and India’s rapidly expanding retinal specialist community create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Retinal Vein Occlusion Treatment Disease Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital ophthalmology network, the Ministry of Health’s anti-VEGF procurement programme, and the population’s above-average diabetes and hypertension prevalence creating RVO risk burden. Brazil leads Latin American revenues at approximately 44.2% through its retinal specialist community, the public healthcare system’s anti-VEGF access programme, and the high RVO burden associated with the country’s hypertension and diabetes prevalence.

UAE’s advanced private ophthalmology sector and South Africa’s retinal specialist community create significant MEA secondary markets whose RVO treatment procurement reflects the respective national healthcare systems’ ophthalmic care investment.

Market Dynamics

Growth Drivers: Aging population increasing RVO incidence and anti-VEGF therapy adoption creating structured treatment procurement

The aging global population is the RVO treatment market’s most structurally certain growth driver. RVO’s strong age association, whose incidence increases substantially after 60 years creating above-average RVO burden in the world’s most rapidly growing demographic segment, creates structural demand growth that compounds with each year’s demographic progression. The WHO’s projection that the global population over 65 will double from 1 billion in 2020 to 2 billion by 2050 creates a commercial demand trajectory whose RVO treatment component sustains consistent market expansion through the forecast period.

Anti-VEGF therapy’s progressive adoption as the standard of care for RVO-associated macular oedema in emerging and developing markets whose previous treatment infrastructure relied on observation and laser photocoagulation creates new commercial procurement from previously untreated patient populations.

Restraints: High anti-VEGF injection treatment burden and reimbursement limitations in emerging markets

Anti-VEGF therapy’s monthly or bi-monthly intravitreal injection requirement creates treatment burden that significantly reduces patient compliance in real-world settings relative to clinical trial outcomes. Each injection missed due to the patient’s inability to attend frequent clinic appointments creates suboptimal visual outcome whose under-treatment reduces both patient benefit and commercial treatment volume below the epidemiologically indicated rate. The practical injection burden creates a structural market limitation whose resolution requires extended-release or longer-acting anti-VEGF formulation development.

Reimbursement limitations for branded anti-VEGF agents in public healthcare systems create cost constraint that favours bevacizumab’s off-label use over approved alternatives at 20-40 times higher cost.

Opportunities: Faricimab extended-dosing and sustained-release drug delivery technology

Faricimab’s dual mechanism and extended treatment durability represent the most commercially significant near-term opportunity in the RVO anti-VEGF market. Each clinical trial result demonstrating faricimab’s ability to maintain BRVO and CRVO macular oedema control at quarterly injection intervals for a substantial proportion of patients creates treatment burden reduction whose clinical value sustains premium prescription preference over standard anti-VEGF alternatives. The commercial migration from monthly ranibizumab and aflibercept toward quarterly faricimab creates per-patient commercial value improvement whose aggregate across the growing RVO treatment population sustains market revenue growth.

Sustained-release anti-VEGF delivery technology development represents the most transformative long-term commercial opportunity whose successful clinical validation and regulatory approval would fundamentally change the RVO treatment paradigm from high-frequency injection therapy toward infrequent refill or single-treatment approaches.

Recent Developments:

-

2026: FDA expanded faricimab (Vabysmo) labeling to support treatment of macular edema due to RVO beyond 6 months, reinforcing its role in long-term chronic therapy management.

-

2025: Clinical evidence from BALATON and COMINO trials confirmed faricimab provides non-inferior visual outcomes vs aflibercept with extended dosing intervals in RVO patients.

-

2025: Next-generation anti-VEGF agents such as aflibercept 8 mg and biosimilars gained traction for reducing injection frequency while maintaining efficacy in retinal edema management.

Retinal Vein Occlusion Treatment Disease Market key players are:

-

Regeneron Pharmaceuticals Inc.

-

Roche Holding AG (Genentech)

-

Bayer AG

-

AbbVie Inc. (Allergan)

-

Novartis AG

-

Santen Pharmaceutical Co., Ltd.

-

Bausch Health Companies

-

Aerie Pharmaceuticals (Alcon)

-

Ocular Therapeutix, Inc.

-

Johnson & Johnson (Janssen)

-

Alcon Inc.

-

Apellis Pharmaceuticals

-

Kodiak Sciences Inc.

-

Outlook Therapeutics Inc.

-

Neurotech Pharmaceuticals, Inc.

-

Clearside Biomedical, Inc.

-

Thrombogenics N.V. (Oxurion)

-

Oculis Ophthalmology

-

Clearpoint Neuro

-

EyePoint Pharmaceuticals

Retinal Vein Occlusion Treatment Disease Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.82 Billion |

| Market Size by 2035 | USD 5.28 Billion |

| CAGR | CAGR of 6.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Central Retinal Vein Occlusion/CRVO, Branch Retinal Vein Occlusion/BRVO) • By Treatment (Anti-VEGF Agents, Corticosteroid Medications, Laser Photocoagulation, Surgical Treatment) • By Route of Administration (Intravitreal Injection, Oral/Systemic, Topical) • By End User (Hospitals & Clinics, Retail Pharmacy, Eye Care Centers, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Regeneron Pharmaceuticals Inc., Roche Holding AG (Genentech), Bayer AG, AbbVie Inc. (Allergan), Novartis AG, Santen Pharmaceutical Co., Ltd., Bausch Health Companies, Aerie Pharmaceuticals (Alcon), Ocular Therapeutix, Inc., Johnson & Johnson (Janssen), Alcon Inc., Apellis Pharmaceuticals, Kodiak Sciences Inc., Outlook Therapeutics Inc., Neurotech Pharmaceuticals, Inc., Clearside Biomedical, Inc., Thrombogenics N.V. (Oxurion), Oculis Ophthalmology, Clearpoint Neuro, EyePoint Pharmaceuticals |

Frequently Asked Questions

The Retinal Vein Occlusion Treatment Disease Market is expected to grow at a CAGR of 6.44% from 2026 to 2035.

The Retinal Vein Occlusion Treatment Disease Market was valued at USD 2.82 Billion in 2025.

Rising prevalence of retinal vein occlusion driven by the aging global population and growing diabetes and hypertension incidence.

Central Retinal Vein Occlusion (CRVO) dominated the market with approximately 58% share in 2025.

North America dominated the market in 2025.

Get in Touch