Industrial Gearbox Market Report Scope & Overview:

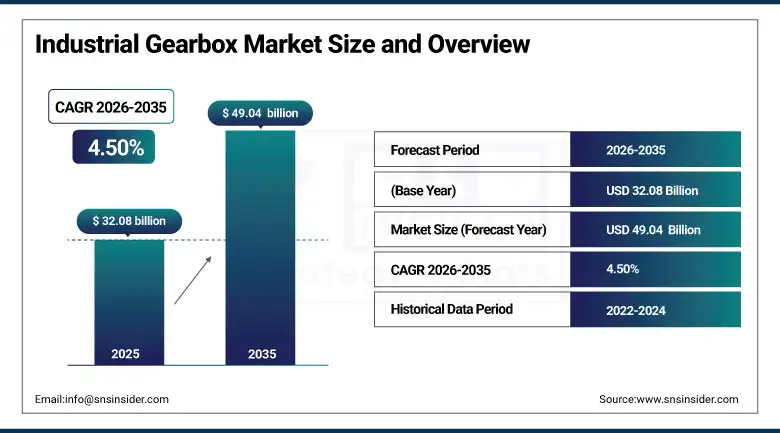

The industrial gearbox market was valued at USD 32.08 billion in 2025 and is expected to reach USD 49.04 billion by 2035, growing at a CAGR of 4.50% from 2026–2035.

Industrial gearboxes represent one of the most fundamental and pervasive mechanical power transmission components in the global industrial equipment ecosystem, serving as the mechanical interface between prime movers including electric motors, engines, and turbines and the driven machinery that performs the actual industrial work, providing the speed reduction, torque multiplication, direction change, or multi-output power split functions that the vast majority of industrial machines require to operate effectively within their designed performance envelope. The technology encompasses an extraordinary range of design architectures from the simple single-stage helical gear pair that reduces conveyor belt drive motor speed and multiplies torque by a fixed ratio, through the multi-stage compound helical and bevel-helical gearbox assemblies that achieve extreme reduction ratios for slow-turning kilns and agitators, to the sophisticated planetary epicyclic gearboxes that package very high torque density within compact housings suited to robot joint drives and wind turbine nacelles where the combination of power concentration and weight minimisation is critical.

The International Energy Agency's 2025 industrial energy efficiency report estimating that electric motor systems including gearboxes account for approximately 45% of global industrial electricity consumption, and that upgrading to premium efficiency designs could reduce this consumption by 20 to 30% at commercially justified payback periods in most industrial applications, provides the energy cost and carbon reduction business case that is driving the industrial gearbox replacement and upgrade market above and beyond the growth driven by new machinery deployment alone.

Market Size and Forecast

-

Market Size in 2026E: USD 33.52 Billion

-

Market Size by 2035: USD 49.04 Billion

-

CAGR: 4.50% from 2026 to 2035

-

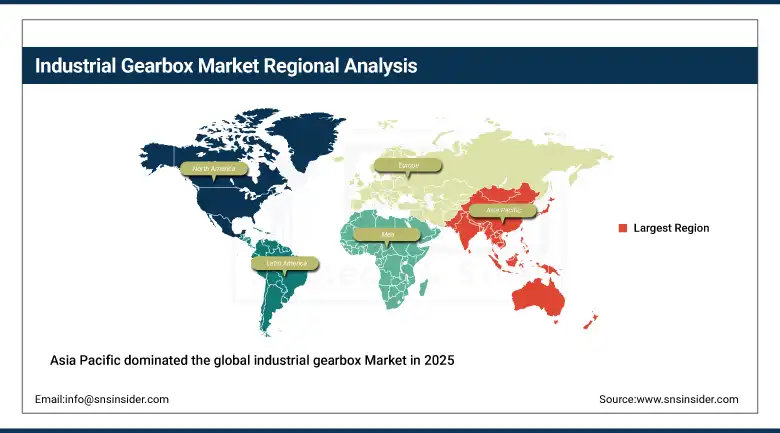

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Industrial Gearbox Market - Request Free Sample Report

Industrial Gearbox Market Trends

-

Accelerating adoption of IoT-enabled smart gearboxes incorporating embedded vibration sensors, temperature monitoring, oil condition sensing, and wireless data transmission capabilities that feed predictive maintenance analytics platforms, enabling condition-based maintenance scheduling that reduces unplanned downtime, extends gearbox service life, and lowers total lifetime maintenance cost compared with fixed-interval preventive maintenance schedules.

-

Growing demand for compact, high-torque-density planetary gearbox configurations in robotics, automated guided vehicle drives, precision machine tool spindle drives, and wind turbine generator drives where the planetary architecture's concentric load path, distributed load sharing across multiple planet gears, and high torque-to-weight ratio provide performance advantages unavailable from parallel shaft helical and bevel alternatives.

-

Increasing adoption of premium and super-premium efficiency IE3 and IE4 gearmotor combinations that reduce the power losses from gear mesh friction, bearing drag, and seal losses that characterise standard efficiency gearboxes, qualifying for regulatory compliance with EU Ecodesign regulation energy efficiency mandates and generating measurable electricity cost reduction benefits that justify the purchase price premium in energy-intensive continuous duty applications.

-

Rising demand for wind turbine gearboxes capable of the extreme reliability requirements of multi-megawatt offshore wind turbine drivetrains, where gearbox failures requiring crane-assisted turbine nacelle access represent some of the most costly maintenance events in renewable energy generation, driving investment in direct-drive and medium-speed hybrid drivetrain concepts alongside improved conventional gearbox lubrication systems, surface coatings, and bearing designs that reduce failure probability.

-

Expanding gearbox application in electric vehicle drivetrain components where the transition from conventional ICE transmissions to single-speed reduction gearboxes for electric motor output adaptation, and the development of multi-speed EV transmissions for improved efficiency across the vehicle speed range, creates a new automotive gearbox market segment with different design requirements from industrial power transmission applications.

The U.S. Industrial Gearbox Market Outlook

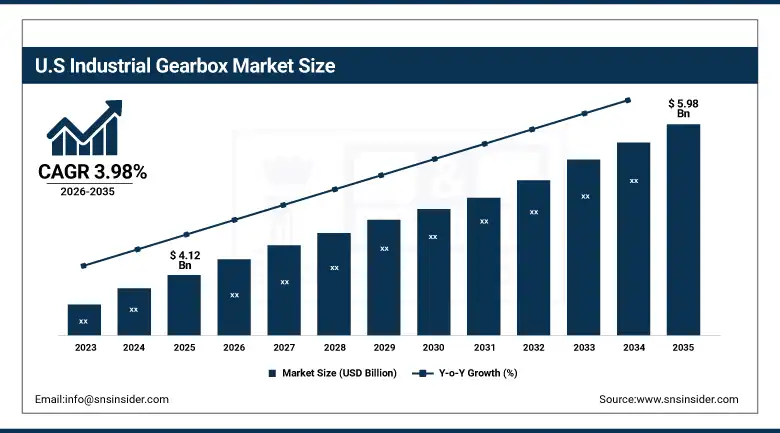

The U.S. industrial gearbox market was valued at approximately USD 4.12 billion in 2025 and is expected to reach approximately USD 5.98 billion by 2035, growing at a CAGR of 3.98%, driven by manufacturing automation investment, material handling infrastructure expansion, energy sector modernisation including wind energy development, and the adoption of high-efficiency gearmotor combinations qualifying for utility rebate programmes and regulatory energy efficiency compliance requirements.

The United States industrial gearbox market benefits from the sustained strength of American manufacturing activity across chemicals, food processing, automotive components, pharmaceutical production, and consumer goods sectors that collectively represent large populations of gearbox-equipped machinery at various stages of service life requiring maintenance parts, remanufactured assemblies, or complete replacement with upgraded technology. The reshoring and nearshoring trends accelerating U.S. manufacturing investment since the COVID-19 supply chain disruption experience are creating new factory construction and equipment investment activity that includes gearbox installations across production line drive systems, material handling conveyors, and automated guided vehicle fleets.

The U.S. Department of Energy's Advanced Manufacturing Office investment in next-generation power transmission component efficiency improvement, combined with state utility commission energy efficiency programme rebates covering premium efficiency gearmotor upgrades in industrial facilities, creates policy-supported investment incentives for the industrial gearbox upgrade market that sustain commercial activity above the baseline driven by machinery age and wear-induced replacement demand.

Industrial Gearbox Market Segment Analysis

-

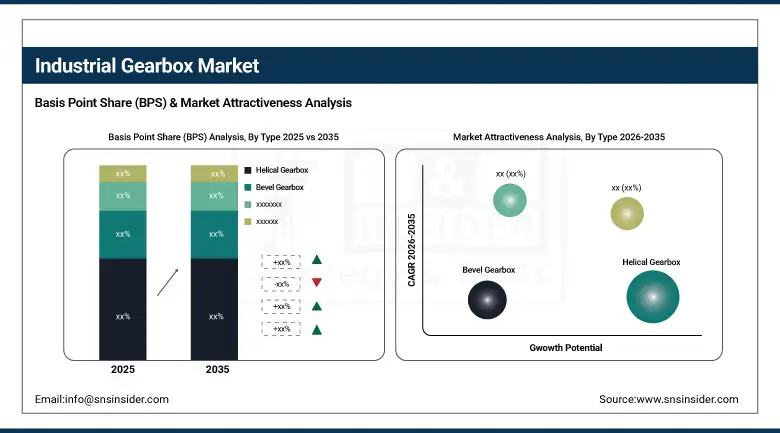

By Type, helical gearbox held the largest market share of 38.42% in 2025 through its suitability for manufacturing lines, conveyors, and heavy machinery requiring smooth torque transmission and low noise with 12,400 units deployed in 2025. Planetary Gearbox is the fastest-growing at a CAGR of 7.56% driven by robotics, precision machinery, and compact automation systems where high torque density, lightweight design, and performance reliability are essential.

-

By Power Rating, the 50 to 500 kW segment dominated with approximately 33.27% in 2025 through suitability for mid-scale industrial, automotive, and production environments. Above 500 kW is the fastest-growing at a CAGR of 6.89% fuelled by large-scale wind farms, mining equipment, and power plant applications demanding robust high-capacity gear systems for extreme load conditions.

-

By Application, material handling accounted for the highest market share of 29.64% in 2025 through gearbox's essential role in conveyor drives, crane hoists, and automated warehouse equipment. Power generation is the fastest-growing application at a CAGR of 8.12% driven by wind energy deployment creating sustained demand for multi-megawatt turbine gearboxes alongside conventional power plant generator drive applications.

-

By End User, manufacturing sector held the largest share of 41.73% in 2025 through the sector's enormous installed base of gearbox-equipped production machinery and continuous new machinery investment in automation and capacity expansion. Energy & utilities are the fastest-growing end user at a CAGR of 7.94% driven by wind turbine drivetrain demand and conventional power generation machinery modernisation.

By Type, helical gearbox dominates, planetary is expected to grow fastest

Helical gearboxes retained the dominant type position with approximately 38.42% of the Industrial Gearbox Market in 2025, reflecting the design's well-established commercial penetration across the broadest range of industrial applications including conveyor drives, pump drives, agitator drives, compressor drives, and general industrial machinery that collectively represent the largest volume of gearbox-equipped applications globally. The helical gear tooth's inclined tooth geometry creates a gradual engagement that distributes load across multiple teeth simultaneously, producing smoother and quieter operation than spur gears at equivalent speed and torque capacity, making helical designs the standard choice for the moderate-speed, moderate-to-high torque applications that constitute the majority of industrial drive requirements.

Planetary Gearboxes are the fastest-growing type at a CAGR of 7.56% through 2035, driven by the extraordinary torque density advantage of epicyclic gear arrangements where load sharing across three or more planet gears in parallel contact with the central sun and outer ring gears enables torque transmission per unit of housing volume and weight that far exceeds what equivalent parallel shaft helical gearboxes can achieve.

By Application, material handling dominates, power generation is expected to grow fastest

Material handling retained the dominant application position with approximately 29.64% of Industrial Gearbox Market revenues in 2025, reflecting the universal dependence of industrial and commercial facilities on conveyor systems, overhead cranes, automated storage and retrieval systems, port container handling equipment, and warehouse sortation systems whose drives collectively represent the largest single installed base of industrial gearbox applications globally. The e-commerce fulfilment industry's extraordinary capital investment in automated warehousing infrastructure is creating a sustained new demand wave for material handling gearboxes in sortation conveyor drives, autonomous mobile robot wheel drives, and goods-to-person system lifter drives that is supplementing the replacement demand from the ageing installed base of conventional distribution centre conveyor systems.

Power generation is the fastest-growing application at a CAGR of 8.12% through 2035, driven primarily by the global wind energy capacity expansion that is deploying hundreds of gigawatts of new wind turbine capacity annually and creating sustained demand for the multi-megawatt turbine gearboxes that transmit low-speed rotor hub torque to high-speed generator input shafts in conventional geared wind turbine drivetrains. Each multi-megawatt wind turbine requires a gearbox with a planetary first stage and helical subsequent stages achieving gear ratios of 60 to 100 from rotor to generator speed while transmitting torques measured in millions of Newton-metres under highly variable and cyclical load conditions that present the most demanding reliability requirements in the industrial gearbox application spectrum.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.6% |

|

Europe |

Germany |

31.4% |

|

Asia Pacific |

China |

56.7% |

|

Middle East & Africa |

Saudi Arabia |

27.3% |

|

Latin America |

Brazil |

42.8% |

North America Industrial Gearbox Market Insights

North America is a large and technically advanced industrial gearbox market with the United States accounting for approximately 83.6% of North American revenues as the world's largest economy with a significant manufacturing and energy sector base requiring gearbox-equipped machinery across diverse industrial applications. The U.S. market's characteristics reflect the combination of strong industrial automation investment creating demand for precision servo gearboxes in robot and machine tool applications, sustained material handling infrastructure investment in logistics and distribution automation, wind energy development generating turbine gearbox demand, and the mining and oil and gas sector's heavy-duty gearbox requirements. The reshoring of manufacturing to the United States driven by supply chain resilience concerns and IRA manufacturing incentives is generating new factory construction activity that includes gearbox installations in production line equipment across semiconductors, electric vehicles, and industrial equipment manufacturing.

Europe Industrial Gearbox Market Insights

Europe is a technically sophisticated industrial gearbox market characterised by the presence of world-leading gearbox manufacturers including Siemens FLENDER, SEW-Eurodrive, Renk AG, Bonfiglioli, and Hansen Drives whose product and technology innovation sets the global benchmark for high-performance industrial power transmission. Germany accounts for approximately 31.4% of European industrial gearbox revenues as the EU's largest industrial economy and the home market of the most globally recognised industrial gearbox brands whose export manufacturing at German facilities serves global industrial customers across mining, cement, power generation, and specialised mechanical engineering applications. The EU Ecodesign regulation's increasing energy efficiency requirements for gear units, complementing the existing motor efficiency tiers, are creating a regulatory-driven upgrade market for premium efficiency gearboxes that replaces older standard efficiency designs in industrial facilities seeking compliance and operational cost reduction simultaneously.

Asia Pacific Industrial Gearbox Market Insights

Asia Pacific dominated the global industrial gearbox Market in 2025 with the largest regional revenue share, anchored by China's position as the world's largest manufacturing economy with an enormous installed base and ongoing expansion of gearbox-equipped industrial machinery across steel, cement, mining, chemicals, food processing, and automotive manufacturing sectors, combined with the fastest-growing wind energy development programme requiring large volumes of turbine gearboxes. China accounts for approximately 56.7% of Asia Pacific industrial gearbox revenues through its combination of the world's largest industrial equipment manufacturing output, substantial wind turbine drivetrain production for both domestic and export markets, and a growing domestic premium efficiency gearbox manufacturing capability from companies including NIDEC Shimpo and domestic specialists competing with European and Japanese imports in the mid-tier performance segment.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Industrial Gearbox Market Insights

Middle East and Africa and Latin America are growing industrial gearbox markets where the combination of mining sector expansion, cement production growth serving construction demand, oil and gas processing equipment investment, and emerging renewable energy infrastructure development are creating sustained gearbox demand across both new equipment installation and replacement of ageing installed machinery. Saudi Arabia leads MEA industrial gearbox revenues at approximately 27.3% of regional revenues through its combination of massive petrochemical refinery and processing infrastructure, cement production for Vision 2030 construction programmes, and growing renewable energy investment in large-scale solar and wind projects whose balance of plant includes gearbox-equipped tracking systems and ancillary mechanical equipment.

Market Dynamics

Growth Drivers: Industrial automation expansion creating sustained gearbox demand combined with wind energy drivetrain investment and energy efficiency upgrade programmes driven by rising electricity costs and regulatory mandates

The primary structural growth drivers for the industrial gearbox market are the global industrial automation expansion that is progressively replacing manual production operations with motor-driven machinery incorporating gearboxes as their power transmission interface across every manufacturing and processing sector from automotive assembly through food production and pharmaceutical manufacturing, creating sustained new gearbox installation demand that is supplemented by the replacement cycle from the large ageing installed base of industrial gearboxes approaching end of service life across mature economy industrial facilities. The renewable energy transition's wind turbine deployment is creating the most technically demanding and commercially significant new gearbox application category of the current decade, where each new wind turbine installation requires a custom-engineered precision gearbox capable of operating reliably for 20 to 25 years under highly variable loading conditions at locations with limited maintenance access, sustaining premium price points and continuous technical innovation investment in wind turbine gearbox design and manufacturing.

Restraints: High manufacturing cost and long lead times for custom high-power gearboxes, market pressure from direct-drive machinery eliminating gearbox requirements in some applications

A significant restraint on the industrial gearbox market is the competitive pressure from direct-drive machinery configurations that eliminate the gearbox entirely by using low-speed, high-torque motors directly coupled to the driven machine, most prominently in the wind energy sector where permanent magnet direct-drive turbine designs from Siemens Gamesa and GE compete with conventional geared drivetrains by eliminating the gearbox reliability and maintenance concerns that represent one of wind turbine's most significant lifecycle cost drivers. The high manufacturing cost and extended lead times for large custom gearboxes in mining, cement, and heavy industrial applications, where units require bespoke engineering for specific speed ratio and torque requirements, custom housing fabrication, and extended gear grinding and quality inspection cycles, can extend delivery timelines to six to eighteen months for the largest units that create equipment procurement planning challenges for industrial facility construction and expansion projects.

Opportunities: Smart gearbox technology and predictive maintenance enabling condition-based service models, high-efficiency design replacement programme driven by energy cost and regulatory pressure

The integration of embedded sensor technology, wireless data transmission, and cloud-based predictive analytics into industrial gearboxes creates a commercial opportunity for gearbox manufacturers to transform from equipment suppliers into condition monitoring service providers whose recurring subscription revenue from predictive maintenance programmes supplements the one-time capital equipment sale with an ongoing service relationship that improves customer retention, increases gearbox system lifetime value, and differentiates technically sophisticated manufacturers from commodity competitors unable to offer the digital service layer. The energy efficiency upgrade market for industrial gearboxes is being accelerated by both rising industrial electricity tariffs that increase the annual operating cost savings available from premium efficiency gearbox replacement and by expanding regulatory requirements for industrial energy efficiency that create compliance deadlines motivating facility managers to schedule systematic gearbox upgrade programmes within defined timelines.

Recent Developments:

-

2025: Siemens FLENDER launched its connected service platform for industrial gearboxes, offering remote condition monitoring through embedded IoT sensors providing vibration spectrum analysis, temperature trending, and oil condition assessment that predict maintenance requirements weeks before failure onset in critical industrial drive applications.

-

2025: SEW-Eurodrive expanded its DriveRadar IoT monitoring service to additional industrial gearbox product lines, adding artificial intelligence-powered anomaly detection algorithms that identify subtle performance deviations in gearbox vibration and thermal signatures that precede mechanical failure events in high-duty-cycle material handling and manufacturing drive applications.

-

2025: Bonfiglioli acquired a specialty planetary gearbox manufacturer to strengthen its portfolio for robotics and collaborative robot joint drive applications, expanding its market position in the precision servo gearbox segment that is growing at the highest rate within the broader industrial gearbox market driven by factory automation investment.

Industrial Gearbox Market Key Players are:

-

Siemens AG

-

SEW-Eurodrive GmbH & Co. KG

-

ABB Ltd. (Dodge)

-

Bonfiglioli Riduttori S.p.A.

-

Renk AG

-

Lenze SE

-

Nord Drivesystems

-

Sumitomo Heavy Industries Ltd.

-

Rexnord Corporation

-

Elecon Engineering Company Ltd.

-

Brevini Power Transmission (Dana Inc.)

-

Zollern GmbH & Co. KG

-

Stober Antriebstechnik GmbH & Co. KG

-

Flender GmbH

-

Radicon Transmission (David Brown Santasalo)

-

Nanjing High Speed Gear Manufacturing Co., Ltd.

-

Bosch Rexroth AG

-

Wikov Industry a.s.

-

Cone Drive Operations Inc.

-

Horsburgh & Scott Company

Industrial Gearbox Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 32.08 Billion |

| Market Size by 2035 | USD 49.04 Billion |

| CAGR | CAGR of 4.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Helical Gearbox, Bevel Gearbox, Worm Gearbox, Planetary Gearbox, Others) •By Power Rating (Below 50 kW, 50–500 kW, Above 500 kW) •By Application (Material Handling, Power Generation, Cement & Mining, Food & Beverages, Automotive, Others) •By End User (Manufacturing Sector, Energy & Utilities, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens AG , SEW-Eurodrive GmbH & Co. KG, ABB Ltd. (Dodge), Bonfiglioli Riduttori S.p.A., Renk AG, Lenze SE, Nord Drivesystems, Sumitomo Heavy Industries Ltd., Rexnord Corporation, Elecon Engineering Company Ltd., Brevini Power Transmission (Dana Inc.), Zollern GmbH & Co. KG, Stober Antriebstechnik GmbH & Co. KG, Flender GmbH, Radicon Transmission (David Brown Santasalo), Nanjing High Speed Gear Manufacturing Co., Ltd., Bosch Rexroth AG, Wikov Industry a.s., Cone Drive Operations Inc., and Horsburgh & Scott Company |

Frequently Asked Questions

Asia Pacific dominated the Industrial Gearbox Market in 2025, driven by China's manufacturing scale and wind energy deployment.

Helical Gearbox dominated with approximately 38.42% of revenues in 2025.

Industrial automation growth, wind energy investments, and energy-efficiency upgrades are driving sustained demand for industrial gearboxes.

The Industrial Gearbox Market was valued at USD 32.08 billion in 2025.

The Industrial Gearbox Market is expected to grow at a CAGR of 4.50% from 2026 to 2035.

Get in Touch