Ball Bearing Market Report Scope & Overview:

Get More Information on Ball Bearing Market - Request Sample Report

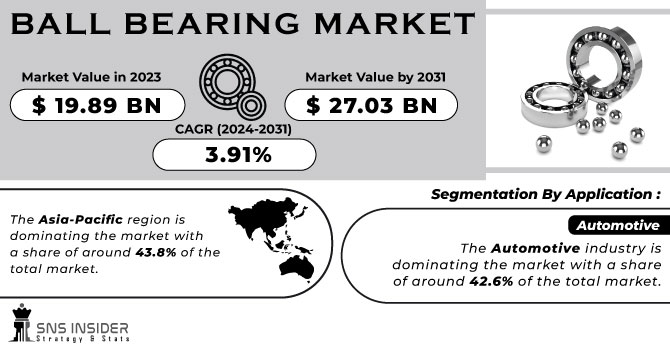

The Ball Bearing Market Size was estimated at USD 10.66 billion in 2023 and is expected to arrive at USD 19.01 billion by 2032 with a growing CAGR of 6.64% over the forecast period 2024-2032. This report offers a unique analysis of the Ball Bearing Market by examining key aspects such as technological adoption and innovations across different regions, supply chain dynamics, and sourcing trends. It also delves into demand and consumption patterns, alongside export/import data, providing a comprehensive view of global trade movements. Maintenance and downtime metrics are explored to highlight operational efficiency trends. Additional insights include the growing integration of smart technologies and advanced materials in manufacturing processes, contributing to higher precision and durability in ball bearing products.

In the U.S. ball bearing market, the sector is expected to experience consistent growth from 2023 to 2032. Starting at a market value of USD 1.78 billion in 2023, the market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.01%, reaching USD 3.28 billion by 2032. This growth reflects increasing demand across various industries, including automotive, aerospace, and industrial applications, which rely heavily on ball bearings for their operational efficiency.

Market Dynamics

Drivers

-

The growing demand for automation and industrial machinery drives the need for high-performance ball bearings to ensure smooth, efficient operation across sectors like manufacturing, robotics, and aerospace.

The growing demand for automation and industrial machinery is a key driver of the ball bearing market. With industries from manufacturing to robotics and aerospace moving toward increasingly automated systems, there is an ever-growing demand for high-performance components such as ball bearings. By minimizing friction, ball bearings allow for smoother machinery operation and increased efficiency, accuracy, and lifespan. Ball bearings are essential for automation in manufacturing processes, computerized numerical control (CNC) machines, and assembly lines requiring high-speed performance and accurate motion control. In the same way, ball bearings allow robots to function with increased precision and stability. For aerospace, state-of-the-art ball bearings keep engines, landing gear, and other critical systems running smoothly. As Industry 4.0 and smart factories gain traction, this trend is anticipated to continue and may even trigger additional demand for high value bearings. With automation rapidly changing ground, ball bearing market is gaining foreseen growth but more focus on premium high-performance, product segment.

Restraint

-

High manufacturing costs of advanced ball bearings, especially ceramic ones, limit their adoption in cost-sensitive industries due to expensive production processes.

High manufacturing costs in the ball bearing market, particularly for advanced products made from specialized materials like ceramics, pose a significant challenge. Ceramic ball bearings have better performance than regular steel bearings in terms of heat resistance, longevity, and friction. On the other hand, the manufacturing process of ceramic bearings involves advanced technologies, thus showing a high overall manufacturing cost. These high costs may be a deterrent to industries that have limited funds or work within cost-sensitive sectors, for example, automotive or industrial machinery. Consequently, companies might hesitate to spend money on these high-end bearings, since less expensive options are available. However, these developments are realised at the expense of time and cost across their industry, and since many one-time tools are still in this medal display viewpoint, the capture of high-speed and efficient bearings becomes unexpected.

Opportunities

-

Innovation in lightweight, high-performance ball bearings using materials like ceramics offers improved efficiency, reduced friction, and longer lifespan, creating growth opportunities in various industries.

Innovation in lightweight and high-performance ball bearings is driven by the need for more efficient and durable components in industries such as automotive, aerospace, and manufacturing. As a result, the need for better-performing bearings that can also operate at higher speeds as well as in more demanding conditions is becoming increasingly important. Innovation will come in the form of advanced materials like ceramics, which have better strength-to-weight ratios and less friction than traditional metals, Will steed said. Ceramic ball bearings are also lighter and more resistant to wear and corrosion, and heat, so they last longer with less maintenance. By utilizing this technology, companies can offer better performing, more cost-effective solutions for demanding applications, making them stand out in a crowded market. This will present huge opportunities for manufacturers to leverage on this as industries move on to more energy efficient and performance-based manufacturing.

Challenges

-

Environmental concerns drive the need for sustainable practices in ball bearing production, requiring costly investments in greener technologies and processes.

Environmental concerns and sustainability have become significant factors influencing industries worldwide, including the ball bearing market. Governments are imposing stricter rules to reduce emissions, and consumers are increasingly seeking out sustainable options. Manufacturers of bearings must, therefore, pay attention to their production processes' environmental footprint, from energy use to waste to material sourcing. Embracing sustainable practices like using renewable energy, cutting emissions, and picking recyclable and biodegradable materials can come at a cost. For sustainability goals, companies may need to invest in new technologies, research, and production processes. Although such efforts are ultimately essential for overall compliance and consumer interest, they can also incur increased ongoing costs. Hence, manufacturers will have to weigh their responsibility on the environment while maintaining profitability, which will have a reflective effect on the complete cost structure of the ball bearing market.

Segmentation Analysis

By Type

The Deep Groove Ball Bearings segment dominated with a market share of over 42% in 2023, owing to their extraordinary versatility and ability to bear both radial and axial loads. The ability to lift loads in opposite directions simultaneously allows them to be used in a wide variety of industries and applications. These are highly used in sectors like automotive, machinery, electric motors, and industrial equipment, where performance and cost considerations are key. Their minimal design, low friction potential, even at high speeds, adds to their popularity. In addition, they are also compatible with different environmental conditions like variations in temperature and load, which further drives their need in many industrial applications. The efficient and widespread use is one of the main reasons that makes deep groove ball bearings dominate the market.

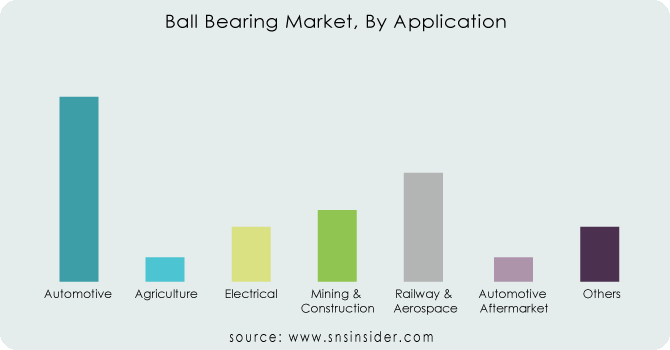

By Application

The Automotive segment dominated with a market share of over 32% in 2023, owing to the burgeoning global automotive production demand. Key regions are contributing extensively to this growth, including Asia-Pacific with their developing automotive industries. The automotive industry's demands for high precision and durability in various applications make ball bearings essential components in engines, transmissions, wheel hubs, and other critical areas. As automotive technology advances, especially with the proliferation of electric vehicles (EVs), the demand for sophisticated ball bearings also increases. Electric vehicles require bearings that meet the challenges of electric drivetrains in terms of their efficiency, durability, and functionality to perform for increasingly longer miles, which helps drive further market growth. The segment's growth is mainly driven by this shift towards electric mobility.

Need Customized Research on Ball Bearing Market - Enquiry Now

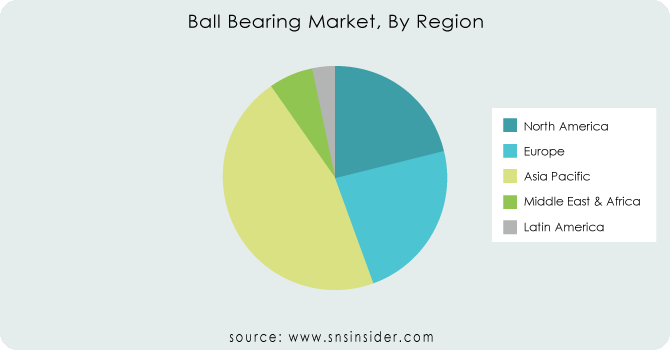

Key Regional Analysis

The Asia-Pacific region dominated with a market share of over 42% in 2023 owing to high manufacturing capabilities and flourishing automotive and industrial sectors in the region. Countries such as China, Japan, and India are significant hubs for this region’s dominance, big size production and substantial demand for ball bearings across the automotive, industrial machinery, and other sectors. Such dominance is exacerbated by the rapid industrialisation and infrastructure in the region. The automotive industry generates some of the highest demand, where ball bearings are critical components of engines, transmissions, and wheel hubs. In Asia-Pacific, the leading position is mostly attributed to multiple leading bearing manufacturers and growing technology investments.

North America region dominated with a market share of over 22% in 2023, fueled by technological advancements and rising demand across key sectors such as automotive, aerospace, and medical. Electric vehicles (EVs) are a key driver of this growth, and EVs require high-performance ball bearings to achieve particular levels of efficiency and durability. Moreover, India's continuous industrial modernization also complements the growth stimuli from the U.S. and Canada of the machine and automation systems, resulting in high demand for advanced ball bearings. The latter is paralleled by advances in specific aerospace and medical applications where precision and reliability are key. This will help drive growth of the North America market; as ball bearings continue to be embraced as a solution across a range of industries.

Some of the major key players in the Ball Bearing Market

-

Brammer PLC (Bearings, Seals, Lubricants)

-

Harbin Bearing Manufacturing Co., Ltd. (Ball Bearings, Roller Bearings)

-

HKT Bearings Ltd. (Ball Bearings, Industrial Bearings)

-

JTEKT Corporation (Ball Bearings, Roller Bearings, Automotive Bearings)

-

NBI Bearings Europe (Ball Bearings, Spherical Bearings, Custom Bearings)

-

NSK Global (Ball Bearings, Linear Motion Bearings, Precision Bearings)

-

NTN Corporation (Ball Bearings, Tapered Roller Bearings, Cylindrical Roller Bearings)

-

RBC Bearings Inc. (Ball Bearings, Needle Bearings, Thrust Bearings)

-

Rexnord Corporation (Ball Bearings, Mounted Bearings, Couplings)

-

RHP Bearings (Ball Bearings, Roller Bearings, Mounted Bearings)

-

SKF Group (Ball Bearings, Roller Bearings, Bearing Units)

-

FAG Bearings (Ball Bearings, Cylindrical Roller Bearings, Spherical Roller Bearings)

-

Timken Company (Ball Bearings, Tapered Roller Bearings, Industrial Bearings)

-

INA Bearings (Schaeffler Group) (Ball Bearings, Needle Bearings, Linear Motion Bearings)

-

MRC Bearings (A part of SKF) (Ball Bearings, Angular Contact Bearings)

-

MinebeaMitsumi Inc. (Ball Bearings, High Precision Bearings, Miniature Bearings)

-

Nachi-Fujikoshi Corp. (Ball Bearings, Industrial Bearings, Automotive Bearings)

-

Koyo Bearings (JTEKT Corporation) (Ball Bearings, Needle Bearings, Tapered Roller Bearings)

-

ZKL Bearings (Ball Bearings, Spherical Roller Bearings, Tapered Roller Bearings)

-

NTN-SNR Roulements (Ball Bearings, Automotive Bearings, Industrial Bearings)

Suppliers for (premium tapered roller bearings and ball bearings, particularly used in heavy-duty applications, including aerospace, automotive, and industrial sectors) on Ball Bearing Market

-

SKF

-

Schaeffler Group

-

NSK Ltd.

-

NTN Corporation

-

Timken Company

-

JTEKT Corporation

-

SKF Group

-

Bearings Limited

-

Nachi-Fujikoshi Corp.

-

ZVL SLOVAKIA

Harbin Bearing Manufacturing Co., Ltd-Company Financial Analysis

Recent Development

-

In September 2023, Schaeffler AG diversified its product portfolio by introducing new offerings in rotary table bearings, torque motors, and linear motors. This expansion includes the introduction of various sizes for rotary table and rotary axis bearings, complemented by the incorporation of bearing-integrated angular measuring systems. The standardization of torque motors within the RKIB series, now available up to size 690, further strengthens the company's capability to offer a comprehensive range of top-tier solutions.

-

In November 2023, The Timken Company acquired Engineered Solutions Group. This acquisition is instrumental in enhancing the company’s standing as a provider of comprehensive solutions within the industrial motion and engineered bearings sector.

-

In December 2023, ENERMAX detected higher-than-expected RMA levels in the REVOLUTION D.F. 2 and REVOLUTION D.F. X product lines. With the new models, the fan bearing issue has been addressed by installing double ball bearings of industrial grade.

| Report Attributes | Details |

| Market Size in 2023 | USD 10.66 Billion |

| Market Size by 2032 | USD 19.01 Billion |

| CAGR | CAGR of 6.64% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Self-Aligning Ball Bearings, Deep Groove Ball Bearings, Angular Contact Ball Bearings, Others) • By Application (Automotive, Industrial Machinery, Mining & Construction, Medical, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Brammer PLC, Harbin Bearing Manufacturing Co., Ltd., HKT Bearings Ltd., JTEKT Corporation, NBI Bearings Europe, NSK Global, NTN Corporation, RBC Bearings Inc., Rexnord Corporation, RHP Bearings, SKF Group, FAG Bearings, Timken Company, INA Bearings (Schaeffler Group), MRC Bearings (A part of SKF), MinebeaMitsumi Inc., Nachi-Fujikoshi Corp., Koyo Bearings (JTEKT Corporation), ZKL Bearings, NTN-SNR Roulements. |

Frequently Asked Questions

Ans: The Ball Bearing Market is expected to grow at a CAGR of 6.64% from 2024-2032.

Ans: The Ball Bearing Market was USD 10.66 billion in 2023 and is expected to reach USD 19.01 billion by 2032.

Ans: The growing demand for automation and industrial machinery drives the need for high-performance ball bearings to ensure smooth, efficient operation across sectors like manufacturing, robotics, and aerospace.

Ans: The “Deep Groove Ball Bearings” segment dominated the Ball Bearing Market.

Ans: Asia-Pacific dominated the Ball Bearing Market in 2023

Get in Touch