IoT Analytics Market Report Scope & Overview:

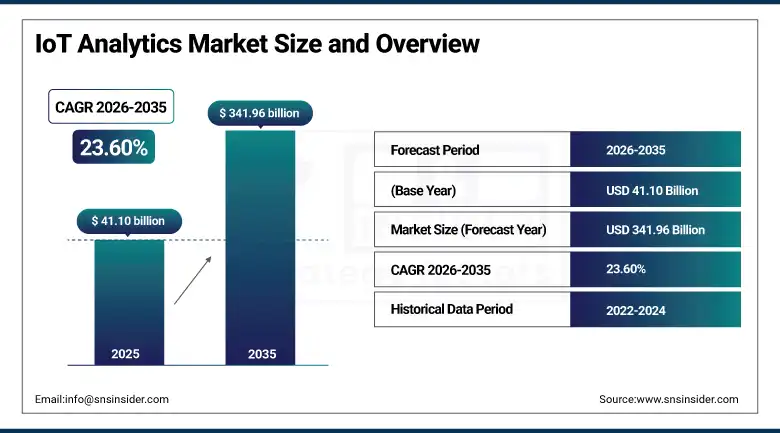

The IoT Analytics Market was valued at USD 41.10 Billion in 2025 and is expected to reach USD 341.96 Billion by 2035, growing at a CAGR of 23.60% from 2026 to 2035.

IoT analytics is the discipline of collecting, processing, and analyzing the continuous streams of structured and unstructured data generated by the billions of sensors, actuators, machines, and connected devices that constitute the Internet of Things ecosystem, and translating that data into actionable operational intelligence. The IoT analytics market's rapid growth reflects the progressive maturation of the full IoT technology stack. Connectivity infrastructure including 5G private networks and NB-IoT enables reliable data transmission from expanding remote and mobile asset types. AI algorithms that identify anomaly signatures and failure precursors in high-dimensional sensor data without manual feature engineering are making IoT analytics deployments faster to commission and more operationally capable.

Synaptics partnered with Google in January 2025 to enhance edge AI for IoT applications, integrating Google's machine learning frameworks with Synaptics' Astra SoC hardware platform to develop AI devices capable of processing vision, voice, and sound data at the edge without cloud round-trip latency. The partnership addressed the growing commercial requirement for IoT analytics devices that deliver real-time inference capability at the data source.

Market Size and Forecast

-

Market Size in 2026E: USD 50.79 Billion

-

Market Size by 2035: USD 341.96 Billion

-

CAGR: 23.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On IoT Analytics Market - Request Free Sample Report

IoT Analytics Market Trends

-

Edge AI analytics is expanding as real-time IoT applications require fast decision-making directly at the data source.

-

Digital twin integration is improving asset monitoring, maintenance planning, and operational optimization through real-time sensor insights.

-

Industrial IoT analytics adoption is growing with Industry 4.0 initiatives focused on connected and intelligent manufacturing.

-

AI-powered anomaly detection is enhancing predictive maintenance accuracy by reducing false alerts and improving reliability.

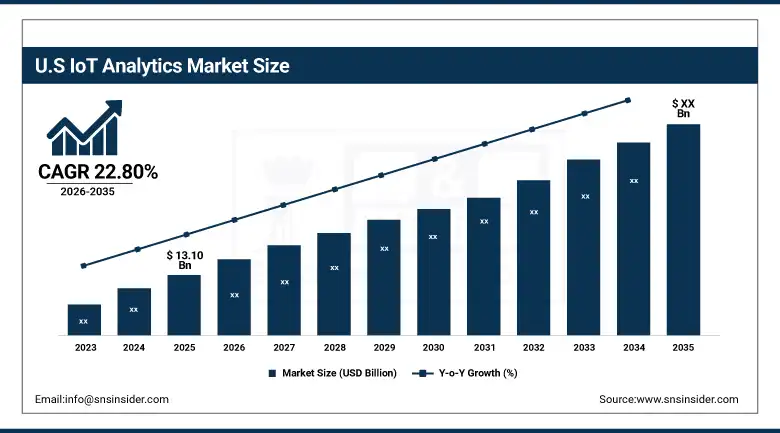

The U.S. IoT Analytics Market Outlook

The U.S. IoT analytics market was valued at approximately USD 13.10 Billion in 2025 and is expected to grow significantly through 2035 at a CAGR of approximately 22.80%.

The U.S. manufacturing sector investment in Industrial IoT and smart factory infrastructure, driven by federal reshoring initiatives, advanced manufacturing tax incentives, and competitive pressure is sustaining the largest single national IoT analytics demand segment globally. The Department of Defense's industrial base modernisation programme, the Department of Energy's grid modernisation and smart building investment, and the Federal Aviation Administration's connected infrastructure monitoring initiatives represent significant government-sector IoT analytics procurement that supplements private sector demand.

Microsoft Azure IoT Hub and Azure Stream Analytics processed over 50 trillion IoT messages per month globally by mid-2025, with the company reporting that its industrial IoT analytics platform had helped manufacturing customers achieve an average of 18% reduction in unplanned equipment downtime. Microsoft's acquisition of Nuance Communications and its subsequent integration of Nuance's AI capabilities into Azure IoT analytics workflows demonstrated the company's strategy of expanding IoT analytics.

IoT Analytics Market Segment Analysis

-

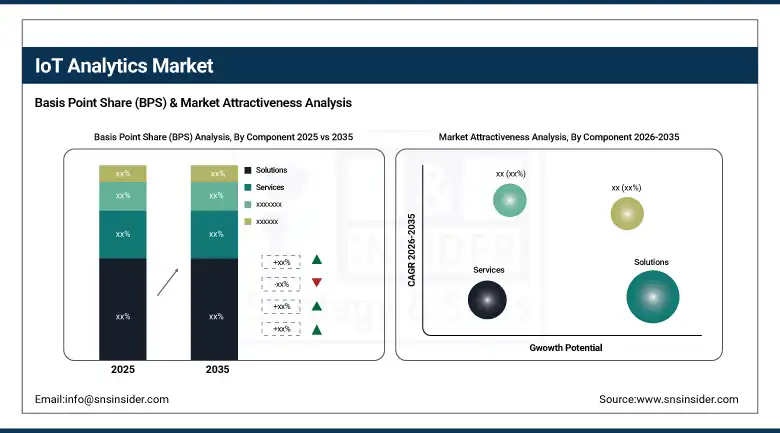

By Component, the solutions segment dominated the market with approximately 68% share in 2025, while the services segment is the fastest growing component with a CAGR of approximately 25% during 2026 to 2035.

-

By Deployment, the on-premise segment dominated the market in 2025, while the cloud-based deployment segment is the fastest growing with strong double-digit CAGR through 2035.

-

By Organization Size, the large enterprises segment dominated the market with approximately 71% share in 2025, while the SME segment is the fastest growing at above-market CAGR.

-

By Application, the predictive maintenance segment dominated the market with approximately 38% share in 2025, while the asset performance management segment is the fastest growing application during 2026 to 2035.

-

By End-User Industry, the manufacturing segment dominated the market with approximately 31% share in 2025, while the energy & utilities segment is the fastest growing industry vertical during 2026 to 2035.

By Component, solutions dominate, services grow fastest

Solutions generated approximately 68% of IoT analytics market revenue in 2025. Their commercial dominance reflects the platform license and SaaS subscription revenue model whose recurring billing structure aligns with the continuous nature of IoT data generation and analytics value delivery. The solutions category includes both horizontal IoT analytics platforms and industrial automation companies, and vertical-specific analytics packages.

Services are growing fastest as the gap between IoT analytics platform capability and enterprise IoT programme maturity creates substantial demand for consulting, system integration, data engineering, and managed analytics operations services.

By Application, predictive maintenance dominates, asset performance management grows fastest

Predictive maintenance accounted for approximately 38% of IoT analytics market revenue in 2025. Organizations that can document the reduction in unplanned equipment downtime costs achieved through predictive maintenance IoT analytics have the most straightforward capital approval pathway. The shift from scheduled preventive maintenance to condition-based predictive maintenance typically reduces maintenance expenditure by 10 to 25% while simultaneously reducing unplanned failures by 30 to 50%.

Asset performance management is growing fastest as IoT analytics platforms expand their application scope from individual asset condition monitoring toward comprehensive fleet-level and process-system-level performance optimisation whose analytical complexity and value creation potential exceeds single-asset predictive maintenance.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

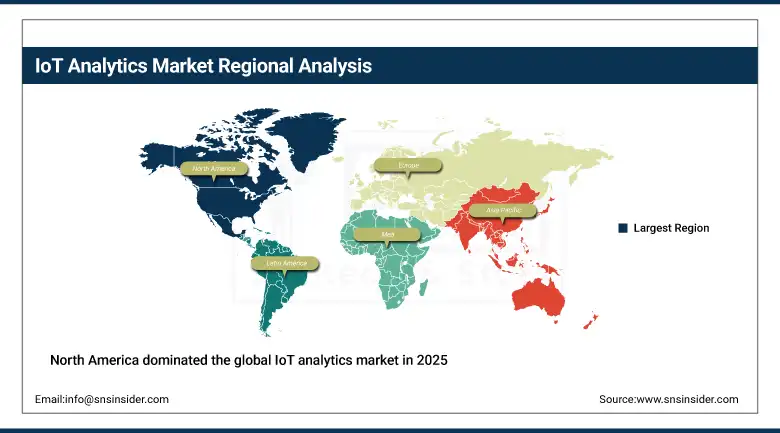

North America IoT Analytics Market Insights

North America dominated the global IoT analytics market in 2025. The United States accounts for approximately 82.47% of regional revenue through its concentration of major IoT analytics platform vendors, the world's most extensive industrial IoT deployment infrastructure across manufacturing, energy, transportation, and healthcare, and the commercial sophistication of its enterprise IoT investment programmes whose scale and maturity generate the highest per-enterprise IoT analytics spending globally. Canada contributes supplementary demand through its oil and gas sector's remote asset monitoring investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe IoT Analytics Market Insights

Europe held a significant share of global IoT Analytics revenues in 2025. Germany, France, the United Kingdom, and the Netherlands are the leading markets, hosting significant manufacturing, energy, and logistics sectors whose Industry 4.0 investment programmes. The European Union's Data Act and Industrial Strategy create regulatory and policy frameworks that sustain enterprise IoT investment across member states. Germany accounts for approximately 28.47% of European revenues through its world-leading automotive and mechanical engineering manufacturing sectors whose connected factory and predictive maintenance investments represent the largest national IoT analytics demand source in Europe.

Asia Pacific IoT Analytics Market Insights

Asia Pacific is the fastest-growing regional IoT analytics market, projected to expand at approximately 22.84% CAGR through 2035. China accounts for approximately 38.47% of Asia Pacific revenues through its government-backed smart manufacturing initiative, its vast industrial base is creating the largest industrial IoT deployment programme and the commercial ambitions of domestic IoT analytics platform providers including Alibaba Cloud, Huawei, and Baidu AI Cloud. Japan, South Korea, India, and Australia each contribute meaningful regional demand through their respective manufacturing, utilities, and smart city IoT programmes.

MEA & Latin America IoT Analytics Market Insights

Middle East and Latin America are growing IoT analytics markets where oil and gas sector remote monitoring investment, smart city infrastructure development, and manufacturing sector digitisation are creating expanding commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through smart city programme's extensive IoT infrastructure investment, the oil and gas sector's operational technology digitization, and the government's AI and digital economy strategy.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large agricultural and manufacturing sectors whose IoT-enabled precision farming and connected factory programmes are creating growing analytics platform demand.

Market Dynamics

Growth Drivers: IoT device growth and proven predictive maintenance benefits are driving strong demand for IoT analytics platforms.

The IoT analytics market's growth is driven by the self-reinforcing cycle of device proliferation and analytics value creation. Each new connected device adds to the data volume whose analysis creates business value, and each documented IoT analytics ROI success story motivates further device and platform investment. The predictive maintenance application's commercial validation across manufacturing, energy, aviation, and transportation has established proof points whose financial magnitude, typically several times the combined cost of IoT hardware and analytics platform investment, removes the investment justification uncertainty that constrained early IoT analytics adoption.

Edge AI processing advances are simultaneously enabling new real-time IoT analytics applications that could not previously be served by cloud-dependent architectures, expanding the addressable IoT analytics market beyond the batch and near-real-time applications that historically defined the category.

Restraints: Data security risks and complex OT-IT integration challenges increase costs and limit large-scale IoT analytics deployment.

Connected industrial assets generate rich operational data whose value is proportional to the accessibility of that data to analytics platforms, but whose connectivity also creates cybersecurity attack surfaces that operational technology operators and industrial asset owners have historically been reluctant to expose. The convergence of IT and OT networks required to bring IoT sensor data to analytics platforms introduces cybersecurity risks in previously air-gapped control environments whose compromise consequences can include equipment damage, production disruption, and safety incidents.

Data integration between OT protocol environments such as Modbus, Profibus, and OPC-UA and cloud analytics platforms whose API architecture is designed for IT data formats requires industrial protocol translation middleware whose procurement, configuration, and maintenance adds implementation complexity and cost beyond standard enterprise software deployment.

Opportunities: AI-native IoT analytics for smart manufacturing and sustainability monitoring offer significant growth opportunities through 2035.

AI-native IoT analytics platforms whose machine learning models are pre-trained on large industrial equipment datasets and whose deployment architecture enables rapid time-to-value without extensive data engineering preamble represent the most commercially compelling product development direction for IoT analytics vendors. Manufacturing customers whose capital approval processes require demonstrated ROI within 12 months face a time-to-value barrier that complex custom analytics implementations cannot clear efficiently, creating a commercial pull for pre-packaged AI models tuned for specific equipment types and failure modes that deliver actionable predictions from minimal custom data collection.

Sustainability analytics applications that combine IoT energy metering, resource consumption monitoring, and emissions estimation to generate the operational data required for Scope 1 and Scope 2 GHG reporting represent a rapidly growing IoT analytics application whose regulatory mandate from SEC climate disclosure rules, CSRD in Europe, and voluntary science-based target commitments is creating compliance-driven investment.

Recent Developments:

-

2025: Synaptics partnered with Google to integrate Google machine learning frameworks with Synaptics Astra SoC hardware for edge AI IoT applications, enabling real-time vision, voice, and sound inference at the device level without cloud latency dependency, targeting industrial inspection, anomaly detection, and environmental monitoring applications.

-

2025: Microsoft Azure IoT reported processing over 50 trillion IoT messages per month globally, with its predictive maintenance analytics capability demonstrating average 18% unplanned downtime reduction at manufacturing customers through AI-powered equipment health monitoring.

-

2024: Amazon Web Services launched AWS IoT TwinMaker integration with AWS Bedrock generative AI services, enabling IoT analytics customers to query digital twin simulation models through natural language interfaces that democratize operational intelligence access beyond specialist data science teams to operations management and engineering staff.

IoT Analytics Market key players are:

-

Microsoft Corporation

-

Amazon Web Services Inc.

-

IBM Corporation

-

Cisco Systems Inc.

-

Oracle Corporation

-

SAP SE

-

Databricks

-

Siemens AG

-

PTC Inc.

-

Software AG

-

Snowflake Inc.

-

SAS Institute Inc.

-

Accenture PLC

-

Dell Technologies Inc.

-

Hewlett Packard Enterprise

-

Hitachi Ltd.

-

C3 AI

-

Alibaba Cloud

-

Huawei Technologies Co. Ltd.

-

Synaptics Incorporated

IoT Analytics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 41.10 Billion |

| Market Size by 2035 | USD 341.96 Billion |

| CAGR | CAGR of 23.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Cloud-Based, On-Premise) • By Organization Size (Large Enterprises, Small & Medium-Sized Enterprises) • By Application (Predictive Maintenance, Fleet Management, Asset Performance Management, Energy Management, Remote Monitoring, Others) • By End-User Industry (Manufacturing, Transportation & Logistics, Healthcare, Energy & Utilities, Retail, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation, Amazon Web Services Inc., IBM Corporation, Cisco Systems Inc., Oracle Corporation, SAP SE, Databricks, Siemens AG, PTC Inc., Software AG, Snowflake Inc., SAS Institute Inc., Accenture PLC, Dell Technologies Inc., Hewlett Packard Enterprise, Hitachi Ltd., C3 AI, Alibaba Cloud, Huawei Technologies Co. Ltd., Synaptics Incorporated |

Frequently Asked Questions

The market is expected to grow at a CAGR of 23.60% from 2026 to 2035.

The market was valued at USD 41.60 Billion in 2025.

The primary growth factors are the exponential proliferation of connected IoT devices generating actionable data volumes at unprecedented scale.

The predictive maintenance segment dominated the market with approximately 38% share in 2025.

North America dominated the IoT Analytics Market in 2025.

Get in Touch