IoT Insurance Market Report Scope & Overview:

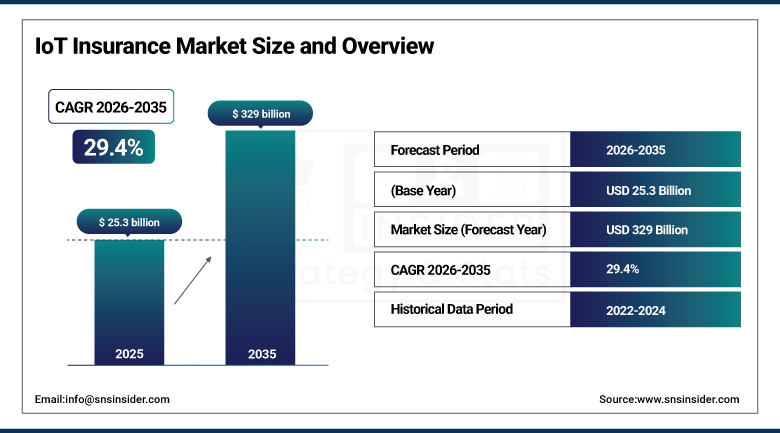

The IoT Insurance Market was valued at USD 25.3 billion in 2025 and is expected to reach USD 329 billion by 2035, growing at a CAGR of 29.4% from 2026–2035.

IoT insurance combines the use of connected devices with the processes of insurance underwriting, risk management, and claims management. Under the current system, insurers use historical information and demographic information to arrive at the right insurance premium. IoT disrupts this process through real-time information that gives insurers information about the actual behavior and conditions surrounding their insured. A connected car provides insurers information about how fast an individual drives, when they apply brakes, and which routes they use. The installation of sensors in a home enables insurers to know if there is any water leakages. A fitness tracker provides information on one’s physical activity and sleep patterns.

AI integration is transforming what IoT data can tell insurers. Machine learning models that analyze driving behavior, property conditions, and health metrics can predict claims before they happen, enabling proactive intervention. Fraud detection systems using IoT data are also reducing false claims by up to 25%, significantly improving insurer profitability.

Market Size and Forecast

-

Market Size in 2025: USD 25.3 Billion

-

Market Size by 2035: USD 329 Billion

-

CAGR: 29.4% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on IoT Insurance Market - Request Free Sample Report

Market Trends

-

Usage-based auto insurance using telematics devices is moving from optional to default in many markets as data shows it reduces accidents.

-

Health and life insurers are partnering with wearable device companies to offer premium incentives for healthy lifestyle behaviors.

-

Smart home sensors for fire, water leak, and security detection are enabling property insurers to move from reactive claims to proactive prevention.

-

AI and machine learning are improving the quality of risk prediction models built on IoT sensor data.

-

Insurtech startups are disrupting traditional insurers by building IoT-native insurance products from the ground up.

-

Commercial property and fleet insurance are seeing rapid adoption of IoT-based monitoring that reduces both risk and premiums.

-

Agricultural IoT sensors for weather, soil, and crop health are enabling insurtech companies to develop parametric crop insurance products.

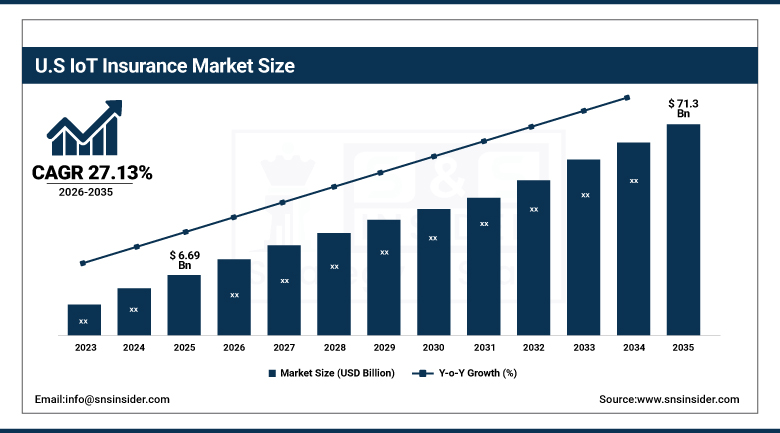

U.S. IoT Insurance Market was valued at USD 6.69 billion in 2025 and is expected to reach USD 71.3 billion by 2035, growing at a CAGR of 27.13% from 2026 to 2035.

The USA represents the largest insurance market for IoT products worldwide. Insurance companies from America were among the first that started providing telematic car insurance programs based on the driver's behavior. Progressive, Allstate, and State Farm offer behavioral pricing for thousands of customers. In addition, the health insurance market in the USA was one of the first that offered programs using wearable devices for collecting data related to healthy behaviors to receive discounts on premiums. Programs for insuring smart houses in collaboration with manufacturers such as Ring and Nest have been developing quickly.

Usage-based insurance in the U.S. automotive sector has grown from a niche offering to a mainstream product option at most major insurers. As younger drivers who are accustomed to sharing data become the primary auto insurance customer segment, adoption rates are expected to rise sharply. By 2035, usage-based pricing could be the default for a majority of personal auto policies.

Market Segment Insights

-

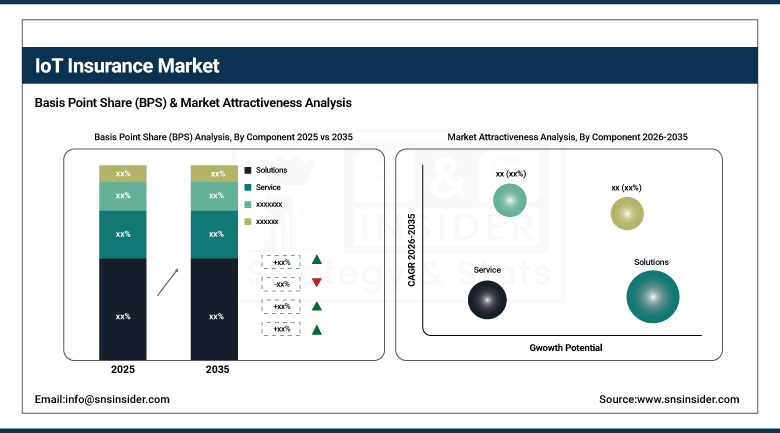

Based on Component, Solutions dominated with 66% revenue share in 2025; the Services segment is growing at the highest CAGR.

-

Based on Insurance Type, Automotive & Transportation led with 27% share in 2025; Healthcare is the fastest-growing insurance type.

-

Based on Application, Automotive & Transportation is the largest application; Health & Wellness applications are growing rapidly.

-

Based on End-Use, Large Enterprises dominate current adoption; SMEs are an emerging growth segment as affordable IoT platforms become available.

Market Segment Analysis

By Component: Solutions Lead, Services Growing Fast

The solutions segment includes the technology used to deliver the IoT insurance solution these are telematics devices, wearable connectivity platforms, smart home sensor systems, analytics platforms, and AI-driven underwriting platforms. Solutions will drive 66% of the revenue share in 2025 as technology infrastructure is an essential investment for any insurer looking to enter the world of IoT.

The Services segment will comprise consulting, data management services, analytics services, and professional services. The increasing number of insurers adopting IoT insurance programs will create high demand for services related to program design, data analysis, and integration with insurance IT infrastructures. The services market is segmented into three categories of providers: the big four consulting firms, specialized insurtech service providers, and technology vendors' professional services divisions.

By Insurance Type: Auto Leads, Health Growing Fastest

Auto insurance was the pioneer of IoT insurance. Telematic technology that measures driver behavior has been available from the largest providers of insurance products for more than a decade. The facts show that usage-based insurance significantly impacts positive changes in driver behavior and reduces accidents. Usage-based insurance programs help millions of drivers around the world, and their popularity is spreading quickly. For organizations that manage fleets of vehicles, telematic technology is used to monitor vehicles.

Health insurance is one of the fastest-growing IoT insurance segments. Devices measuring the number of steps per day, heart rate, quality of sleep, and other health parameters are widely used. Insurance companies from South Africa to Hong Kong to the United States are offering discounts and awards to clients for exceeding their target metrics. It was proven that the usage-based insurance in this segment leads to better results in terms of clients' well-being and risk reduction for insurers. IoT property and casualty insurance is developing fast. Devices monitoring water leaks, security cameras, fire detectors, and temperature help property insurers measure risk levels. In some cases, insurers cooperate with device manufacturers to distribute free devices among policyholders.

By Application: Automotive Biggest, Agriculture Emerging

The automotive sector still constitutes the largest IoT insurance application worldwide. Connected cars generate a large amount of telematics data which can be leveraged by the insurer for its purposes. As the connection level in vehicles increases and cars move towards becoming completely autonomous, the data for insurers to work on would increase manifold.

Another promising use case in IoT insurance would be for agricultural purposes. The farmers have huge financial risk exposure due to adverse weather, pests, and diseases. IoT sensors used to measure soil moisture, weather conditions, and crop conditions give rise to innovative insurance products based on parametric insurance that pay out once sensor data indicates a certain threshold has been reached.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

79% |

|

Europe |

United Kingdom |

30% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

UAE |

37% |

|

Latin America |

Brazil |

51% |

North America

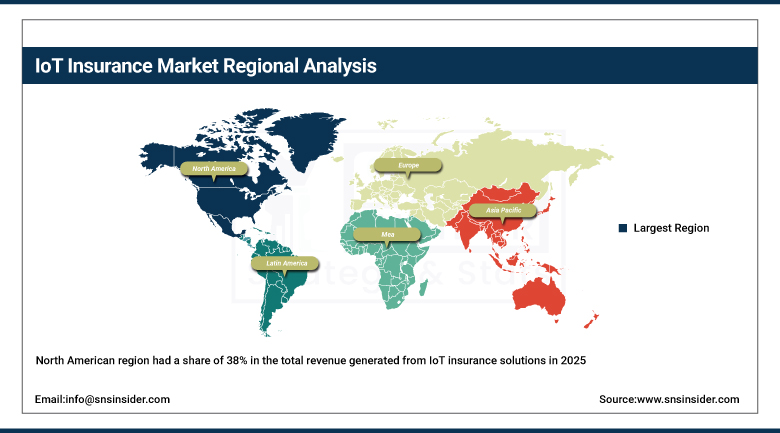

The North American region had a share of 38% in the total revenue generated from IoT insurance solutions in 2025. The U.S. emerged as the leader in the market. Insurers in the United States are leading in telematics auto insurance products and wearable health insurance plans. Advanced digital technology, high usage of smartphones and connected devices, and competition in the insurance industry drive growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe

Europe represents an important market with a high uptake of telematics insurance products for cars, especially in Italy and UK, which have some of the highest penetration rates worldwide. GDPR imposes certain limitations regarding how IoT data can be gathered and leveraged by insurance companies, resulting in a need for designing programs that comply with the GDPR requirements.

Asia Pacific

Asia-Pacific is the most rapidly growing IoT insurance market region, having a compound annual growth rate (CAGR) of 31.1% during the forecast period. This rapid growth in China, India, Japan, and other southeast Asian nations is due to high smartphone usage, population growth, increasing awareness regarding insurance, and backing from the government for smart cities and digital healthcare. Telematics has been adopted early by Chinese automobile insurers with support from the vehicle connectivity system.

Middle East & Africa

Middle East is one region in which the IoT insurance can flourish quickly due to high use of smartphones, increased knowledge regarding insurance services, and digital transformation efforts by governments in the area. South Africa stands out in Africa in terms of telematics auto insurance coverage and health insurance wearables offered by many insurance providers in that country.

Latin America

Latin America is a new IoT insurance market, where increased traffic accidents are encouraging the use of telematics auto insurance due to the presence of strong economic incentives. Brazil, Mexico, and Colombia are the most promising markets in Latin America. Insurtech start-ups are developing IoT-based products in order to circumvent the limitations posed by conventional insurance technologies.

Market Growth Drivers

-

Real-time IoT data enables better risk pricing and proactive loss prevention

Market for IoT Insurance is experiencing rapid growth with the help of real-time data coming from IoT technology, which helps insurance companies to assess risks better, increase the accuracy of their pricing, and improve client interactions. For instance, use of telematics devices, wearables, and connected home sensors helps insurance companies track their clients' activities and minimize potential risks. Moreover, usage of such connected technologies helps avoid fraudulent claims and minimize expenses.

The ability of IoT systems to prevent losses before they occur is a major differentiator. When a smart home sensor detects a water leak and alerts both the homeowner and the insurer before significant damage occurs, the claim that never happens saves everyone money and stress. This prevention capability is creating new value propositions that expand the role of insurers from passive risk compensators to active risk managers in their customers' lives.

Market Restraints

-

Privacy concerns and data security risks are barriers to consumer adoption

Many consumers are uncomfortable with the level of surveillance that IoT insurance programs require. Driving behavior monitoring, home sensor networks, and health data collection all involve tracking behavior in very personal domains. High-profile data breaches at insurance companies have increased anxiety about what happens when this sensitive data is compromised. Regulators in some markets are tightening rules on data collection and use, which adds compliance complexity and limits some program designs.

Market Opportunities

-

Parametric insurance and micro-insurance enabled by IoT data reach new markets

The data from IoT can lead to a completely new line of insurance products, which would significantly enlarge the market. For instance, parametric insurance, which provides payouts based on the activation of certain sensors measuring flood levels, temperature, or earthquake intensity, removes the entire process of adjusting the claim, allowing insurance to become faster and easier during emergencies. It works especially well in agriculture and weather insurance. Micro-insurance products made possible by IoT data would cover the uninsured people of developing nations.

Recent Developments

-

2025: Progressive launched Snapshot 3.0 with enhanced AI-driven driver coaching, giving customers real-time feedback on driving habits through their smartphone app and showing measurable premium savings of 15-30% for consistently safe drivers over 12 months.

-

2024: Arity and Toyota affiliate CAS announced a partnership to share connected vehicle driving data with auto insurers, expanding the data pipeline for usage-based insurance and demonstrating how OEM-insurer data sharing partnerships are reshaping the telematics insurance model.

Key Players

Leading companies in the IoT Insurance Market:

-

Progressive Corporation – Snapshot Usage-Based Insurance

-

Allstate Corporation – Drivewise Telematics Program

-

State Farm Mutual – Drive Safe & Save Program

-

Cisco Systems Inc. – Cisco Kinetic for Insurance

-

Accenture PLC – Connected Insurance Platform

-

Verisk Analytics Inc. – AIR Worldwide and Telematics

-

Wipro Limited – HOLMES IoT Insurance Analytics

-

Google LLC – Google Cloud IoT for Insurance

-

IBM Corporation – IBM IoT Insurance Platform

-

Microsoft Corporation – Azure IoT Hub for Insurers

-

Synechron Inc. – Digital Financial Services Solutions

-

LexisNexis Risk Solutions – Telematics and Risk Data

-

Lemonade Inc. – AI-Native Homeowners Insurance

-

Root Insurance Company – Mobile Telematics Auto Insurance

-

Metromile Inc. – Pay-Per-Mile IoT Auto Insurance

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.3 Billion |

| Market Size by 2035 | USD 329 Billion |

| CAGR | CAGR of 29.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Insurance Type (Life & Health, Property & Casualty, Automotive, Commercial & Residential Buildings, Agriculture, Others) • By Application (Automotive & Transportation, Health & Wellness, Smart Home & Property, Business & Enterprise, Agriculture, Others) • By End-Use (Large Enterprises, SME) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Progressive Corporation, Allstate Corporation, State Farm Mutual, Cisco Systems Inc., Accenture PLC, Verisk Analytics Inc., Wipro Limited, Google LLC, IBM Corporation, Microsoft Corporation, Synechron Inc., LexisNexis Risk Solutions, Lemonade Inc., Root Insurance Company, Metromile Inc. |

Frequently Asked Questions

The market was valued at USD 25.3 billion in 2025.

The market is expected to grow at a CAGR of 29.4% from 2026 to 2035.

Get in Touch