Lancet Market Report Scope & Overview:

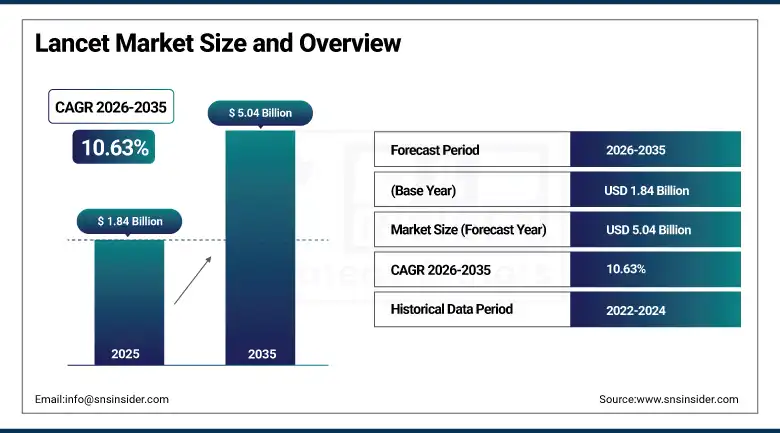

The Lancet Market was valued at USD 1.84 Billion in 2025 and is expected to reach USD 5.04 Billion by 2035, growing at a CAGR of 10.63% from 2026-2035.

The global lancet market is experiencing robust growth driven by the growing global prevalence of diabetes, expanding self-monitoring blood glucose practices, and rising point-of-care diagnostic testing adoption. Lancets are small, disposable, single-use medical devices that pierce skin to obtain capillary blood samples for glucose monitoring, cholesterol testing, hemoglobin measurement, and infectious disease diagnostic testing. With more than 537 million people living with diabetes globally and IDF projections indicating growth toward 783 million by 2045, the SMBG-driven demand for lancets represents the most commercially certain structural growth driver in the market. Advances in lancet technology including ultra-thin needles, push-button safety mechanisms, and pressure-activated designs are fueling consumer demand for less painful blood sampling devices.

In 2024, Becton, Dickinson and Company (BD) launched its BD Microtainer Contact-Activated Lancet with enhanced ergonomic grip and 30-gauge needle for pediatric and neonatal blood collection applications, offering ultra-low volume capillary blood sampling from heel stick procedures with reduced pain and improved patient compliance. The product launch reflects the commercial direction of safety lancet development toward patient-specific designs whose ergonomic improvements and procedure-specific needle gauge optimization create clinical workflow advantages that sustain premium specification above commodity lancet alternatives.

Market Size and Forecast

-

Market Size in 2026E: USD 2.04 Billion

-

Market Size by 2035: USD 5.04 Billion

-

CAGR: 10.63% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Lancet Market - Request Free Sample Report

Lancet Market Trends

-

Ultra-thin lancets with 36-gauge and smaller needles reduce pain, improving patient compliance in home diagnostics.

-

Safety lancet adoption is increasing due to healthcare regulations aimed at preventing needlestick injuries in clinical settings.

-

Integrated lancet and lancing devices simplify blood sampling, improving usability for elderly and visually impaired patients.

-

Rising CGM adoption is reshaping lancet demand while expanding diabetes diagnosis and overall patient monitoring volumes.

-

Community diabetes screening programs are increasing lancet consumption through large-scale glucose and HbA1c testing initiatives.

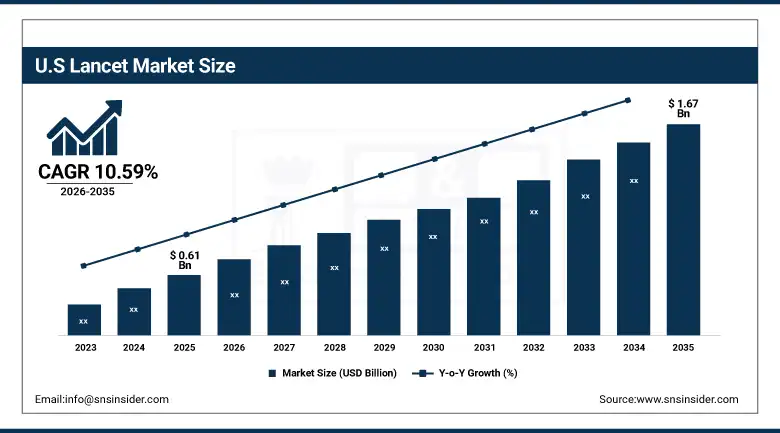

The U.S. Lancet Market Outlook

The U.S. Lancet Market was valued at approximately USD 0.61 Billion in 2025 and is expected to reach approximately USD 1.67 Billion by 2035, growing at a CAGR of approximately 10.59%.

The U.S. is the most commercially sophisticated lancet market within North America’s dominant revenue position. Becton Dickinson, Roche Diagnostics, Abbott, LifeScan, and Terumo collectively define the domestic lancet commercial landscape. The CDC’s estimate of 38.4 million Americans with diabetes and 97.6 million with prediabetes creates the world’s most commercially concentrated diabetes lancet demand environment. CMS reimbursement for SMBG supplies under Medicare Part B creates structured government-funded procurement that sustains above-average U.S. market commercial value. OSHA’s Bloodborne Pathogen Standard’s needle safety device requirements create institutional healthcare setting compliance procurement that sustains safety lancet adoption across hospitals and clinical laboratories.

In 2023, Owen Mumford launched the Unistik Touch safety lancet in the U.S. market with a 28-gauge needle and ergonomically designed trigger mechanism that provides single-handed activation without requiring the patient to manually set the depth adjustment, reducing the procedure steps that create compliance barriers for patients with limited dexterity or vision. The launch reflects the commercial importance of patient-centric lancet design whose usability improvement for elderly, arthritic, and visually impaired SMBG patients creates commercial differentiation that sustains premium pricing above commodity lancet alternatives.

Lancet Market Segment Analysis

-

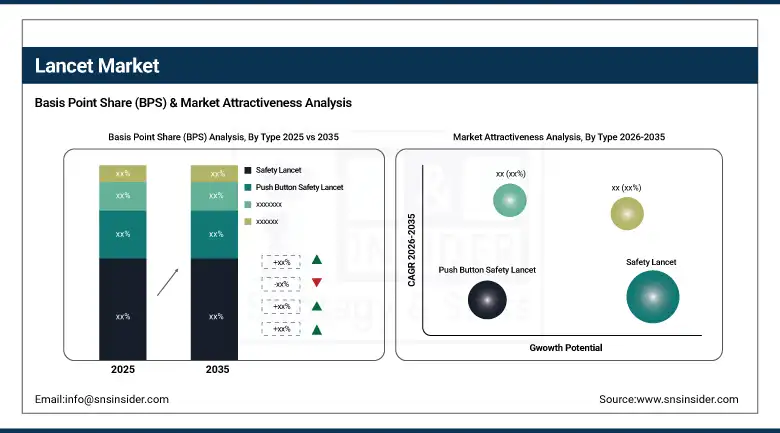

By Type, the safety lancet segment dominated the lancet market with approximately 48% share in 2025, while the push button safety lancet segment is the fastest growing.

-

By Gauge Size, the 23G-33G segment dominated the market with approximately 41% share in 2025, while the above 33G segment is the fastest growing.

-

By Age group, the adults segment dominated the lancet market with approximately 67% share in 2025, while the pediatrics segment is the fastest growing.

-

By End User, the hospitals & clinics segment dominated the lancet market with approximately 38% share in 2025, while the home diagnostics segment is the fastest growing.

By Type, safety lancets dominate, push button grows fastest

Safety lancets retained the dominant type position with approximately 48% of the lancet market in 2025. Their commercial primacy reflects the structured compliance requirement that occupational health and safety regulations create for healthcare setting lancet procurement. OSHA’s Needlestick Safety and Prevention Act’s requirement for needle safety devices, EU Directive 2010/32/EU’s sharp injury prevention mandate, and equivalent national needlestick prevention regulations across major markets collectively create institutional procurement preference for safety lancets whose automatic needle retraction eliminates the post-use exposure risk that conventional lancets create for healthcare workers.

Push button safety lancets are the fastest-growing type because the home diagnostics market’s 537 million diabetic patient population’s self-monitoring blood glucose practice creates consumer lancet procurement whose patient-centric design preference favors the push button mechanism’s single-handed activation simplicity over the multi-step setting and manual insertion process that conventional lancet-and-lancing-device combinations require. Each elderly diabetic patient whose arthritis or reduced dexterity creates difficulty with conventional lancet loading and safety cap removal creates commercial motivation for push button lancet specification whose operational simplicity sustains above-average adoption growth in the ageing global diabetes patient population.

By End User, hospitals dominate, home diagnostics grows fastest

Hospitals and clinics retained the dominant end-user position with approximately 38% of the lancet market in 2025. Hospital laboratory settings’ daily capillary blood glucose monitoring across inpatient populations, pediatric blood collection programmes requiring heel stick capillary sampling, and point-of-care testing for infectious disease, cholesterol, and hemoglobin levels collectively create the most commercially concentrated institutional lancet procurement environment. Each hospital’s formulary committee selection of a preferred safety lancet brand creates volume procurement relationships whose contract renewal sustains long-duration commercial partnerships with hospital group purchasing organisations.

Home diagnostics is the fastest-growing end user because the global diabetes patient population’s SMBG compliance creates the most commercially extensive consumer lancet demand category whose daily per-patient lancet consumption across 537 million patients creates aggregate annual demand exceeding 200 billion lancets globally. Each newly diagnosed diabetic patient who initiates SMBG monitoring creates a multi-year consumer lancet procurement relationship whose frequency, averaging 1-4 finger sticks per day for Type 2 patients and 4-10 per day for intensively managed Type 1 patients, creates above-average annual consumption relative to any other consumer medical device.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

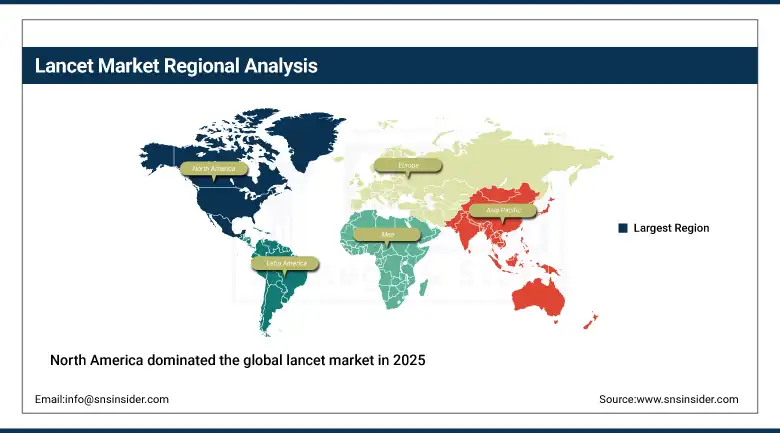

North America Lancet Market Insights

North America dominated the global lancet market in 2025 driven by the high prevalence of diabetes and pre-diabetes, advanced healthcare infrastructure, established SMBG practice, and the commercial presence of Becton Dickinson, Roche Diagnostics, Abbott, LifeScan, and Terumo. The United States accounts for approximately 87.4% of North American revenues through CMS Medicare Part B reimbursement for diabetes monitoring supplies, OSHA needlestick safety compliance creating institutional safety lancet procurement, and the above-average per-capita healthcare investment that sustains premium lancet specification.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system’s diabetes monitoring supply coverage, the provincial health insurance programmes’ lancet reimbursement, and the growing Type 2 diabetes prevalence creating consumer home diagnostics demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Lancet Market Insights

Europe is a technically sophisticated lancet market where EU Directive 2010/32/EU’s mandatory sharp injury prevention requirement creates structured safety lancet procurement across all healthcare settings, the National Health Service reimbursement schemes sustain consistent institutional demand, and the universal healthcare coverage creates equitable lancet access. Germany accounts for approximately 22.3% of European revenues through its above-average diabetes prevalence, the hospital sector’s strict needlestick safety compliance, and B. Braun Melsungen’s domestic commercial presence.

The United Kingdom, France, and Sweden are significant secondary markets where NHS lancet supply provision, statutory needlestick prevention regulation, and the growing diabetes patient population create consistent commercial demand. Sarstedt’s and Owen Mumford’s European commercial presence sustain regional market supply from established manufacturing and distribution networks.

Asia Pacific Lancet Market Insights

Asia Pacific is the fastest-growing regional lancet market, driven by the world’s largest diabetes patient population concentrated in China and India, rapid healthcare infrastructure expansion, growing SMBG awareness, and the progressive adoption of point-of-care diagnostic testing across public health programmes. China accounts for approximately 44.8% of Asia Pacific revenues through its estimated 140 million diabetic citizens whose SMBG adoption creates the world’s most commercially significant single-country lancet consumer market, combined with the hospital sector’s institutional procurement.

India represents the most commercially dynamic emerging market within Asia Pacific where the 101 million diabetic population, the government’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke, and the rapidly growing retail pharmacy chain’s lancet accessibility create above-average market growth that compounds with India’s healthcare infrastructure development trajectory.

MEA & Latin America Lancet Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through the Gulf region’s above-average diabetes prevalence estimated at 17.6% of the adult population, the Ministry of Health’s national diabetes management programme, and the advanced hospital sector’s institutional safety lancet procurement. Brazil leads Latin American revenues at approximately 44.2% through its large diabetic population, the SUS public health system’s diabetes monitoring supply distribution, and the growing private healthcare sector’s diagnostic testing investment. Growing diabetes burden across both regions and expanding healthcare access collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Global diabetes epidemic and safety regulation mandating needlestick-safe lancet procurement

The global diabetes epidemic is the lancet market’s most commercially certain structural growth driver. The IDF’s documentation of 537 million adults with diabetes in 2021, growing to a projected 643 million by 2030 and 783 million by 2045, creates a continuously expanding patient population whose SMBG practice creates per-patient daily lancet consumption that compounds with diagnosis rate improvement. Each new diabetes diagnosis that initiates SMBG monitoring creates a multi-year consumer lancet procurement relationship whose frequency and duration create above-average lifetime commercial value per acquired customer. The WHO’s Global Diabetes Compact seeking to enhance access to diabetes monitoring in underserved populations creates additional below-market access programme procurement that sustains volume growth beyond commercial market dynamics.

Occupational safety regulation mandating safety lancet use in healthcare settings creates structured non-discretionary institutional procurement across hospital, laboratory, and clinical care environments. Each healthcare institution’s occupational health programme that specifies safety lancets as standard procedure creates procurement that sustains safety lancet market leadership through compliance motivation independent of price differential versus conventional alternatives.

Restraints: CGM adoption reducing SMBG frequency and high cost in low-income markets

Continuous glucose monitor adoption among intensively managed Type 1 diabetes patients is creating structural headwind for lancet per-patient consumption as each CGM user who replaces multiple daily finger stick readings with continuous sensor measurement reduces lancet consumption from 4-10 per day to near-zero during CGM wear periods. Each CGM adoption cycle that replaces SMBG practice creates lancet volume displacement that moderates per-diagnosed-patient lancet procurement growth rates in developed markets with above-average CGM adoption.

High advanced safety lancet cost relative to conventional alternatives creates affordability barriers in low-income countries and cost-sensitive patient populations whose out-of-pocket lancet expenditure limits consumption frequency below clinically recommended testing schedules. Each patient whose financial constraint reduces SMBG frequency below recommended levels creates suboptimal glycemic management outcomes whose commercial impact moderates the full market potential that diabetes prevalence growth theoretically enables.

Opportunities: Minimally invasive lancet innovation and emerging market diabetes programme expansion

Minimally invasive lancet innovation through ultra-fine needle gauge, micro-needle array, and non-sharp penetration technologies represents the most commercially premium product development direction whose pain elimination creates patient preference that sustains premium pricing above commodity lancet alternatives. Each technology improvement that demonstrably reduces lancet use pain creates commercial adoption momentum among SMBG-resistant diabetic patients whose finger stick discomfort has historically created non-compliance with recommended testing frequency.

Emerging market diabetes programme expansion represents the most commercially significant volume growth opportunity whose large and rapidly growing diabetic populations in India, Africa, and Southeast Asia create first-time SMBG adoption markets whose per-patient lancet consumption establishment creates multi-decade recurring procurement relationships that compound with diabetes prevalence growth.

Recent Developments:

-

2026: Terumo Corporation strengthened its capillary blood collection solutions by introducing higher-precision lancet technologies designed for home healthcare and point-of-care diagnostics.

-

2025: Becton, Dickinson and Company (BD) expanded its safety-engineered blood collection portfolio by enhancing lancet designs focused on needlestick injury prevention and patient comfort.

-

2025: Owen Mumford Ltd. advanced its safety lancet product range with improved single-use activation mechanisms and low-pain blood sampling technology for diabetes testing applications.

Lancet Market key players are:

-

Becton, Dickinson and Company (BD)

-

Roche Diagnostics

-

Abbott Laboratories

-

LifeScan Inc. (Platinum Equity)

-

Terumo Corporation

-

Owen Mumford Ltd.

-

B. Braun Melsungen AG

-

Sarstedt AG & Co. KG

-

Nipro Corporation

-

ARKRAY Inc.

-

Ypsomed AG

-

Improve Medical Instruments (Zhejiang)

-

GMMC (Suzhou) Medical Instrument Co., Ltd.

-

Trividia Health

-

Greiner Bio-One GmbH

-

HTL-STREFA S.A.

-

Medline Industries, LP

-

Bionime Corporation

-

Agappe Diagnostics

-

ForaCare Inc.

Lancet Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.84 Billion |

| Market Size by 2035 | USD 5.04 Billion |

| CAGR | CAGR of 10.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Safety Lancet, Push Button Safety Lancet, Pressure Activated Safety Lancet, Personal Lancet) • By Age Group (Adult, Pediatrics) • By Gauge Size (22G and Below, 23G-33G, Above 33G) • By End User (Hospitals & Clinics, Diagnostic Centers & Pathology Laboratories, Home Diagnostics, Research & Academic Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Becton, Dickinson and Company (BD), Roche Diagnostics, Abbott Laboratories, LifeScan Inc. (Platinum Equity), Terumo Corporation, Owen Mumford Ltd., B. Braun Melsungen AG, Sarstedt AG & Co. KG, Nipro Corporation, ARKRAY Inc., Ypsomed AG, Improve Medical Instruments (Zhejiang), GMMC (Suzhou) Medical Instrument Co., Ltd., Trividia Health, Greiner Bio-One GmbH, HTL-STREFA S.A., Medline Industries, LP, Bionime Corporation, Agappe Diagnostics, ForaCare Inc. |

Frequently Asked Questions

The Lancet Market is expected to grow at a CAGR of 10.63% from 2026 to 2035.

The Lancet Market was valued at USD 1.84 Billion in 2025.

The growing global prevalence of diabetes affecting more than 537 million people creating sustained SMBG-driven lancet demand.

Safety Lancet dominated the Lancet Market with approximately 48% share in 2025.

North America dominated the Lancet Market in 2025.

Get in Touch