Blood Glucose Monitoring Device Market Size Analysis:

Get more information on Blood Glucose Monitoring Device Market - Request Sample Report

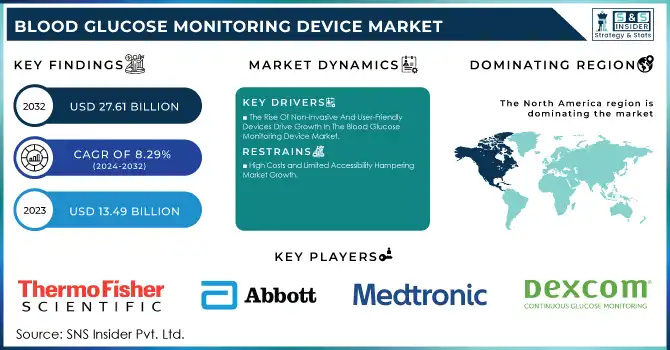

The Blood Glucose Monitoring Device Market Size was valued at USD 13.49 billion in 2023 and is expected to reach USD 27.61 billion by 2032 and grow at a CAGR of 8.29% over the forecast period 2024-2032.

The Blood Glucose Monitoring Device Market is experiencing robust growth, driven by the rising global prevalence of diabetes. According to the International Diabetes Federation, approximately 537 million adults will be living with diabetes in 2021, a number expected to grow to 643 million by 2030. Sedentary lifestyles, poor dietary habits, and an aging global population primarily drive this increase. As a result, the demand for efficient glucose monitoring devices is at an all-time high, particularly in diabetes management.

Technological innovations in Continuous Glucose Monitoring (CGM) systems also significantly influence market growth. Devices such as Abbott's FreeStyle Libre and Dexcom's CGM systems provide real-time glucose readings, offering better accuracy and less frequent need for finger pricks. Recent advancements include Abbott's Libre Rio and Lingo models, which were approved by the FDA in 2024 for over-the-counter (OTC) use. These innovations make CGMs more accessible, expanding their adoption among both diabetic and non-diabetic individuals who want to monitor their metabolic health. This OTC clearance is expected to drive adoption in the wider consumer market, beyond traditional diabetes care.

Moreover, the glucose monitoring device market is extending beyond diabetes management. Athletes and fitness enthusiasts are increasingly using CGMs to optimize performance by better managing their glucose levels. Studies have shown that CGMs can help individuals improve energy management, training efficiency, and recovery times. This growing interest in monitoring glucose levels for general wellness and performance optimization is expected to be a key market driver in the coming years.

Despite these positive developments, the market faces challenges such as the high cost of advanced monitoring systems and limited access in rural regions, particularly in low-income countries. However, government initiatives like the National Clinical Care Commission’s “All-of-Government” approach and ongoing efforts to reduce diabetes care costs and increase product accessibility are expected to mitigate some of these barriers.

Blood Glucose Monitoring Device Market Dynamics

Drivers

-

The Rise Of Non-Invasive And User-Friendly Devices Drive Growth In The Blood Glucose Monitoring Device Market

Innovations like continuous glucose monitoring systems and flash glucose monitors are enhancing accuracy and convenience, which in turn drives higher consumer adoption. These cutting-edge devices provide real-time glucose level data, empowering individuals to manage their health more effectively and prevent diabetes complications. Another significant driver is the growing emphasis on personalized medicine, where glucose monitoring solutions play an essential role in tailoring treatment plans to meet individual patient needs. These devices enable data-driven decision-making, allowing healthcare providers to enhance patient outcomes and improve overall diabetes management.

-

Rising Awareness About Diabetes Care Is Also Contributing To Market Growth

Governments, non-profit organizations, and healthcare providers are making concerted efforts to educate the public on the importance of blood glucose monitoring. Campaigns aimed at promoting better diabetes management and encouraging early detection of blood sugar abnormalities are boosting the demand for glucose monitoring devices. The aging population in developed and emerging markets is also a key factor driving the market's expansion. Older adults are more susceptible to developing type 2 diabetes, creating a rising demand for reliable glucose monitoring systems to manage age-related health challenges.

Restraints

-

High Costs and Limited Accessibility Hampering Market Growth

The Cardiac Monitoring Device Market faces significant challenges stemming from the high costs associated with advanced cardiac monitoring technologies. Devices such as implantable loop recorders, portable ECG monitors, and wearable cardiac monitors are often expensive to produce and purchase due to the integration of cutting-edge technology and sophisticated features. These elevated costs pose a barrier to adoption, particularly in low- and middle-income regions, where healthcare budgets are constrained, and a large proportion of the population remains uninsured. The affordability factor becomes a critical restraint, limiting access to these life-saving devices for economically disadvantaged patients.

Furthermore, the accessibility of cardiac monitoring devices is restricted in rural and remote areas, where healthcare infrastructure is underdeveloped, and distribution networks are insufficient. Many regions lack adequate healthcare facilities or trained professionals to recommend or manage advanced cardiac devices, hindering their penetration in these markets. The limited availability exacerbates the challenge of timely diagnosis and effective monitoring of cardiac conditions in these areas.

Blood Glucose Monitoring Device Market Segmentation Analysis

By Product

In 2023, self-monitoring devices dominated the blood glucose monitoring device market, holding 60% of the market share. These devices, such as traditional blood glucose meters, are widely used by diabetes patients due to their affordability, ease of use, and portability. Self-monitoring devices allow patients to track their blood glucose levels regularly at home, making them a cost-effective and accessible solution. The convenience of at-home monitoring empowers users to make timely adjustments to their lifestyle and medication, leading to improved diabetes management. This widespread adoption has contributed to the dominance of self-monitoring devices in the market.

Continuous blood glucose monitoring devices are the fastest-growing segment throughout the forecast period. These devices are gaining traction due to their ability to offer real-time, continuous tracking of glucose levels, providing users with more detailed and accurate information than traditional self-monitoring devices. CGMs help in improving the overall management of diabetes, as they provide data that allows users to monitor their glucose levels throughout the day without needing to perform multiple finger-prick tests. The increased awareness of the benefits of CGMs and technological advancements in their development has made them a preferred choice for many users.

By End-use

The hospitals segment led the market in 2023, contributing 45% of the total market share. Hospitals are primary settings for advanced diabetes care, where blood glucose monitoring devices, including both self-monitoring devices and CGMs, are used to monitor and manage glucose levels in patients. The adoption of these devices in hospitals is driven by the need for accurate and real-time glucose data for managing patients with diabetes and other related conditions. Hospitals also play a vital role in educating patients about the importance of glucose monitoring, making this segment a key area for the growth of blood glucose monitoring devices.

The home care segment is anticipated to be the fastest-growing segment over the forecast period 2024-2032, with more patients choosing to monitor their glucose levels from the comfort of their homes. This segment is increasingly important as more individuals with diabetes prefer the convenience of managing their condition outside clinical settings. Advances in blood glucose monitoring technology, particularly the development of user-friendly devices like CGMs, have contributed to the rise in home care adoption. This trend is driven by the desire for greater control over diabetes management, as well as the convenience and accessibility offered by home monitoring devices.

Blood Glucose Monitoring Device Market Regional Overview

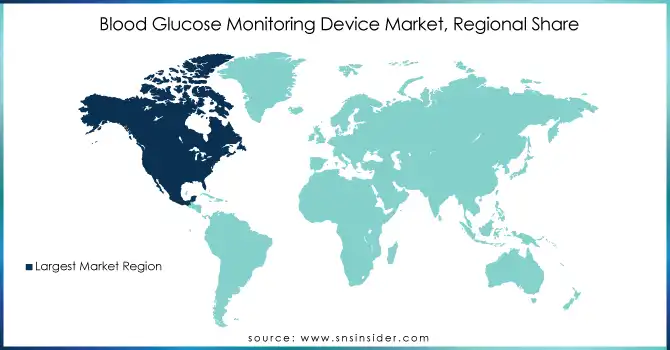

In 2023, the North American region led the blood glucose monitoring device market, accounting for a significant share due to the high prevalence of diabetes and advanced healthcare infrastructure. The United States, in particular, dominates the market owing to the increasing adoption of continuous glucose monitoring systems, government initiatives to promote diabetes awareness, and better reimbursement policies for diabetes-related technologies. The rising number of people with diabetes, combined with strong support from healthcare systems, contributes to North America's dominant market position.

The European market is also substantial, driven by growing awareness and technological advancements in glucose monitoring devices. Countries like Germany, the UK, and France are seeing increased adoption of advanced devices like CGMs and flash glucose monitors. Government-funded healthcare systems in these regions help make glucose monitoring devices more accessible, which further drives market growth.

The Asia-Pacific region is experiencing rapid growth, with the emergence of countries such as China and India. The increasing diabetic population, improving healthcare infrastructure, and growing disposable income in these countries are fueling the demand for blood glucose monitoring devices. Moreover, the adoption of innovative and affordable monitoring solutions is contributing to the expansion of the market in this region.

Need any customization research on Blood Glucose Monitoring Device Market - Enquiry Now

Key Players &Their Products

-

Thermo Fisher Scientific (Patheon)

-

Blood glucose test kits and diagnostic services

-

FreeStyle Libre, FreeStyle Precision Neo

-

Guardian Connect, MiniMed Insulin Pumps with CGM systems

-

F. Hoffmann-La Roche Ltd

-

Accu-Chek Guide, Accu-Chek Instant, Accu-Chek Aviva

-

Ascensia Diabetes Care Holdings AG

-

Contour Next One, Contour Next, Contour XT

-

Dexcom, Inc.

-

Dexcom G6, Dexcom G7 (Continuous glucose monitoring systems)

-

Sanofi

-

Lantus, Apidra (Diabetes management solutions)

-

Novo Nordisk

-

NovoPen, NovoLog (Insulin pens and devices integrated with glucose monitoring)

-

Insulet Corporation

-

Omnipod (Insulin management system with glucose monitoring)

-

Ypsomed Holdings

-

my life Diabetes care (Blood glucose monitoring systems)

-

Glysens Incorporated

-

Glysens Continuous Glucose Monitoring System

-

B. Braun Melsungen

-

Omnilink (Blood glucose meters)

-

Nipro

-

True Metrix (Blood glucose meters)

-

Arkray

-

Glucocard (Blood glucose meters)

-

Prodigy Diabetes Care

-

Prodigy Voice, Prodigy No Coding (Blood glucose meters)

-

Acon Laboratories

-

On-Call (Blood glucose meters)

-

Nova Biomedical

-

StatStrip (Blood glucose meters)

-

Lifescan

-

OneTouch (Blood glucose monitoring system)

Recent Development

In Sept 2024, Abbott launched its over-the-counter continuous glucose monitoring system in the U.S., becoming the second company to offer such a device, following rival Dexcom. This new product allows individuals to monitor their blood sugar levels without a prescription.

In June 2024, Prevounce Health introduced the Pylo GL1-LTE, a clinically validated, cellular-connected remote blood glucose monitoring device. Designed to improve remote patient monitoring (RPM) programs for diabetes management, the device ensures reliable data transmission across the United States.

In May 2024, Dexcom, Inc. launched the Dexcom ONE+, a continuous glucose monitoring (CGM) device designed to track real-time glucose levels for improved diabetes management. Additionally, the company unveiled the Dexcom State of Type 2 Report, highlighting alarming rates of anxiety and depression among individuals with Type 2 diabetes.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 13.49 billion |

| Market Size by 2032 | USD 27.61 Billion |

| CAGR | CAGR of 8.29% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [Self-monitoring Devices (Blood glucose meter, Testing Strips, Lancets), Continuous blood glucose monitoring devices (Sensors, Transmitter & Receiver, Insulin Pumps)] • By End-use [Hospitals, Home care, Diagnostic centers] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific (Patheon), Abbott, Medtronic plc, F. Hoffmann-La Roche Ltd, Ascensia Diabetes Care Holdings AG, Dexcom, Inc., Sanofi, Novo Nordisk, Insulet Corporation, Ypsomed Holdings, Glysens Incorporated, B. Braun Melsungen, Nipro, Arkray, Prodigy Diabetes Care, Acon Laboratories, Nova Biomedical, Lifescan |

| Key Drivers | • Technological Advancements and Rising Awareness Drive Growth in the Blood Glucose Monitoring Device Market |

| Restraints | • High Costs and Limited Accessibility Hampering Market Growth |

Frequently Asked Questions

Ans: North America is the dominant region in the Blood Glucose Monitoring Device market.

Ans: The expensive nature of continuous glucose monitoring systems and other advanced glucose monitoring devices can limit their accessibility, particularly in low-income regions or for uninsured individuals.

Ans: Ongoing technological advancements in glucose monitoring systems, particularly the rise of non-invasive and user-friendly devices are propelling the growth of the blood glucose monitoring device market.

Ans: The blood Glucose Monitoring Device market is estimated at USD 13.49 billion in 2023 and is expected to reach USD 27.61 billion by 2032.

Ans: The estimated compound annual growth rate is 8.29% during the forecast period for the Blood Glucose Monitoring Device market.

Get in Touch