Large And Small-Scale Bioprocessing Market Report Scope & Overview:

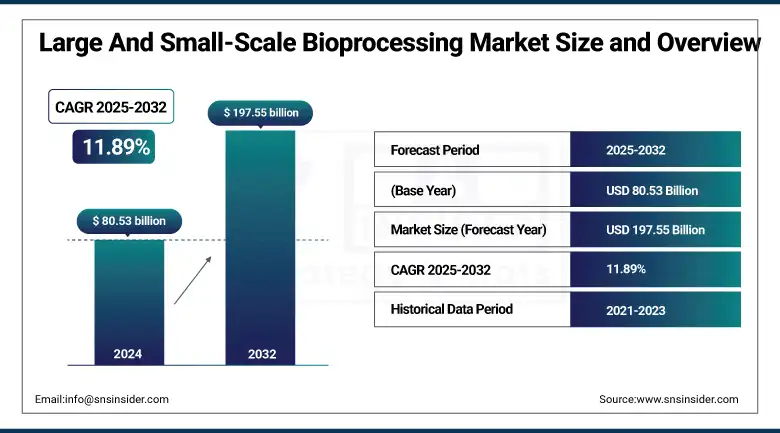

The large and small-scale bioprocessing market size was valued at USD 80.53 billion in 2024 and is expected to reach USD 197.55 billion by 2032, growing at a CAGR of 11.89% over 2025-2032.

The large and small-scale bioprocessing market is rapidly evolving with changing market scenarios and expansion of market scope due to technological advancement, increasing demand for biologics, and a trend shift toward flexible manufacturing. Single-use system use is increasing, particularly in smaller-scale companies, and they are changing process flow, turnaround times, and overall costs.

In March 2024, Sartorius AG unveiled the new modular single-use bioreactor system that has Next-gen features, which facilitates flexible scale-up ranging from 50L to 2,000L, thereby strengthening the company’s large and small-scale bioprocessing market position.

To Get more information On Large And Small-Scale Bioprocessing Market - Request Free Sample Report

Suppliers, on their side, are scaling up biomanufacturing capacity in response to increasing global demand for cell and gene therapies, recombinant proteins, and biosimilars. In 2023, there was more than USD 4.5 billion worth of new bioprocessing facility investment announced, as companies, such as Thermo Fisher, Sartorius, and Cytiva, accelerated production investments. R&D investments have significantly increased with biopharmaceutical companies dedicating 12%–15% of annual revenues to pipeline development and toward the design of a scalable process.

Furthermore, there are accommodating regulatory pathways for continuous manufacturing and single-use technologies, such as the FDA's Emerging Technology Program, expediting innovations. The demand for decentralized manufacturing models and the increasing speed of the clinical delivery timelines are some of the factors boosting the large and small-scale bioprocessing market share and large and small-scale bioprocessing market growth.

For instance, in June 2024, Cytiva introduce AI-powered bioprocess monitoring suite for advanced predictive analytics and process stability. Key developments that are contributing to future in the large and small-scale bioprocessing market trends.

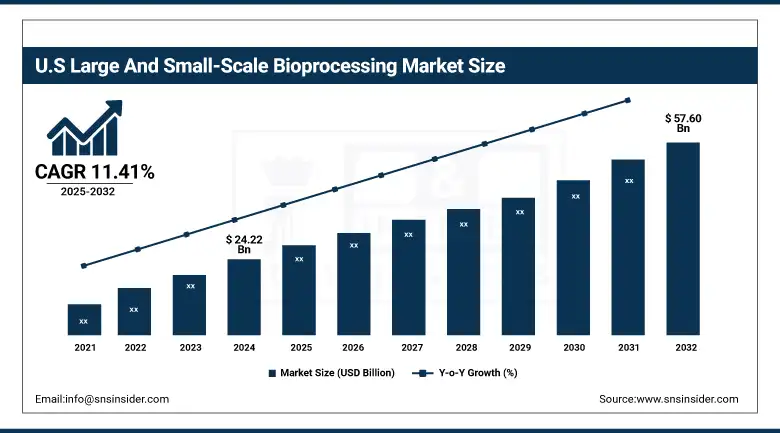

The U.S. large and small-scale bioprocessing market size was valued at USD 24.22 billion in 2024 and is expected to reach USD 57.60 billion by 2032, growing at a CAGR of 11.41% over 2025-2032. The U.S. is the most advanced biopharmaceutical market in the world and has a leading network of biopharmaceutical companies and contract manufacturers, facilitated by efficient regulatory ecosystems and innovation. Canada is also playing a major role, particularly with the progress of biologics manufacturing and the continued expansion of biotech clusters in provinces, such as Ontario and British Columbia. It is a mature and innovation-driven market with strong funding and talent infrastructure.

Market Dynamics:

Drivers:

-

Rising Biologic Demand, Tech Advancements, and Flexible Manufacturing Models Fuel Market Expansion

The large and small-scale bioprocessing market is driven by the surge in global demand for biologics, biosimilars, vaccines, and cell therapies, which are all resulting in significant capacity expansions and process innovations. Biologics represent over 60% of the medications currently in the development pipeline for which demand is increasing for flexible, high-throughput bioprocessing platforms to accelerate the rate of drug development. Upstream and downstream technologies, such as perfusion systems and intensified chromatography are facilitating fast scale-up with high productivity, especially in multiproduct and contract manufacturing environments. The rise in demand is also evident in the expansion of supply chains, as companies, such as ABEC and Repligen scaled up their production of single-use systems to accommodate industry requirements.

Investment volume is on the rise and venture capital in biotech tops USD 25 billion in 2023, with a significant amount funneled toward biomanufacturing scalability. Regulatory drivers, notably, the EMA adaptive pathways and the FDA’s guidance on continuous manufacturing, promote earlier market access. Further, a rise in AI-assisted bioprocess automation and integration of smart sensors is enhancing the success rate and consistency of batches, contributing to overall large and small-scale bioprocessing market growth. Taken together, these trends influence market uptake by facilitating greater flexibility, efficiency, and speed in the entire biomanufacturing lifecycle.

Restraints:

-

Infrastructure Limitations, Workforce Gaps, and Standardization Challenges Propel Market Growth

While the demand is increasing, the large and small-scale bioprocessing market is constrained to a certain extent, such as infrastructure barriers, shortage of skilled workforce, and lack of standardization across facilities, among others. Early-stage and mid-sized companies often find that they do not have the capital or space to commit to fully realized biomanufacturing facilities, leading to delays in tech transfer or product launch timing.

More than 35% of global biomanufacturers, according to industry statistics, have facility capacity limitations and struggle to be productive during peak demand times. Adding to the complexity, there is a global scarcity of trained bioprocess engineers and automation professionals, which interrupts the scalability of end-to-end production. In addition, although there have been regulatory progressions, global GMP requirements vary, and the validation of single-use systems remains inconsistent. Quality assurance is a particular worry in multi-site or outsourced production.

Supply chain fragility, which was revealed during Covid-19, remains, particularly for critical parts, such as bags, tubing, and specialty resins. These challenges impede the smooth enlargement of the large and small-scale bioprocessing market share and require strategic partnership, regulatory harmonization, and infrastructure to respond to bottlenecks.

Segmentation Analysis:

By Scale

Large-scale bioprocessing held the largest share of the market in 2024, primarily driven by the growing preference for high-volume bioprocessing activities in the commercial production of biosimilars and monoclonal antibodies. The increased use of fed-batch and perfusion with larger-scale stainless steel and hybrid reactors supported its dominance. However, pilot-scale bioprocessing was the fastest-growing segment, owing to the increasing usage in R&D, process development, and preclinical manufacturing. The small biotech and academic institutions are making big investments in pilot facilities to cut time-to-clinic and prove early-phase biologics before scaling up production. Affordable modular platforms and single-use systems are also playing a role in the product expansion in developing countries.

By Workflow

The upstream processing accounted for the largest market share in 2024 and was valued at 41.2% of the global large and small-scale bioprocessing market analysis. This has largely been driven by major advancements in cell line optimization, media development, and sensor-based monitoring technologies to maximize yield and cell viability. Growing attention to scalability and speed as well, particularly for cell and gene therapies, continued to push upstream investments. The downstream processing segment is growing the fastest due to mounting pressure to improve purification efficiency for rising upstream titers. Increased requests for viral vector purification, membrane chromatography, and single-use filtration are driving demand for strong downstream workflows.

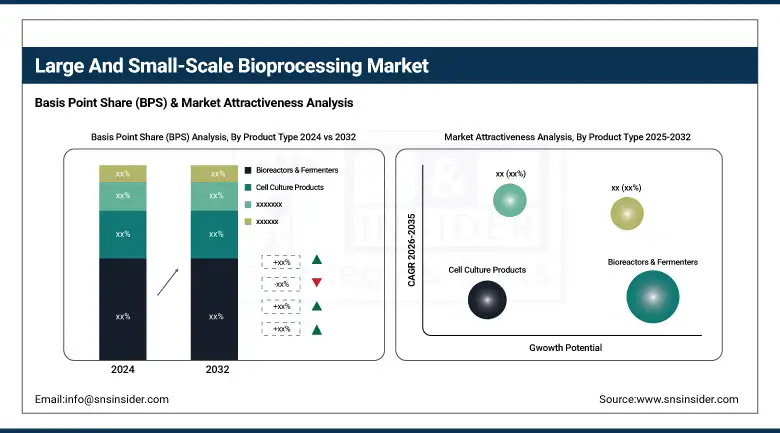

By Product Type

Bioreactors & fermenters accounted for the largest market share of 28.3% in 2024, with widespread adoption among commercial and pilot-scale manufacturing facilities. Their ubiquitous involvement in upstream cell culture and fermentation makes them critical to biologics manufacturing. High utilization was due to innovative technology, such as automated control structures, flexible vessel designs, and scale-down models. Single-use bags and containers are the fastest-growing product type owing to their capability to eliminate cross-contamination and setup and validation times. Their increasing presence in personalized, small batch, and modular facility designs is reshaping the operational field, particularly for emerging biotech and CDMOs.

By Application

In 2024, biopharmaceutical production continued as the largest area of application with 61.5% market share, primarily driven by global demands for monoclonal antibodies, recombinant proteins, vaccines, and gene therapies. Large pharma companies are spreading manufacturing across their footprints to supply the pipeline and commercial demand.

Environmental applications were the fastest-growing, driven by demand for bioprocessing in wastewater treatment, bioremediation, and carbon capture. Increasing environmental regulations and a push for environmentally friendly, microbial-based waste management systems are encouraging investment and innovation, particularly in Asia Pacific and Europe.

By Bioprocessing Type

The batch processing segment held the highest share of the market in 2024, owing to the widespread application of this technology in the production of therapeutic proteins, vaccines, and enzymes on a large scale. Its ease of use and regulatory acceptance make it the most widely employed across both stainless steel and hybrid sites.

On the other hand, continuous processing is the fastest-growing based on the demand for high productivity, smaller operational footprints, and the ability to monitor quality in real time. More and more companies are moving toward continuous upstream perfusion in combination with integrated downstream purification to significantly shorten cycle times, particularly for high-demand biologics, such as viral vectors and mAbs.

By End-Use

In 2024, the large and small-scale bioprocessing market was dominated by the pharmaceutical & biotechnology companies segment, which held 57.1% of the market share. These companies are making enormous bets on scaling infrastructure, personalized therapy pipelines, and in-house manufacturing processes to maintain control of the product. Strategic in-house expansions and the demand for biologics play a major role. Meantime, the fastest growing end-use segment is the bioenergy sector, as the world is focused on renewable bio-oils and circular bioeconomy solutions. Policy requirement and investments on renewable sources as substitute of fossil fuels are leading to rise of attention due to microbial fermentation for production of ethanol and biodiesel in particularly in U.S., Brazil and India.

Regional Analysis:

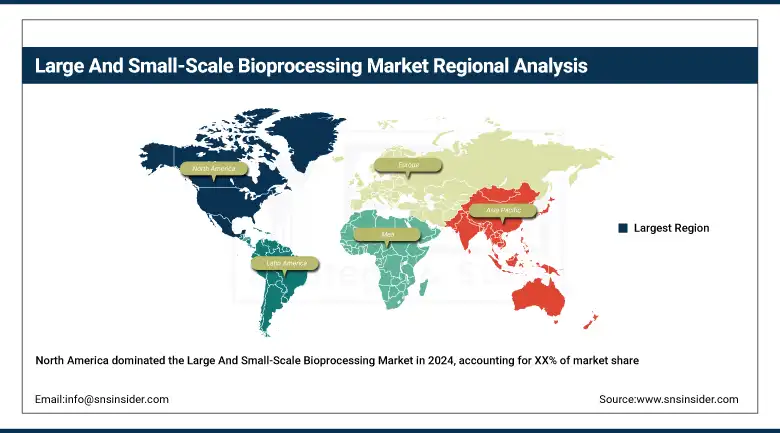

North America was the largest regional large and small-scale bioprocessing market owing to a large number of players in the biotechnology field available here, higher spending on R&D, and high acceptance of single-use technologies. The region is also home to South Korean companies making leaps and bounds in globalization, pushed by leading market ecosystems in China, Japan, and the U.S.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is considered the second leading region, which is supported by strong regulatory support, the continuation in bioprocessing, and government support. Germany is the frontrunner, being home to a large number of biomanufacturing sites and talent. The U.K. and France are driving modular bioproduction technologies and the role of CMOs. Italy and Spain demonstrate increasing demand for biosimilars, and Poland and Russia are low-cost manufacturing hubs. The sub-region of Eastern Europe, Poland, and the Rest of Eastern Europe in particular, has also witnessed very high growth rates as a result of greater investment and exports in biologics. The same region’s coordinated industry policy and investment for sustainability also make it more competitive.

Asia Pacific is projected to be the fastest-growing region in the global large and small-scale bioprocessing market analysis, owing to the growing adoption of biologics, significant patient pool, and growing investments in biomanufacturing facilities. China’s industry overlord is investing heavily in bioprocessing capacity, state-of-the-art fermentation capabilities, and burgeoning biosimilar pipelines. Following India, its low-cost manufacturing environment, fast development of biotech parks, and support by favorable government programs have led to domestic and international CDMO alliances. Japan and South Korea are innovating predominantly in bioreactor and purification technologies, while Australia and ASEAN are experiencing a lot of interest in vaccine production and academic collaboration.

Key Players:

Leading large and small-scale bioprocessing companies in the market include Merck KGaA, Thermo Fisher Scientific, Danaher Corporation (Cytiva), Corning Inc., Sartorius AG, Lonza Group, CESCO Bioengineering, Bio-Process Group, BPC Instruments AB, Eppendorf AG, Getinge AB, PBS Biotech, Bio-Synthesis Inc., Meissner Filtration Products, Entegris, KUHNER AG, ExcellGene SA, Repligen Corporation, Avantor Inc., and CerCell A/S.

Recent Developments:

In April 2025, Thermo Fisher Scientific launched the 5 L DynaDrive single-use bioreactor, which enables seamless scale-up from benchtop to 5,000 L, significantly speeding up process development and reducing cost per run. This innovation enhances efficiency across early-phase and commercial-scale manufacturing platforms.

In October 2024, Sartorius introduced enhancements to its single-use bioprocessing portfolio, including more efficient bioreactors and filtration systems designed to streamline workflows and improve scalability for both pilot and large-scale operations.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 80.53 billion |

| Market Size by 2032 | USD 197.55 billion |

| CAGR | CAGR of 11.89% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Scale (Large-Scale Bioprocessing, Small-Scale Bioprocessing, and Pilot-Scale Bioprocessing) • By Workflow (Upstream Processing, Fermentation, and Downstream Processing) • By Product Type (Bioreactors & Fermenters, Cell Culture Products, Filtration Systems, Single-Use Bags & Containers, Bioprocessing Accessories, and Others [integrated software, control systems, mixers]) • By Application (Biopharmaceutical Production, Food & Beverage Fermentation, Biofuels, Agricultural Biotechnology, Environmental Applications, and Specialty Industrial Chemicals) • By Bioprocessing Type (Batch Processing, Fed-Batch [Semi-Continuous] Processing, and Continuous Processing) • By End-Use (Pharmaceutical & Biotechnology Companies, Food & Beverage Industry, Agriculture & Animal Health, Bioenergy Sector, Water and Wastewater Treatment) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Merck KGaA, Thermo Fisher Scientific, Danaher Corporation (Cytiva), Corning Inc., Sartorius AG, Lonza Group, CESCO Bioengineering, Bio-Process Group, BPC Instruments AB, Eppendorf AG, Getinge AB, PBS Biotech, Bio-Synthesis Inc., Meissner Filtration Products, Entegris, KUHNER AG, ExcellGene SA, Repligen Corporation, Avantor Inc., and CerCell A/S. |

Frequently Asked Questions

Ans: Contract Manufacturing Organizations (CMOs) enable scalability and flexibility by offering outsourced bioprocessing services, especially to small and mid-sized biotech firms.

Ans: North America leads due to advanced biomanufacturing infrastructure, while Asia-Pacific is the fastest-growing region driven by cost-effective contract manufacturing and government support.

Ans: Rising demand for personalized medicine, single-use technologies, and increased biotech startup activity are key growth drivers in the small-scale bioprocessing segment.

Ans: Large-scale systems cater to high-volume commercial production, while small-scale setups dominate R&D and early-phase manufacturing with faster turnaround and lower capital investment.

Ans: The global large and small-scale bioprocessing market was valued at over USD 80.53 billion in 2024, with continued growth projected through 2032. Increasing demand for biologics and flexible manufacturing models fuels this expansion.

Get in Touch