Silver Wound Dressing Market Report Scope & Overview:

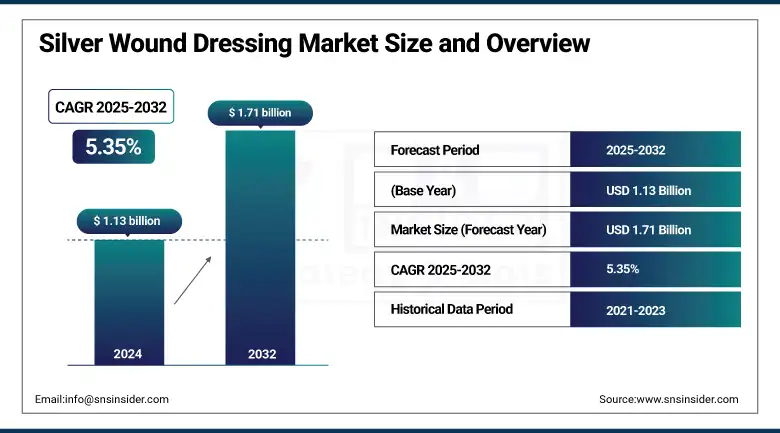

The silver wound dressing market size was valued at USD 1.13 billion in 2024 and is expected to reach USD 1.71 billion by 2032, growing at a CAGR of 5.35% over 2025-2032.

The increasing prevalence of chronic diseases, including diabetes, venous leg ulcers, and pressure sores, has resulted in high demand for advanced wound care products, which in turn, is driving the silver wound dressing market growth. There are over 537 million adults globally living with diabetes, and 25–30 of them are at risk of developing diabetic foot ulcers, a main driver for the usage of silver dressings. Pressure ulcers alone impact nearly 2.5 million people annually in the U.S., enhancing the need for antimicrobial wound management. Furthermore, more than 11 million burn cases need medical care annually, several of which are treated by silver-based dressings, which can control the infections.

To Get more information On Silver Wound Dressing Market - Request Free Sample Report

More than 25 silver-containing wound care devices have obtained FDA 510(k) clearance, and silver dressings are recommended in many clinical guidelines for wound care at the national level for chronic wounds. R&D companion shows that investment in new technologies continues to increase, with leading players investing in the order of 8–10% of their annual budget in developments for nanocrystalline silver/silver-plated fibers/hydrofiber matrices. Smart wound dressings, including sensor-embedded wound dressings to detect bacteria in real time and monitor moisture, have also led to the adoption, particularly across post-operative and high-risk patients. Increasing outpatient surgeries, home healthcare programs, and favorable reimbursement policies, particularly in the Americas and Europe, are also enhancing the demand for consumables, thus augmenting the supply chain and making products accessible.

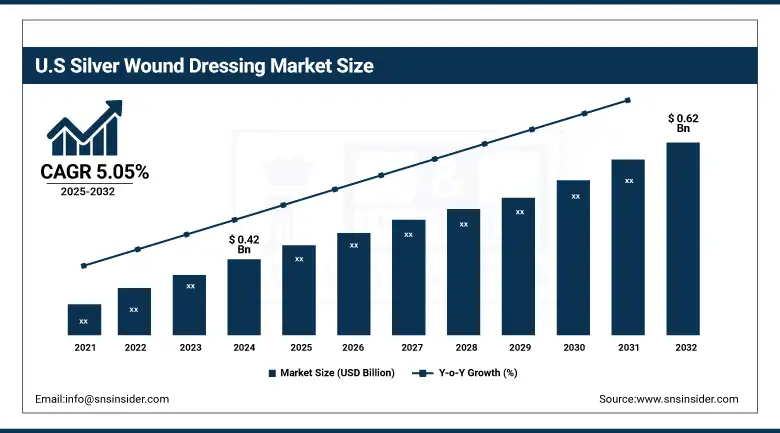

The U.S. silver wound dressing market size was valued at USD 0.42 billion in 2024 and is expected to reach USD 0.62 billion by 2032, growing at a CAGR of 5.05% over 2025-2032. The U.S. is the highest contributor, with more than 37.3 million patients with diabetes and 6.5 million patients with chronic wounds each year. Moreover, the growing prevalence of nanocrystalline dressings during post-operative care, coupled with the existence of major participants that include 3M, Medline, and Cardinal Health, underscores its dominance. Canada is growing fast, albeit on a much smaller scale, attributed to upward surgical trends and increased awareness of antimicrobial resistance.

Market Dynamics:

Drivers:

-

Growth of the Silver Wound Dressing Market, Supported by Rising Demand, Innovation, and Regulatory Backing

The global silver wound dressing market is growing due to increasing awareness about antimicrobial resistance, escalating burden of post-operative wound infections, and the rising trend toward the shift of healthcare from hospitals toward home care. Healthcare-associated infections (HAIs) are prevalent in 7% of admissions in high-income countries and 10% in low and middle-income countries, leading to a market need for silver antiseptic dressings. On the supply side, the response is strong, as companies are investing in innovations, such as silver-releasing foams and films, which can reduce microbial load over extended periods. Increasing use is being made of advanced polymer composites containing silver, which offer improved levels of exudate management and a healing environment.

Regulatory authorities, such as the EMA and the FDA, are fast-tracking approvals and issuing revised guidelines incorporating the use of silver dressings in post-operative care protocols. R&D spending is on the rise too, and some of the largest manufacturers claim to have invested around 10% of their annual revenues in wound care research, with a particular focus on biocompatible silver nanoparticles and combination anti-microbial therapies. All of these factors are creating a dynamic, innovation-based market with meaningful clinical and commercial relevance.

Restraints:

-

Key Barriers Limiting the Growth of the Silver Wound Dressing Market Include Safety Concerns, Pricing Pressures, and Clinical Hesitancy

The silver wound dressing market growth is hindered due to several restraints, such as cytotoxicity issues and the high cost of advanced dressings. High silver ion concentrations can cause delayed epithelialization and cytotoxicity in some patients, particularly children and immunocompromised patients. These concerns of safety have led clinicians to use non-silver types of dressing, which have globally taken the place of silver dressings in situations where there is little risk of infection. Moreover, the costs associated with nanocrystalline and hydrofiber silver dressings, which are expensive to produce, have resulted in these products being priced at a premium, which would likely pose a budgetary issue for publicly funded health systems and slow adoption by low-cost settings.

From a regulatory perspective, not all countries offer aligned standards for such dressings, and this may result in a longer time to approval and time to reimbursement inclusion. Furthermore, mixed clinical protocols among institutions on the indication of silver dressings and the way of silver application decreased its use in common practices. Environmental issues relating to the disposal of silver nanoparticles are also becoming apparent, and some research has demonstrated the ecotoxicological impact of silver waste, leading to new regulation and legislation, which may impact supply chains and production choices.

Segmentation Analysis:

By Product Type

Nanocrystalline silver dressings dominated in 2024, with over 32.4% of the revenue. The advantage of these dressings is their long-lasting silver ion release, with a broad-spectrum antimicrobial action, and the ability to treat chronic and infected wounds. They are highly clinically used in hospitals, especially for burns and ulcers.

The fastest growing segment is silver hydrogel/hydrofiber dressings, powered by their enhanced ability for the retention of moisture, ease of use, and less cytotoxicity. These dressings are also getting increasing attention in outpatient and home care settings, such as moderate to heavily exuding wounds. This demand is upheld by a combination of other therapies and the increasing preference for dressings which offer antimicrobial protection alongside the promotion of ideal wound hydration, and the acceleration in healing rates of both acute and chronic wounds.

Table: Product Type Penetration by Care Setting (2024)

|

Product Type |

Hospitals & Clinics |

Home Healthcare |

Ambulatory Centers |

Burn Units |

|

Silver Foam Dressings |

High |

Medium |

Medium |

High |

|

Nanocrystalline Silver Dressings |

High |

Low |

Medium |

Very High |

|

Silver Hydrogel Dressings |

Medium |

High |

Low |

Medium |

|

Silver Nitrate Dressings |

Medium |

Low |

Low |

High |

By Wound Type

Chronic Wounds was the most dominant segment in 2024 and accounted for 58.7% of the silver wound dressing market share. This is due to the increasing prevalence of diabetic foot ulcers, venous leg ulcers, and pressure ulcers that need time-consuming management with modern silver-containing dressings. This segment’s dominance is, in turn, supported by the growing geriatric population and rising incidence of lifestyle diseases.

Acute Wounds, on the other hand, is the fastest growing among the segments, driven by an increase in traumatic injuries, post-surgical wound care, and burn cases. Enhanced emphasis on infection prevention in the early stages of wound healing and the rising prevalence of silver dressings for use on surgical cuts and minor cuts are fostering demand. Additionally, the rapid introduction of quick-acting silver formulations and the widening access to emergency care settings have furthered the use of silver dressings in the acute wound.

By Indication

By 2024, ulcers had become the leading segment, with a global silver wound dressing market share of 35.1%. High incidence of diabetic foot ulcers, particularly among obese and old age people, is leading to the demand for antimicrobial wound care products, such as silver dressings. These products are being used more and more in chronic wound care protocols because of their infection prevention and granulation acceleration properties.

Concurrently, skin grafts is the fastest-growing indication, and is witnessing an augmented demand in burn and reconstructive surgeons. Silver dressings are important in preventing infection and maintaining graft take. Sensitive post-graft skin and moist wound healing can be achieved and these factors contribute to the product expansion into trauma centers and specialized plastic surgery departments.

By End-User

Hospitals & clinics dominated the market in 2024 with a silver wound dressing market share of 46.5% attributed to their availability of sophisticated wound care technologies, well-equipped clinicians, and large patient population with chronic and post-operative wounds. Institutional procurement and insurance coverage also serve to promote adoption.

Home healthcare settings are also seeing the fastest growth, as a result of rising demand for home care and aging populations. Patients with chronic wounds, especially those who need long-term dressing changes, prefer silver-containing products for fewer dressing changes and better infection control. An improved home care infrastructure, patient education, and the ease of self-application dressings are major factors in encouraging demand. Furthermore, manufacturer and home healthcare provider collaborations are increasing the availability and compliance of products.

By Distribution Channel

Offline channels accounted for 68.9% of revenue in 2024. Hospital pharmacies, retail pharmacies, and wholesalers are still the main sourcing outlets especially for institutional and emergency procurement. Healthcare facility bulk buying and clinician preference for in-person product validation contribute to the strength of offline channels.

Nonetheless, online channels are the fastest expanding distribution mode propelled by surging internet penetration, growing consumer knowledge, and availability of direct-to-door shipping services. Percentage of patients and caregivers looking to purchase online wound care, and more advanced products for use at home for chronic treatment. Increased penetration of digital healthcare platforms, e-pharmacies, and manufacturer-direct sales are rendering silver wound dressings more accessible. The surge of sales is also being propelled by subscription-based services and the company's strategy of pairing their dressings with telemedicine visits.

Regional Analysis:

North America dominated the silver wound dressing market analysis in 2024, driven by the well-established modern healthcare system, high surgical volumes, and prevalence of chronic diseases. The region's leadership position is primarily attributed to robust reimbursement policies, swift regulatory approvals, and the growing acceptance of advanced wound care products in hospitals as well as in outpatient settings.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe ranks as the second fastest-growing region in 2024, reflecting rapidly aging populations and robust public health systems. Sophisticated reimbursement systems and treatment guidelines in, for instance, Germany, France, and the U.K. facilitate the use of silver-based products, especially for pressure ulcers and diabetic foot care. Germany is the largest market in the region, and a high density of hospitals and stringent regulatory requirements to ensure the usage of CE-marked silver-based wound products drive the market in this country. Silver-based dressings have been used extensively within the French healthcare system as part of a concerted effort by the government to drive down surgical site infections in hospitals. Increasing investment towards wound care innovation and the adoption of smart dressing technologies within the U.K. also drives the regional growth.

Asia Pacific is estimated to grow at the highest CAGR in the silver wound dressing market trends during 2025-2032 due to the high prevalence of diabetes, the growing number of trauma cases, and the increasing healthcare expenditure. China is the largest contributing factor with over 140 million diabetic population, and increasing urbanization and surgical volumes. Government efforts to decrease hospital-acquired infection risk are also propelling the demand for silver dressings among tertiary care centers. There is also strong growth in India, where there are high rates of chronic wounds and burns, and more R&D spending and local manufacturing. On the other hand, in Japan, wound care for the elderly is emphasized, and the introduction of technology into the traditional dressing method has become a topic of discussion. Increasing medical tourism and private hospital chains in ASEAN countries and Australia are also fueling the silver wound dressing market growth.

Table: Regulatory Approvals of Silver-Based Dressings (2022–2024)

|

Year |

Product Name |

Company |

Approval Body |

Indication |

|

2024 |

Aquacel Ag+ Extra |

ConvaTec |

FDA (510k) |

Chronic and surgical wounds |

|

2024 |

ALLEVYN Life Ag |

Smith+Nephew |

CE Mark |

Pressure ulcers |

|

2023 |

Biatain Silicone Ag |

Coloplast |

FDA (510k) |

Exuding wounds |

|

2023 |

Mepilex Border Ag |

Mölnlycke |

TGA (Australia) |

Burns and donor sites |

|

2022 |

Silverlon Burn Contact |

Argentum Medical |

FDA |

Partial-thickness burns |

Key Players:

Leading silver wound dressing companies operating in the market include 3M Company, Smith+Nephew plc, Mölnlycke Health Care AB, URGO Medical, MedWay Group, ConvaTec Group plc, Coloplast A/S, Medline Industries LP, Cardinal Health Inc., PAUL HARTMANN AG, Datt Mediproducts Pvt. Ltd., Advanced Medical Solutions Group plc, Bravida Medical, B. Braun Melsungen AG, DermaRite Industries LLC, Integra LifeSciences Corporation, Scapa Group Ltd., Essity Medical Solutions, Hollister Incorporated, and Ferris Manufacturing Corporation.

Recent Developments:

In April 2024, Smith+Nephew announced the expansion of its ALLEVYN Life Foam Dressings product line with enhanced silver antimicrobial variants, aimed at improving exudate management and reducing infection rates in chronic wounds, particularly for diabetic foot ulcers and pressure injuries.

In January 2024, Convatec launched its new Aquacel Ag+ Extra silver dressing in global markets, featuring enhanced Hydrofiber technology and ionic silver for superior bacterial biofilm management, targeting hospital-acquired wound infections.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.13 billion |

| Market Size by 2032 | USD 1.71 billion |

| CAGR | CAGR of 5.35% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type [Silver Foam Dressings, Nanocrystalline Silver Dressings, Silver Alginate Dressings, Silver Hydrogel/Hydrofiber Dressings, Silver Plated Nylon Fiber Dressings, Silver Nitrate Dressings, Others (Silver Sulfadiazine Creams & Ointments, Silver-coated Films, Silver-impregnated Non-woven Dressings)] • By Wound Type [Chronic Wounds, Acute Wounds] • By Indication [Surgical Wounds, Burns, Ulcers, Lacerations and Cuts, Skin Grafts, Other Indications (Donor Site Wounds, Radiation-induced Skin Injuries, Infected Wounds)] • By End User [Hospitals & Clinics, Ambulatory Surgical Centers, Home Healthcare Settings, Others (Long-term Care Facilities [Nursing Homes], Military & Emergency Medical Services, Burn Units & Specialized Wound Care Centers)] • By Distribution Channel [Offline (Hospital Pharmacies, Retail Pharmacies), Online (E-commerce Platforms, Direct Company Websites)] |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | 3M Company, Smith+Nephew plc, Mölnlycke Health Care AB, URGO Medical, MedWay Group, ConvaTec Group plc, Coloplast A/S, Medline Industries LP, Cardinal Health Inc., PAUL HARTMANN AG, Datt Mediproducts Pvt. Ltd., Advanced Medical Solutions Group plc, Bravida Medical, B. Braun Melsungen AG, DermaRite Industries LLC, Integra LifeSciences Corporation, Scapa Group Ltd., Essity Medical Solutions, Hollister Incorporated, and Ferris Manufacturing Corporation. |

Frequently Asked Questions

Ans: Companies are investing significantly in nanotechnology, smart sensor-integrated dressings, and biocompatible silver formulations to enhance effectiveness and meet evolving clinical needs.

Ans: Hospitals & clinics dominate due to high patient volumes and advanced wound care protocols, though home healthcare is emerging as the fastest-growing segment.

Ans: Rising incidence of chronic wounds, increased surgical procedures, growing awareness of infection control, and technological advancements in silver-based materials are major growth drivers.

Ans: Nanocrystalline silver dressings, silver foam dressings, and silver alginate dressings are among the most commonly used due to their sustained silver ion release and moisture management properties.

Ans: Silver wound dressings offer broad-spectrum antimicrobial activity, reduce infection risk, and promote faster healing, especially in chronic and surgical wounds.

Get in Touch