Linear Low-Density Polyethylene (LLDPE) Market Report Scope & Overview

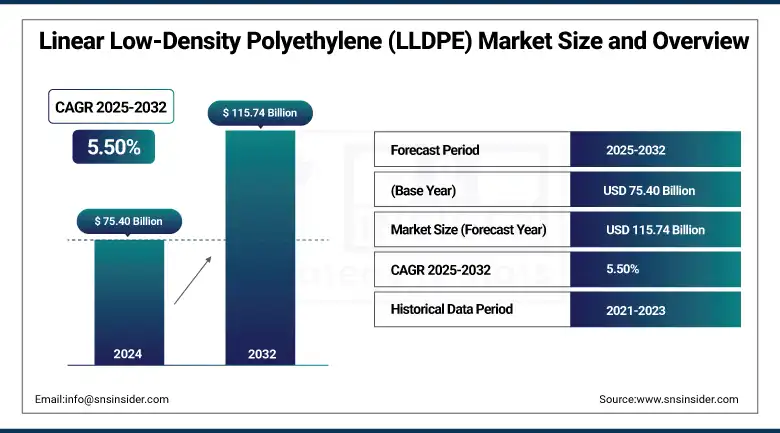

The Linear Low-Density Polyethylene (LLDPE) market size was USD 75.40 billion in 2024 and is expected to reach USD 115.74 billion by 2032, growing at a CAGR of 5.50% over the forecast period of 2025-2032.

Linear low-density polyethylene (LLDPE) market analysis indicates that the growing demand for flexible packaging with LLDPE is a key factor driving the market's expansion. Their features, including cost-effectiveness, lightweight, and convenience, provide ample growth opportunities in sectors such as food and beverages, pharmaceuticals, and consumer goods. Given LLDPE's high tensile strength, flexibility, and puncture resistance, it is an ideal flexible packaging material. Consumer preference trend for portable and convenient packaging solutions is encouraging manufacturers to convert to LLDPE from conventional packaging and wraps and more pouches, which drives the linear low-density polyethylene (LLDPE) market growth.

To Get more information On Linear Low-Density Polyethylene (LLDPE) Market - Request Free Sample Report

The US Census Bureau’s North American Industry Classification System (NAICS) industry code 326112 covers establishments mainly involved in converting plastic resins into plastic packaging (flexible) film and packaging sheets. This category consists of manufacturers who process flexible plastic packaging raw materials, which is one of the major applications of LLDPE.

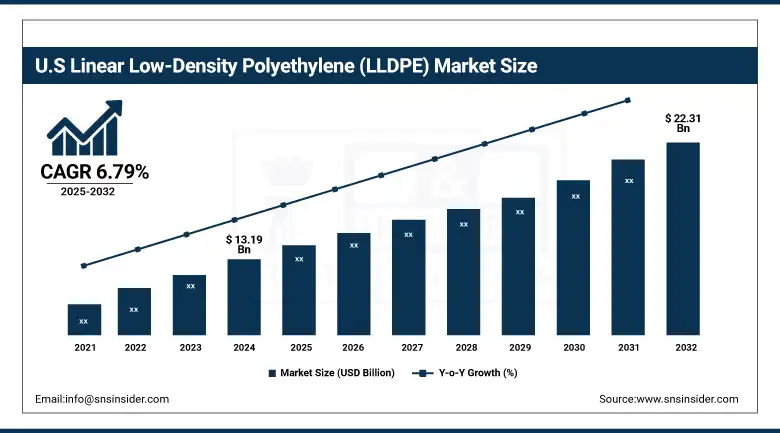

U.S Linear Low-Density Polyethylene (LLDPE) market size was USD 13.19 billion in 2024 and is expected to reach USD 22.31 billion by 2032 and grow at a CAGR of 6.79% over the forecast period of 2025-2032. It is owing to the availability of a well-developed petrochemical industry, which has higher availability of raw materials, heading towards diversification among end-use industries. The U.S. has an experienced petrochemical industry and abundant ethylene and natural gas supplies, important feedstocks for the LLDPE industry. This comes with a benefit in the form of mass production and price competitiveness.

Market Dynamics

Drivers

-

Growth in the automotive industry drives the market growth.

The lightweight and tough nature of this market segment, along with the cost-effective properties of LLDPE, make it suitable for automotive applications such as interior components, exterior trim, bumpers, and under-the-hood parts. With increasing pressure on automakers to enhance fuel economy and lower weight, LLDPE has increasingly become prized for its ability to offer lightweight options without sacrificing strength and durability. Furthermore, the chemical resistance and flexibility of LLDPE allow you to utilize it in parts subject to conditions like heat and moisture. The growing popularity of electric vehicles (EVs) and the emphasis on environmentally friendly solutions in the automotive market are also expected to increase the uptake of LLDPE due to its recyclability and contribution toward sustainability targets.

The U.S. Bureau of Labor Statistics (BLS) tends to mean, rather precisely, that employment in the motor vehicle manufacturing sector is expected to increase by 5.8% over the 2023–2033 decade. The growing production of electric vehicles (EVs), along with the demand for lightweight materials such as LLDPE to improve vehicle performance and efficiency, will drive the growth of LLDPE for EV applications in the global automotive market over the coming years.

Furthermore, motor vehicles and parts manufacturing production and nonsupervisory workers have set the pace in average hourly earnings, increasing to USD 31.84 in January 2025, suggesting strength in that sector as well.

Restrain

-

High energy consumption in production may hamper the market growth.

One of the major factors that can restrain market growth is the high energy consumption required for the production of linear low-density polyethylene (LLDPE). LLDPE is produced by polymerizing ethylene at low temperatures and pressure with the help of specialized catalysts, thereby consuming lots of energy, especially in large-scale industrial applications. The energy-intensive nature of this not only raises the overall cost of production but also contributes to an increased level of greenhouse gas emissions. Producers could see increasing compliance costs and operational limitations as energy efficiency standards and carbon emissions limits are tightened across the world by governments and regulatory bodies.

Opportunities

-

The rising use of agricultural films creates opportunities in the market.

The global demand for high-performance plastic films has been high and growing due to the changing global agricultural practices towards efficiency and sustainability, such as mulch films, greenhouse covers, silage wraps, and irrigation tubing, among others. Because of its high flexibility, strength, puncture resistance, and UV stability, this is one of the most preferred polymers in these applications (LLDPE). These characteristics assist in increasing the production of crops, minimizing the loss of water to evaporation, depressing the growth of weeds, and shielding crops from pressing environmental circumstances. Also, against the backdrop of the growing focus on food security and climate resilience, several countries, especially in Asia-Pacific, Latin America, and Africa, are investing more money to modernize agricultural infrastructure to increase the linear low-density polyethylene (LLDPE) market trends.

In 2025, ExxonMobil began test operations at its USD 10 billion Huizhou petrochemical complex in Guangdong province, China. It has a 1.6 million tons per year steam cracker and multiple polyethylene production units, including two LLDPE units with a total annual capacity of 1.2 million tons. At the complex, the first on-spec LLDPE pellets were produced in early February 2025

Segmentation Analysis

By Process Type

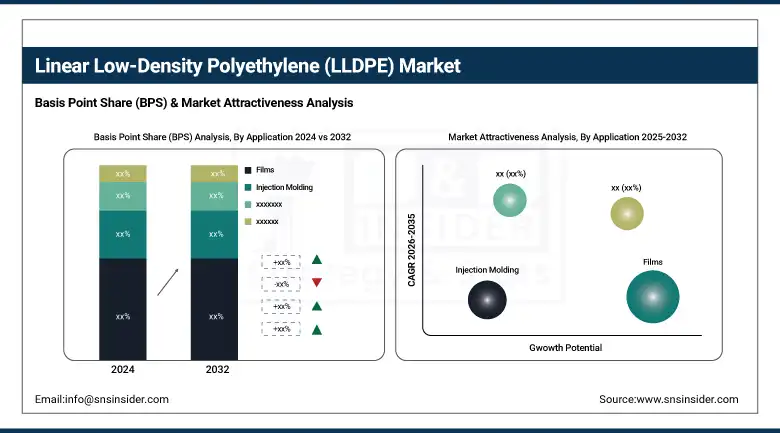

Gas Phase held the largest Linear Low-Density Polyethylene (LLDPE) market share, around 38%, in 2024. It is due to high operational efficiencies and is cost-effective and environmentally friendly. In this process, gaseous monomers (usually ethylene with alpha-olefins) are polymerized in a gas-fluidized bed reactor at low pressure and moderate temperature (150–250 °C). A major benefit is the precise control it offers over molecular weight distribution and comonomer content, both critical to the mechanical strength and flexibility of the finished LLDPE resins. Additionally, the gas phase technology needs lower capital investment and energy consumption than the other methods, e.g., slurry or solution processes, making it an economically attractive technology for manufacturers.

Slurry Loop held a significant Linear Low-Density Polyethylene (LLDPE) market share, owing to the capability to produce quality nature of polymer items with a wide scope of molecular structures. The slurry loop measure is extended to account for the largest offer in the market for linear low-density polyethylene (LLDPE). Here, monomers comprise a slurry phase, and polymerization is carried out in a liquid-phase system under high pressure with a high level of dispersion. Its versatility to produce LLDPE resins with a broad density and property range for a wide range of applications, including films, containers, and injection-molded products, is a key reason for its strength in the marketplace.

By Application

The film held the largest market share, around 48%, in 2024. It is owing to the growing demand from packaging applications triggered growth in different industries. LLDPE films are preferred for their superior combination of flexibility, strength, and durability, an essential property in packaging materials. They are suitable for food packaging, agricultural films, and protective wraps, with a stiffness that can provide good resistance to puncture, tear, and stretch. Moreover, with the growth of e-commerce, the demand for economical and lightweight solutions increases, which also plays a vital part in growing the market for LLDPE films.

Rotomolding holds a significant market share in the Linear Low-Density Polyethylene (LLDPE) market owing to its majorly demanded application of manufacturing durable, light-weight, and cost-effective products. Rotomolding is a process for heating plastic resin in a mold that is rotated on two axes perpendicular to each other to allow the resin to melt and cover the inside of the mold evenly. It produces hollow, repetitive, and rigid products that are commonly used in the automobile, industrial, and packaging industries. Rotomolding is especially appealing due to its ability to make complex shapes with a good surface finish and consistent thickness, providing great versatility over a large number of product choices, from storage tanks to playground equipment and automotive components.

Regional Analysis

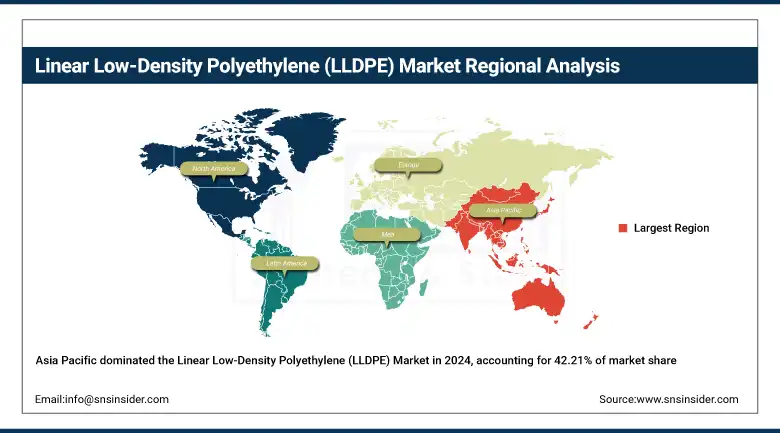

Asia Pacific held the largest market share, around 42.21%, in 2024. It is in demand for flexible packaging, agricultural films, and construction materials. The population and urbanization growth in nations like China, India, and Southeast Asia have considerably increased the demand for packaged food, consumer goods, and infrastructure products, which are primarily dependent on LLDPE. In addition, several major petrochemical and polymer production centers are located in Asia Pacific, taking advantage of low-cost raw materials, low-cost manufacturing, and government assistance for industrial expansion. Moreover, Linear Low-Density Polyethylene (LLDPE) Companies focused on rising investments in agriculture and construction, along with the presence of prominent packaging and automotive sectors, will drive a further push towards LLDPE demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

In September 2024, SABIC launched a certified low-carbon product portfolio based on the company's ambition to achieve carbon neutrality by 2050. Methanol from captured CO₂ fed to upstream processes was the first product developed, leading to lower reliance on traditional feedstocks and a lower carbon footprint of the product.

North America linear low-density polyethylene market held a significant market share and is the fastest-growing segment in the forecast period. It is owing to the high availability of raw material, strong industrial base, developed infrastructure for manufacturing, and high demand from end-use industries. The abundance of ethylene and natural gas, which are significant LLDPE feedstocks, reinforces the strong petrochemical industry in the region, especially in the US. It helps to propose large-scale manufacturing and low-cost operation.

The beneficial application of the In different sectors, such as packaging, automotive, construction, agriculture, etc., of the country, LLDPE is used for films and wraps in packaging due to its flexibility and toughness, which comes in handy with the increased demand in e-commerce and food packaging

Europe held a significant market share in the forecast period. It is due to industrial base, high technology penetration, and rising need for sustainable packaging solutions. This dominance is due to the highly mature manufacturing infrastructure in the region and the high consumption of LLDPE in various sectors such as packaging, automotive, and construction. LLDPE recyclability and versatility make it a material of choice for the packaging industry against the backdrop of increasing consumer and regulatory demand for sustainable solutions, in which Europe is taking the lead by driving sustainability efforts.

Key Players

ExxonMobil, LyondellBasell, SABIC, Dow, Borealis, INEOS, Reliance Industries, China Petrochemical Corporation (Sinopec), Braskem, Formosa Plastics, and others.

Recent Development:

-

In 2024, SABIC launched a new, more sustainable series of LLDPE products targeting the manufacturing carbon footprint. This effort is aimed at helping customers and the value chain achieve their sustainability targets and gain access to lower-carbon-footprint products.

-

In Sept 2024, IOCL chose Univation's UNIPOL PE Process Technology for a new line to be built at its Paradip Petrochemical Complex in India. The plant is expected to have the capability to deliver 650,000 tons per annum of polyethylene and be capable of producing LLDPE and high-density polyethylene (HDPE) products.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 75.40 billion |

| Market Size by 2032 | USD 115.74 Billion |

| CAGR | CAGR of5.50% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Process Type (Gas Phase, Solution Phase, Slurry Loop • By Application Application (Films, Injection Molding, Rotomolding, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ExxonMobil, LyondellBasell, SABIC, Dow, Borealis, INEOS, Reliance Industries, China Petrochemical Corporation (Sinopec), Braskem, Formosa Plastics |

Frequently Asked Questions

Ans: Asia Pacific led the Linear Low-Density Polyethylene (LLDPE) Market in the region with the highest revenue share in 2024.

Ans: Growth in the automotive industry drives the market growth.

Ans: Gas Phase will grow rapidly in the Linear Low-Density Polyethylene (LLDPE) Market from 2025 to 2032.

Ans: The expected CAGR of the global Linear Low-Density Polyethylene (LLDPE) Market during the forecast period is 5.50%

Ans: The Linear Low-Density Polyethylene (LLDPE) Market was valued at USD 75.40 billion in 2024.

Get in Touch