Pulp and Paper Market Report Scope & Overview:

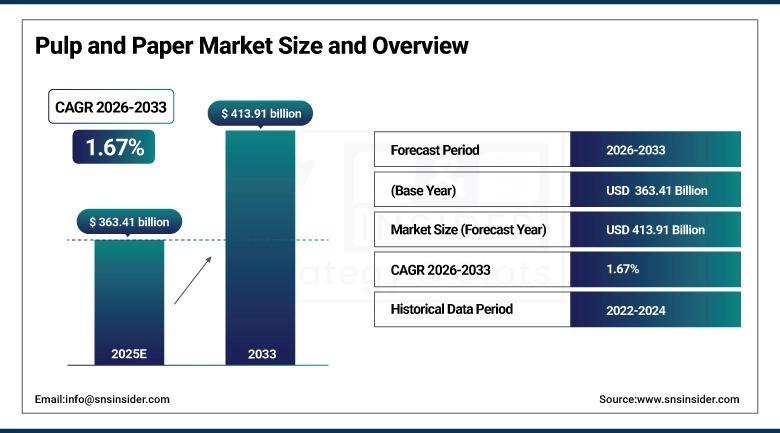

The Pulp and Paper Market was valued at USD 363.41 Billion in 2025 and is expected to reach USD 413.91 Billion by 2035, growing at a CAGR of 1.67% from 2026–2035.

Pulp and paper are one of the world's largest and most capital-intensive manufacturing industries, producing the materials that underpin global commerce, communication, packaging, hygiene, and education. The industry processes wood fiber, recycled paper, and agricultural residues into a spectrum of products from tissue and toilet paper through corrugated containerboard for e-commerce shipping through premium coated printing papers and specialty technical papers for filtration, food packaging, and medical applications. The market is undergoing a structural transition from a graphic paper industry toward a packaging-led industry. The long-term decline in newspaper, magazine, and office printing paper demand from digital substitution is being more than offset by packaging volume growth from e-commerce logistics, food service, and the broader sustainability-driven shift from plastic packaging to paper-based alternatives. The incorporation of recycled fibers into packaging is rising due to mandatory minimum recycled content levels imposed on packaging material by the company sustainability initiatives and EPR regulations. Tissue papers continue to be sturdy. Health consciousness instigated by the pandemic will result in a sustained increase in tissue paper usage per capita across several emerging markets.

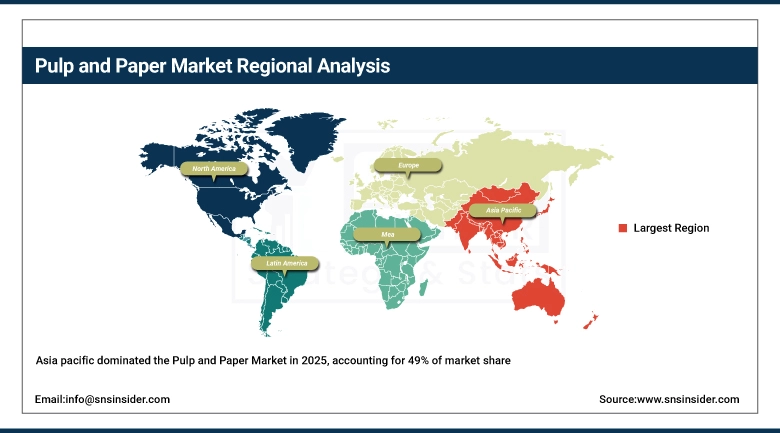

Asia Pacific was responsible for about 49% of the global pulp and paper market revenues in 2025. The Asia Pacific's market share is attributable to China being the largest producer and consumer of paper globally, coupled with the growth in the production capacity of Indonesia, India, and Vietnam due to their fast-growing economies.

Market Size and Forecast

-

Market Size in 2026E: USD 369.48 Billion

-

Market Size by 2035: USD 413.91 Billion

-

CAGR: 1.67% from 2026 to 2035

-

Fastest Growing Segment: Specialty Paper and Recycled Fiber Processing

-

Largest Region: Asia Pacific

To Get more information on Pulp and Paper Market - Request Free Sample Report

Pulp and Paper Market Trends

-

The expansion of e-commerce will continue to create strong demand for corrugated containerboard and kraft paper packaging, since the change from brick-and-mortar to online purchasing replaces the former single-use plastic bags in stores with one-for-one cardboard packages in shipments.

-

The trend toward regulation of plastic packaging use in favor of paper-based solutions in the EU, UK, India, and increasing Asia Pacific creates structural demand for paper-based flexible packaging and molded fiber packaging in food and consumer applications.

-

Recycled fiber content targets mandated by corporate sustainability commitments and Extended Producer Responsibility regulations are increasing demand for recovered paper feedstock and for capital investment in de-inking and recycled fiber processing capacity.

-

Specialty paper growth in filtration, food packaging, medical packaging, and technical paper applications is outperforming the broader market as these high-value product categories face no direct digital substitute and benefit from both regulatory and consumer quality requirements.

-

Kraft pulp price volatility driven by weather events affecting South American eucalyptus plantations, shipping disruptions, and energy cost fluctuations continues to create margin uncertainty for paper manufacturers who depend on purchased pulp rather than integrated upstream forestry assets.

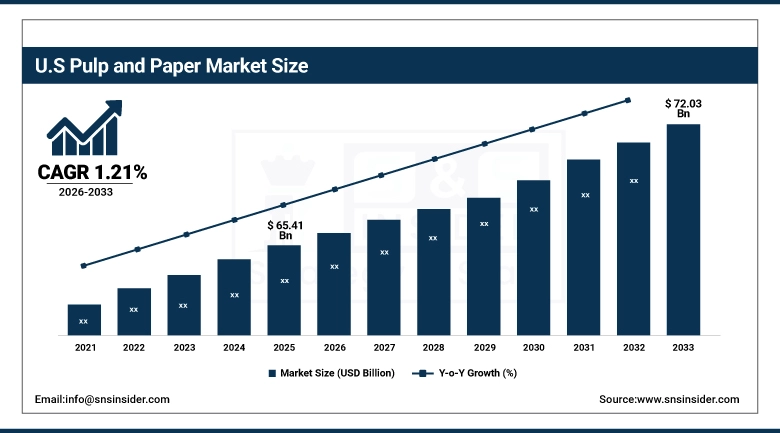

The U.S. Pulp and Paper Market Outlook

The U.S. Pulp and Paper Market was valued at approximately USD 65.41 Billion in 2025 and is expected to reach approximately USD 72.03 Billion by 2035, growing at a CAGR of 1.21%.

The United States is the world's second-largest national pulp and paper market by revenue, home to major integrated producers including International Paper, Georgia-Pacific, Packaging Corporation of America, and Clearwater Paper. The containerboard capacity in the United States has grown significantly during the last ten years to meet the needs of packaging caused by e-commerce. The volume shipped by Amazon forms some of the largest sources for purchasing corrugated packaging materials in the world. In the U.S. tissue market, there are three primary brands: Bounty and Charmin from Procter & Gamble, Angel Soft and Brawny from Georgia Pacific, and Cottonelle and Scott from Kimberly-Clark. Private label tissue has grown its share at the margin but has not displaced the premium national brands that command price premiums for softness, strength, and absorbency. U.S. specialty paper producers serve growing markets in filtration media, food packaging barrier papers, and pharmaceutical packaging, where performance specifications create differentiated products that cannot be easily commoditized or displaced by digital alternatives.

However, according to data from the U.S. Environmental Protection Agency released in 2025 showing a recycling rate of 68.2 percent of the total production of paper and cardboard, which can be recycled, shows how well this rate exceeds those in all other material streams and proves the competitive advantage that this industry has.

Pulp and Paper Market Segment Analysis

-

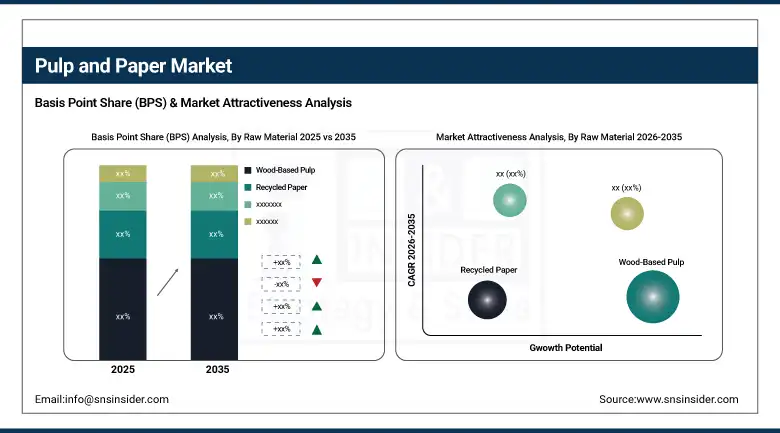

By Raw Material, wood-based pulp dominated with approximately 57% share in 2025; recycled paper is the fastest-growing raw material.

-

By Manufacturing Process, chemical pulping dominated with approximately 52% share in 2025 as the primary process for producing strong, high-brightness kraft and sulphite pulps for packaging and printing paper; recycled fiber processing is the fastest-growing process as recovered paper feedstock replaces virgin fiber in containerboard and tissue manufacturing.

-

By Product Type, packaging paper held the largest share of approximately 38% in 2025, driven by corrugated containerboard and kraft paper demand from e-commerce, food, and consumer goods packaging; specialty paper is the fastest-growing product type through filtration, technical, and food packaging paper demand that commands premium pricing.

-

By Application, packaging dominated with approximately 42% share in 2025 and is also the fastest-growing application.

By Raw Material, wood-based pulp dominates, recycled paper grows fastest

Wood-based pulp held approximately 57% of pulp and paper market revenues in 2025. This dominance reflects the pulp and paper industry's historical dependence on forest fiber for high-quality product manufacturing across all major paper grades. Chemical kraft pulp from softwood and hardwood species provides the strength, brightness, and uniformity that tissue, packaging, and printing paper specifications require. Major wood pulp producers including Suzano, CMPC, and Sveza operate at scale in South America, North America, and Northern Europe where sustainable forestry certification provides the provenance documentation that European and North American corporate procurement requires. The integrated forest-to-paper production model provides raw material cost stability that non-integrated paper producers dependent on market pulp cannot achieve.

Recycled paper is the fastest-growing raw material through 2035. Every ton of recycled fiber used in paper manufacturing displaces a ton of virgin wood pulp, reducing energy consumption, water use, and forest resource demand. Containerboard manufacturing, which includes the linerboard and medium that form corrugated shipping boxes, now uses more than 85% recovered fiber content in leading producers' operations. New containerboard mills in North America and Europe are being built as 100% recycled facilities without any virgin fiber processing capability. Regulatory mandates and corporate packaging sustainability commitments are ensuring that recovered fiber content continues to increase across all packaging paper grades through the forecast period.

By Application, packaging dominates and grows fastest

Packaging held approximately 42% of pulp and paper market application revenues in 2025 and is simultaneously the fastest-growing application category. E-commerce shipping volumes are the most powerful single driver of corrugated packaging demand growth. Every parcel shipped by Amazon, JD.com, Mercado Libre, or any other e-commerce platform requires a corrugated box, kraft paper void fill, and typically paper tape. The growth of e-commerce has transformed corrugated containerboard from a mature, slowly growing commodity into a high-growth essential input for the digital retail economy. The plastics packaging substitution trend represents an additional and potentially larger long-term demand driver as food, personal care, and consumer goods brands replace plastic flexible packaging with paper alternatives.

The competitive dynamics within packaging paper are shifting toward higher-value products. Standard corrugated medium and linerboard remain the highest-volume products by weight. However, barrier-coated papers for liquid food packaging, molded fiber packaging for consumer electronics and fresh food applications, and heat-sealable paper packaging for snacks and confectionery are all growing faster than commodity containerboard. These specialty packaging paper grades command significantly higher revenue per ton and require more sophisticated manufacturing capabilities, creating differentiation opportunities for producers investing in coatings, barrier layers, and precision fiber engineering.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

27.3% |

|

Asia Pacific |

China |

52.4% |

|

Middle East & Africa |

UAE |

26.8% |

|

Latin America |

Brazil |

44.3% |

North America Pulp and Paper Market Insights

North America is a large and technically sophisticated pulp and paper market characterized by a rationalized producer base that has reallocated manufacturing capacity from declining graphic paper toward growing packaging, tissue, and specialty paper grades. The United States accounts for approximately 83.4% of North American revenues and is home to several of the world's largest fully integrated paper companies. U.S. containerboard capacity has expanded to serve Amazon, Walmart, and Target's e-commerce packaging procurement at unprecedented volumes. The U.S. paper recycling infrastructure is among the most developed globally, with more than 68% recovery rates creating a reliable domestic recovered fiber supply for recycled-content packaging production. Canada is a major pulp and paper producing country with significant kraft pulp export capacity from its British Columbia, Ontario, and Quebec forestry sectors supplying European, Asian, and U.S. paper mills. Canada's abundant hydro-electric power gives its paper mills a structural cost advantage in energy-intensive pulping operations relative to mills in energy-cost-exposed geographies.

Europe Pulp and Paper Market Insights

Europe is a mature pulp and paper market undergoing significant structural transformation driven by graphic paper capacity closure and packaging capacity investment. Germany accounts for approximately 27.3% of European revenues as the EU's largest paper producer and consumer with strong positions in packaging paper, specialty paper, and tissue through producers including Smurfit Westrock, Mondi, and Sappi. EU packaging regulations including the Packaging and Packaging Waste Regulation are creating structural demand for paper-based packaging alternatives to single-use plastic that European paper manufacturers are investing in specialized coating and forming capabilities to serve.

Nordic countries including Sweden and Finland are major kraft pulp producers supplying European and global paper mills. Stora Enso, UPM-Kymmene, and Metsa Group operate large integrated forest-to-paper operations that give Scandinavian producers industry-leading sustainability credentials through Forest Stewardship Council certified fiber sourcing, renewable energy use, and verified carbon sequestration from managed forests. These sustainability credentials are commercially valuable in European corporate procurement that increasingly requires certified sustainable packaging supply.

Asia Pacific Pulp and Paper Market Insights

Asia Pacific dominated the global pulp and paper market in 2025 with approximately 49% of global revenues. China accounts for approximately 52.4% of Asia Pacific revenues as the world's largest paper producer and consumer market whose combination of massive packaging demand from domestic e-commerce, tissue and hygiene product consumption growth, and an active specialty paper manufacturing sector creates the world's largest single national market. Indonesia is a major kraft pulp and paper producer through APP (Asia Pulp & Paper) and APRIL, supplying both domestic demand and Asian and European export markets from large-scale plantation-based pulpwood operations.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Pulp and Paper Market Insights

The Middle East and Africa and Latin America are growing pulp and paper markets at different stages of industrial development. South America is a major global pulp supply source. Brazil's eucalyptus plantations, operated by Suzano, CMPC, and Klabin, produce the world's most cost-competitive kraft pulp through the combination of tropical growing rates, large-scale plantation management, and integrated processing. Brazil leads Latin American revenues at approximately 44.3% of the regional share as both the continent's largest pulp exporter and a large domestic paper consumer. Middle Eastern markets including the UAE are growing paper consumers rather than producers, importing paper products for their expanding packaging, printing, and consumer goods sectors.

Market Dynamics

Growth Drivers: E-commerce packaging demand, plastic packaging substitution, and tissue and hygiene paper consumption growth.

E-commerce is the single most powerful structural demand driver for the pulp and paper industry. Each percentage point of global retail sales shifting from physical stores to online channels adds incremental corrugated packaging demand at scale. The growth of food delivery, grocery e-commerce, and cross-border online retail has extended e-commerce packaging demand beyond electronics and apparel into every product category. This trend is particularly powerful in Asia Pacific where e-commerce penetration is growing from a lower base than North America and Europe but at considerably faster rates.

Regulatory plastic packaging substitution is the second major structural growth driver. The EU's Single-Use Plastics Directive, India's plastic bag phase-outs, China's plastic restrictions, and corporate net-zero packaging commitments from consumer goods multinationals are together creating demand for paper-based food packaging, molded fiber food service items, and coated paper flexible packaging that did not previously exist at commercial scale. These regulatory and commercial commitments are creating multi-year capital investment cycles at paper mills that are investing in coatings and fiber forming technologies to capture the substitution opportunity.

Restraints: Structural decline in printing and writing paper from digital substitution.

The biggest threat to the industry comes through structural obsolescence due to digital alternatives in relation to printing and writing papers. Since the beginning of the 2000s, the use of printing paper in offices around the world has been declining gradually due to digitization of document processing and bills. Newspaper and magazine printing paper demand has declined even more severely. These declines are creating mill closures, asset write-downs, and capacity rationalization costs that weigh on industry profitability even as growing packaging and tissue segments partially offset the volume loss. Wood fiber and energy represent 60 to 70% of total paper manufacturing costs and both are subject to significant price volatility. Producers with integrated upstream forestry assets and renewable energy from biomass and hydroelectric sources are structurally advantaged relative to manufacturers dependent on purchased pulp and grid electricity.

Opportunities: High-barrier specialty paper for plastic packaging replacement and dissolving pulp for textile fiber represent the strongest near-term growth opportunities.

High-barrier specialty paper is the fastest-growing commercial opportunity in the pulp and paper industry. Food packaging that requires moisture, grease, or gas barrier properties has historically been served by plastic laminated paper or plastic films. Each food packaging conversion from plastic to paper represents a multi-year supply contract that anchors stable premium-priced volume for the converting mill. Dissolving pulp for lyocell and viscose textile fiber production is an adjacent market that kraft pulp manufacturers can serve with process modifications that create a higher-value product than commodity papermaking pulp. As the textile industry responds to regulatory and consumer pressure to reduce its synthetic fossil fuel-derived fiber dependence, demand for forest-sourced cellulosic textile fiber is growing. Suzano's strategic investment in lyocell fiber production and the expanding dissolving pulp capacity of Nordic producers reflect industry recognition that textile fiber represents a premium growth market adjacent to the core paper business.

Recent Developments:

-

2025: Smurfit WestRock completed its merger to form one of the world's largest containerboard and corrugated packaging companies, combining Irish and U.S. operations to create a fully integrated pan-Atlantic packaging supplier with unmatched scale for major e-commerce customer negotiations.

-

2025: Suzano announced capacity expansions at its Cerrado mill in Brazil, one of the world's largest single-site kraft pulp facilities, increasing global eucalyptus pulp supply capacity to serve growing tissue and packaging demand in Asia and Europe.

-

2025: Mondi invested in new coated barrier paper production capacity in Europe, specifically targeting the food and fresh produce packaging market's transition away from plastic flexible packaging toward high-performance coated paper alternatives.

-

2025: International Paper progressed its strategic focus on corrugated packaging by completing planned asset disposals of printing paper businesses, concentrating capital allocation toward the containerboard and corrugated box segments aligned with e-commerce demand growth.

Pulp and Paper Market key players are:

-

Suzano SA

-

International Paper Company

-

Smurfit WestRock plc

-

Packaging Corporation of America

-

Mondi plc

-

UPM-Kymmene Corporation

-

Stora Enso Oyj

-

Georgia-Pacific LLC

-

Kimberly-Clark Corporation

-

Procter & Gamble Company

-

Sappi Limited

-

APP (Asia Pulp & Paper)

-

APRIL Group

-

Metsä Group

-

Clearwater Paper Corporation

-

Domtar Corporation

-

Resolute Forest Products

-

CMPC (Empresas CMPC)

-

Klabin SA

-

Nippon Paper Industries

Pulp and Paper Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 363.41 Billion |

| Market Size by 2035 | USD 428.87 Billion |

| CAGR | CAGR of 1.67% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Raw Material (Wood-Based Pulp, Recycled Paper, Non-Wood Pulp) • By Manufacturing Process (Chemical Pulping, Mechanical Pulping, Recycled Fiber Processing) • By Product Type (Packaging Paper, Printing & Writing Paper, Tissue & Hygiene Paper, Specialty Paper, Others) • By Application (Packaging, Printing & Publishing, Tissue & Personal Care, Industrial & Consumer Products, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Suzano SA, International Paper Company, Smurfit WestRock plc, Packaging Corporation of America, Mondi plc, UPM-Kymmene Corporation, Stora Enso Oyj, Georgia-Pacific LLC, Kimberly-Clark Corporation, Procter & Gamble Company, Sappi Limited, APP (Asia Pulp & Paper), APRIL Group, Metsä Group, Clearwater Paper Corporation, Domtar Corporation, Resolute Forest Products, CMPC (Empresas CMPC), Klabin SA, Nippon Paper Industries |

Frequently Asked Questions

Asia Pacific dominated the pulp and paper market in 2025 with approximately 49% of global revenues.

Packaging dominated with approximately 42% of revenues in 2025.

E-commerce packaging demand and the structural shift from plastic to paper-based packaging are the primary growth drivers.

The pulp and paper market was valued at USD 363.41 Billion in 2025.

The pulp and paper market is expected to grow at a CAGR of 1.67% from 2026 to 2035.

Get in Touch