Low Noise Amplifier Market Report Scope & Overview:

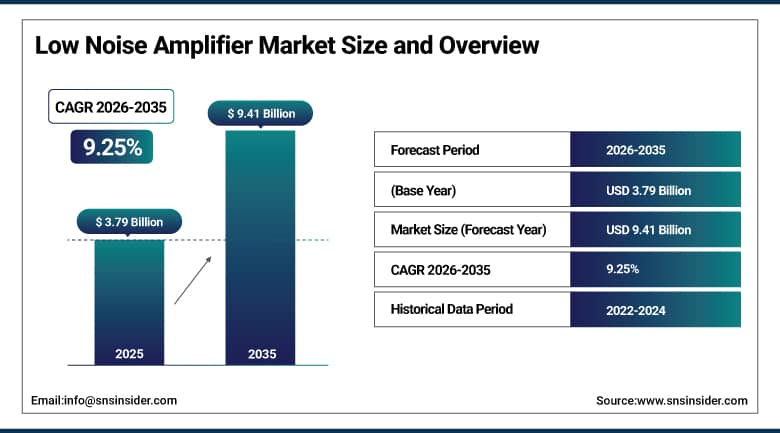

The Low Noise Amplifier (LNA) Market was valued at USD 3.79 billion in 2025 and is expected to reach USD 9.41 billion by 2035, growing at a CAGR of 9.25% from 2026-2035.

In wireless communication receiver - from a smartphone's cellular radio to a satellite ground station's signal chain - the low noise amplifier occupies the most critically sensitive position in the signal processing architecture: the first active component after the receive antenna, where the incoming signal is at its weakest and the addition of any noise by the amplifier permanently degrades the signal-to-noise ratio for all subsequent processing stages. The physics of signal chains means that the first amplifier's noise figure dominates the entire receiver's noise performance - a 2 dB noise figure LNA followed by a 15 dB noise figure mixer produces a combined receiver noise figure only marginally worse than the LNA alone, because the mixer's noise contribution is reduced by the LNA's gain. Low Noise Amplifier (LNA) devices must amplify weak signals with minimal noise, resist interference and distortion, and operate efficiently across different frequencies, materials, and circuit designs required for diverse wireless communication applications. The market's 9.25% CAGR reflects the compounding demand from 5G infrastructure - whose massive MIMO antenna arrays require thousands of LNAs per base station - satellite communication receivers, automotive radar, defense electronic warfare, and the expanding IoT device ecosystem.

Ericsson's 5G Network report documents that a massive MIMO 64T64R base station antenna - the standard configuration for urban 5G densification - contains 128 individual antenna ports each requiring a dedicated receive LNA in the antenna integrated circuit, creating per-base-station LNA demand of 128+ units that multiplies across the millions of 5G base stations being deployed globally. The Satellite Industry Association's State of the Satellite Industry 2024 report documents that over 7,000 commercial satellites were operational - each LEO satellite requiring precision low-noise amplifiers across its receive antenna arrays - with planned satellite internet constellations targeting 40,000+ satellites by the end of the decade.

LNA Market Size and Forecast

-

Market Size in 2025: USD 3.79 Billion

-

Market Size by 2035: USD 9.41 Billion

-

CAGR: 9.25% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Low Noise Amplifier Market - Request Free Sample Report

LNA Market Trends

-

GaN-based Low Noise Amplifier (LNA) development for mmWave 5G and satellite communication is increasing due to high-frequency performance and superior power handling above 60 GHz.

-

Integrated RF frontend modules combining LNAs, filters, and switches are enabling compact massive MIMO and advanced wireless infrastructure designs.

-

Cryogenic LNA development for quantum computing is creating a high-value niche market for ultra-low-noise amplification at extremely low temperatures.

-

6G research is accelerating development of sub-terahertz LNAs operating above 100 GHz for future ultra-high-speed communication networks.

-

Rising adoption of 77 GHz and 79 GHz automotive radar systems is driving demand for precision LNAs in ADAS and autonomous vehicles.

-

Ultra-low-power LNA designs for IoT devices are improving battery efficiency while maintaining reliable wireless signal reception.

-

Phased-array antenna systems in satellite communication and 5G mmWave networks are increasing demand for highly integrated multi-channel LNA architectures.

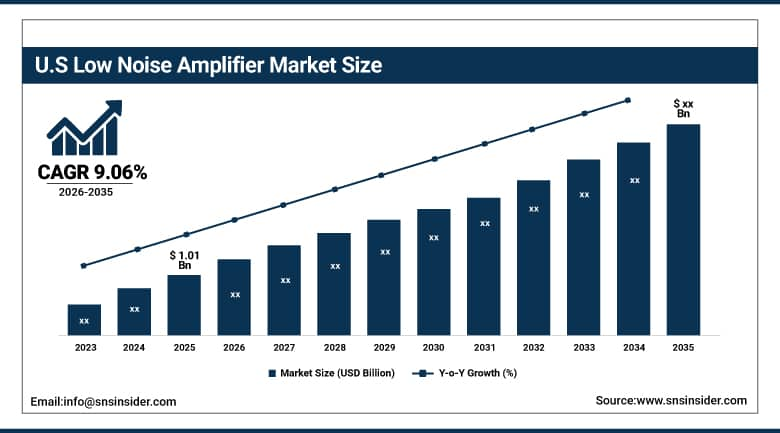

The U.S. Low Noise Amplifier Market was valued at USD 1.01 billion in 2025 and is expected to grow at a CAGR of 9.06% from 2026-2035.

In 2025, the United States lead the North American LNA market due to the dominance of top semiconductor and RF component suppliers like Qorvo, Skyworks Solutions, Analog Devices, MACOM Technology Solutions, and pSemi. This increased the market dominance of the country in designing and producing LNAs for applications in defense and aerospace, satellite communication, and wireless infrastructures. Its defense and aerospace sectors have huge demands for LNAs made from GaAs and GaN material that can function effectively at low-noise levels and high frequencies in radar equipment, electronic warfare systems, and satellite communication platforms. Moreover, the deployment of new infrastructures for 5G and incentives provided to semiconductor production by the government via FCC spectrum expansion programs would also fuel the rising demand for LNAs in the country.

Qorvo's fiscal year 2025 annual report documents that the company's LNA-containing radio frequency products generated the majority of its USD 4+ billion in annual revenue - demonstrating the commercial scale that LNA integration within RF front-end modules achieves in the smartphone, base station, and defense markets that Qorvo primarily serves. Skyworks Solutions' integrated LNA-based receive diversity module - deployed in over 1 billion smartphones annually - represents the world's largest single-company LNA consumer electronics deployment, whose handset volume sustains Skyworks' domestic manufacturing and design investment.

LNA Market Segment Analysis

-

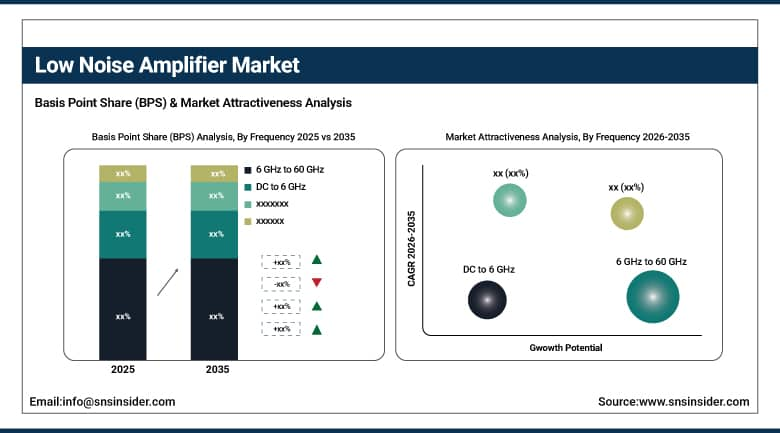

By Frequency, DC to 6 GHz dominated with the largest share in 2025; Greater than 60 GHz growing at fastest CAGR.

-

By Material, Silicon (Si) dominated with ~38.8% share in 2025; GaN growing fastest for mmWave and defense.

-

By Application, Consumer Electronics dominant; Telecom & Datacom growing at fastest CAGR.

By Frequency: DC-6 GHz dominant, >60 GHz fastest CAGR

DC to 6 GHz held the dominant frequency position in the LNA Market in 2025, reflecting the enormous volume of wireless devices operating in this spectrum - cellular communication from 700 MHz to 5 GHz, Wi-Fi at 2.4 GHz and 5 GHz, Bluetooth at 2.4 GHz, GPS at 1.575 GHz, and IoT protocols across multiple sub-6 GHz bands - whose aggregate handset, tablet, laptop, and IoT device volume creates LNA demand that higher-frequency segments cannot match by unit count. Silicon CMOS and SiGe BiCMOS LNA designs are standard across sub-6 GHz applications, whose semiconductor technology maturity enables cost optimization that sustains the commercial electronics market's volume-driven demand economics. The Greater than 60 GHz segment is growing at the fastest CAGR, driven by the deployment of mmWave 5G in urban environments - where 28 GHz and 39 GHz frequencies provide the multi-gigabit throughput for stadium, arena, and dense urban capacity - and the deployment of automotive radar at 77-79 GHz and 76-81 GHz - where every autonomous and ADAS-equipped vehicle contains multiple radar front-end modules requiring precision GaAs or SiGe LNAs.

By Material: Silicon dominant, GaN growing fastest

In the year 2025, silicon dominated with approximately 38.8% of market shares in LNA due to its economic pricing, integration capability, and use of CMOS technology. Silicon LNAs have a higher degree of advanced fabrication process at foundries and are integrated with digital baseband circuitry in order to reduce costs. GaAs technology still holds relevance in applications that require low noise, ultra-sensitivity like cellular receivers, satellite communication, and defense radar. On the other hand, GaN LNA technology is rapidly growing and holds significance due to its superior capabilities when it comes to handling high RF power. Additionally, it is well suited for mmWaves due to its large bandgap and hence used in many 5G, satellite and advanced radars that require efficiency along with low noise.

By Application: Consumer Electronics dominant, Telecom fastest CAGR

Consumer Electronics held the dominant application position in the LNA Market in 2025, reflecting the enormous volume of LNA-containing devices in the consumer electronics market - where every smartphone, tablet, laptop, smartwatch, wireless earphone, and Wi-Fi router contains multiple LNA components in its wireless receiver chains. The smartphone alone - with 1.2+ billion units shipped annually each containing 10-15 RF front-end modules including multiple LNAs for diversity reception, GPS, and Wi-Fi - creates aggregate LNA demand whose unit count dwarfs any other single application category. Telecom and Datacom is growing at the fastest CAGR, driven by the 5G base station infrastructure deployment - where each massive MIMO antenna requires 128+ LNA receive paths - and the satellite broadband ground terminal deployment whose millions of customer terminals each require precision low-noise receive chains. 6G research investment sustaining terahertz LNA development creates a technology pipeline whose commercial adoption timeline beyond the forecast period is sustaining R&D investment within the forecast period.

LNA Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Asia Pacific |

China |

42% |

|

Europe |

Germany |

27% |

|

Middle East & Africa |

Israel |

40% |

|

Latin America |

Brazil |

48% |

North America LNA Market Insights

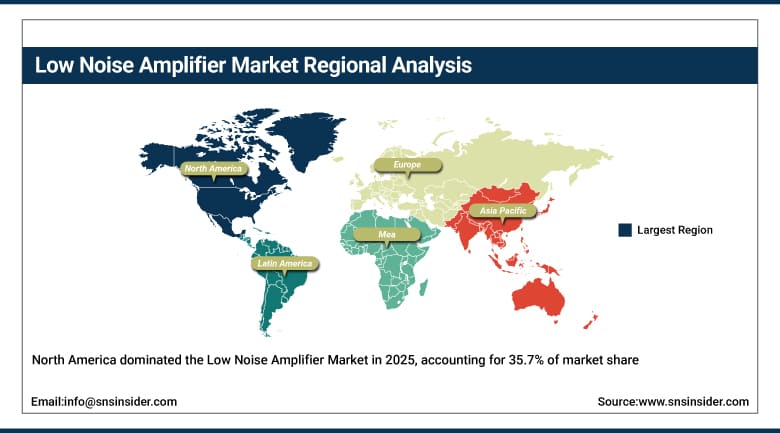

North America dominated the global LNA Market with approximately 35.7% revenue share in 2025, sustained by the United States' LNA semiconductor company concentration, defense and aerospace LNA procurement, and the domestic 5G infrastructure investment that sustains base station LNA procurement. The U.S. export control environment - where GaN-based LNA technology for defense radar and electronic warfare is export-controlled under ITAR and EAR provisions - sustains domestic LNA manufacturing investment by defense contractors and their semiconductor supply chain whose export-controlled technology cannot be sourced from offshore alternatives.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific LNA Market Insights

Asia Pacific is the fastest-growing regional LNA Market, driven by China's massive 5G base station infrastructure deployment - which has installed more 5G base stations than all other countries combined - India's growing telecommunications infrastructure investment, and the region's smartphone manufacturing concentration whose LNA procurement reflects global handset production scale. China's 5G base station deployment - with over 3 million base stations installed - has created the world's largest single-country 5G infrastructure LNA procurement market, where domestic suppliers including CMOS3C, Unigroup Spreadtrum, and national champion foundries sustain domestic LNA supply alongside imports from Qorvo and Skyworks.

Europe LNA Market Insights

Europe's LNA Market is growing with the European 5G infrastructure rollout - whose multi-band spectrum deployments across 700 MHz, 2.1 GHz, 3.5 GHz, and 26 GHz require LNA-containing radio equipment across European carrier base station networks - and the European Space Agency's satellite program procurement whose LNA requirements span Earth observation, deep space communication, and navigation satellite receiver chains. Infineon Technologies and STMicroelectronics sustain European LNA semiconductor design capability, serving automotive radar and industrial applications where European manufacturing has established market positions.

MEA and Latin America LNA Market Insights

Israel's LNA Market is active relative to its size - with defense companies including Elta Systems (IAI), Elbit Systems, and Rafael deploying advanced radar and electronic intelligence systems whose LNA specifications represent some of the world's most demanding performance requirements - sustaining Israeli LNA research and procurement at levels that support national defense capability independent of import supply chain reliability. Latin America's market concentrates in Brazil and Mexico's growing telecommunications infrastructure investment and consumer electronics distribution markets.

LNA Market Growth Drivers:

-

5G massive MIMO infrastructure and satellite communication expansion driving sustained low noise amplifier market growth globally

The LNA Market's 9.25% CAGR is driven by the extraordinary scale of 5G infrastructure deployment - whose massive MIMO antenna architectures require 128+ LNA components per base station at global deployment scales of millions of base stations - and the satellite communication expansion whose LEO constellation buildout is creating LNA demand at ground terminal and spacecraft scales that previous geostationary satellite programs could not generate. The simultaneous growth of automotive radar - whose ADAS and autonomous driving sensor requirements create per-vehicle LNA demand that is growing with each successive automotive safety specification level - compounds the infrastructure-driven demand with automotive volume that sustains LNA market growth across economic cycles whose infrastructure investment may fluctuate.

LNA Market Restraints:

-

Price pressure from integrated RFIC solutions and material substitution creating LNA market adoption challenges globally

The LNA market's standalone component value is being progressively compressed by the integration trend - where LNA, filter, power amplifier, and switch functions are combined in monolithic RF front-end module ICs that distribute the module's value across integrated components at margins below the sum of discrete component values. As silicon CMOS process scaling enables integration of previously GaAs-requiring LNA functions - with each CMOS node improvement enabling higher frequency operation at lower cost - the market share of premium GaAs and GaN LNA discrete components faces downward pressure from CMOS integration that reduces per-function value while expanding total silicon content.

LNA Market Opportunities:

-

Cryogenic quantum computing LNAs and 6G terahertz development creating significant low noise amplifier market growth opportunities globally

Cryogenic LNA for quantum computing represents the most commercially premium new LNA application - where superconducting quantum computers operating at 20 millikelvin require quantum-limited noise amplifiers operating at 4K whose noise temperature approaches the quantum noise floor (one photon per measurement bandwidth per second) and whose commercial availability is currently limited to a handful of specialist suppliers. Each quantum computing system requiring signal readout from 1,000+ qubits creates demand for cryogenic LNA arrays whose per-chip value of USD 5,000-50,000 - orders of magnitude above commercial wireless LNAs - creates premium revenue opportunity for the specialist suppliers who solve the quantum-limited cryogenic amplification challenge at commercial reproducibility standards. 6G terahertz LNA development - targeting 100-300 GHz operation for the sub-terahertz communication bands whose atmospheric transmission windows enable dense urban 6G - sustains InP HEMT development investment at semiconductor research institutions globally.

Recent Developments:

-

2026: Qorvo launched its QPL0065 5G mmWave LNA. It is a SiGe BiCMOS LNA optimized for 24-29.5 GHz 5G NR n257/n258/n261 band reception in massive MIMO antenna modules. This is used for achieving 1.2 dB noise figure and 20 dB gain in a 0.9mm × 0.9mm package whose size enables the 128-element antenna array integration density that Huawei, Nokia, and Ericsson massive MIMO RU designs require, with Qorvo reporting design wins at two Tier-1 base station OEMs representing combined annual volume exceeding 50 million units.

-

2025: Analog Devices launched its ADMV1018 W-band LNA. It is a GaAs pHEMT amplifier covering 76.5-85 GHz for 77 GHz automotive radar and 80 GHz point-to-point backhaul. It is used for achieving 3.2 dB noise figure and 22 dB gain across the full automotive temperature range from -40°C to +125°C, qualifying for ISO 26262 ASIL-B automotive functional safety requirements and receiving design-in confirmation from two European automotive Tier-1 radar module suppliers whose combined production represents 40 million automotive radar channel units annually.

-

2025: Low Noise Factory (LNF) AB launched the LNF-LNC4_16A cryogenic LNA. It operates at 4 Kelvin with 2K noise temperature across 4-16 GHz, covering all major superconducting qubit readout frequency bands - achieving the lowest noise temperature of any commercially available broadband cryogenic LNA and receiving procurement orders from IBM Quantum, IQM Quantum Computers, and Quantinuum whose quantum computing system expansions require cryogenic amplification at each qubit readout chain in processor arrays scaling toward 1,000+ qubit systems.

Low Noise Amplifier Market Key Players

-

Qorvo Inc.

-

Skyworks Solutions Inc.

-

Analog Devices Inc.

-

NXP Semiconductors NV

-

Macom Technology Solutions Inc.

-

pSemi Corporation

-

Broadcom Inc.

-

Infineon Technologies AG

-

STMicroelectronics NV

-

Texas Instruments Inc.

-

Microchip Technology Inc.

-

Renesas Electronics Corporation

-

Mini-Circuits

-

API Technologies Corp.

-

Teledyne Microwave Solutions Inc.

-

Cernex Inc.

-

Low Noise Factory AB

-

Cosmic Microwave Technology Inc.

-

Calteq Inc.

-

Richardson RFPD Inc.

Low Noise Amplifier Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.79 Billion |

| Market Size by 2035 | USD 9.41 Billion |

| CAGR | CAGR of 9.25% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Frequency (DC to 6 GHz, 6 GHz to 60 GHz, Greater than 60 GHz) • By Material (Silicon [Si], Silicon Germanium [SiGe], Gallium Arsenide [GaAs], Gallium Nitride [GaN], Others) • By Application (Consumer Electronics, Telecom & Datacom, Aerospace & Defense, Healthcare, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Qorvo Inc., Skyworks Solutions Inc., Analog Devices Inc., NXP Semiconductors NV, MACOM Technology Solutions Inc., pSemi Corporation, Broadcom Inc., Infineon Technologies AG, STMicroelectronics NV, Texas Instruments Inc., Microchip Technology Inc., Renesas Electronics Corporation, Mini-Circuits, API Technologies Corp., Teledyne Microwave Solutions Inc., Cernex Inc., Low Noise Factory AB, Cosmic Microwave Technology Inc., Calteq Inc., Richardson RFPD Inc. |

Frequently Asked Questions

Ans: North America dominated the Low Noise Amplifier Market in 2023.

Ans: DC to 6 GHz dominated; Greater than 60 GHz is growing at the fastest CAGR.

Ans: Silicon (Si) dominated with approximately 38.8% share; GaN is growing fastest.

Ans: Telecom & Datacom is growing fastest; Consumer Electronics dominated in 2025.

Ans: The Low Noise Amplifier Market was valued at USD 3.79 billion in 2025.

Get in Touch