Satellite Communication Market Report Scope & Overview:

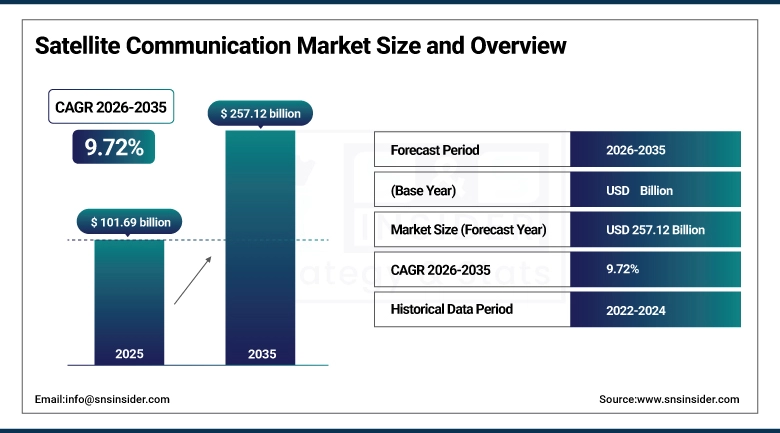

The Satellite Communication Market size was valued at USD 101.69 Billion in 2025 and is projected to reach USD 257.12 Billion by 2035, growing at a CAGR of 9.72% during 2026–2035.

The demand for satellite-based communication services has been increasing, and the Satellite Communication market is growing as the demand for reliable global connectivity continues to rise along with the increasing data traffic. The continuous evolution of satellite technologies such as Low Earth Orbit constellations (LEO) and high-throughput satellites (HTS) are increasing network capacity, coverage and bandwidth. Moreover, rising adoption in defense, aviation, maritime, broadcasting and remote connectivity applications along with rising investment by government and private space organizations expected to drive the market growth during the forecast years.

Satellite Communication Market Size and Growth Forecast:

-

Market Size in 2025: USD 101.69 Billion

-

Market Size by 2035: USD 257.12 Billion

-

CAGR: 9.72% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Satellite Communication Market - Request Free Sample Report

Satellite Communication Market Key Trends:

-

Rising Demand for High-Speed Global Connectivity: Increasing need for reliable broadband connectivity in remote and underserved regions is driving the adoption of satellite communication systems worldwide.

-

Growth of Low Earth Orbit (LEO) Satellite Constellations: Expansion of LEO satellite networks is improving latency, coverage, and data transmission speeds, significantly enhancing satellite communication capabilities.

-

Increasing Adoption in Defense and Government Applications: Governments and defense organizations are increasingly using satellite communication for secure communication, surveillance, and strategic operations.

-

Integration with 5G Networks: Satellite communication is being integrated with 5G infrastructure to extend network coverage and support seamless connectivity in rural and maritime areas.

-

Rising Use in Maritime, Aviation, and IoT Applications: Growing demand for in-flight connectivity, maritime communication systems, and satellite-based IoT solutions is expanding the application scope of satellite communication technologies.

US Satellite Communication Market Size Outlook

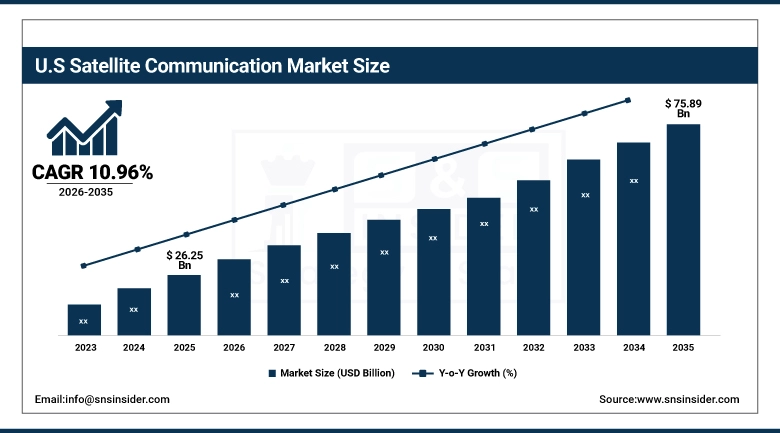

The United States Satellite Communication Market size was valued at USD 26.25 Billion in 2025 and is projected to reach USD 75.89 Billion by 2035, growing at a CAGR of 10.96% during 2026–2035. Strong growth in demand for high-speed connectivity, secure communication networks, and different satellite-based services for commercial and government sectors are contributing to the growth of U.S. Satellite Communication market. Increasing investments in modern satellite technologies, such as Low Earth Orbit (LEO) constellations and next-gen communication satellite is aiding the growth of this market.

Satellite Communication Market Key Drivers:

-

Rising Demand for Global Connectivity and Data Services

The Satellite Communication market is driven by an increase in the demand for reliable high-speed connectivity across remote and underserved regions. The rise in demand for broadband internet, broadcasting, and secure communication services among defense, aviation, maritime, and enterprise networks has fueled demand, resulting in solid market growth. Investment in state-of-the-art satellite technologies such as high-throughput satellites and low Earth orbit (LEO) constellations continues to expand coverage, bandwidth and communication efficiency across the globe.

Satellite Communication Market Key Restraints:

-

High Infrastructure and Deployment Costs

The high pricing of satellite design and deployment and land-based techniques is limiting industry expansion. Operational challenges also exist, including regulatory complexities, spectrum allocation issues and risks of space debris. Moreover, increasing terrestrial competition from fibre and 5G networks could also restrict the uptake in some areas.

Satellite Communication Market Key Opportunities:

-

Expansion of LEO Satellite Networks and Emerging Applications

With the rapid global deployment of LEO satellite constellations which offer reduced latency and greater coverage opportunities they are becoming increasingly significant. The proliferation of satellite communication for IoT connectivity, disaster management, remote monitoring, and autonomous systems is opening new revenue streams. Increased in-flight connectivity demand, maritime broadband services and satellite-enabled 5G backhaul should further propel the market growth during the forecast period.

Satellite Communication Market Segments:

-

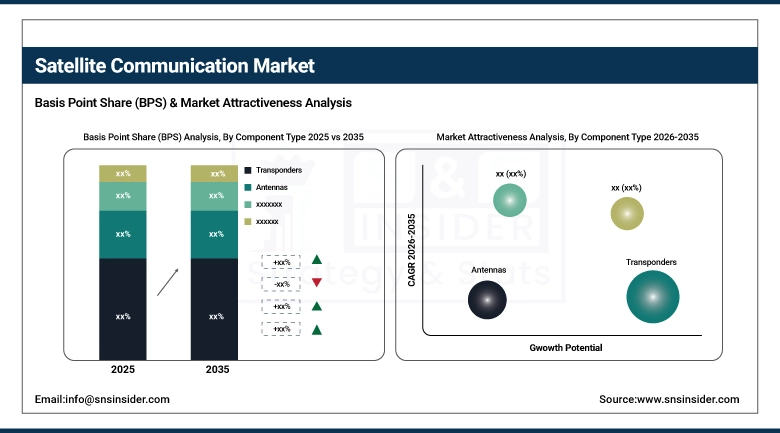

By Component Type: In 2025, Transponders dominated with 48% share; Antennas are the fastest growing segment during 2026–2035.

-

By Technology: In 2025, Very Small Aperture Terminal (VSAT) dominated with 46% share; Satellite Broadband is the fastest growing segment during 2026–2035.

-

By Application: In 2025, Broadcasting dominated with 41% share; Data Communication is the fastest growing segment during 2026–2035.

-

By End User: In 2025, Government & Defense dominated with 44% share; Maritime & Aviation is the fastest growing segment during 2026–2035.

By Component Type: Transponders Led as Antennas Emerge as the Fastest-Growing Segment.

Transponders are the most significant component in Satellite Communication market, for which, Satcom Transponder is a vital component that receives, amplifies, and retransmits communication signals from satellites to ground stations. This makes them an essential building block through most satellite systems, because they play a crucial role in the signal transmission for broadcasting, navigation and broadband services. The growing requirement for high-throughput satellites, and the rising demand for greater global connectivity, are also boosting demand for novel transponder technology.

The lowest segment in terms of revenue is antennas which is owing to the increasing need for high performance ground terminals and mobile satellite communication systems. Phased-array and electronically steered antenna technology advancements allow for faster data connections, increased signal accuracy, and overall improved performance in aviation, maritime, and defense sectors.

By Technology: VSAT Dominated as Satellite Broadband Expands Rapidly.

The Satellite Communication market is dominated by Very Small Aperture Terminal (VSAT) technology as it is widely used in enterprise networks, providing remote facility connectivity, and broadband communication services. The various industry verticals using VSAT includes banking, retail, oil & gas, government communication networks, etc., built to obtain reliable connectivity in marginal locations. These have further enhanced their scalability, cost efficiency, and proven reliability in supporting the market-leading position.

This new technology segment, in particular, satellite broadband is spreading faster owing to high-speed internet demand and rapid deployment of Low Earth Orbit (LEO) satellite constellations. Wireless technologies are evolving into advanced systems with greater data throughput and less latency, driving their use in home, enterprise and mobile communications services.

By Application: Broadcasting Led as Data Communication Shows Strong Growth Momentum.

The Satellite Communication market has been led by the Broadcasting segment as satellite has been used extensively for television distribution, radio broadcasting, and media transmission for a long time now.

Among these, data communication has emerged as the fastest-growing application segment, with organizations depending more on satellite networks for providing broadband services, cloud connectivity services, and secure data transmission. A growing number of satellite data networks to meet the fast-growing demand of Internet of Things devices, remote operations and digital communication platforms.

By End User: Government & Defense Led as Maritime & Aviation Experience Rapid Growth.

The Satellite Communication market is primarily driven by the government and defense sector because this sector is largely dependent on secure communication, surveillance, intelligence gathering, and navigation systems. Satellite is a key connection tool for military, disaster and national security tasks. This segment continues its dominance through renewed investment in advanced satellite infrastructure and defense communication systems.

Maritime and aviation are the fastest-growing end-user segments of the satellite-based IoT market due to the demand for real-time communication, navigation, and high-speed onboard connectivity. Increase in demand for in-flight Internet services, satellite used for fleet management, and maritime broadband solution is propelling strong growth across these industries.

Satellite Communication Market Regional Analysis:

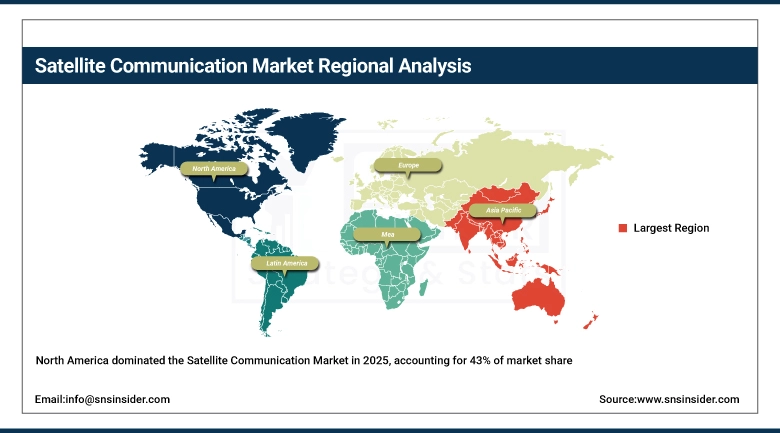

North America Satellite Communication Market Insights:

North America is the dominating region in Satellite Communication market with the largest market share of 43% in 2025. The region benefits from a combination of solid technological competencies, heavy investments in satellite infrastructure, and the high concentration of major satellite operators and aerospace companies in the United States and Canada. The satellite communication market is experiencing growth due to the high demand for satellite communication, in which a large number of defense, broadcasting, aviation, maritime, and enterprise connectivity applications is driving the market growth. The persistent technological advancements in satellite satellites such as LEO constellations and high/work-throughput satellites further cements North America dominance in the Satellite Communication market globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Satellite Communication Market Insights:

The satellite communication market is being driven by rapid growth in the region like Asia Pacific and it is expected to grow at approximately 10.69% CAGR through the forecast duration of 2026–2035. Increase in investments in space programs, development of satellite launches, and demand for high-speed connectivity among countries, including China, India, Japan, and South Korea, has driven the rapid growth. Increasing penetration of digitalization, need for broadband services in remote areas, and increasing use of satellite services in defense, aviation, maritime, and telecommunication industries are some of the key driving factors contributing to the growth of this market.

Europe Satellite Communication Market Insights:

Europe accounts for a considerable share of the global satellite communication market, due to the commanding aerospace and satellite manufacturing potential across Germany, France, the UK, and Italy. The region is witnessing growth owing to its advanced research programs, supportive government for space programs, and the increasing demand for satellite based communication services in defense, broadcasting and transportation. Its increasing need for protection communication networks and all satellite link connectivity broadband services are also supporting market establishment of distributed data in Europe

Latin America Satellite Communication Market Insights:

Latin America Satellite Communication market is also growing with a stable growth factor owing to increasing demand for broadband connectivity in remote and rural areas with lack of terrestrial infrastructure. Satcom services in telecom, broadcast and disaster management applications are gaining increasing acceptance in countries such as Brazil, Mexico and Argentina. The implementation of satellite communication technologies is being supported across the region by government initiatives to improve digital connectivity and broaden communication infrastructure.

Middle East & Africa (MEA) Satellite Communication Market Insights:

Satellite Communication Market in the Middle East and Africa (MEA) is gradually bulging as the demand for secure communication continues to rise, telecommunications infrastructure keeps expanding, and space technology continues to record high investment. Connectivity is provided through satellite communication, especially in remote regions of the continent, such as parts of Africa and the Middle East. Market growth is driven by increased adoption in defense, oil & gas operations, aviation and maritime communication, and more robust future growth is anticipated as government invests in satellite programs and digital infrastructure.

Satellite Communication Market Competitive Landscape:

SpaceX is a leading aerospace manufacturer and satellite communications provider, widely recognized for its Starlink satellite internet constellation, which delivers high-speed broadband connectivity globally. In the Satellite Communication market, SpaceX focuses on deploying Low Earth Orbit (LEO) satellites to provide low-latency, high-capacity internet services for residential, commercial, maritime, and aviation users. The company’s vertically integrated launch capabilities and rapid satellite deployment strategy strengthen its competitive position in the global satellite communications industry.

-

May 22, 2025, SpaceX expanded its Starlink constellation with multiple satellite launches to enhance global broadband coverage and network capacity.

Hughes Network Systems is a major provider of satellite broadband and managed network services, offering connectivity solutions for enterprises, governments, and consumers worldwide. In the Satellite Communication market, Hughes specializes in satellite internet services, ground systems, and Very Small Aperture Terminal (VSAT) technologies that support remote connectivity and enterprise communication networks. The company’s extensive satellite infrastructure and strong partnerships with global operators support reliable broadband delivery across rural and underserved regions.

-

March 18, 2025, Hughes Network Systems announced the expansion of its satellite broadband services to improve connectivity solutions for enterprise and government customers.

Viasat Inc. is a global communications company providing satellite broadband services, secure networking systems, and advanced communication technologies. In the Satellite Communication market, Viasat focuses on high-throughput satellite systems that support broadband connectivity for aviation, maritime, defense, and residential users. The company continues to invest in next-generation satellite infrastructure to enhance network capacity, coverage, and service reliability worldwide.

-

July 9, 2025, Viasat expanded its satellite communication capabilities by advancing high-capacity satellite services to support growing global broadband demand.

Satellite Communication Companies are:

-

SpaceX

-

Viasat Inc.

-

SES S.A.

-

Intelsat S.A.

-

Thales Alenia Space

-

Boeing Defense, Space & Security

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Cobham SATCOM

-

Gilat Satellite Networks

-

Inmarsat

-

Globalstar, Inc.

-

Telesat

-

Iridium Communications Inc.

-

Orbital ATK

-

Kratos Defense & Security Solutions

-

L3Harris Technologies

-

Blue Origin

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 101.69 Billion |

| Market Size by 2035 | USD 257.12 Billion |

| CAGR | CAGR of 9.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component Type: (Transponders, Antennas, Receivers & Transmitters) •By Technology: (Very Small Aperture Terminal (VSAT), Satellite Telemetry Tracking & Control (TT&C), Satellite Broadband) •By Application: (Broadcasting, Navigation & Positioning, Data Communication) •By End User: (Government & Defense, Commercial Enterprises, Maritime & Aviation). |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX, Hughes Network Systems, Viasat Inc., SES S.A,Intelsat S.A., Eutelsat Communications, Thales Alenia Space, Boeing Defense, Space & Security, Lockheed Martin Corporation, Northrop Grumman Corporation, Cobham SATCOM, Gilat Satellite Networks, Inmarsat, Globalstar, Inc., Telesat, Iridium Communications Inc., Orbital ATK, Kratos Defense & Security Solutions, L3Harris Technologies, Blue Origin. |

Frequently Asked Questions

North America dominated the Satellite Communication Market in 2025.

The Transponder segment dominated the Satellite Communication Market due to its essential role in signal transmission, broadcasting services, and satellite-based communication networks.

The key drivers of the Satellite Communication Market include the rising demand for global connectivity, increasing deployment of satellite constellations, and growing adoption across defense, aviation, maritime, and broadband communication services.

The market was valued at USD 101.69 Billion in 2025 and is projected to reach USD 257.12 Billion by 2035.

The Satellite Communication Market is expected to grow at a CAGR of 9.72% during 2026-2035.

Get in Touch