All-Flash Array Market Report Scope & Overview:

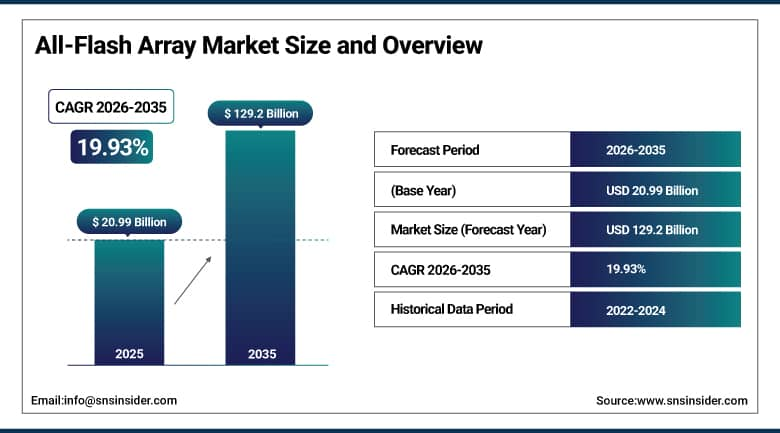

The All-Flash Array Market size was USD 20.99 Billion in 2025 and is expected to reach USD 129.2 Billion by 2035, growing at a CAGR of 19.93% from 2026–2035.

The All-Flash Array (AFA) Market is witnessing exponential growth owing to the rising need for high-speed, high-performing, and low-latency storage solutions in enterprise IT systems. Data creation from cloud computing, artificial intelligence, machine learning, and big data analytics is the reason behind enterprises switching from traditional storage based on HDDs to flash storage technology. Enterprises are keen to get faster data access speed, scalability, and energy efficiency.

In addition, the increase in the deployment of hyper-converged infrastructure, virtualization, and digital transformation initiatives in BFSI, healthcare, IT & telecom, and retail industries is also aiding the market growth.

Market Size and Forecast:

-

Market Size in 2026E: USD 25.17 Billion

-

Market Size by 2035: USD 129.2 Billion

-

CAGR: 19.93% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On All-Flash Array Market - Request Free Sample Report

All-Flash Array Market Trends:

-

NVMe-based AFA adoption keeps accelerating as enterprises demand lower latency and higher throughput.

-

AI and machine learning workloads are driving fresh demand for high-performance, low-latency flash storage.

-

Energy-efficient AFA designs are gaining priority as data center operators face growing power cost pressures.

-

Custom Flash Modules are gaining traction for AI and financial analytics workloads requiring specialized storage.

-

Cloud-integrated AFA solutions are expanding as enterprises pursue hybrid storage across on-premises and cloud.

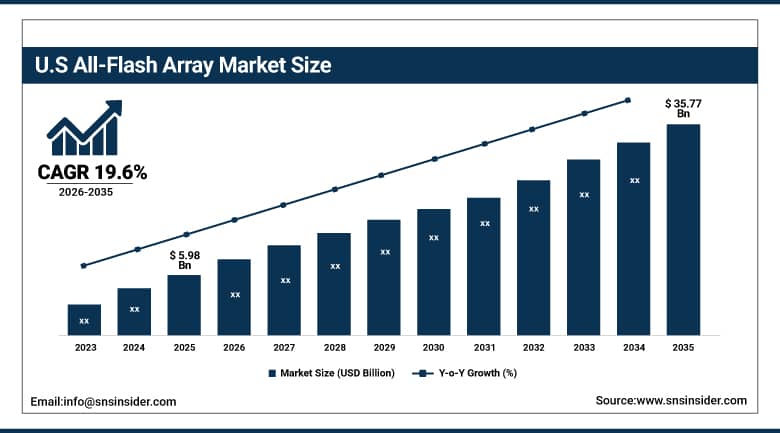

U.S. All-Flash Array Market Outlook:

The U.S. All-Flash Array Market was valued at approximately USD 5.98 Billion in 2025. It is expected to reach approximately USD 35.77 Billion by 2035. The market is growing at a CAGR of approximately 19.6%.

The growth of the U.S. All-Flash Array Market is attributed to increasing demand for cloud computing, artificial intelligence-enabled workloads, and digital transformation among various industry verticals. Enterprises are turning towards all-flash storage for higher performance and faster data processing in comparison with conventional storage technologies. Growing demand from hyperscale data centers, BFSI, healthcare, and IT & telecommunications industry segments is adding fuel to the fire. Apart from this, growing investment in cybersecurity, analytics, and hybrid cloud environments is making enterprises adopt next-generation storage technologies due to the need for energy efficiency and cost optimization.

IBM unveiled the FlashSystem 5300 in April 2024, an entry-level all-flash storage platform for SMEs. The system is designed to deliver enhanced performance, scalability, and cyber resilience specifically. It targets organizations with demanding performance requirements but more constrained budgets.

All-Flash Array Market Segment Analysis:

This section examines performance across each major segmentation dimension covered in this report.

-

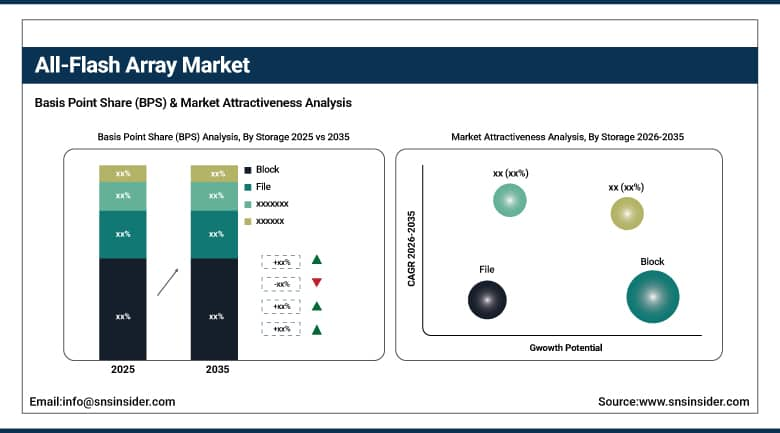

By Storage, the Block segment dominated the All-flash array market with approximately 46.4% share in 2025. The File segment is expected to register the fastest CAGR through the forecast period.

-

By Flash Media, the SSD segment dominated the All-flash array market with approximately 73.9% share in 2025. The Custom Flash Modules segment is expected to register the fastest CAGR through the forecast period.

-

By Industry, the BFSI segment dominated the All-flash array market with approximately 29.8% share in 2025. The Retail segment is expected to register the fastest CAGR through the forecast period.

By Storage, block dominates, file grows fastest

The block storage segment dominated the storage category with an estimated revenue share of about 46.4% in 2025. Excellent performance and fast response times tailored to structured data makes this segment the ideal storage solution for important enterprise applications. Databases, ERPs, and virtualization all depend on block storage in particular. Extensive adoption of block storage among BFSI, health care, and telecommunications segments continues to solidify its position as the dominant segment. Transaction frequency and downtime constraints are both well suited to block storage in these industries.

The file storage segment is projected to have the fastest CAGR during the forecast period. Growing demand for content collaboration platforms, unstructured data management solutions, and media-rich applications is propelling the growth in the file storage market. The media and entertainment sector, research institutes, and cloud storage services are some of the segments adopting file storage solutions. This is due to the scalability and efficient sharing capability of the file storage segment.

By Flash Media, SSD dominates, CFM grows fastest

The Solid State Drives were the major segment under the flash media category with a revenue market share of about 73.9%. This is due to the prevalence of SSDs in enterprise storage systems and data centers due to its cost-effective nature and reliability. They provide high-speed processing of vast amounts of data compared to conventional drives, are easy to incorporate into IT infrastructure, and are preferred by various industries such as BFSI, healthcare, and retail for storing massive transactional data volumes.

Custom Flash Modules are forecasted to have the highest CAGR throughout the forecast period. CFMs are becoming popular due to their ability to provide customized high-performance storage that works for particular workloads. Various workloads such as AI & machine learning, real-time analytics, and financial modeling gain from the CFM-tailored performance due to improved stamina, elasticity, and efficiency while handling complex data sets. With increasing demand for AI workloads, CFM demand will continue to increase rapidly.

By Industry, BFSI dominates, retail grows fastest

The BFSI sector accounted for around 29.8% market share in 2025, which makes up for the biggest industry category. Increasing reliance on speedy, secure, and fast data storage solutions for transactions, customer information, and analytics explains such a big share. AFAs can be used for improving latency of data access, enhancing fraud detection technologies, and creating digital banking services. Furthermore, the BFSI sector plans to improve customer experience through data analysis; therefore, the implementation of AFAs will continue growing. The Government and Telecommunications sectors contribute considerably to the overall industry demand.

Among other industry categories, the Retail segment demonstrates the highest CAGR due to increasing usage of e-commerce platforms, customer analytics, and targeted marketing. Therefore, there is a rising demand for scalable storage solutions. AFAs become necessary for retailers who need to store data about inventory, customer activity, and carry out online transactions. Healthcare industry invests in AFAs to manage electronic health records, medical imagery, and real-time monitoring of patients' state. Telecommunications companies invest in AFAs to manage increasing number of subscribers and analytics. Further development of digital commerce and data-based retail industry will continue driving this category.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

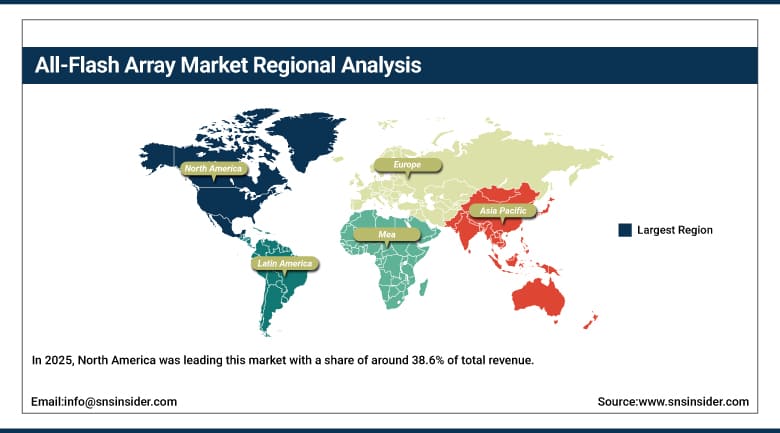

North America All-Flash Array Market Insights

In 2025, North America was leading this market with a share of around 38.6% of total revenue. High density of data centers, cloud service providers and big technology firms have been instrumental behind such leadership in this region. Adoption of enterprises for better data processing through BFSI, healthcare and IT segments adds strength to such dominance in the region. Dominance of leading AFA suppliers like IBM, Pure Storage, NetApp and Dell Technologies further drives innovation in the country. Stringent laws related to data protection also speed up adoption of AFA for safe storage and disaster recovery. Increasing investments in AI infrastructure by hyperscalers further increases demand for AFA.

Around 82.5% of total North American revenue is generated by the United States. Increasing investments in cloud computing and AI infrastructure are fueling the domestic demand for AFA.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe All-Flash Array Market Insights

Europe offers a substantial market opportunity for AFAs driven by tight regulations around data privacy and investments in digital transformation. Germany dominates this region in terms of the AFA market, with its well-developed industrial IT and finance sectors' demand for AFAs. France and the UK offer demand due to their development of data centers and cloud services.

Germany makes up around 24.6% of revenues in Europe. Increasing focus on data sovereignty drives more organizations in Europe to deploy AFA solutions on-premises. Such a regulatory landscape should continue to drive stable growth in Europe.

Asia Pacific All-Flash Array Market Insights

The Asia Pacific region is likely to post the highest CAGR over the forecast period. Smart city initiatives, 5G, and data generated from digital services are seeing fast growth in countries such as China, India, and Japan. Hyperscaler companies like Alibaba Cloud have been rolling out high-end AFA solutions to handle data from e-commerce and clouds. The fast-growing fintech industry of India is seeing the rapid integration of AFAs to process transactions quickly.

South Korea and Singapore have become significant regional players owing to their fast growth in data centers. China holds around 40.6% share of Asia Pacific revenues. Fast-growing data center deployments and AI workloads are fueling the demand for AFA.

MEA & Latin America All-Flash Array Market Insights

The UAE leads MEA revenue at approximately 22.8%. Growing investment in smart city infrastructure and expanding data center capacity both support this position. Saudi Arabia is also expanding its cloud and enterprise IT infrastructure through digital transformation initiatives.

Brazil leads Latin American revenue at approximately 43.8%. Expanding digital banking, healthcare digitization, and cloud adoption all drive this regional lead. Mexico and Argentina contribute secondary demand through their own expanding enterprise IT sectors.

Market Dynamics:

Growth Drivers: Rising demand for high-performance storage from data-intensive industries

The rising need for high performance storage solutions among the data-centric industries is aiding the growth of the All-flash array market. The rising need for cloud computing, big data analysis, and AI have driven the demand for high-speed and low latency data access. The BFSI sector, healthcare, and telecommunications industry are making large investments into AFAs to enhance their data processing capability, security, and IT efficiency. The increasing shift from hard drive storage solutions to flash drives is also driving market growth.

The growing volume of unstructured data is continuously increasing the need for these solutions across almost all major industries. Faster storage systems are required by enterprises due to AI inference and training applications. The rising need for the replacement of power-consuming HDDs with flash drives is also driving the market. As the adoption of AI continues to increase globally, this factor will remain strong during the forecast period.

Restraints: Data security challenges and integration complexity limiting adoption

Security of data and privacy pose important concerns in the All-flash array market. The trend towards adoption of AFAs increases susceptibility to cyber threats, data breach, and ransomware. Adequate data security measures, encryption, and recovery are vital, especially in BFSI and healthcare industries. Complying with changing data privacy laws creates additional complications.

Integrating AFAs with existing IT architecture is difficult and requires substantial investment. The time and expertise involved in integrating make the implementation process challenging. Enterprises that do not have requisite IT expertise may delay their decision on adopting AFAs even after realizing performance gains from AFA solutions.

Opportunities: Emerging NVMe technology and digital transformation driving AFA growth

New technologies such as NVMe offer improved data transfer rates and facilitate quick workload management. Such advancements open up numerous opportunities within the AFA industry for high-performing applications. Specialized storage solutions for particular workloads, including CFMs used in AI and financial analysis, will open up yet another avenue of expansion for vendors.

Increasing investments in digital transformation in developing economies within Asia Pacific and Latin America offer diverse opportunities as well. As data centers evolve through the implementation of energy-efficient technologies, those who manage to improve their performance while minimizing total cost of ownership will continue to grow their share in the market.

Recent Developments:

-

2024: IBM unveiled the FlashSystem 5300, an entry-level all-flash storage platform delivering enhanced performance, scalability, and cyber resilience for SMEs.

-

2024: Dell Technologies launched PowerStore Prime, an AI-driven storage management software update enabling automated optimization and cyber resilience across its PowerStore array portfolio.

-

2024: Pure Storage announced FlashArray for AWS Outposts, integrating enterprise-grade on-premises flash storage with AWS cloud services for hybrid deployments.

All-Flash Array Market Key Players are:

These vendors span hyperscale storage leaders, enterprise hardware specialists, and high-performance computing storage providers.

-

IBM

-

Pure Storage

-

NetApp

-

HPE

-

Dell Technologies

-

Huawei

-

Hitachi Vantara

-

Western Digital

-

Cisco

-

iXsystems

-

Tintri

-

StarWind

-

Supermicro

-

DDN

-

Oracle

-

Kioxia Corporation

-

Micron Technology, Inc.

-

Samsung Electronics Co., Ltd.

-

Nutanix, Inc.

-

Infinidat Ltd.

All-Flash Array Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 20.99 Billion |

| Market Size by 2035 | USD 129.2 Billion |

| CAGR | CAGR of 19.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Storage (File, Object, Block) • By Flash Media (Custom Flash Modules (CFM), Solid-State Drives (SSD)) • By Industry (BFSI, Healthcare, Retail, Telecommunications, Government) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM, Pure Storage, NetApp, HPE, Dell Technologies, Huawei, Hitachi Vantara, Western Digital, Cisco, iXsystems, Tintri, StarWind, Supermicro, DDN, Oracle, Kioxia Corporation, Micron Technology, Samsung Electronics, Nutanix, and Infinidat are leading global all-flash array and enterprise storage solution providers offering high-performance data storage systems, cloud-integrated storage architectures, and scalable infrastructure solutions for modern data centers and enterprise IT environments. |

Frequently Asked Questions

The All-Flash Array Market is expected to grow at a CAGR of 19.93% from 2026 to 2035.

The All-Flash Array Market was valued at USD 20.99 Billion in 2025.

Rising demand for high-performance storage from AI, cloud computing, and data-intensive industries is the primary growth factor.

The Block segment dominated the All-Flash Array Market with approximately 46.4% share in 2025. The File segment is expected to grow fastest.

North America dominated the All-Flash Array Market with approximately 38.6% revenue share in 2025, supported by a high concentration of cloud providers and enterprise technology companies. Asia Pacific is the fastest-growing region.

Get in Touch