Luxury Fashion Market Report Scope & Overview:

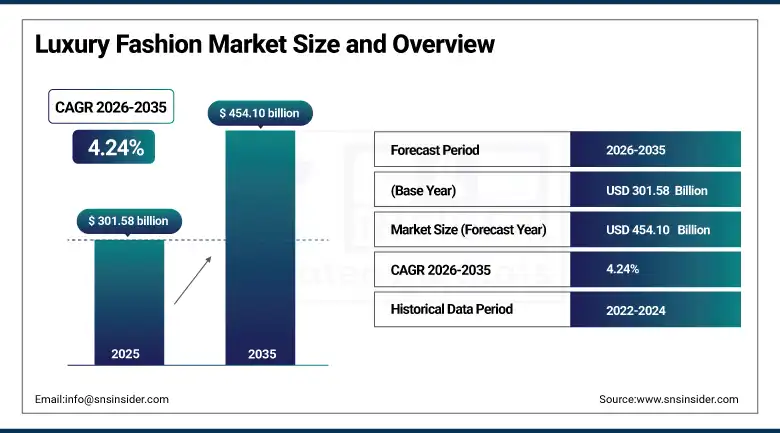

The Luxury Fashion market was valued at USD 301.58 billion in 2025 and is expected to reach USD 454.10 billion by 2035, growing at a CAGR of 4.24% from 2026–2035.

Luxury fashion represents the apex of the global apparel, footwear, and accessories markets. The market encompasses the complete spectrum of luxury fashion product categories from the haute couture ateliers of Paris. The luxury fashion market's sustained commercial relevance across economic cycles reflects the fundamental human motivations of status signaling, beauty seeking, and self-expression that are not extinguished by economic adversity among the affluent consumer segments whose income and wealth are sufficiently insulated from cyclical downturns to sustain luxury consumption behavior through periods that see discretionary spending decline broadly across mass market categories. The market is simultaneously expanding its consumer base as rising incomes in China, India, and Southeast Asian markets bring new cohorts of affluent consumers into the luxury fashion purchasing demographic for the first time, while digital access through e-commerce, social media discovery, and resale platforms is extending luxury brand awareness and aspiration to consumer segments whose income levels enable occasional or aspirational luxury purchase even if they cannot sustain regular luxury consumption.

Bain & Company's 2025 Global Luxury Study's confirmation that global personal luxury goods spending reached approximately EUR 390 billion in 2024, supported by a global luxury consumer base that has expanded from approximately 140 million people in 2000 to over 400 million in 2024, demonstrates the extraordinary broadening of luxury market participation that rising global affluence has delivered even as the category's highest price points continue to appreciate to ensure the exclusivity that defines genuine luxury positioning.

Market Size and Forecast

-

Market Size in 2026E: USD 314.37 Billion

-

Market Size by 2035: USD 454.10 Billion

-

CAGR (2026 to 2035): 4.24%

-

Fastest Growing Region: Asia Pacific

-

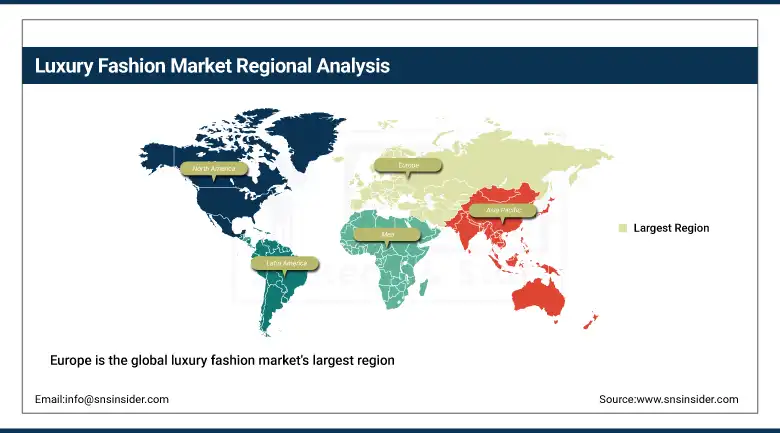

Largest Region: Europe

To Get more information On Luxury Fashion Market - Request Free Sample Report

Luxury Fashion Market Trends

-

Luxury fashion brands are expanding digital retail through e-commerce, virtual appointments, AI shopping assistants, and augmented reality tools.

-

The luxury pre-owned market is growing through authenticated resale platforms and certified brand-operated second-hand fashion programs.

-

Gen Z luxury engagement is increasing through streetwear collaborations, music partnerships, and digitally driven social media marketing campaigns.

-

Sustainability investments in luxury fashion include circular economy programs, regenerative sourcing, repair services, and supply chain transparency initiatives.

-

Luxury brands are expanding experiential offerings through immersive retail, private events, travel experiences, and exclusive membership communities.

The U.S. Luxury Fashion Market Outlook

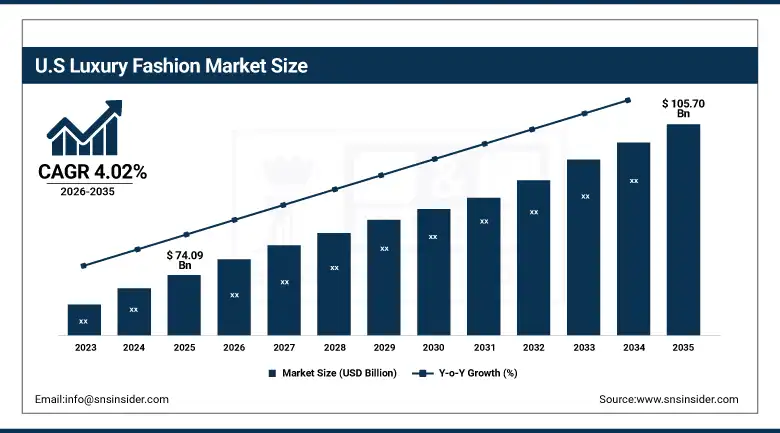

The U.S. Luxury Fashion Market was valued at approximately USD 74.09 billion in 2025 and is expected to reach approximately USD 105.70 billion by 2035, growing at a CAGR of 4.02%. The United States is the world's largest single national luxury fashion market by revenue, where the combination of the highest absolute number of high-net-worth individuals of any country, deep brand loyalty to established European luxury houses among the established affluent consumer base, and the rapidly growing luxury engagement of younger affluent Americans whose spending patterns are being shaped by digital-first discovery, influencer-driven brand awareness, and the premium resale economy collectively sustain above-average luxury fashion spending growth relative to most European markets that are dealing with more constrained affluent population growth and greater macroeconomic sensitivity among aspirational luxury consumers. American luxury fashion purchasing is also supported by the world's most extensive luxury multi-brand retail infrastructure encompassing dedicated luxury department stores including Neiman Marcus, Saks Fifth Avenue, and Bergdorf Goodman alongside the flagship boutiques of every major luxury brand in New York, Beverly Hills, and other major luxury retail concentrations.

The U.S. luxury fashion market's resilience through the 2022 to 2023 luxury demand normalization that followed the extraordinary post-pandemic revenge spending surge, where American luxury consumers maintained above-pre-pandemic spending levels even as European and Asian luxury markets experienced sharper corrections, demonstrates the structural demand characteristics of the world's largest absolute affluent consumer population whose luxury spending capacity is less dependent on cyclical income fluctuations than markets where luxury consumption is more concentrated in the aspirational consumer segment.

Luxury Fashion Market Segment Analysis

-

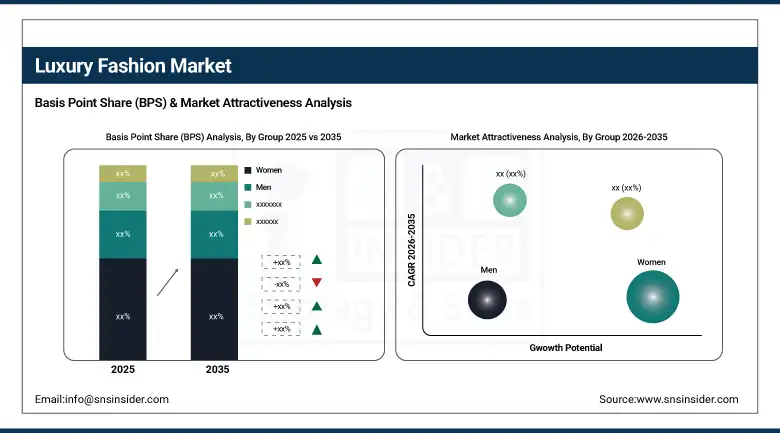

By Group, women led the market with approximately 58.50% share in 2025; men segment is the fastest-growing segment at a CAGR of 7.80%.

-

By Type, clothing & apparel led with approximately 52.40% share in 2025; accessories are the fastest-growing at a CAGR of 7.60%.

-

By Application, personal luxury dominated with approximately 68.70% in 2025; experiential luxury is the fastest-growing application at a CAGR of 7.80%.

-

By Distribution Channel, store-based led with approximately 62.50% in 2025; non-store-based is the fastest-growing at a CAGR of 7.04%.

By Group, women dominate, men are expected to grow fastest

Women retained the dominant position with approximately 58.50% of the luxury fashion market in 2025, reflecting the historical concentration of luxury fashion product development, marketing investment, and retail infrastructure in the women's category where the luxury industry's most culturally prominent product categories including haute couture, ready-to-wear, handbags, and fine jewelry have been concentrated since the origins of modern luxury fashion in the nineteenth-century Parisian couture houses whose customer base was exclusively female. The women's luxury fashion market commands the highest average transaction values across all luxury categories through the combination of premium handbag pricing from Louis Vuitton, Chanel, Hermès, and their competitors whose flagship bag silhouettes command five to six figure price points, luxury ready-to-wear season collections that sustain twice-annual purchasing cycles among the most fashion-engaged luxury consumers, and the fine jewelry and watch categories whose investment dimensions sustain high-value purchases that extend beyond fashion motivation into asset acquisition.

Men is the fastest-growing segment at a CAGR of 7.80% through 2035, driven by the structural expansion of the luxury menswear and accessories market that has accelerated over the past decade as younger male consumers raised in an era of streetwear brand consciousness and social media fashion culture have developed luxury brand awareness and purchasing motivation that their generational predecessors largely lacked. The convergence of luxury fashion and streetwear aesthetics through high-profile brand collaborations including Louis Vuitton's Virgil Abloh era, Gucci's Alessandro Michele-era eclecticism, and Balenciaga's luxury streetwear positioning has created entry points for younger male luxury consumers who engage with luxury fashion through cultural reference points that speak to their experience rather than requiring the old-money luxury vocabulary that defined men's luxury fashion access for previous generations.

By Type, clothing & apparel dominates, accessories are expected to grow fastest

Clothing and apparel retained the dominant type position with approximately 52.40% of the luxury fashion market in 2025, representing the category's original and definitive commercial foundation in the Parisian couture house system whose seasonal ready-to-wear collections set the design direction that flows through the entire luxury fashion ecosystem. The luxury apparel category's commercial strength reflects both its highest absolute spending position among luxury product types and the fashion system's twice-annual new collection structure that creates recurring purchase occasions for the most fashion-engaged luxury consumers who renew wardrobe elements each season in response to evolving brand aesthetic direction. Premium outerwear, suiting, and leather goods in the apparel category command particularly strong demand from the established luxury consumer base whose investment in lasting wardrobe pieces at premium price points is sustained by the category's combination of functional clothing utility and brand identity expression.

Accessories are the fastest-growing type at a CAGR of 7.60% through 2035, as the luxury accessories category including handbags, small leather goods, belts, scarves, and sunglasses provides the most accessible entry points to luxury brand ownership. The handbag's extraordinary cultural centrality to luxury fashion brand identity, where specific silhouettes including the Hermès Birkin and Kelly, Chanel 2.55, Louis Vuitton Speedy, and Gucci Horsebit Bag function simultaneously as fashion statements, status signals, and investment assets whose waiting lists and resale premiums create scarcity-driven desirability that sustains premium pricing across generational transitions in the brand's consumer base.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.4% |

|

Europe |

France |

34.6% |

|

Asia Pacific |

China |

52.3% |

|

Middle East & Africa |

UAE |

38.7% |

|

Latin America |

Brazil |

43.2% |

North America Luxury Fashion Market Insights

North America is the world's second-largest luxury fashion market by revenue, with the United States accounting for approximately 85.4% of North American revenues as the single country with the world's highest absolute number of ultra-high-net-worth individuals and the most extensive luxury retail infrastructure outside Europe. The U.S. luxury market's resilience through the luxury sector's post-pandemic demand normalization and the 2024 aspirational consumer pullback that affected European luxury houses' less affluent customer segments demonstrates the structural demand depth that the U.S. concentration of genuine high-net-worth consumers provides, where luxury spending motivation derives from wealth effect confidence rather than income stretch that makes it more resistant to macroeconomic uncertainty than aspirational market luxury consumption.

Europe Luxury Fashion Market Insights

Europe is the global luxury fashion market's largest region and its cultural and commercial heartland, where the concentration of the world's most prestigious luxury fashion houses in Paris and Milan and the surrounding geographic cluster of European luxury manufacturing excellence in French and Italian ateliers, leather goods workshops, textile mills, and accessory factories creates a heritage production ecosystem whose authenticity and craftsmanship credentials underpin the premium positioning of European luxury fashion globally. France accounts for approximately 34.6% of European luxury fashion revenues through its concentration of the most commercially powerful luxury fashion houses including Louis Vuitton, Chanel, Hermès, Christian Dior, Givenchy, Balenciaga, and Saint Laurent whose combined global revenues represent a substantial proportion of the entire global luxury fashion market.

Asia Pacific Luxury Fashion Market Insights

Asia Pacific is the fastest-growing luxury fashion market, anchored by China's position as the world's largest single national luxury consumer market by purchasing power when including mainland China purchases alongside Chinese tourist purchases in European and Asian luxury retail destinations, combined with the rapid development of luxury fashion consumer bases in South Korea, Japan, India, Southeast Asia, and Australia whose growing affluent populations are increasingly engaging with luxury fashion as a primary form of aspirational consumer expression. China accounts for approximately 52.3% of Asia Pacific luxury fashion revenues through its combination of the world's fastest-growing high-net-worth population, the cultural alignment of luxury brand ownership with Chinese social status signaling norms, and the extraordinary influence of Chinese consumer spending on European luxury house financial performance whose China revenue dependency has become a defining strategic risk and opportunity for every major luxury group.

MEA & Latin America Luxury Fashion Market Insights

The Middle East and Africa and Latin America are growing luxury fashion markets where Gulf Cooperation Council affluent consumers represent an important and growing luxury spending segment, particularly for statement clothing and accessories that feature prominently in social and formal occasions, and where the Latin American luxury market is developing through the growth of Brazil's domestic wealthy consumer class and the expansion of luxury brand retail networks in major Latin American metropolitan markets. UAE leads MEA luxury fashion revenues at approximately 38.7% of regional revenues through its combination of the region's highest per-capita luxury spending, the extraordinary retail infrastructure of Dubai's luxury malls and branded flagship stores, and the luxury tourism destination positioning that attracts high-spending international visitors whose luxury purchases in Dubai contribute to the UAE's luxury retail revenue base. Brazil leads Latin American revenues at approximately 43.2% through its established luxury retail market in Sao Paulo and Rio de Janeiro where major European luxury houses maintain flagship boutiques serving the country's substantial wealthy consumer class.

Market Dynamics

Growth Drivers: Rising global high-net-worth population expanding the core luxury consumer base

The primary structural growth drivers for the luxury fashion market are the sustained global expansion of the high-net-worth and ultra-high-net-worth population across all major regions, but most significantly across Asia Pacific where the creation of new wealth through technology entrepreneurship, real estate appreciation, and financial market participation is bringing millions of new genuinely affluent consumers into the luxury fashion market annually at income levels that support regular luxury purchasing rather than the occasional aspirational purchase that characterizes the aspirational consumer segment's luxury engagement. The progressive digitization of luxury brand consumer relationships through brand e-commerce, social media content strategy, influencer marketing, and digital clientele tools is simultaneously broadening the geographic reach of luxury brand awareness and aspiration to consumer segments in emerging markets that lack physical luxury retail access, and improving conversion efficiency among already-aware consumers by creating digital pathways to purchase that complement rather than replace the physical luxury retail experience.

Restraints: Aspirational consumer pullback in response to economic uncertainty reducing the mid-tier luxury segment's volume

A significant restraint on the luxury fashion market is the sensitivity of the aspirational consumer segment, which represents a substantial proportion of volume purchasing in the accessible luxury entry price tiers, to economic uncertainty and consumer confidence deterioration, where the combination of elevated interest rates, housing affordability concerns, and employment uncertainty that characterized several major markets in 2023 and 2024 led to meaningful spending pullbacks among the lower-income luxury consumers who stretch their budgets to participate in luxury fashion rather than the genuinely wealthy consumers whose luxury spending is supported by asset wealth rather than monthly income. Counterfeiting of luxury brands at scale through organized manufacturing in unregulated jurisdictions and distribution through digital marketplace platforms remains a structural threat to luxury brand exclusivity whose commercial and reputational damage to leading luxury houses is estimated to cost the global luxury industry tens of billions of dollars annually.

Opportunities: Resale market integration enabling circular luxury economics and experience-based luxury brand extension creating new premium revenue streams

The strategic integration of pre-owned luxury market access into brand-owned resale programmes, where luxury houses including Burberry, Stella McCartney, and Kering-owned Gucci have launched authenticated pre-owned product sales through brand-controlled channels, represents an opportunity to capture commercial participation in the secondary market that has historically accrued entirely to third-party resale platforms rather than the brands whose value creation underpins the resale economy. Brand-operated pre-owned programmes simultaneously generate direct revenue from secondary market transactions, maintain brand control over product authentication and presentation quality that protects brand equity, and enable the circular economy narrative that sustainable luxury purchasing credentials increasingly require from the most environmentally conscious affluent consumer segments.

Recent Developments:

-

2025: LVMH reported sustained growth across its Fashion & Leather Goods division anchored by Louis Vuitton and Christian Dior, with particular strength in the brand's most exclusive product tiers and continued outperformance in the United States and Japan markets that demonstrated the luxury spending resilience of the most genuinely affluent consumer segments relative to the more volatile aspirational consumer base that drove post-pandemic normalisation.

-

2025: Kering implemented accelerated transformation programmes across its luxury brand portfolio following a period of underperformance relative to LVMH peers, with Gucci's new creative direction under Sabato De Sarno completing its first full season of collections and early commercial reception data from major retail markets informing the brand's multi-year revival strategy.

-

2025: Chanel confirmed continued private luxury brand strategy with new flagship boutique openings in major Asian markets including Singapore and Seoul, maintaining its positioning as the most commercially successful privately held luxury fashion house whose selective distribution and premium pricing discipline has sustained extraordinary brand equity value independent of stock market performance pressures faced by publicly traded luxury group peers.

Luxury Fashion Market Key Players are:

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

Compagnie Financière Richemont SA

-

Chanel S.A.

-

Hermes International S.A.

-

Prada S.p.A.

-

Burberry Group plc

-

Capri Holdings Limited

-

Tapestry Inc.

-

Ralph Lauren Corporation

-

Moncler S.p.A.

-

Hugo Boss AG

-

Salvatore Ferragamo S.p.A.

-

Ermenegildo Zegna

-

Tod’s S.p.A.

-

Versace

-

Dolce & Gabbana S.r.l.

-

Balenciaga

-

Saint Laurent

-

Bottega Veneta

Luxury Fashion Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 301.58 Billion |

| Market Size by 2035 | USD 454.10 Billion |

| CAGR | CAGR of 4.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Group (Women, Men, Unisex) • By Type (Clothing & Apparel, Footwear, Accessories) • By Application (Personal Luxury, Gifting, Experiential Luxury) • By Distribution Channel (Store-Based, Non-Store-Based) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | LVMH Moët Hennessy Louis Vuitton SE, Kering SA, Compagnie Financière Richemont SA, Chanel S.A., Hermes International S.A., Prada S.p.A., Burberry Group plc, Capri Holdings Limited, Tapestry Inc., Ralph Lauren Corporation, Moncler S.p.A., Hugo Boss AG, Salvatore Ferragamo S.p.A., Ermenegildo Zegna, Tod’s S.p.A., Versace, Dolce & Gabbana S.r.l., Balenciaga, Saint Laurent, Bottega Veneta |

Frequently Asked Questions

Europe dominated the luxury fashion market in 2025, as the historic home and production hub of the world's most prestigious luxury fashion houses.

Women dominated with approximately 58.50% of revenues in 2025.

Rising global high-net-worth population expanding the core luxury consumer base combined with digital channel democratization broadening aspirational luxury access.

The luxury fashion market is expected to grow at a CAGR of 4.24% from 2026 to 2035.

Get in Touch