Maritime Cybersecurity Market Report Scope & Overview:

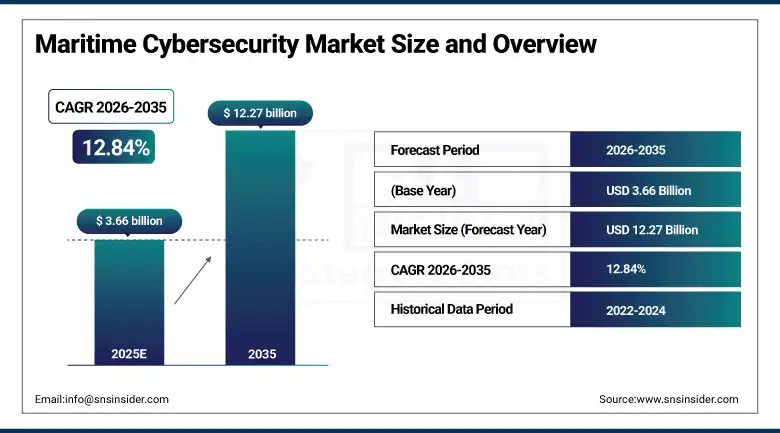

Maritime Cybersecurity Market was valued at USD 3.66 billion in 2025 and is expected to reach USD 12.27 billion by 2035, growing at a CAGR of 12.84% from 2026–2035.

The global Maritime Cybersecurity Market is experiencing a fundamental transformation in its strategic importance as the digitisation of maritime operations accelerates from incremental technology adoption to comprehensive digital-physical integration across vessel navigation, cargo management, port operations, fleet monitoring, and supply chain visibility systems that simultaneously enhance operational efficiency and dramatically expand the cyber-attack surface that malicious state and non-state actors can exploit. Maritime transport carries over 80% of global trade by volume, and the maritime industry's progressive adoption of connected technologies including the Internet of Things sensors for cargo condition monitoring, autonomous navigation assistance systems, satellite-based vessel tracking, integrated bridge systems, electronic chart display and information systems, and port community systems creates a vastly interconnected digital infrastructure that was largely absent a decade ago and has not been secured at the pace of its deployment. The maritime industry experienced a 900% increase in cyber-attacks on operational technology systems between 2017 and 2022 according to Naval Dome analysis, and high-profile incidents including the 2017 NotPetya ransomware attack causing an estimated USD 300 million loss to Maersk, GPS spoofing incidents disrupting vessel navigation in contested maritime zones, and ransomware attacks on major port systems have established the existential operational and financial risk of inadequate maritime cyber defence. Regulatory frameworks including the International Maritime Organization's MSC-FAL.1/Circ.3 guidelines requiring cyber risk management incorporation in ship safety management systems by 2021, the U.S. Coast Guard's maritime cyber risk management regulations, and the EU's NIS2 Directive requirements for critical infrastructure cybersecurity are progressively converting maritime cybersecurity from a voluntary best practice into a mandatory compliance requirement.

A CAGR of 12.84% in the period of 2026 to 2035 within the Maritime Cybersecurity Market can be attributed to the growing importance of protecting the maritime digital infrastructure that has control over billions of dollars worth of transactions taking place through international maritime business, whereby a cyber-attack against the port management systems, the vessel navigation software, or the cargo logistics platform would lead to major disruptions or even a collapse in the supply chain process for those economies relying heavily on maritime business for importing their oil and other necessities of life. This would include such product developments as January 2025 Cydome announcement of full EDR capabilities in their maritime cybersecurity software as well as their partnership with MarineNet for ClassNK-approved cybersecurity solution integration.

Maritime Cybersecurity Market Size and Forecast

-

Market Size in 2025: USD 3.667 Billion

-

Market Size by 2035: USD 12.27 Billion

-

CAGR: 12.84% from 2026 to 2035

-

Forecast Period: 2026–2035

-

Base Year: 2025

-

Historical Data: 2022–2024

To Get more information On Maritime Cybersecurity Market - Request Free Sample Report

Maritime Cybersecurity Market Trends

-

Rapid deployment of AI-powered threat detection and anomaly monitoring systems across vessel onboard networks and port management systems that provide continuous behavioural baseline monitoring capable of detecting ransomware deployment, GPS spoofing attacks, and unauthorised system access at speeds that human security operations cannot match.

-

Growing adoption of zero-trust network architecture in maritime environments, replacing traditional perimeter-based security approaches that assumed vessel and port network interiors were trusted with continuous identity verification, device authentication, and minimal-privilege access enforcement across all users and systems.

-

Accelerating integration of OT cybersecurity frameworks specifically designed for maritime industrial control systems including propulsion management, ballast control, cargo pumping, and navigation, where standard IT cybersecurity tools cannot safely interact with real-time control systems without risking operational disruption.

-

Rising adoption of satellite-delivered managed security services for maritime vessels that provide continuous monitoring, threat intelligence, and incident response capabilities to ships on international voyages where shore-based security operations centres provide 24/7 maritime cyber defence support.

-

Growing ship classification society engagement with maritime cybersecurity certification, with DNV GL, Lloyd's Register, ClassNK, and Bureau Veritas developing cyber-resilient ship notation programmes that validate vessel cybersecurity posture against defined technical standards.

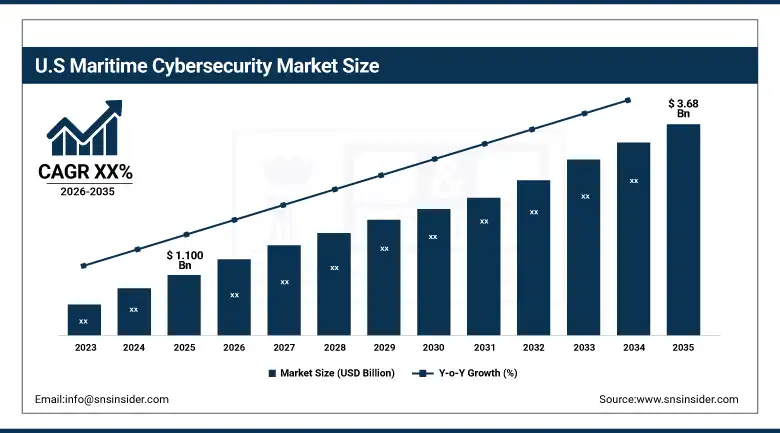

U.S. Maritime Cybersecurity Market was valued at approximately USD 1.100 billion in 2025 and is expected to reach approximately USD 3.68 billion by 2035, driven by stringent Coast Guard regulations, extensive commercial shipping operations, and the world's largest strategic naval presence.

The U.S. is considered the most important commercial and strategic maritime cybersecurity market in the world because the country features the most developed network of commercial ports that support the biggest national economy in the world along with the need for the highest level of cyber defense technologies to be used in securing the country's nuclear-powered ships and its navy's networks. The regulations adopted by the U.S. Coast Guard and the U.S. Coast Guard's maritime cybersecurity standards for high-capacity fixed facilities, together with the 2021 executive order that assigned the U.S. Coast Guard with the task of ensuring cybersecurity in the maritime environment, have provided an enforceable framework which forces all leading American shipping firms to use cybersecurity programs.

In March 2025, Microsoft announced the launch of Azure Maritime Security, a product line designed to protect shipboard IoT, navigation, and onboard networks, delivering integrated threat detection and response for commercial fleets. This product launch by the world's largest enterprise cloud platform provider into the maritime-specific cybersecurity market confirms that maritime cybersecurity has crossed the threshold from a niche specialty market into a mainstream enterprise security investment category, creating the competitive dynamics and commercial scale that will sustain exceptional maritime cybersecurity market growth through the 2026 to 2035 forecast period.

Maritime Cybersecurity Market Segment Insights

-

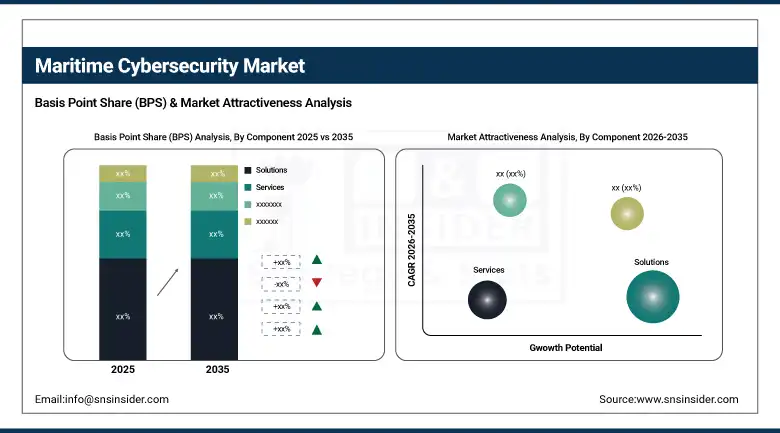

According to Component, Solutions dominated in 2025, holding approximately 70% of global revenues, driven by widespread adoption of integrated maritime cybersecurity platforms providing comprehensive threat detection, prevention, and response capabilities; Services is expected to grow at the fastest CAGR of approximately 13.1% from 2026 to 2035 driven by escalating demand for managed security services, professional consulting, and incident response.

-

In terms of Security Type, Network Security dominated with approximately 33% revenue share in 2025, reflecting the critical importance of protecting maritime network infrastructure connecting vessels, port facilities, and cargo management systems; Operational Technology Security is expected to grow at the fastest CAGR driven by increasing cyber risks to shipboard control systems.

-

By Deployment, On-Premises dominated in 2025 for vessel-based security systems; Cloud is the fastest-growing deployment mode as shore-based security operations centres and managed service providers adopt cloud-delivered maritime security analytics and monitoring.

-

By Organization Size, Large Enterprises dominated with approximately 70.81% of revenues in 2025 through their complex fleet operations and regulatory compliance requirements; Small and Medium Enterprises are expected to grow at the fastest CAGR of approximately 13.2% driven by rising affordable cloud-delivered cybersecurity solutions accessible to smaller shipping and port operators.

-

By End-User, Commercial Shipping dominated with approximately 42.19% of revenues in 2025; Oil and Gas and Offshore is one of the fastest-growing end-users through the extreme cyber risk exposure of offshore platforms controlling critical energy infrastructure.

Maritime Cybersecurity Market Segment Analysis

By Component: Solutions dominate, Services grows fastest

Solutions retained the dominant component position in the Maritime Cybersecurity Market in 2025 with approximately 70% of global revenues, driven by the widespread adoption of integrated maritime cybersecurity platforms providing comprehensive threat detection, intrusion prevention, identity and access management, encryption, and incident response capabilities specifically designed for maritime operational environments. Maritime cybersecurity solutions must address unique technical challenges including the segmented network architecture of vessel OT and IT systems, the variable satellite bandwidth constraints affecting real-time monitoring data transmission, the crew rotation patterns that create recurring insider threat exposure through removable media and personal device connectivity, and the global roaming nature of vessels transiting through diverse national cyber threat environments. Leading maritime cybersecurity solution providers including Fortinet, Cisco, CrowdStrike, Darktrace, and maritime-specialist companies including Naval Dome, CyberOwl, and Cydome are continuously advancing their platform capabilities to address the evolving threat landscape facing digitised maritime operations.

Services is projected to grow at the fastest component CAGR of approximately 13.1% through 2035, driven by the maritime industry's recognition that sophisticated, continuously evolving cyber threats require specialist security expertise that shipping companies, port operators, and offshore platform operators cannot develop and maintain in-house at the depth and currency required for effective defence. Maritime cybersecurity services encompass managed security operations centre monitoring of vessel and port networks, professional consulting for cybersecurity risk assessment, penetration testing and vulnerability assessment, incident response and forensic investigation, and training programme delivery for maritime personnel. The growth of vessel-based managed security services, where specialist maritime cybersecurity firms provide remote 24/7 monitoring and incident response for ships on international voyages, represents the most rapidly expanding maritime cybersecurity service category.

By Security Type: Network Security dominates, OT Security grows fastest

Network Security retained the dominant security type position in 2025 with approximately 33.2% of revenues, reflecting the foundational role of network security infrastructure in protecting the communications fabric that connects vessel IT systems, bridge navigation networks, cargo management systems, and shore-based operations centres across the diverse and often untrusted network environments that maritime operations traverse. Maritime vessel networks present unique security challenges including the use of VSAT and marine very high frequency communication links with variable bandwidth and security characteristics, the need to segment operational technology network traffic from crew welfare internet access on the same underlying satellite bandwidth, and the absence of physical network perimeter boundaries that exist in shore-based enterprise environments. Firewall, intrusion detection, network traffic analysis, and secure gateway technologies designed specifically for maritime network architectures are the largest product categories within the network security segment.

Operational Technology Security is predicted to record the highest growth rate among all types of maritime security due to the realization within the maritime industry that cyber-attacks on the ship propulsion control systems, ballast control systems, navigation systems, and cargo pumping systems could result in a safety hazard and operational disaster that goes beyond the damage that is typically caused by a simple IT security data breach. The maritime operational technology systems such as programmable logic controllers, distributed control systems, and maritime Internet of Things sensors are not designed for security and as such pose various security gaps like out-of-date operating systems that are unable to apply security patches, hard coded default authentication, and lack of encryption. The convergence of IT and OT systems in modern ships which have their bridge navigation systems integrated into their corporate shipping management systems means that air-gap isolation no longer exists, and hence the need for maritime OT cybersecurity.

By End-User: Commercial Shipping dominates, Oil and Gas and Offshore grows rapidly

Commercial Shipping retained the dominant end-user position in the Maritime Cybersecurity Market in 2025 with approximately 42.19% of revenues, reflecting the global shipping fleet's enormous scale encompassing approximately 100,000 commercial vessels carrying the world's trade, the extensive digitisation of vessel operations that creates the cyber-attack surface, and the growing regulatory pressure from IMO requirements and flag state enforcement that compels shipping companies to invest in documented cybersecurity management systems. Major global container shipping lines, bulk cargo operators, tanker fleets, and cruise companies each operate complex digital ecosystems spanning vessel management systems, port interface platforms, cargo tracking, crew management, and commercial operations that require comprehensive cybersecurity protection across multiple interconnected system categories.

Oil and Gas and offshore represents one of the fastest-growing end-user segments through 2035, driven by the extreme cyber risk exposure of offshore drilling platforms and production facilities where successful cyber-attacks on process control systems can cause catastrophic physical consequences including well blowouts, fire and explosion, and uncontrolled hydrocarbon release that dwarf the financial consequences of conventional data breach incidents. The offshore oil and gas sector operates some of the world's most complex and safety-critical OT systems, with programmable logic controllers and distributed control systems managing drilling operations, pressure management, fire and gas detection, and emergency shutdown systems that must be protected from cyber compromise that could override safety systems. The sector's historically strong safety culture is driving systematic application of the same risk management rigour to cybersecurity that decades of offshore safety regulation have established for physical process safety.

Maritime Cybersecurity Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~82% |

|

Europe |

Norway |

~27% |

|

Asia Pacific |

Singapore |

~30% |

|

Middle East & Africa |

UAE |

~32% |

|

Latin America |

Brazil |

~43% |

North America Maritime Cybersecurity Market Insights

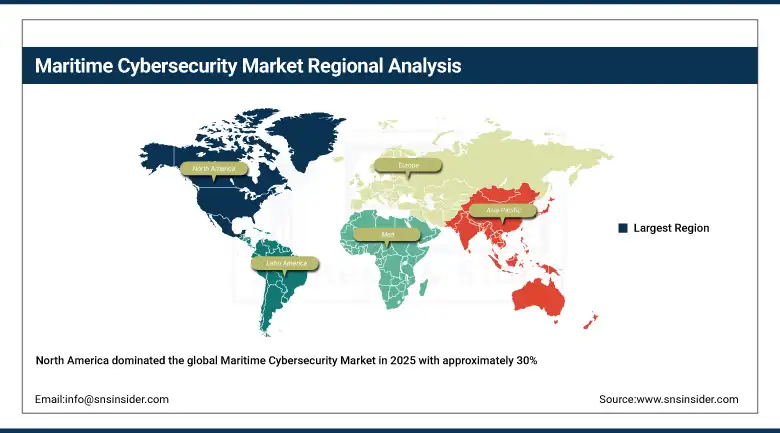

North America dominated the global Maritime Cybersecurity Market in 2025 with approximately 30% of global revenues, led by the United States which accounted for approximately 82% of North American revenues. U.S. market leadership is driven by the U.S. Coast Guard's active maritime cybersecurity regulatory enforcement, the world's most extensive commercial port infrastructure across major gateway ports, the U.S. Navy and Department of Defense's substantial maritime cyber defence investment, and the concentration of leading cybersecurity technology companies providing maritime-specific solutions. Canada contributes through its extensive Arctic maritime operations and major Pacific and Atlantic port facilities requiring cybersecurity protection.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Maritime Cybersecurity Market Insights

The Asia Pacific will witness the highest regional CAGR at around 13.1% by 2035 due to the high number of the most throughput-efficient ports of the world situated in the region, strong investments in the smart ports' digitalization in China, Singapore, South Korea, and Japan, and an increased exposure to cyber threats from nation-state threat actors actively operating in the Asia Pacific maritime environment. Singapore, which boasts the second largest container port of the world and serves as a prominent maritime center, with a sophisticated cybersecurity framework set up by the port authorities, is leading ASEAN maritime cybersecurity adoption efforts. China, with its substantial domestic shipping fleet and key port companies such as COSCO and SIPG, is heavily investing in maritime cybersecurity.

Europe Maritime Cybersecurity Market Insights

Europe is another important maritime cybersecurity market driven by the NIS2 Directive introduced by the EU mandating cybersecurity requirements for critical maritime infrastructure, the IMO guidelines which the European Maritime Safety Agency is championing among the EU member states, and the existence of major maritime players such as Norway, Greece, Germany, Denmark, and the Netherlands which have sizable fleets and efficient port infrastructures to fuel market demands. The Norwegian dominance of major shipping companies in the global scene, the Port of Rotterdam smart port facilities in the Netherlands, and the supremacy of Greece as the largest merchant fleet holder in the world constitute the biggest European maritime cybersecurity demand base.

Middle East & Africa and Latin America Maritime Cybersecurity Market Insights

MEA and Latin America are growing maritime cybersecurity markets, driven by the region's critical maritime trade infrastructure including the Suez Canal, Strait of Hormuz, and major Gulf energy export terminal complexes whose successful cyber-attacks would have global economic consequences. The UAE leads MEA adoption through Jebel Ali Port's world-class smart port investment and the Emirates' sophisticated cybersecurity regulatory environment. Brazil leads Latin American revenues through its major export port infrastructure for commodities including Santos, Paranagua, and Tubarao, which collectively handle hundreds of millions of tonnes of agricultural and mineral exports requiring cybersecurity protection.

Maritime Cybersecurity Market Growth Drivers:

-

Escalating maritime cyber-attack frequency and sophistication combined with mandatory IMO and national regulatory compliance requirements driving systematic cybersecurity investment across the global shipping and port industry

The primary structural growth drivers for the Maritime Cybersecurity Market are the escalating frequency, sophistication, and operational impact of cyber-attacks targeting maritime infrastructure, combined with the progressive mandatory regulatory framework requiring documented cybersecurity risk management across the global fleet and port operator community. The maritime industry's rapid digital transformation creating an expanding attack surface, combined with the sector's historical underinvestment in cybersecurity relative to its operational technology complexity, creates a substantial vulnerability remediation requirement across tens of thousands of vessels and hundreds of ports that generates sustained demand for maritime cybersecurity solutions and services through the forecast period.

Cydome's January 2025 introduction of a full Endpoint Detection and Response solution integrated into its maritime cybersecurity platform, delivering advanced capabilities for continuous monitoring, automated threat mitigation, and forensic analysis across fleet-wide assets, combined with Cydome's June 2025 strategic partnership with Marine Net integrating ClassNK-approved cybersecurity solutions into a unified IT and security management system, confirm the accelerating maturation of the maritime cybersecurity product ecosystem. These product developments demonstrate that purpose-built maritime cybersecurity technology is achieving the operational maturity and classification society certification status that shipping companies require before committing to enterprise-wide deployment across their vessel fleets through the 2026 to 2035 forecast period.

Maritime Cybersecurity Market Restraints

-

Connectivity limitations constraining real-time monitoring on vessels, legacy OT system incompatibility with standard cybersecurity tools, and maritime industry cultural resistance to cybersecurity investment

A significant restraint on the Maritime Cybersecurity Market is the variable and bandwidth-constrained satellite connectivity of ocean-going vessels that limits the volume of security monitoring data that can be transmitted to shore-based security operations centres in real time, constraining the effectiveness of cloud-delivered managed security services for ships on international voyages where security-critical network traffic monitoring generates more data than affordable satellite bandwidth can transmit. Legacy OT systems on older vessels running outdated operating systems that cannot accept security patches, combined with proprietary industrial protocols that standard cybersecurity tools cannot safely inspect, create technical barriers to comprehensive vessel cybersecurity implementation that require expensive custom integration work. The maritime industry's historically cost-focused culture, where cybersecurity investment has traditionally been evaluated against freight rate economics rather than risk-adjusted return, creates institutional resistance to cybersecurity budget allocation beyond minimum regulatory compliance requirements.

Maritime Cybersecurity Market Opportunities

-

Autonomous vessel cybersecurity requirements, smart port digital infrastructure protection, and maritime cybersecurity insurance premium incentives

The development of autonomous and semi-autonomous vessel technology, where remote command and control systems enable crew-reduced or unmanned vessel operation, creates a maritime cybersecurity category where successful cyber-attacks on autonomous vessel systems can cause immediate physical navigation hazards, creating an existential cybersecurity requirement for autonomous maritime operations that will command the highest per-vessel cybersecurity investment premiums in the market. Smart port digital infrastructure investment, where port community systems, automated container handling equipment, and real-time cargo tracking platforms are being comprehensively digitised in major gateway ports, is creating a substantial port-side maritime cybersecurity market separate from the vessel-based segment. The maritime insurance market's emerging interest in cybersecurity performance-based premium adjustment, where shipping companies demonstrating robust documented cybersecurity programmes command lower cyber insurance premiums, creates financial incentives for cybersecurity investment beyond minimum regulatory compliance.

Recent Developments:

-

June 2025: Cydome entered a strategic partnership with Marine Net to integrate its ClassNK-approved cybersecurity solutions into Marine Net’s MN-Station platform, providing large maritime enterprises with a cohesive IT and security management system tailored to vessel and shore-based operations.

-

March 2025: Microsoft launched Azure Maritime Security, a dedicated product line designed to protect shipboard IoT, navigation, and onboard networks, delivering integrated threat detection and response for commercial fleets from the world's largest enterprise cloud platform provider.

-

January 2025: Cydome introduced a full Endpoint Detection and Response solution integrated into its maritime cybersecurity platform, delivering advanced continuous monitoring, automated threat mitigation, and forensic analysis capabilities across fleet-wide maritime assets.

-

2025: Fortinet expanded its FortiGate security appliance range with maritime-hardened variants designed for the extreme temperature, vibration, and humidity conditions of vessel bridge environments, providing consolidated firewall, intrusion prevention, and VPN capabilities in ruggedised marine-certified form factors.

-

2025: CyberOwl expanded its maritime threat intelligence platform with new vessel network anomaly detection capabilities using machine learning trained on maritime-specific operational technology network behaviour, enabling earlier detection of novel attacks that signature-based detection methods miss.

Maritime Cybersecurity Market Key Players

-

Fortinet Inc.

-

Cisco Systems Inc.

-

Northrop Grumman Corporation

-

Thales Group

-

BAE Systems plc

-

Kongsberg Gruppen ASA

-

Marlink SAS

-

Naval Dome Ltd.

-

Cydome Security Ltd.

-

CyberOwl Ltd.

-

ABS Group of Companies Inc.

-

Waterfall Security Solutions Ltd.

-

Raytheon Technologies Corporation

-

Honeywell International Inc.

-

L3Harris Technologies Inc.

-

Wärtsilä Corporation

-

Radiflow Ltd.

-

BlueVoyant LLC

-

ioXt Alliance

-

HENSOLDT AG

Maritime Cybersecurity Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.66 Billion |

| Market Size by 2035 | USD 12.27 Billion |

| CAGR | CAGR of 12.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Operational Technology Security, Others) • By Deployment (On-Premises, Cloud) • By Organization Size (Large Enterprises, Small and Medium Enterprises) • By End-User (Commercial Shipping, Ports and Terminals, Defense and Government, Oil and Gas and Offshore, Logistics and Supply Chain, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Fortinet Inc., Cisco Systems Inc., Northrop Grumman Corporation, Thales Group, BAE Systems plc, Kongsberg Gruppen ASA, Marlink SAS, Naval Dome Ltd., Cydome Security Ltd., CyberOwl Ltd., ABS Group of Companies Inc., Waterfall Security Solutions Ltd., Raytheon Technologies Corporation, Honeywell International Inc., L3Harris Technologies Inc., Wärtsilä Corporation, Radiflow Ltd., BlueVoyant LLC, ioXt Alliance, HENSOLDT AG |

Frequently Asked Questions

Ans: North America dominated with approximately 30% of global revenues in 2025, led by the United States with active Coast Guard cybersecurity regulatory enforcement, the world's most extensive commercial port infrastructure, U.S. Navy maritime cyber defence investment, and the concentration of leading cybersecurity technology companies providing maritime-specific solutions.

Ans: Operational Technology Security is expected to grow at the fastest CAGR through 2035, driven by maritime industry recognition that cyber attacks on vessel OT systems including propulsion control, ballast management, and navigation can cause catastrophic physical safety consequences, combined with the progressive elimination of air-gap isolation as IT and OT systems on modern smart vessels become interconnected.

Ans: Solutions dominated with approximately 70% of global revenues in 2025, driven by widespread adoption of integrated maritime cybersecurity platforms providing comprehensive threat detection, intrusion prevention, identity and access management, and incident response capabilities specifically designed for maritime operational environments.

Ans: The escalating frequency and sophistication of cyber attacks on maritime infrastructure including the 900% increase in OT cyber attacks between 2017 and 2022, combined with mandatory IMO cybersecurity requirements and national regulatory enforcement compelling systematic cybersecurity investment across the global fleet and port operator community, and the rapid digital transformation of maritime operations expanding the cyber attack surface.

Ans: The Maritime Cybersecurity Market was valued at USD 3.667 billion in 2025.

Ans: The Maritime Cybersecurity Market is expected to grow at a CAGR of 12.84% from 2026 to 2035.

Get in Touch