Medical Alert Systems Market Report Scope & Overview:

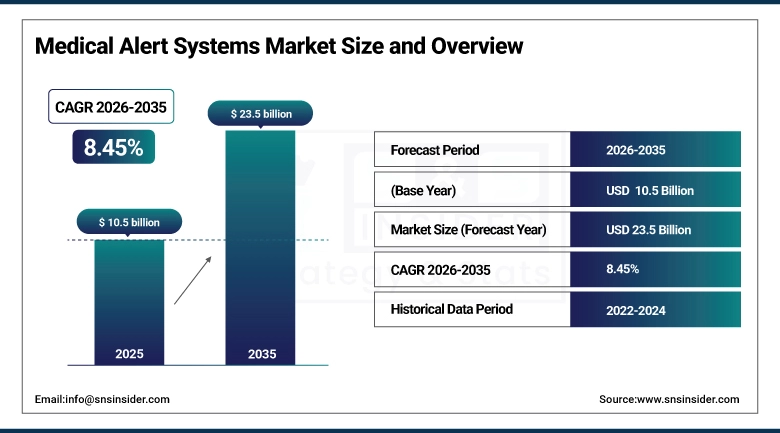

The Medical Alert Systems Market size was valued at USD 10.5 billion in 2025 and is expected to reach USD 23.5 billion by 2035, growing at a CAGR of 8.45% from 2026-2035.

A medical alert system is, in its simplest form, a button connected to help. But that simple description masks the profound autonomy that medical alert technology enables for the elderly individuals, chronic disease patients, and mobility-limited adults whose ability to call for help in an emergency is the difference between living independently at home and requiring supervised residential care. The market exists at the intersection of a demographic trend and a clinical reality that are both growing simultaneously: the global population over 75 is growing at 4% annually, and adults over 75 have a 30% annual probability of experiencing a fall making fall-related emergency response the primary clinical use case that sustains the market's fundamental demand. What has transformed the medical alert industry from a niche assistive technology into a mainstream consumer electronics growth market is the technology's evolution from basic landline-connected pendant buttons to GPS-enabled mobile systems that work anywhere on the cellular network, AI-powered fall detection that triggers alerts without requiring the user to press a button, and smartwatch integration that makes medical alert functionality invisible within the daily wearable technology that consumers already adopt.

The CDC's fall injury statistics document that falls are the leading cause of injury-related death among adults over 65 in the United States, with 36 million falls occurring annually and 3 million emergency department visits resulting from fall injuries. The National Council on Aging's fall prevention data shows that medical alert system users who fall receive emergency response within an average of 8 minutes versus 77 minutes for non-users who fall when alone a response time advantage that substantially reduces the serious secondary injury from prolonged time on the floor that elevates mortality risk in fall-related hospitalizations.

Market Size and Forecast

-

Market Size in 2025: USD 10.5 Billion

-

Market Size by 2035: USD 23.5 Billion

-

CAGR: 8.45% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Medical Alert Systems Market - Request Free Sample Report

Medical Alert Systems Market Trends

-

AI-powered passive fall detection using accelerometer and gyroscope data to automatically detect fall events without button press is expanding the user population served by medical alerts to include individuals with dementia, cognitive decline, or physical limitations that prevent reliable button activation.

-

Smartwatch-integrated medical alert functionality is making emergency response capability invisible within mainstream consumer wearable devices — Apple Watch's Emergency SOS and Fall Detection features represent the highest-volume deployment of medical alert capability in consumer technology history.

-

Telehealth platform integration is enabling medical alert monitoring centers to connect users with virtual nurse triage rather than immediately dispatching emergency services — improving clinical appropriateness of emergency response while reducing unnecessary 911 calls that strain emergency response systems.

-

Smart home integration with voice assistant platforms (Amazon Alexa Guard, Google Home) is extending medical alert capability into ambient monitoring that doesn't require wearing a device — particularly valuable for users who resist wearing visible pendant-style alert systems.

-

Medication adherence monitoring integration with medical alert platforms is enabling two-in-one aging-in-place solutions where the emergency response capability and medication management are bundled in a single subscription service.

-

Machine learning analysis of continuous activity and vital sign data is enabling proactive health deterioration detection — where unusual patterns in sleep quality, gait, and daily activity rhythm indicate developing health events before clinical symptoms appear.

-

Caregiver app integration providing family members with real-time location tracking, activity monitoring, and emergency notification creates a connected care network that improves the overall effectiveness of home-based elder care.

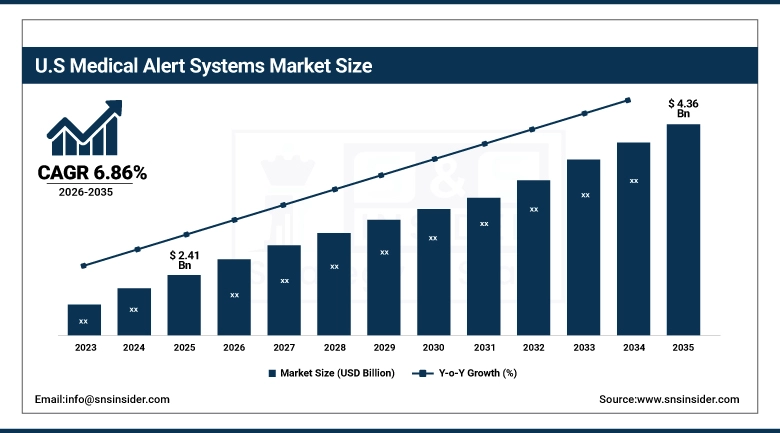

U.S. Medical Alert Systems Market Size Outlook:

The U.S. Medical Alert Systems Market was valued at USD 2.41 billion in 2025 and is expected to reach USD 4.36 billion by 2035, growing at a CAGR of 6.86% from 2026-2035. North America dominated the global Medical Alert Systems Industry, driven by the United States' combination of the world's largest elderly population in absolute terms, the most developed consumer medical alert brand ecosystem, and the cultural preference for aging-in-place independence that makes medical alert systems an emotionally compelling investment for elderly adults and their adult children. The U.S. market's commercial maturity is reflected in its brand diversity: Life Alert (whose 'I've fallen and I can't get up' campaign created nationwide brand recognition), ADT Medical Alert, Medical Guardian, LifeFone, and Bay Alarm Medical collectively serve millions of U.S. subscribers through both direct-to-consumer and healthcare provider referral channels. Medicare Advantage plans' increasing inclusion of medical alert system benefits — where members receive subsidized or free medical alert devices as preventive health benefit inclusions — is expanding access to the lower-income elderly population whose medical need is highest but whose out-of-pocket spending capacity is lowest.

AARP's 2024 Aging in Place survey documents that 77% of adults over 50 prefer to stay in their own home as they age — a preference that creates natural demand for safety technology including medical alert systems that make independent living safer. The National Institute on Aging documents that hip fractures following falls cost Medicare an average of USD 22,000 per patient in the year following injury — creating a documented healthcare cost savings argument for medical alert system adoption that Medicare Advantage plan actuaries are increasingly using to justify benefit inclusion.

Medical Alert Systems Market Segment Analysis

-

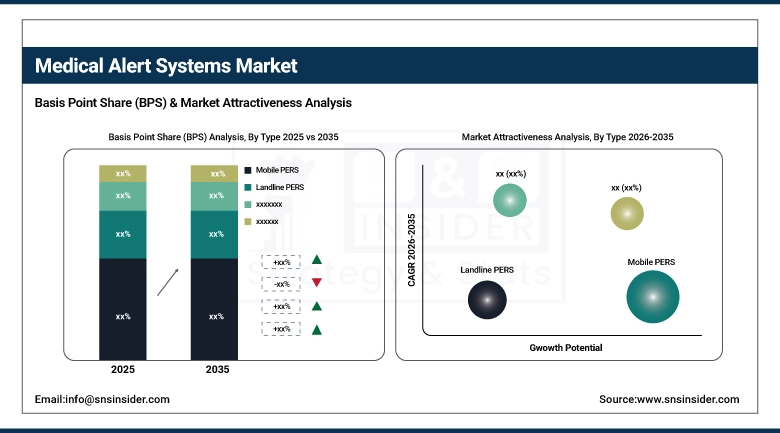

By Type, Mobile PERS dominated with 54.3% share in 2025; Standalone PERS growing at the fastest CAGR during the forecast period.

-

By End User, Home-Based Users dominated with 47.7% share in 2025 and also growing at the highest CAGR among end users.

By Type: Mobile PERS dominates at 54.3%, Standalone growing fastest

Mobile Personal Emergency Response Systems (PERS) held approximately 54.3% of the Medical Alert Systems Market in 2025, driven by the fundamental mobility advantage that GPS-enabled cellular-connected alert devices provide over their landline-tethered predecessors. A mobile PERS user is protected wherever they go — walking to the mailbox, driving to a doctor's appointment, or traveling to visit family in another city — rather than only within the radio range of a home base unit connected to a landline telephone. The mobile PERS market's commercial development has been driven by the cellular network's coverage expansion that makes GPS-tracked cellular devices practical for the nationwide mobility of older adults whose fall risk is equally present at home and in the community. Medical Guardian, Life Alert's mobile products, and Apple Watch's Emergency SOS have each contributed to mobile PERS adoption, creating a product category that has displaced the landline-based home systems that historically dominated the market.

Standalone PERS — systems that operate independently without requiring cellular connectivity to a base unit or landline connection — are growing at the fastest type CAGR, driven by the technology's ability to combine GPS, fall detection, two-way voice, and emergency response in a single wearable device without monthly service plan complications. Standalone PERS products — including Apple Watch Emergency SOS, Samsung Galaxy Watch's emergency calling, and dedicated medical alert smartwatches — are increasingly integrating medical alert functionality within mainstream consumer electronics that elderly users adopt for multiple purposes, reducing the stigma associated with dedicated medical alert pendant wearing that has historically limited adoption among image-conscious elderly adults. Landline PERS — the traditional home-based system whose help button communicates through a console connected to a telephone landline — retains a declining but still significant market segment among users who do not need mobile coverage and whose landline telephone provides reliable communication infrastructure that cellular connectivity cannot guarantee in all geographic locations.

By End User: Home-Based dominant at 47.7% and growing fastest

Home-Based Users held approximately 47.7% of the Medical Alert Systems Market in 2025, reflecting the primary use case that medical alert systems have historically addressed elderly adults living independently at home whose risk of fall-related injury is highest in the home environment where most of their time is spent. The home-based market's simultaneous dominance and highest-growth-rate status reflects the powerful demographic force of baby boomer aging 10,000 Americans turn 65 every day, and a significant proportion of this cohort will adopt medical alert technology within their first decade of Medicare eligibility as they experience their first fall events or healthcare provider recommendations. The aging-in-place preference that drives home-based medical alert demand is fundamentally an expression of independence users who choose home-based living with a medical alert system over supervised residential care are making an explicit statement that independence, even with safety assistance technology, is preferred over the dependency of institutional care.

Senior Living Facilities including independent living communities, assisted living facilities, and continuing care retirement communities represent a commercially significant institutional market segment where medical alert systems are deployed facility-wide as a safety infrastructure component rather than as individually purchased consumer products. Nurse call system manufacturers including Rauland, Jeron Electronic Systems, and Cornell Communications serve the institutional medical alert market with wired and wireless systems whose integration with facility communication infrastructure and resident monitoring platforms differs from the consumer product approach of home-based systems. Assisted Living Facilities are expected to grow at a particularly high CAGR as the number of assisted living residents grows with the aging population's transition from independent home living to supervised residential care.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

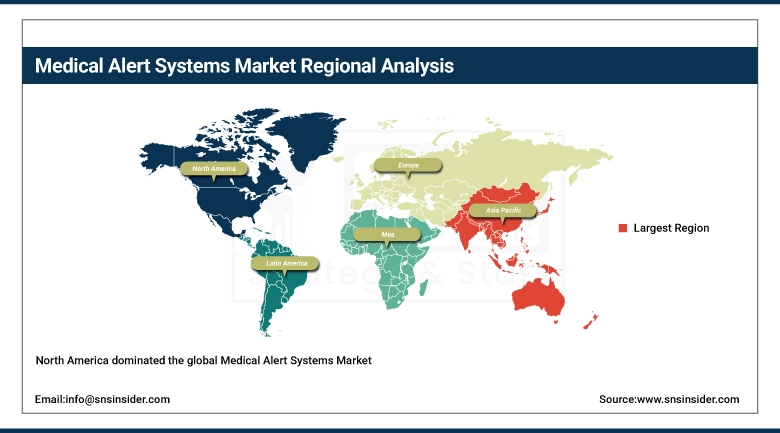

North America Medical Alert Systems Market Insights

North America dominated the global Medical Alert Systems Market, led by the United States' mature and commercially developed medical alert industry whose brand diversity, Medicare Advantage benefit integration, and physician recommendation patterns create a structured market development pipeline that no other national market approaches. The U.S. market's evolution from pure emergency response toward continuous health monitoring — where medical alert platforms are integrating activity data, heart rate monitoring, sleep quality analysis, and medication adherence tracking alongside their core emergency response function — is creating subscription service revenue that grows within existing user relationships and attracts health-conscious subscribers who would not have adopted traditional emergency response-only products.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Medical Alert Systems Market Insights

Asia Pacific is the fastest-growing regional Medical Alert Systems Industry, driven by Japan's extremely aged population with 29% of citizens over 65, the world's highest proportion China’s 260 million elderly adults whose government is investing heavily in elder care technology infrastructure, and South Korea and Australia's growing elder care technology adoption. Japan's government long-term care insurance system which subsidizes approved assistive technology including emergency response devices for elderly beneficiaries is creating structured public sector demand for medical alert systems that sustains the Japanese market's sophisticated product adoption. Companies including Secom, Huawei Health, and Xiaomi Smart Health are developing Asia-specific medical alert products that incorporate the design preferences, mobile payment integration, and connectivity infrastructure of Asian markets.

Europe Medical Alert Systems Market Insights

Europe's Medical Alert Systems Market is growing with the EU's aging demographic projected to have 30% of its population over 65 by 2050 and the EU's Active and Assisted Living Joint Programme which funds technology development and adoption support for elderly-oriented technology including medical alert systems. Germany, France, the UK, and the Nordic countries are the primary European markets, where national social care systems provide some level of assisted living support that includes emergency response equipment for eligible elderly beneficiaries. Tunstall Healthcare a UK-based medical alert provider is the European market leader whose products serve both consumer and social care sector markets across multiple EU member states.

MEA and Latin America Medical Alert Systems Market Insights

The Middle East's Medical Alert Systems Market is growing with the Gulf states' aging population and growing elder care awareness historically, Gulf culture's family-based elder care model has reduced demand for formal medical alert technology, but urbanization and nuclear family structure changes are creating conditions where technological supplementation of family monitoring is increasingly sought. Saudi Arabia's Vision 2030 healthcare and elder care components explicitly identify aging population support technology as an investment priority. Latin America's market is growing in Brazil and Mexico, where urbanization has separated extended family members who previously provided continuous monitoring for elderly relatives, creating demand for technology-based safety solutions that maintain independence while providing emergency response access.

Growth Drivers: Aging global population and aging-in-place preference driving sustained medical alert systems industry growth globally

The Medical Alert Systems Market's 8.45% CAGR is driven by the most reliable demographic trend in the developed world: the aging of the baby boom generation. The U.S. population over 75 — the age cohort with the highest fall risk and the greatest medical alert adoption propensity — will grow from 22 million in 2025 to over 35 million by 2035, creating a 60% expansion in the primary target market within the forecast period. The aging-in-place preference that 77% of adults over 50 express is the commercial engine of medical alert demand — each elderly adult who chooses to remain at home rather than enter residential care represents an addressable consumer for medical alert technology whose subscription relationship can sustain for years.

Restraints: Device adoption stigma and high false alarm rates creating medical alert systems market challenges for elderly users globally

The medical alert market's persistent challenge is the cultural stigma that many elderly adults attach to visible medical alert pendant wearing — which signals physical limitation, healthcare dependency, and age-related vulnerability in ways that independent-minded older adults resist. Studies consistently document that a significant proportion of medical alert system owners do not wear their devices consistently, despite purchasing them, because the social signal of pendant wearing conflicts with their self-image as capable, independent adults. Device manufacturers are actively addressing this stigma through smartwatch integration, jewelry-style pendant designs, and discreet wrist-worn formats — but the fundamental tension between visible safety devices and independence-focused self-presentation remains a market penetration barrier. High false alarm rates — where automatic fall detection algorithms trigger alerts during normal activities like sitting down quickly or bending over — create operational frustration for users and monitoring centers whose response to false alarms must be treated as genuine emergencies until confirmed otherwise.

Opportunities: Medicare Advantage benefit expansion and AI health monitoring integration creating significant medical alert systems market growth opportunities

Medicare Advantage plans' growing inclusion of supplemental benefits where the CMS allows MA plans to offer non-medical benefits that improve health outcomes and reduce care costs — represents the most commercially significant near-term growth opportunity in the medical alert market. As MA plans increasingly offer medical alert system subscriptions as a zero-premium supplemental benefit for qualifying members (those with fall risk documented in their health record), the addressable market expands from the subset of elderly adults willing and able to pay for medical alert subscriptions out of pocket to the entire MA-enrolled elderly population whose plan benefits include the device. Over 32 million Americans are enrolled in Medicare Advantage plans as of 2025, with plan benefit inclusion representing a potentially transformative channel that could triple medical alert market penetration relative to current out-of-pocket adoption rates.

Recent Developments:

-

2026: Apple Watch Series 12 introduced a new Emergency Response Coordination feature combining its existing fall detection and Emergency SOS with an AI-powered severity assessment that evaluates accelerometer, heart rate, blood oxygen, and ECG data to provide 911 dispatchers with a preliminary assessment of likely injury severity before emergency crews arrive reportedly reducing average emergency response scene preparation time by 4 minutes in partnered trauma center evaluations.

-

2025: Medical Guardian launched its ActiveProtect smartwatch the company's first smartwatch-form factor medical alert with 2-day battery life, LTE cellular connectivity independent of paired smartphone, 24/7 monitoring center subscription, AI fall detection, and heart rate irregularity alerts targeting the market segment of active seniors who resist pendant-style medical alerts but who would wear a fitness-style smartwatch that does not announce its medical alert function.

-

2025: UnitedHealth Group's UnitedHealthcare Medicare Advantage plans expanded medical alert system coverage to include a USD 25/month benefit credit applicable to any FCC-approved PERS device from a network of 12 partnered providers — creating a subsidized access pathway for its 7.8 million Medicare Advantage members that is expected to increase medical alert adoption in this population by an estimated 35% within two years of benefit implementation.

Medical Alert Systems Companies are:

-

Medical Guardian LLC

-

ADT Inc. (ADT Medical Alert)

-

Bay Alarm Medical

-

MobileHelp Inc.

-

Philips Lifeline (Philips)

-

Tunstall Healthcare Group

-

Lively (GreatCall)

-

Apple Inc. (Apple Watch Emergency SOS)

-

Alerto Inc.

-

Rescue Alert of Utah Inc.

-

ResponseNow (In The Home)

-

Nortek Security & Control

-

LogicMark LLC

-

Numera Inc.

-

Connect America Co. LLC

-

Petzl Inc.

-

Secom Co. Ltd.

-

Electronic Caregiver Inc.

Medical Alert Systems Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.5 Billion |

| Market Size by 2035 | USD 23.5 Billion |

| CAGR | CAGR of 8.45% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Landline PERS, Mobile PERS, Standalone PERS) • By End Use (Home-based Users, Nursing Home, Assisted living facilities, Hospices) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Life Alert Emergency Response Inc., Medical Guardian LLC, ADT Inc. (ADT Medical Alert), Bay Alarm Medical, LifeFone Services Inc., MobileHelp Inc., Philips Lifeline (Philips), Tunstall Healthcare Group, Lively (GreatCall), Apple Inc. (Apple Watch Emergency SOS), Alerto Inc., Rescue Alert of Utah Inc., ResponseNow (In The Home), Nortek Security & Control, LogicMark LLC, Numera Inc., Connect America Co. LLC, Petzl Inc., Secom Co. Ltd. |

Frequently Asked Questions

Ans: North America dominated; Asia Pacific is the fastest growing regional market.

Ans: Home-Based Users dominated with approximately 47.7% share and are also growing at the highest CAGR.

Ans: Mobile PERS dominated with approximately 54.3% share; Standalone PERS is growing fastest.

Ans: The Medical Alert Systems Market was valued at USD 10.5 billion in 2025.

Ans: The Medical Alert Systems Market is expected to grow at a CAGR of 8.45% from 2026 to 2035.

Get in Touch