Medical Collagen Market Report Scope & Overview:

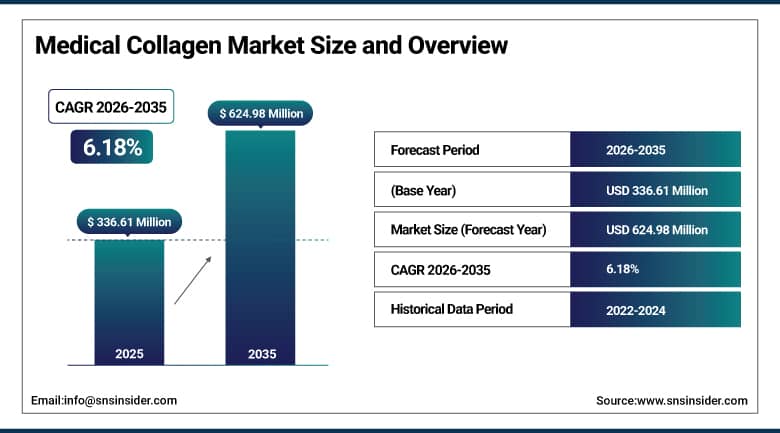

The Medical Collagen Market was valued at USD 336.61 Million in 2025 and is expected to reach USD 624.98 Million by 2035, growing at a CAGR of 6.18% from 2026–2035.

The global medical collagen market refers to the manufacturing and application of pure collagen obtained from bovine, porcine, marine, recombinant, and plant sources for pharmaceutical purposes. Collagen finds extensive use in tissue engineering, wound repair, orthopedics, cardiovascular surgeries, dentistry, and drug delivery systems. Growth of this market is expected on account of rising demands for regenerative medicine, higher incidence rates of chronic wounds and orthopedic conditions, and growing use of collagen materials in cosmetic and reconstructive surgeries. Developments in the technology associated with the manufacture of collagen products have contributed to the safety and functionality of these products along with better compliance with regulations.

In 2025, MiMedx advanced its HELIOGEN collagen product platform with Type I and III collagen matrices for tissue regeneration and wound care applications, offering improved handling and storage characteristics alongside enhanced wound healing outcomes. The product development reflects the commercial direction of medical collagen toward application-specific formulations whose clinical performance data differentiates premium medical collagen products from commodity alternatives across wound care, orthopedic, and surgical tissue repair procurement channels.

Market Size and Forecast:

-

Market Size in 2026E: USD 357.41 Million

-

Market Size by 2035: USD 624.98 Million

-

CAGR: 6.18% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Medical Collagen Market - Request Free Sample Report

Medical Collagen Market Trends:

-

Recombinant and synthetic collagen adoption is rising due to improved safety, consistency, and absence of animal-derived contamination risks.

-

Marine collagen demand is growing because of halal, kosher, and disease-free sourcing advantages over bovine alternatives.

-

3D bioprinting with collagen bioinks enables patient-specific tissue scaffolds for advanced regenerative medicine applications.

-

Self-assembling collagen scaffolds are improving wound healing and tissue regeneration by mimicking natural extracellular matrix structures.

-

Patent-driven innovation in collagen materials and drug delivery systems is supporting premium product differentiation and market growth.

U.S. Medical Collagen Market Outlook:

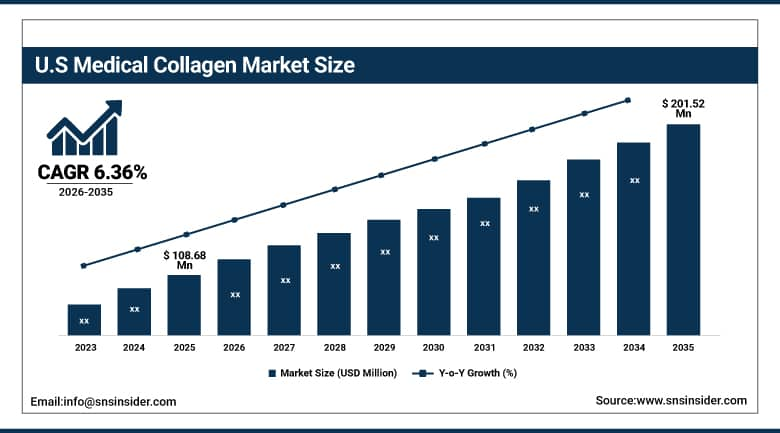

The U.S. Medical Collagen Market was valued at approximately USD 108.68 Million in 2025 and is expected to reach approximately USD 201.52 Million by 2035, growing at a CAGR of approximately 6.36%.

The U.S. is the most commercially sophisticated medical collagen market within North America’s dominant 37.42% global revenue position. Integra LifeSciences, MiMedx, Collagen Matrix, Medtronic, and Organogenesis collectively define the domestic commercial landscape. The FDA’s well-established 510(k) and PMA regulatory pathways for collagen-based medical devices create the regulatory certainty whose expedited clearance sustains commercial launch timelines. The growing chronic wound care burden whose diabetic foot ulcers, venous leg ulcers, and pressure injuries create structured institutional procurement, the orthopedic surgery sector’s tendon and ligament repair collagen demand, and the reconstructive surgery market’s soft tissue replacement requirement collectively sustain above-average U.S. medical collagen commercial demand.

In 2024, Integra LifeSciences received FDA clearance for its next-generation Integra Dermal Regeneration Template with enhanced bilayer collagen-glycosaminoglycan scaffold for severe burn wound treatment, featuring improved vascularization kinetics and reduced time to second-stage skin grafting. The clearance reflects the ongoing innovation investment in advanced collagen wound care products whose clinical performance differentiation sustains premium pricing in the severe wound management market where clinical outcome improvement justifies the cost premium above conventional wound dressing alternatives.

Medical Collagen Market Segment Analysis:

-

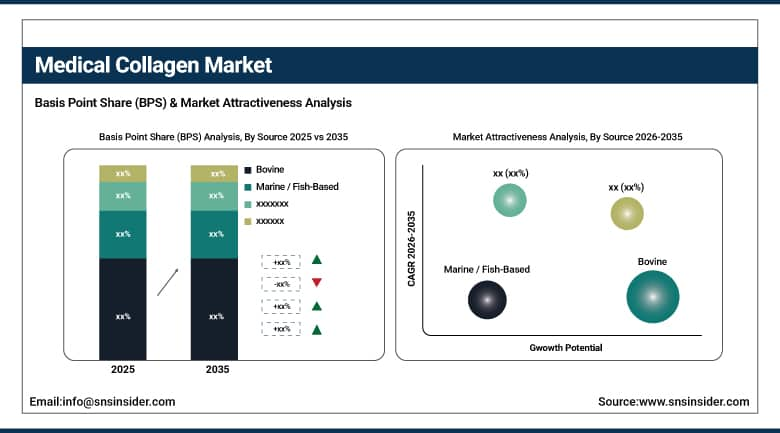

By Source, the bovine segment dominated the medical collagen market with approximately 42% share in 2025, while the marine/fish-based segment is the fastest growing.

-

By Product Type, the gelatin segment dominated the medical collagen market with approximately 35% share in 2025, while the synthetic/engineered collagen segment is the fastest growing.

-

By Application, the wound care & management segment dominated the medical collagen market with approximately 32% share in 2025, while the tissue engineering & regenerative medicine segment is the fastest growing.

-

By Form, the membrane/sheet segment dominated the medical collagen market with approximately 28% share in 2025, while the gel/hydrogel segment is the fastest growing.

By Source, bovine dominates, marine grows fastest

Bovine retained the dominant source position with approximately 42% of the medical collagen market in 2025. The bovine collagen source’s commercial primacy reflects decades of established medical device clinical use whose biocompatibility documentation, regulatory approval track record, and supply chain infrastructure create specification certainty that newer source alternatives must overcome through equivalence demonstration. Bovine Type I collagen’s tensile strength and fibril-forming properties closely approximate human dermal collagen’s structural characteristics, creating wound healing and tissue repair performance whose clinical evidence base is the most extensive of any collagen source.

Marine collagen is the fastest-growing source because the convergence of BSE elimination motivation, religious certification accessibility, and structural advantages for specific medical applications creates systematic specification migration from bovine alternatives in premium applications. Fish collagen peptides’ lower molecular weight and enhanced bioavailability relative to terrestrial animal alternatives creates absorption advantage in pharmaceutical oral delivery applications.

By Product Type, gelatin dominates, synthetic collagen grows fastest

Gelatin retained the dominant product type position with approximately 35% of the medical collagen market in 2025. Gelatin’s commercial dominance reflects its thermally reversible gel property, solubility, and processing versatility that create the widest range of medical applications of any collagen-derived product form. Gelatin capsule excipients for pharmaceutical drug delivery, hemostatic gelatin sponges for surgical bleeding control, wound dressing gelatin matrices, and tissue sealant gelatin formulations collectively represent the application breadth whose combined procurement creates gelatin’s dominant position.

Synthetic collagen is the fastest-growing product type because its animal-free production through microbial or plant expression systems creates a collagen source whose defined amino acid sequence, absence of contaminating non-collagen proteins, and batch-to-batch consistency creates regulatory advantages in the most demanding pharmaceutical and advanced medical device applications. Each biotechnology company that develops collagen-based drug delivery matrices or implantable scaffolds for regenerative medicine creates specification motivation for recombinant collagen whose regulatory compliance documentation is simplified by the product’s defined composition relative to animal-extracted alternatives.

By Application, wound care dominates, tissue engineering grows fastest

Wound care and management retained the dominant application position with approximately 32% of the medical collagen market in 2025. The growing global burden of chronic wounds, whose diabetic foot ulcer prevalence affecting 15-25% of the 537 million diabetic patients globally, venous leg ulcer incidence, and hospital-acquired pressure injury occurrence collectively create structured institutional collagen wound care product procurement. Collagen wound dressings’ biological mechanism creating growth factor binding, cell migration scaffolding, and protease modulation in the wound environment creates clinical performance differentiation from passive wound dressings that sustains premium collagen wound product specification in wound care clinical settings.

Tissue engineering and regenerative medicine is the fastest-growing application because advances in 3D bioprinting using collagen bioinks, patient-specific scaffold design from CT/MRI imaging data, and stem cell integration with collagen matrices collectively create a growing clinical demand for precision collagen-based tissue constructs whose application breadth spans cartilage, bone, tendon, ligament, skin, and vascular tissue repair. Each academic medical center that establishes a tissue engineering laboratory and each biotech company that advances a collagen scaffold clinical programme creates above-average premium collagen procurement whose research-grade specification and per-unit value substantially exceed commodity wound dressing alternatives.

By Form, membrane/sheet dominates, gel/hydrogel grows fastest

Membrane and sheet collagen retained the dominant form position with approximately 28% of the medical collagen market in 2025. The membrane and sheet form’s versatility across wound covering, guided tissue regeneration in dental and periodontal surgery, surgical barrier application, and dural repair collectively create the most commercially diverse single collagen form deployment. Each guided tissue regeneration membrane placement in dental implant surgery, each collagen dural substitute used in neurosurgery, and each wound management collagen sheet application creates procurement that compounds with the respective procedure volume.

Gel and hydrogel collagen is the fastest-growing form because injectable collagen hydrogels’ minimally invasive delivery, 3D bioprinting compatibility, and drug delivery matrix capability create growing adoption in soft tissue augmentation, regenerative medicine research, and controlled release pharmaceutical applications. Each dermal filler treatment that uses collagen-based injectable hydrogel, each 3D cell culture experiment that requires collagen hydrogel scaffold, and each drug delivery programme that develops collagen matrix-controlled release creates gel form procurement whose combined growth compounds with the minimally invasive procedure trend and regenerative medicine research investment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Medical Collagen Market Insights

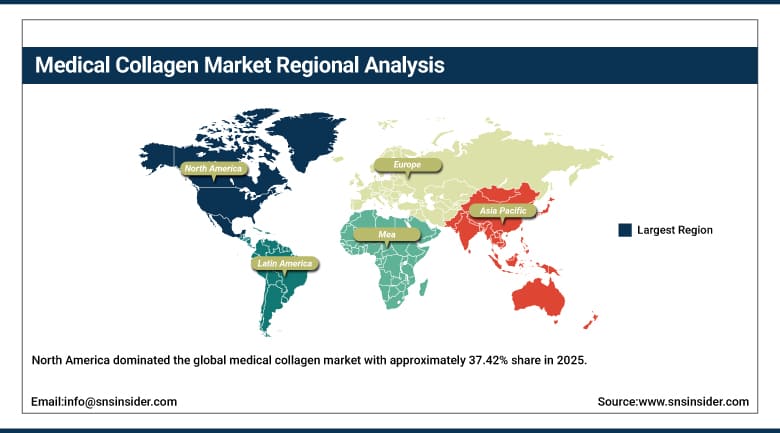

North America dominated the global medical collagen market with approximately 37.42% share in 2025 driven by advanced biomedical research infrastructure, established regenerative medicine commercial ecosystem, and the presence of Integra LifeSciences, MiMedx, Collagen Matrix, Medtronic, and Organogenesis. The United States accounts for approximately 87.4% of North American revenues through FDA-regulated medical device and pharmaceutical markets, CMS reimbursement for advanced wound care products, and the surgical sector’s collagen hemostatic and tissue repair procurement.

Canada contributes approximately 12.6% of North American revenues through its academic biomedical research community’s collagen scaffold procurement, the healthcare system’s wound care collagen product adoption, and the growing regenerative medicine biotech sector’s collagen material investment.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Medical Collagen Market Insights

Europe is a technically sophisticated medical collagen market with approximately 25.16% share in 2025 where the EU MDR’s rigorous collagen medical device regulatory framework, Germany’s biomedical engineering leadership, and the presence of Collagen Solutions, Geistlich Pharma, and Symatese create a complete medical collagen ecosystem. Germany accounts for approximately 22.3% of European revenues through its medical device sector’s collagen procurement, Geistlich Pharma’s dental and periodontal collagen product leadership, and the hospital sector’s advanced wound care investment.

Switzerland, France, and the United Kingdom are significant secondary markets where Geistlich Pharma’s Swiss operations, the pharmaceutical industry’s collagen excipient procurement, and the National Health Service’s advanced wound care collagen product adoption create consistent commercial demand.

Asia Pacific Medical Collagen Market Insights

Asia Pacific is the fastest-growing regional medical collagen market whose share is progressively increasing as healthcare infrastructure expansion, rising chronic disease burden, and growing regenerative medicine investment create above-average market development. China accounts for approximately 44.8% of Asia Pacific revenues through its hospital sector’s wound care collagen adoption, the pharmaceutical industry’s gelatin excipient procurement, and the rapidly growing domestic biomedical device sector’s collagen material investment.

Japan and South Korea represent technically sophisticated secondary markets where advanced regenerative medicine research programmes, the cosmetic surgery market’s injectable collagen demand, and the biomedical device industry’s precision collagen scaffold development create consistent above-average per-application collagen procurement.

MEA & Latin America Medical Collagen Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital sector’s wound care and surgical collagen product adoption, Vision 2030’s healthcare investment creating above-average medical device procurement, and the growing cosmetic surgery market’s collagen dermal filler demand.

Brazil leads Latin American revenues at approximately 44.2% through its large hospital network’s wound care collagen procurement, the growing aesthetic medicine market’s injectable collagen adoption, and the pharmaceutical industry’s gelatin excipient demand. Growing healthcare infrastructure and rising surgical volumes collectively sustain regional market development through 2035.

Market Dynamics:

Growth Drivers: Chronic wound burden and regenerative medicine adoption creating structured medical collagen procurement

The global chronic wound burden is the medical collagen market’s most commercially certain structural growth driver. Diabetic foot ulcers affecting 15-25% of the 537 million global diabetic population, venous leg ulcers’ estimated 1% of the adult population prevalence, and hospital-acquired pressure injuries collectively create a wound care market whose advanced collagen wound product adoption grows with chronic disease prevalence. Each chronic wound patient whose standard-of-care wound dressing fails to achieve healing within the expected treatment timeline creates clinical motivation for advanced collagen-based wound management escalation whose commercial adoption sustains premium collagen wound product procurement.

Regenerative medicine’s expanding clinical pipeline is simultaneously creating growing demand for precision medical collagen in tissue engineering scaffold, bioink, and drug delivery matrix applications whose per-unit commercial value substantially exceeds wound care commodity collagen economics. Each new clinical programme that advances collagen-based tissue engineering toward clinical translation creates research-phase and clinical-phase collagen procurement that compounds with the regenerative medicine pipeline’s breadth across Orthopedics, cardiovascular, and neurological repair applications.

Restraints: Animal-derived immunogenicity risk and high production cost for recombinant alternatives

Animal-derived collagen’s immunogenicity risk, whose potential for adverse immune response in sensitized patients creates clinical contraindication, creates specification barriers in applications where recombinant or synthetic alternatives’ defined composition provides superior safety profile. Each patient whose adverse reaction to bovine collagen creates treatment cessation creates clinical evidence that motivates specification migration toward marine or recombinant alternatives in subsequent formulary decisions.

Recombinant collagen production’s above-commodity cost creates pricing barriers for cost-sensitive institutional procurement whose formulary decisions balance clinical advantage against acquisition cost. Each medical device development programme that evaluates recombinant collagen faces production economics that require premium device pricing whose market acceptance depends on clinical differentiation demonstration sufficient to justify above-animal-collagen cost in institutional procurement decisions.

Opportunities: 3D bioprinting collagen bioink and marine collagen premium application development

3D bioprinting collagen bioink represents the most commercially innovative near-term medical collagen opportunity whose tissue engineering application creates per-unit commercial value substantially exceeding any conventional collagen product category. Each bioprinting research programme that validates collagen bioink for specific tissue construct creation, and each clinical programme that advances 3D-bioprinted collagen scaffold toward regulatory submission, creates premium collagen procurement whose high concentration, defined rheological properties, and sterility requirements create above-commodity commercial relationships.

Marine collagen premium application development represents the most commercially accessible growth opportunity for suppliers seeking to differentiate from commodity bovine collagen through source advantage. Each regulatory market that requires BSE-free source documentation for implantable medical devices creates structured marine collagen specification motivation whose commercial adoption grows with global regulatory tightening around animal-derived medical material safety.

Recent Developments:

-

2026: Geistlich Pharma AG strengthened its collagen biomaterial portfolio in 2026 through innovations in dental and orthopedic regeneration products, improving tissue integration and clinical performance.

-

2025: Integra LifeSciences expanded its regenerative tissue portfolio in 2025 through advancements in collagen-based wound care and soft tissue reconstruction products, enhancing healing outcomes in surgical applications.

-

2025: CollPlant Biotechnologies advanced its recombinant human collagen platform in 2025, supporting next-generation tissue engineering and 3D bioprinting applications for regenerative medicine.

-

2025: MiMedx advanced its HELIOGEN collagen product platform with Type I and III collagen matrices for tissue regeneration and wound care applications offering improved handling and storage characteristics.

Medical Collagen Market key players are:

-

Integra LifeSciences Holdings Corporation

-

MiMedx Group Inc.

-

Collagen Matrix Inc.

-

Medtronic plc

-

Organogenesis Holdings Inc.

-

Geistlich Pharma AG

-

Collagen Solutions plc

-

Symatese

-

Advanced BioMatrix Inc.

-

CollPlant Biotechnologies Ltd.

-

Stryker Corporation (ColFusion)

-

Arthrex Inc.

-

BioTissue Technologies GmbH

-

Nippi Inc.

-

Nitta Gelatin Inc.

-

Anika Therapeutics Inc.

-

Bioventus LLC

-

Covalon Technologies Ltd.

-

GELITA AG

-

Encoll Corporation

Medical Collagen Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 336.61 Million |

| Market Size by 2035 | USD 624.98 Million |

| CAGR | CAGR of 6.18% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Source (Bovine, Porcine, Marine/Fish-Based, Avian, Recombinant/Synthetic, Human, Plant-Derived) • By Product Type (Gelatin, Hydrolyzed Collagen, Native Collagen, Collagen Peptides, Synthetic/Engineered Collagen) • By Application (Wound Care & Management, Tissue Engineering & Regenerative Medicine, Orthopedics & Musculoskeletal, Cardiovascular Surgery, Dental Applications, Drug Delivery, Cosmetic & Reconstructive Surgery, Others) • By Form (Membrane/Sheet, Gel/Hydrogel, Sponge/Foam, Powder, Fiber/Thread, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Integra LifeSciences Holdings Corporation, MiMedx Group Inc., Collagen Matrix Inc., Medtronic plc, Organogenesis Holdings Inc., Geistlich Pharma AG, Collagen Solutions plc, Symatese, Advanced BioMatrix Inc., CollPlant Biotechnologies Ltd., Stryker Corporation (ColFusion), Arthrex Inc., BioTissue Technologies GmbH, Nippi Inc., Nitta Gelatin Inc., Anika Therapeutics Inc., Bioventus LLC, Covalon Technologies Ltd., GELITA AG, Encoll Corporation |

Frequently Asked Questions

The market is expected to grow at a CAGR of 6.18% from 2026 to 2035.

The market was valued at USD 336.61 Million in 2025

Rising global chronic wound burden from diabetic foot ulcers and pressure injuries creating structured institutional collagen wound care product procurement.

Bovine dominated the market with approximately 42% share in 2025.

North America dominated the market with approximately 37.42% share in 2025.

Get in Touch