Clinical Trial Investigative Site Network Market Report Scope & Overview:

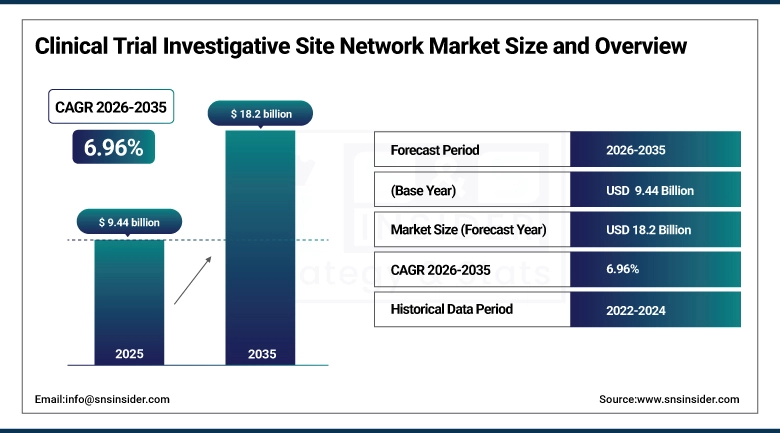

The Clinical Trial Investigative Site Network Market was valued at USD 9.44 billion in 2025 and is expected to reach USD 18.2 billion by 2035, growing at a CAGR of 6.96% from 2026-2035.

Clinical trials are the mechanism by which pharmaceutical science converts biological discovery into medicine the process that stands between a molecule's demonstration in laboratory experiments and its availability to patients who need it. Every drug that reaches a pharmacy shelf has passed through a sequence of clinical trials, each conducted at investigative sites where qualified physicians, research nurses, and clinical coordinators enroll patients, administer study treatments, collect protocol-specified data, and report findings to the sponsoring pharmaceutical company or its contracted research organization. The investigative site network exists to aggregate, standardize, and operationalize this clinical research capacity providing pharmaceutical sponsors with pre-qualified sites, established patient populations, operational infrastructure, and institutional expertise that would take years to assemble independently for each new trial. As clinical trials grow more complex as precision medicine trials require specific biomarker-positive patient populations, as adaptive trial designs require real-time data collection and analysis, as decentralized trial models require remote monitoring and digital data capture the operational sophistication that dedicated site networks provide becomes more commercially valuable relative to the alternative of assembling trial infrastructure ad hoc for each study.

ClinicalTrials.gov registry data documented over 450,000 registered clinical trials globally in 2023, representing a 15% increase from 2020 and reflecting the expanding pharmaceutical and biotech development pipeline. PhRMA documents that the U.S. biopharmaceutical industry invested USD 102 billion in R&D in 2023, the largest annual R&D investment in the industry's history sustaining the clinical trial activity that investigative site network revenue depends on.

Clinical Trial Investigative Site Network Market Size and Forecast

-

Market Size in 2025: USD 9.44 Billion

-

Market Size by 2035: USD 18.2 Billion

-

CAGR: 6.96% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Clinical Trial Investigative Site Network Market - Request Free Sample Report

Clinical Trial Investigative Site Network Market Trends

-

Decentralized clinical trial (DCT) models combining traditional site visits with home-based telemedicine visits, at-home sample collection, wearable biosensor data capture, and electronic patient-reported outcomes are becoming standard practice across therapeutic areas where disease burden and treatment monitoring requirements are compatible with remote assessment.

-

AI-powered patient recruitment platforms that match potential trial participants to eligibility criteria by mining electronic health records, insurance claims, and patient registry data are dramatically reducing enrollment timelines at site network member locations.

-

Site network consolidation through private equity investment is creating larger, more professionally managed site organizations with standardized operational processes, centralized regulatory affairs teams, and technology platforms shared across multiple physical locations.

-

Risk-based monitoring (RBM) approaches that focus on-site visits on data quality exceptions rather than 100% source data verification are reducing the time burden on site staff and improving monitoring efficiency across large trial networks.

-

Patient-centric site design making participation accessible through convenient parking, flexible scheduling, virtual visit options, and trial participation compensation that genuinely reflects participant time investment is improving enrollment and retention rates.

-

Rare disease trial specialization is creating premium network segments where sites with specific rare disease patient registries, specialized diagnostic capabilities, and gene therapy administration infrastructure command premium trial placement rates.

-

Diversity and inclusion mandate from FDA draft guidance on enhancing diversity in clinical trials is requiring site networks to actively enroll underrepresented minority populations, creating demand for sites in geographic and community settings that traditional academic medical center networks underserve.

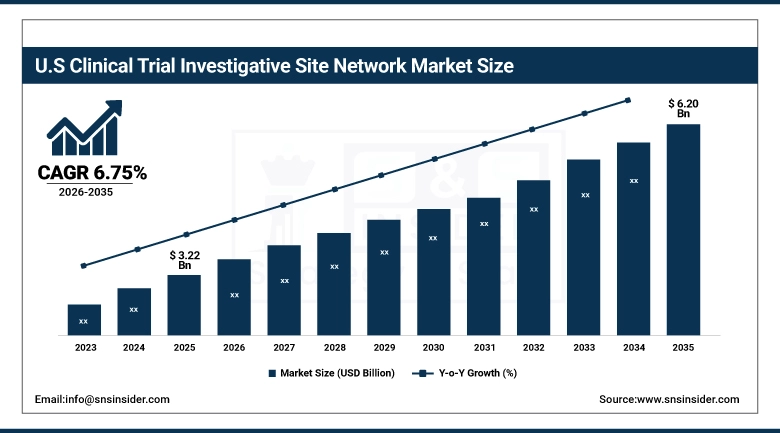

U.S. Clinical Trial Investigative Site Network Market was valued at USD 3.22 billion in 2025 and is expected to reach USD 6.20 billion by 2035, growing at a CAGR of 6.75% from 2026-2035.

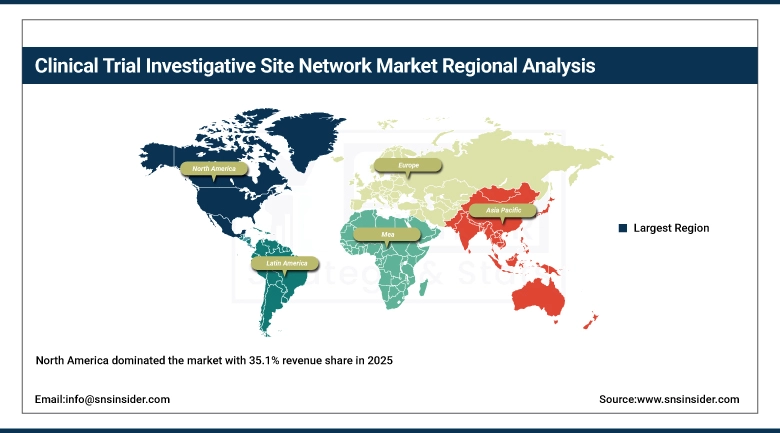

North America dominated the global Clinical Trial Investigative Site Network Market with approximately 35.1% revenue share in 2025, anchored by the United States' extraordinary pharmaceutical research ecosystem with the world's highest pharmaceutical R&D spending, the FDA's efficient and scientifically sophisticated drug review process, and the most developed commercial site management organization industry globally. The U.S. clinical trial site landscape spans from major academic medical centers including Mayo Clinic, Johns Hopkins, and Mass General Brigham to dedicated commercial research site organizations including Velocity Clinical Research, Javara, and Elligo Health Research whose business model is built entirely around clinical trial execution rather than clinical care. The concentration of pharmaceutical and biotech company headquarters in New York, Boston, San Francisco, and New Jersey means that U.S. site networks have the shortest relationship distance to their primary sponsors of any regional market.

The NIH's Clinical and Translational Science Awards (CTSA) program funds clinical research infrastructure at 65 academic medical centers across the U.S., creating a network of well-equipped academic investigative sites with established IRB infrastructure, trained research staff, and patient populations engaged in research participation. ClinicalTrials.gov documents that the U.S. accounts for approximately 34% of all globally registered clinical trial sites, the highest national concentration in the world.

Clinical Trial Investigative Site Network Market Segment Analysis

-

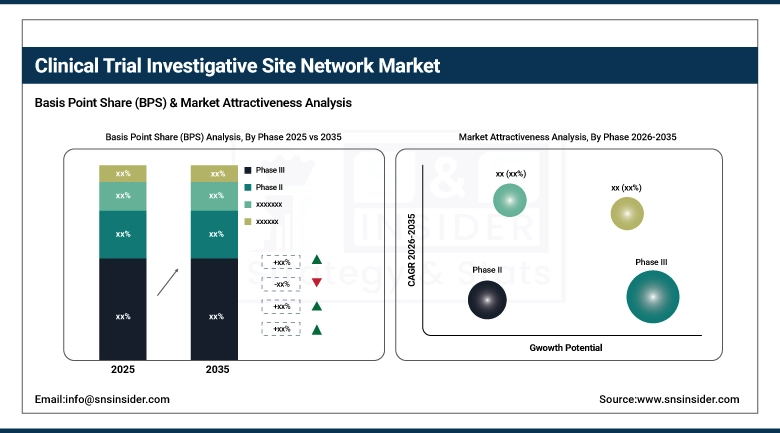

By Phase, Phase III dominated with 49.3% share in 2025; Phase I expected to grow at the fastest CAGR.

-

By Therapeutic Area, Oncology dominated with 32.1% share in 2025; Pain Management expected to grow fastest.

-

By End-User, Pharmaceutical & Biopharmaceutical Companies dominated; CROs growing at fastest CAGR.

By Phase: Phase III dominates, Phase I growing fastest

Phase III trials held approximately 49.3% of the Clinical Trial Investigative Site Network Market in 2025, a dominance that reflects the operational scale and resource intensity of pivotal registration trials whose patient enrollment requirements, multi-site geographic distribution, and regulatory data quality standards collectively represent the greatest demand for well-organized site network services. Phase III trials routinely involve hundreds of investigative sites across 30-50 countries, enrolling thousands of patients over 3-5 year recruitment periods an operational coordination challenge that only site networks with established international footprints, standardized start-up processes, and experienced operational teams can execute efficiently. The commercial stakes of Phase III execution are enormous: trial failure due to enrollment delays, data quality issues, or protocol deviation rates that impair regulatory review can cost pharmaceutical sponsors hundreds of millions in delayed commercial revenue.

Phase I trials are growing at the fastest CAGR, driven by the expanding early-phase drug development pipeline particularly in oncology, where first-in-human oncology trials are growing at above-market rates as targeted therapy and immuno-oncology approaches generate large numbers of novel molecular entities requiring initial safety and dose-escalation evaluation. Phase I site networks which require specialized clinical pharmacology units with pharmacy compounding capability, intensive patient monitoring infrastructure, and experienced clinical teams capable of managing complex adverse events are a premium network segment whose site density remains much lower than Phase II/III infrastructure. The increasing number of cell and gene therapy first-in-human trials is creating additional Phase I site demand for facilities with specialized cell therapy administration capability.

The FDA's Center for Drug Evaluation and Research documents that 1,756 new INDs were filed in FY2023 a record with oncology representing the largest therapeutic area. Each IND filing eventually requires Phase I investigative sites, creating structural long-term demand growth for first-in-human trial infrastructure.

By Therapeutic Area: Oncology dominates at 32.1%, Pain Management growing fastest

Oncology dominated the Clinical Trial Investigative Site Network Market with approximately 32.1% revenue share in 2025, a position driven by the world's largest clinical trial therapeutic area pipeline over 1,200 oncology drugs in active clinical development as of 2025 combined with the operational complexity of oncology trials whose biomarker selection criteria, combination therapy protocols, and immune-related adverse event monitoring requirements demand investigative sites with specialized oncology clinical infrastructure. The complexity of oncology trial eligibility criteria which routinely require genomic profiling of biopsies, specific mutation confirmation, and prior treatment history requirements makes patient identification and screening resource-intensive, creating particular value for site networks with established oncology patient populations and on-site molecular pathology capability.

Pain Management is expected to grow at the fastest therapeutic area CAGR, driven by the surging incidence of chronic pain disorders globally and the regulatory pressure to develop non-opioid pain treatments as alternatives to the opioid analgesics whose epidemic consequences have created both public health urgency and commercial opportunity for pharmaceutical developers. Chronic pain affects approximately 20% of adults in developed countries over 50 million Americans creating a massive patient population that pharmaceutical companies are investing to serve with novel mechanisms including CGRP antagonists, sodium channel blockers, and neuromodulation devices.

By End-User: Pharma companies dominate, CROs growing fastest

Pharmaceutical and Biopharmaceutical Companies held the dominant end-user position in the market in 2025, representing the primary sponsors whose pipeline programs generate investigative site network demand. Large pharmaceutical companies with extensive internal clinical operations capabilities are nevertheless the largest buyers of site network services because their trial volume exceeds internal site relationship capacity, because they require specialized therapeutic area expertise or geographic reach that their own networks don't provide, and because external site networks offer enrolment performance accountability that internal site relationships often cannot enforce. The growing biotech sector which collectively runs clinical programs at higher per-company average volumes than any prior generation of pharmaceutical development has become an important sponsor segment whose reliance on external site networks for clinical development execution sustains site network demand growth above the large pharma baseline.

Contract Research Organizations are the fastest-growing end-user segment, as CROs increasingly offer site network services alongside their traditional project management, data management, and regulatory affairs services creating comprehensive end-to-end trial service packages that pharmaceutical sponsors can procure from a single vendor relationship. IQVIA, Labcorp Drug Development, ICON, and Syneos Health have each built or acquired site network capabilities, competing with pure-play site management organizations for the investigative site services component of clinical trial outsourcing contracts.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

93% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

China |

38% |

|

Middle East & Africa |

Israel |

40% |

|

Latin America |

Brazil |

52% |

Clinical Trial Investigative Site Network Market North America Insights

North America dominated the market with 35.1% revenue share in 2025, led by the United States where the world's highest pharmaceutical R&D spending, FDA regulatory leadership, and the most commercially developed site management organization industry create unmatched clinical trial activity. The U.S. site network industry's maturity is reflected in the consolidation that private equity investment has accelerated: Velocity Clinical Research, Javara, and Continuum Clinical each operate networks of 30-100+ research sites under consolidated operational management, providing sponsors with standardized processes and performance guarantees that independent site models cannot match. Canada's bilingual research infrastructure and favorable regulatory environment sustain a secondary North American clinical research market of meaningful scale.

Get Customized Report as per Your Business Requirement - Enquiry Now

Clinical Trial Investigative Site Network Market Asia Pacific Insights

Asia Pacific is the fastest-growing regional Clinical Trial Site Network Market, driven by the pharmaceutical industry's recognition that Asian patient populations are essential for regulatory submissions seeking global approvals, that operational costs at Asian sites are 30-50% below Western equivalents, and that patient recruitment for many therapeutic areas proceeds faster in Asia where disease burden and healthcare utilization patterns create accessible patient populations. China's clinical regulatory reforms including the country's 2017 ICH membership and progressive alignment of NMPA requirements with international standards have made China-based investigative sites viable for global multi-regional clinical trials in ways that were not commercially practical before regulatory harmonization. India's vast patient population, English-language scientific community, and growing pharmaceutical manufacturing industry create particularly strong conditions for clinical research capacity investment.

China's NMPA approved 67 innovative drugs in 2025 a record reflecting the country's rapidly maturing regulatory review capacity that sustains domestic clinical trial activity at scale. India's Schedule Y regulations aligned with ICH GCP standards enable Indian investigative sites to generate data that FDA and EMA accept in regulatory submissions, making India's cost-efficient clinical research capacity directly usable for global regulatory filings.

Clinical Trial Investigative Site Network Market Europe Insights

Europe holds a significant and technically sophisticated Clinical Trial Site Network Market, with the UK, Germany, France, Spain, and the Netherlands as primary national markets. European investigative sites operate under the EU Clinical Trial Regulation (EU CTR No 536/2014) which created a harmonized multi-country trial authorization system — reducing the administrative burden of running trials across EU member states and making pan-European site network operations more efficient. The UK's post-Brexit MHRA regulatory framework has maintained its global trial authorization speed advantage, sustaining the UK's attractiveness as a clinical trial host despite the complexity of UK/EU regulatory divergence. European academic medical centers including Karolinska, Charité, and the Institut Gustave Roussy maintain world-class investigative site infrastructure in therapeutic areas including oncology, neurology, and cardiovascular disease.

Clinical Trial Investigative Site Network Market Middle East & Africa and Latin America Insights

The Middle East's clinical trial market is growing primarily through Israel's sophisticated biotech and clinical research ecosystem Israel has one of the world's highest densities of clinical trial participation per capita, reflecting the country's excellent clinical research infrastructure, tech-forward medical practice culture, and relatively contained and ethnically diverse patient population that makes Israel attractive for early-phase proof-of-concept studies. Saudi Arabia and UAE are developing clinical trial capacity as part of their healthcare system investments, with Saudi Arabia's Vision 2030 healthcare agenda explicitly targeting clinical research capacity development. Latin America's market concentrates in Brazil and Mexico, where large patient populations, improving regulatory frameworks, and cost efficiencies sustain growing pharmaceutical industry interest in Latin American clinical trial sites.

Clinical Trial Investigative Site Network Market Growth Drivers:

Pharmaceutical pipeline expansion and decentralized trial adoption driving sustained clinical trial site network market growth globally

The Clinical Trial Investigative Site Network Market's growth is directly coupled to global pharmaceutical R&D spending, which has grown at approximately 5% annually for a decade and shows no sign of structural reversal. The expanding pipeline of precision medicine drug candidates each requiring biomarker-specific patient populations that conventional recruitment approaches struggle to identify efficiently creates premium demand for site networks with genomic profiling capability, patient registry integration, and specialist clinical expertise. The decentralized clinical trial model's commercial adoption is creating a second growth driver: as DCT protocols expand what counts as an investigative site visit to include remote video assessments, home nursing visits, and wearable sensor data collection, the definition of investigative site capability is evolving in ways that create new service categories and new competitive entrants in site network services.

Clinical Trial Investigative Site Network Market Restraints:

Site staff burden and complex protocol requirements creating clinical trial site network capacity and quality challenges globally

Investigative site operations face a compounding administrative burden that clinical research coordinators consistently identify as the primary driver of site staff burnout and turnover. Each new clinical trial brings a unique protocol document averaging 200-300 pages, a site initiation visit package, an electronic data capture system requiring user training, source documentation requirements, monitoring visits, and regulatory inspection preparation administrative demands that accumulate across a site's concurrent trial portfolio and consume staff capacity that clinical care operations and trial execution should receive. Site staff turnover rates above 30% annually are documented at many research sites, creating a continuous training demand that disproportionately affects smaller site organizations without the institutional infrastructure to systematize the onboarding and training process.

Clinical Trial Investigative Site Network Market Opportunities:

Rare disease trial specialization and AI-powered recruitment creating transformative clinical trial site network growth opportunities

Rare disease clinical research represents the market's most commercially premium growth segment, where FDA orphan drug designations 295 granted in 2025 alone generate clinical development programs whose patient identification challenges and protocol complexity create intense demand for site networks with specific rare disease expertise. Building a clinical research network in a rare disease where eligible patients are geographically dispersed, where disease-specific registries are essential for identification, and where investigators with sufficient clinical experience to serve as qualified principal investigators are scarce requires years of institutional investment creating durable competitive moats for site organizations that make that investment ahead of the commercial demand.

Recent Developments:

-

2026: Velocity Clinical Research announced expansion to 75 investigative sites across the United States through acquisition of ClinPoint Trials' Southeast network, establishing the U.S.'s largest dedicated commercial site management organization footprint with a focus on standardized decentralized trial capability across all member sites reporting average study activation timelines 40% shorter than industry benchmarks for Phase II-III trials in its therapeutic area focus areas.

-

2025: ICON plc launched its PRA Site Solutions integrated site network service combining site identification, feasibility assessment, site management, and patient recruitment technology in a single service platform allowing pharmaceutical sponsors to access a pre-qualified network of 600+ global investigative sites under a standardized performance guarantee framework that replaces ad-hoc site selection with enrollment milestone-linked contracting.

-

2025: The FDA published its updated guidance on Diversity, Equity, and Inclusion in Clinical Trials requiring all Phase III trial sponsors to submit diversity action plans documenting enrollment targets for underrepresented racial and ethnic populations creating compliance-driven investment in site network geographic expansion into community health centers, federally qualified health centers, and rural clinical sites that represent underserved populations with disproportionate chronic disease burden.

Clinical Trial Investigative Site Network Market Key Players

Some of the Clinical Trial Investigative Site Network Market Companies

-

IQVIA Holdings Inc.

-

ICON plc

-

Labcorp Drug Development (Covance)

-

Velocity Clinical Research

-

WCG Clinical LLC

-

Elligo Health Research Inc.

-

Clinipace Ltd.

-

Meridian Clinical Research

-

Javara Inc.

-

ClinChoice Ltd.

-

Novatek International

-

Syneos Health Inc.

-

Premier Research Group Ltd.

-

Worldwide Clinical Trials LLC

-

Vericel Corporation

-

HCA Healthcare Inc.

-

Inovalon Holdings Inc.

-

Roper Technologies Inc. (Accelrys)

-

Medpace Holdings Inc.

-

BioClinica Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.44 Billion |

| Market Size by 2035 | USD 18.2 Billion |

| CAGR | CAGR of 6.96% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Phase [Phase I, Phase II, Phase III, Phase IV] • By Therapeutic Areas [Oncology, Cardiology, CNS Conditions, Pain Management, Endocrine, Others] • By End Use (Pharmaceutical & Biopharmaceutical Companies, Medical Device Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IQVIA Holdings Inc., ICON plc, Labcorp Drug Development (Covance), Velocity Clinical Research, WCG Clinical LLC, Elligo Health Research Inc., Clinipace Ltd., Meridian Clinical Research, Javara Inc., ClinChoice Ltd., Novatek International, Syneos Health Inc., Premier Research Group Ltd., Worldwide Clinical Trials LLC, Vericel Corporation, HCA Healthcare Inc., Inovalon Holdings Inc., Roper Technologies Inc. (Accelrys), Medpace Holdings Inc., BioClinica Inc. |

Frequently Asked Questions

North America dominated with approximately 35.1% share; Asia Pacific is the fastest growing.

Oncology dominated with approximately 32.1% share; Pain Management is growing fastest.

Phase III dominated with approximately 49.3% share in 2025; Phase I is the fastest growing.

The Clinical Trial Site Network Market was valued at USD 9.44 billion in 2025.

The Clinical Trial Site Network Market is expected to grow at a CAGR of 6.96% from 2026 to 2035.

Get in Touch