Medical Device Reprocessing Market Report Scope & Overview:

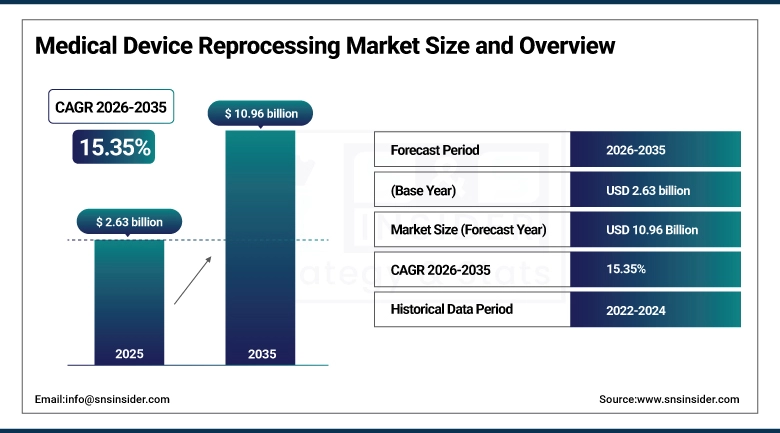

The Medical Device Reprocessing Market size was estimated at USD 2.63 billion in 2025 and is expected to reach USD 10.96 billion by 2035 and grow at a CAGR of 15.35% over the forecast period of 2026-2035.

The medical device reprocessing market is experiencing substantial growth, fueled by increasing cost pressures within health care systems, growing concern about the sustainability of hospital practices, and increased regulatory acceptability of third-party reprocessing programs. Reprocessing single-use devices (SUDs) will allow healthcare organizations to save 40%-60% of procurement costs as opposed to purchasing new OEM devices while also maintaining clinical equivalence that is established by the FDA and other international regulatory agencies.

Hospitals and IDNs are partnering with third-party organizations for medical device reprocessing for different surgical procedures including cardiology, gastroenterology, orthopedics, and general surgery. Sustainability objectives coupled with savings on costs have resulted in making medical device reprocessing not only a cost-saving solution but a core part of hospitals' overall supply chain management system. The AMDR claims that medical device reprocessing saves approximately USD 470 million annually at hospitals in the USA.

Medical Device Reprocessing Market Size and Forecast:

-

Market Size in 2025: USD 2.63 billion

-

Market Size by 2035: USD 10.96 billion

-

CAGR: 15.35% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Medical Device Reprocessing Market - Request Free Sample Report

Medical Device Reprocessing Market Trends:

-

Accelerated shift to third-party SUD reprocessing in U.S. and EU hospitals as hospital administration increases pressure to lower costs and pursue sustainable operations

-

Adding to the number of reprocessed devices cleared under the FDA 510(k) program, where over 100 types of single-use devices are now cleared for reprocessing.

-

Progressing towards more advanced tracking and verification technologies in the reprocessing workflows (for example, electronic tagging of devices utilizing RFID technology).

-

Growing fraction of purchases of third-party reprocessed devices by hospitals, including electorphysiology catheters, laparoscopic trocars, ultrasound transducers, becoming more routine purchases

-

Expanding uptake in ASCs and outpatient centers with reprocessing companies building smaller business cases for high volumes of low complexity procedures

-

Growing significance and relevance of ESG reporting for healthcare organizations, leading to reprocessing and therefore reducing medical waste output and carbon emissions from hospitals.

-

Physical consolidation of third-party reprocessors and OEMs establishing in-house reprocessing subsidiaries, intensifying competitive dynamics and expanding geographic coverage.

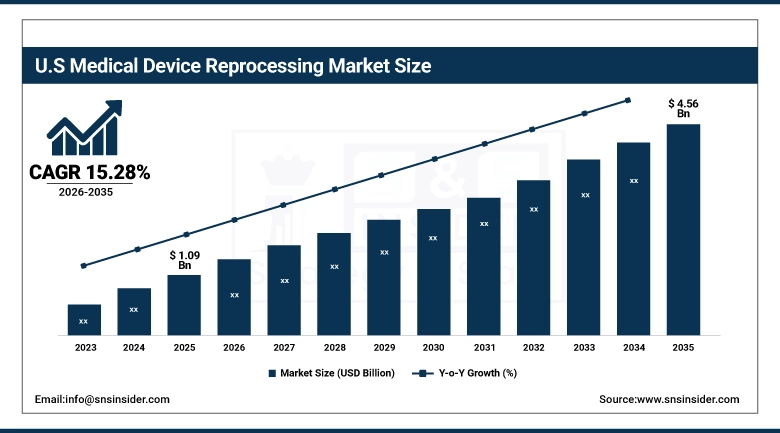

The U.S. Medical Device Reprocessing Market size was valued at USD 1.09 billion in 2025 and is expected to reach USD 4.56 billion by 2035, growing at a CAGR of 15.28% during the forecast period 2026-2035. The USA today accounts for the highest share of the global medical device reprocessing as it has an established regulatory structure (governed by the FDA), a well-defined network of third party reprocessors and also highest per capita incidence of SUD procedures in the world.

Hospital waste of which SUDs are part is discarded annually by healthcare facilities in the U.S. in the amount of over 400,000 tons. Sustainability mandates at the federal–state level, coupled with the heavy impetus to change reimbursement practices, will continue to be the major forces behind expanding reprocessing in US hospitals.

Medical Device Reprocessing Market Growth Drivers:

-

Rising Healthcare Cost Pressures and Hospital Budget Constraints are Accelerating the Medical Device Reprocessing Market Expansion

Increasing hospital operational expenses and limited budget allocations are the major contributing factors toward the adoption of device reprocessing in global health care systems. Device reprocessing allows saving between 40% and 60% compared with the price of brand-new devices, helping the facility save money without affecting the quality and outcome of procedures performed with reprocessed single-use devices.

Health care facilities that engage in device reprocessing report saving between one and six million dollars per year, depending on the number of procedures performed within a particular specialty, as well as the specific type of device. Electrophysiology and orthopedic arthroscopy are the most profitable areas for device reprocessing because of the high unit price of devices involved in the procedures performed in these specialties.

Medical Device Reprocessing Market Restraints:

-

Regulatory Complexity and OEM Restrictions are Limiting the Medical Device Reprocessing Market Penetration

Despite growing acceptance, reprocessing continues to face several challenges, which include fragmentation in regulation and resistance from original equipment manufacturers. No national regulatory environment exists outside the U.S. that recognizes or permits reprocessing of third-party SUDs within Asian-Pacific, Latin American or Middle Eastern countries. Lack of global standards are translating to expensive compliance costs and elevated barriers to entry for third-party reprocessors that work across various jurisdictions.

Additionally, OEMs frequently designate devices as single use, due to hospital contracts that prohibit the latter from engaging in reprocessing programs, thereby reducing reuse opportunities at the device supply level. Moreover, legal risks related to liability concerning any adverse events associated with reprocessed devices create enormous barriers to hospital adoption.

Medical Device Reprocessing Market Opportunities:

-

Expansion of Reprocessable Device Categories and Emerging Market Penetration are Creating New Growth Avenues for the Medical Device Reprocessing Market

The expansion of SUD classifications with FDA exemptions for reprocessing them can be viewed as a great opportunity in the short term, especially as the FDA has cleared more complex devices–including electrophysiology mapping catheters, powered orthopedic devices, and laparoscopy systems–to be reprocessed. With each new approval comes a broader range of devices and a larger revenue generating opportunity for the incumbents in reprocessing.

Simultaneously, the continuous evolution of healthcare infrastructure in countries such as India, Brazil, China, and Southeast Asian nations have increased the demand for effective management of devices. While new hospitals are being built in these emerging nations and governments impose mandatory budget cuts, reprocessors offer a business case that allows for optimal device purchasing through outsourcing.

Medical Device Reprocessing Market Segment Analysis:

-

By Type, reprocessed medical devices accounted for the largest share of approximately 62.4% in 2025, while reprocessing support and services is expected to register the fastest growth with a CAGR of 16.1%.

-

By Device category, semi-critical devices dominated the market with nearly 44.8% share in 2025, whereas critical devices are anticipated to witness the highest growth with a CAGR of 15.9%.

-

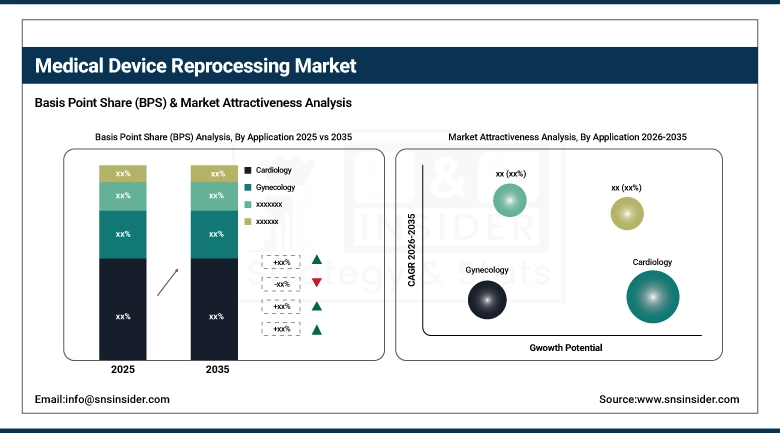

By Application, Cardiology held the largest market share of 31.7% in 2025, and gastroenterology was estimated to be the fastest-growing application with a growth rate of 16.4%

By Application, Cardiology Leads the Market, While Gastroenterology Registers Fastest Growth

Cardiology retains its leadership status because of the higher price of cardiovascular devices such as electrophysiology catheters, hemostasis valves, and cardiology mapping systems, making reprocessing highly lucrative in cath lab applications. The number of procedures performed using cardiovascular devices in the U.S. is greater than seven million procedures per year.

Gastroenterology registers as the fastest-growing application owing to the increase in the prevalence of GI disorders around the world, the higher prevalence of endoscopic procedures, and increased cost-efficiency in endoscope reprocessing at hospitals. Automated endoscope reprocessor and complex channel scope reprocessing will be among the main drivers for growth in this area.

By Type, Reprocessed Medical Devices Leads the Market, While Reprocessing Support and Services Emerges as the Fastest Growing Segment

Reprocessed medical devices have a commanding lead because of the sheer number of approved SUDs that currently undergo the reprocessing procedure in hospitals, such as electrophysiology catheters, ultrasound transducers, trocars, and pulse oximeter sensors. The volume of already-inventoried devices available for reprocessing at hospitals in the United States and Europe makes this sub-segment very demanding.

There is a growing market in reprocessing support and services, including device tracking, regulatory compliance, employee training, and more. Hospitals lacking their own capabilities outsource the responsibility of managing these programs to reprocessing support companies. There is an increasing need to manage more complex reprocessing procedures and related paperwork due to stringent guidelines around the world.

By Device Category, Semi-Critical Devices Dominate, While Critical Devices Register Rapid Growth

Semi-critical medical devices that include endoscopes, laryngoscope blades, and respiratory therapy devices have the highest share because of the frequent use of these devices in gastroenterology, pulmonology, and anesthesia, along with the standard reprocessing process that is used in this segment. A standard reprocessing protocol decreases turnaround time and operational costs for central sterile processing departments in hospitals.

The critical devices, which include surgical instruments, biopsy forceps, and electrocardiography (ECG) electrodes and catheters that need complete sterilization, are showing strong growth. The advancement of new sterilization techniques and FDA clearance for new critical segments of SUDs are allowing companies to gain access to these markets.

Medical Device Reprocessing Market Regional Highlights:

North America Medical Device Reprocessing Market Insights:

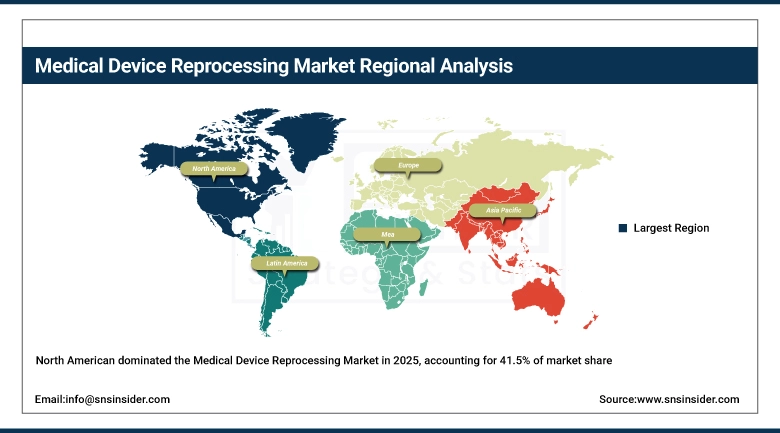

In 2025, North America was the top leader in the market of medical devices reprocessing. It comprised about 41.5% of the overall global market share. The position of North America can be attributed to its most advanced regulatory framework compared to other regions. This is because the Food and Drug Administration oversees the reprocessing of SUDs according to 21 CFR Part 820. Moreover, there is the need for all the cleared reprocessors to meet the same criteria of quality and safety as the original device manufacturers. In North America, the USA makes up the major part of revenues. There are approximately 4,500 hospitals that engage in the reprocessing activities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Medical Device Reprocessing Market Insights:

The Asia Pacific region is expected to be the fastest-growing region during the forecast period with a CAGR of 16.2%. With leading regions including China, India, Japan, and South Korea, regional spend on health care continues to expand at over 8% per year. The drive from the Chinese policy on lowering the costs of healthcare in the nation is pressuring the public hospitals to utilize reprocessing services, where more than 200 tertiary hospitals have already taken place in pilots in Beijing and Shanghai.

Europe Medical Device Reprocessing Market Insights:

Europe had the second-biggest market share in the medical device reprocessing industry in 2025, contributing to roughly 27%–29% of the total market share. Some of the leading countries include Germany, the United Kingdom, France, and the Netherlands due to cost containment measures in national health services and the presence of infrastructure for hospital sterilization. The MDR 2017/745 from the European Union is a structured policy that provides guidelines on the reprocessing of Single-use devices (SUDs). Germany boasts the most developed system of reprocessing at hospitals. An estimated 90 million units of medical devices undergo reprocessing in Europe per year.

Latin America (LATAM) and Middle East & Africa (MEA) Medical Device Reprocessing Market Insights:

LATAM and MEA are regions of developing economies and are expected to grow at CAGRs of about 13% to 15% during the forecast period. The Brazilian market represents the most important market in the Latin America region as savings-driven reforms take hold within the SUS healthcare system and reprocessed SUDs become more widely accepted through new ANVISA regulation. Mexico could be the second most important market for the company within the LATAM region, given the fact that hospitals have begun considering the device reprocessing concept as direct costs of devices increase.

Medical Device Reprocessing Market Competitive Landscape:

Stericycle Inc., a leading provider of medical waste and compliance solutions, operates one of the most extensive SUD reprocessing networks in North America. The company's reprocessing division manages high-volume programs across cardiology and orthopedic device categories for major U.S. hospital systems and IDNs.

-

In January 2025: Stericycle launched an expanded SUD reprocessing services platform integrating RFID-based device tracking and real-time compliance reporting, deployed across 300 partner hospital facilities in the United States.

Stryker Sustainability Solutions, a division of Stryker Corporation, is a dominant force in the orthopedic and surgical SUD reprocessing market. The division collects, reprocesses, and redistributes FDA-cleared devices including powered surgical instruments, ultrasonic scalpels, and pulse oximeters to hospitals across North America and Europe.

-

In April 2025: Stryker Sustainability Solutions expanded its reprocessing portfolio with FDA clearance for three new powered orthopedic instrument categories, increasing addressable device volume by an estimated 18% and strengthening partnerships with major orthopedic surgery centers.

Innovative Health LLC, headquartered in Scottsdale, Arizona, specializes in the reprocessing of high-cost electrophysiology catheters and cardiovascular devices. The company has built a reputation as a clinically validated, FDA-registered reprocessor with a focus on electrophysiology labs and catheterization suites at major academic medical centers.

-

In February 2025: Innovative Health received FDA 510(k) clearance for reprocessing of advanced 3D mapping catheters, enabling entry into one of the highest unit-cost SUD categories in cardiovascular medicine and significantly expanding its cardiology client base.

Medical Device Reprocessing Market Key Players:

-

Stericycle Inc.

-

Stryker Sustainability Solutions

-

Innovative Health LLC

-

Medline ReNewal

-

ReNu Medical Inc.

-

SureTek Medical

-

Ascent Health Technology

-

Hygia Health Services

-

Vanguard Medical Specialties

-

NEScientific Inc.

-

STERIS plc

-

Getinge AB

-

Olympus Corporation

-

Medivators (STERIS)

-

Cardinal Health Inc.

-

Healthmark Industries

-

Case Medical Inc.

-

Cygnus Medical LLC

-

Centurion Medical Products

-

Arjo AB

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.63 Billion |

| Market Size by 2035 | USD 10.96 Billion |

| CAGR | CAGR of 15.35% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Reprocessing Support & Services, Reprocessed medical devices) • By Device Category (Critical Devices, Semi- Critical Devices, Non- Critical Device) • By Application (Cardiology, Gastroenterology, Gynecology, Arthroscopy & Orthopedic Surgery, General Surgery and Anesthesia, Other Device Categorys (Urology, non-invasive surgeries, patient monitoring) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Stericycle Inc., Stryker Sustainability Solutions, Innovative Health LLC, Medline ReNewal, ReNu Medical Inc., SureTek Medical, Ascent Health Technology, Hygia Health Services, Vanguard Medical Specialties, NEScientific Inc., STERIS plc, Getinge AB, Olympus Corporation, Medivators (STERIS), Cardinal Health Inc., Healthmark Industries, Case Medical Inc., Cygnus Medical LLC, Centurion Medical Products, Arjo AB |

Frequently Asked Questions

The Medical Device Reprocessing Market refers to the industry focused on cleaning, sterilizing, testing, and reusing single-use medical devices (SUDs). It helps healthcare facilities reduce costs by 40% to 60% while maintaining clinical safety standards approved by regulatory authorities.

The Medical Device Reprocessing Market was valued at USD 2.63 billion in 2025 and is projected to reach USD 10.96 billion by 2035, growing at a CAGR of 15.35% from 2026 to 2035.

Key growth drivers of the Medical Device Reprocessing Market include rising healthcare cost pressures, increasing adoption of sustainable hospital practices, regulatory approvals for reprocessed devices, and growing partnerships with third-party reprocessors.

In the Medical Device Reprocessing Market, reprocessed medical devices dominate with a 62.4% market share in 2025, while reprocessing support and services are the fastest-growing segment with a CAGR of 16.1%.

North America leads the Medical Device Reprocessing Market, holding approximately 41.5% market share in 2025, driven by strong regulatory frameworks, high adoption of SUD reprocessing, and widespread hospital participation.

Get in Touch