Medical Sensors Market Report Scope & Overview:

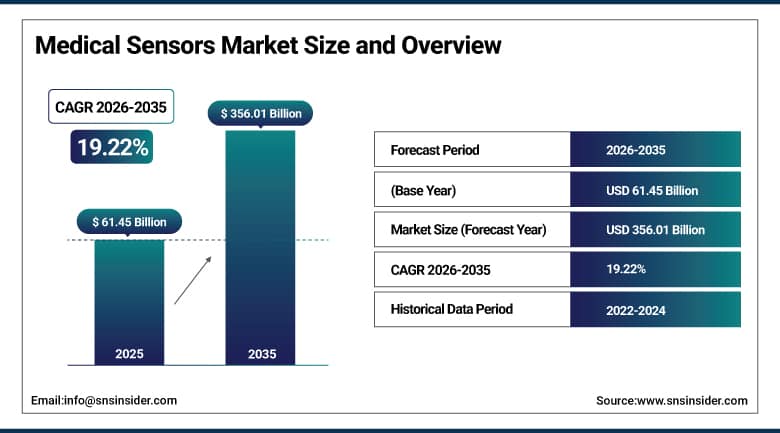

The Medical Sensors Market was valued at USD 61.45 Billion in 2025 and is expected to reach USD 356.01 Billion by 2035, growing at a CAGR of 19.22% from 2026–2035.

The global medical sensors market is growing at an exceptional and transformative pace. Medical sensors are devices that detect, measure, and transmit physiological, biochemical, and environmental parameters in clinical, home care, and research settings, enabling real-time patient monitoring, diagnostic imaging, surgical guidance, and therapeutic delivery. The market is driven by the increasing use of medical sensors in wearable devices, remote monitoring, and home healthcare solutions, alongside the demand for high-precision, real-time monitoring that has led to advancements in sensor performance, miniaturization, and energy efficiency. Enhanced interoperability through IoT, 5G, and cloud technologies is improving data transfer and integration with healthcare systems, while AI-enabled sensor analytics are creating diagnostic insight generation capability that raw measurement alone cannot provide.

In 2024, Abbott Laboratories launched its Lingo continuous glucose monitor and continuous ketone monitor as over-the-counter wearable biosensor devices for non-diabetic wellness users, creating the first mainstream consumer biosensor product targeting metabolic health optimization beyond clinical glucose management. The launch represents the commercial expansion of clinical biosensor technology into the wellness consumer market whose addressable population substantially exceeds the diabetic patient base, creating new biosensor procurement channels that compound with the existing clinical market.

Market Size and Forecast:

-

Market Size in 2026E: USD 73.26 Billion

-

Market Size by 2035: USD 356.01 Billion

-

CAGR: 19.22% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Medical Sensors Market - Request Free Sample Report

Medical Sensors Market Trends:

-

Continuous glucose monitoring (CGM) sensor adoption is expanding beyond diabetes management into wellness monitoring, preventive healthcare, sports performance tracking, and gestational diabetes management

-

AI-powered medical sensor analytics are enhancing clinical decision-making by transforming physiological data into predictive insights, risk assessments, and personalized healthcare recommendations

-

Development of implantable biosensors is enabling long-term continuous monitoring of glucose levels, cardiac biomarkers, and therapeutic drug concentrations

-

Integration of tactile and force sensors into surgical robotic systems is improving precision, control, and safety during minimally invasive surgical procedures

-

Multi-parameter wearable biosensor patches are gaining adoption for continuous monitoring of vital signs, supporting remote patient monitoring, early disease detection, and hospital patient management programs

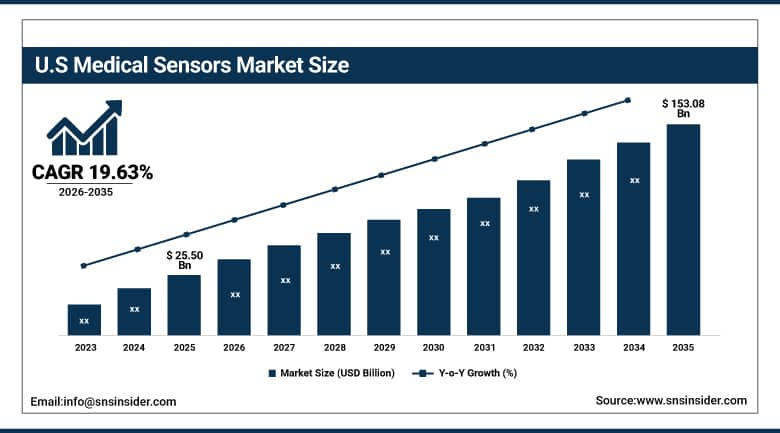

U.S. Medical Sensors Market Outlook:

The U.S. Medical Sensors Market is estimated to be USD 25.50 Billion in 2025 and is projected to reach USD 153.08 Billion by 2035, growing at a CAGR of 19.63% during 2026–2035.

The U.S. Medical Sensors Market is the world’s most commercially sophisticated national medical sensor market within North America’s dominant position. Abbott’s FreeStyle Libre and Lingo biosensor platforms, Medtronic’s continuous glucose and cardiac monitoring sensors, Dexcom’s CGM technology, and the FDA’s progressive De Novo and 510(k) pathway for novel sensor technologies collectively define the most commercially advanced medical sensor ecosystem globally. The U.S. healthcare system’s above-average medical technology spending, the CMS’ reimbursement framework for remote patient monitoring, and the FDA’s progressive approval pathway for novel sensor categories sustain above-average premium medical sensor procurement.

Dexcom launched the Dexcom G7 continuous glucose monitor in 2024 with a redesigned 60% smaller wearable sensor and 30-minute warmup period versus the prior generation’s 2-hour warmup, creating user experience improvement whose adoption acceleration demonstrates the commercial impact of sensor wearability and usability advancement beyond pure analytical performance. The G7’s Apple Watch integration and expanded pharmacy over-the-counter availability broadens CGM market access to the pre-diabetic and wellness monitoring demographic whose market scale substantially exceeds the established Type 1 diabetes patient base.

Medical Sensors Market Segment Analysis:

-

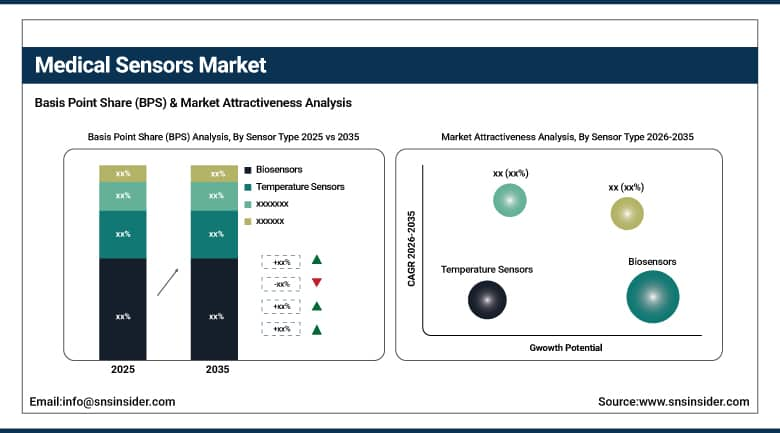

By Sensor Type, the Biosensors segment dominated the Medical Sensors Market with 42.6% share in 2025, while the Image Sensors segment is anticipated to exhibit the fastest CAGR.

-

By Application, the Surgical segment dominated the Medical Sensors Market with 33.6% share in 2025, while the Diagnostics segment is expected to register the fastest CAGR.

-

By End User, the Hospitals & Clinics segment dominated the Medical Sensors Market with 60.8% share in 2025, while the Home Healthcare segment is expected to grow at the highest CAGR.

By Sensor Type, biosensors dominate, image sensors grow fastest

Biosensors retained the dominant sensor type position with 42.6% of the medical sensors market in 2025. Biosensors’ commercial primacy reflects their position as the most clinically and commercially significant medical sensor category whose glucose monitoring, cardiac biomarker detection, and infectious disease testing applications create the largest aggregate medical sensor procurement. The continuous glucose monitor’s transformation from a niche Type 1 diabetes management tool to a mainstream metabolic health platform creates consumer biosensor procurement that compounds with the clinical CGM installed base. Each new biosensor application that achieves regulatory approval creates a new commercial procurement category whose clinical evidence sustains adoption. The COVID-19 pandemic’s lateral flow antigen biosensor’s extraordinary global deployment demonstrated the commercial scale that biosensor manufacturing can achieve when clinical demand creates non-discretionary procurement motivation.

Image sensors are the fastest-growing sensor type because the convergence of capsule endoscopy, miniaturized surgical camera, AI-assisted endoscopic diagnosis, and robot-assisted surgery’s optical guidance create multiple simultaneous above-average growth vectors in a single sensor type category. Each new minimally invasive surgical procedure that requires high-resolution optical guidance creates image sensor procurement whose per-procedure commercial value reflects the sensor’s critical role in surgical safety and efficacy. AI-enabled endoscopy’s polyp detection, lesion characterization, and automated quality assessment create premium camera sensor procurement whose diagnostic intelligence capability sustains above-commodity pricing.

By Application, surgical dominates, diagnostics grows fastest

Surgical applications retained the dominant position with 33.6% of the medical sensors market in 2025. The surgical application’s commercial primacy reflects the premium sensor specification that robotic-assisted surgery, minimally invasive procedure, and intraoperative imaging require whose performance standards create above-commodity procurement. Each da Vinci robotic surgical system’s force sensor, optical camera, and laparoscopic instrument sensor creates per-system procurement whose aggregate across the global installed base creates consistent commercial demand. The growing adoption of robotic-assisted surgery for orthopedic, cardiac, and general surgical procedures creates expanding surgical sensor procurement whose per-procedure sensor consumption compounds with procedure volume growth.

Diagnostics is the fastest-growing application because chronic disease’s progressive global expansion, personalized medicine’s biomarker-guided treatment selection, and AI-enabled diagnostic platform’s high-throughput screening capability create multiple simultaneous above-average diagnostic sensor demand drivers. The liquid biopsy’s circulating tumor DNA detection biosensor, the point-of-care cardiac biomarker panel’s troponin and BNP measurement, and the continuous glucose monitor’s real-time metabolic assessment collectively create diagnostic sensor procurement whose combined volume growth compounds with each new clinical validation.

By End User, hospitals dominate, home healthcare grows fastest

Hospitals and clinics retained the dominant end-user position with 60.8% of the medical sensors market in 2025. The hospital’s comprehensive medical sensor deployment across patient monitoring, surgical suite, diagnostic laboratory, and intensive care creates the most commercially concentrated medical sensor procurement environment. Each hospital’s patient monitoring infrastructure, surgical robot, clinical laboratory analyzer, and radiology imaging system creates sensor procurement whose per-institution commercial value reflects the hospital’s complexity and specialization. The smart hospital initiative’s IoT sensor network deployment creates new infrastructure procurement that compounds with individual diagnostic and therapeutic device sensor investment.

Home healthcare is the fastest-growing end user because remote patient monitoring’s extraordinary commercial momentum, driven by chronic disease management’s cost reduction motivation and the aging population’s preference for home-based care, creates above-average sensor demand outside institutional healthcare settings. Each chronic disease patient whose remote monitoring programme creates continuous biosensor procurement represents a new commercial relationship whose per-patient annual sensor consumption sustains recurring revenue. The telemedicine platform’s integration with connected biosensors creates clinical data transmission infrastructure whose adoption compounds with telehealth’s progressive mainstream acceptance.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

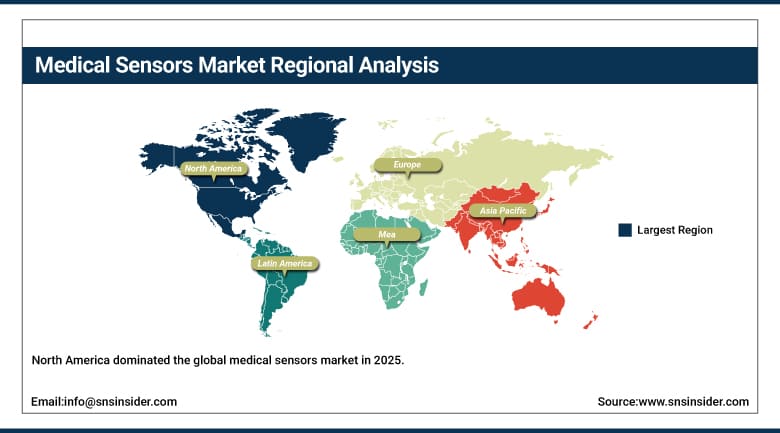

North America Medical Sensors Market Insights

North America dominated the global medical sensors market in 2025 with the highest per-capita medical technology spending and most commercially sophisticated sensor regulatory framework. The United States accounts for approximately 87.4% of North American revenues through Abbott, Medtronic, Dexcom, Becton Dickinson, and Honeywell’s commercial operations whose combined portfolio creates the global medical sensor technology standard.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system’s medical sensor procurement, the growing home healthcare sector, and the medical device manufacturing community’s domestic sensor innovation.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Medical Sensors Market Insights

Europe is a technically sophisticated medical sensors market where EU MDR’s medical device regulation, GDPR’s patient data protection, and Siemens Healthineers’ and Philips’ commercial operations create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced hospital infrastructure, Siemens Healthineers’ imaging sensor commercial leadership, and the medical device manufacturing sector’s domestic procurement.

France, Italy, and the United Kingdom are significant secondary markets where the national healthcare system’s medical sensor procurement, the growing home monitoring sector, and the medical device industry’s innovation investment create consistent demand.

Asia Pacific Medical Sensors Market Insights

Asia Pacific is the fastest-growing regional medical sensors market, driven by China’s extraordinary hospital network expansion, India’s rapidly growing healthcare infrastructure, Japan’s advanced medical technology adoption, and South Korea’s sophisticated hospital system. China accounts for approximately 44.8% of Asia Pacific revenues through its hospital equipment procurement, the domestic medical device manufacturer’s sensor development, and the growing home healthcare sector’s remote monitoring adoption.

India’s rapidly expanding hospital network, Japan’s advanced sensor technology and robotics integration, and South Korea’s connected health investment create significant secondary markets whose combined procurement sustains Asia Pacific’s fastest-growing regional status.

MEA & Latin America Medical Sensors Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital network’s sensor procurement, Vision 2030’s healthcare investment, and the growing remote patient monitoring programme. Brazil leads Latin American revenues at approximately 44.2% through its large hospital sector’s diagnostic sensor procurement, the growing home healthcare market, and the telemedicine platform’s biosensor integration.

Market Dynamics:

Growth Drivers: Remote patient monitoring adoption and wearable biosensor consumer market expansion

The increasing use of medical sensors in wearable devices, remote monitoring, and home healthcare solutions is SNS Insider’s confirmed primary market driver. Remote patient monitoring’s CMS reimbursement framework, whose CPT code structure creates structured commercial motivation for sensor procurement, sustains healthcare provider investment in home monitoring biosensor programmes. Each chronic disease patient enrolled in remote monitoring creates per-patient annual sensor consumption whose recurring nature sustains consistent commercial procurement. The extraordinary commercial success of Abbott’s FreeStyle Libre and Dexcom’s G7 continuous glucose monitors demonstrates the commercial scale that medical biosensor markets can achieve when clinical utility, user experience, and reimbursement alignment create simultaneous adoption drivers.

Wearable biosensor consumer market expansion is creating new procurement channels whose addressable population substantially exceeds the clinical patient base. Each wellness consumer who adopts continuous glucose monitoring, continuous ECG recording, or multi-parameter health patch creates commercial sensor procurement whose aggregate across the wellness market creates scale that clinical procurement alone cannot match. Apple Watch’s, WHOOP’s, and Oura Ring’s sensor-equipped wearables demonstrate the consumer market’s extraordinary commercial momentum.

Restraints: Regulatory approval complexity and data security concerns for connected medical sensors

FDA’s medical device regulatory pathway for novel sensor technologies, whose 510(k) and De Novo approval processes require clinical validation data whose collection extends development timelines and cost, creates commercialization barriers that moderate the pace of innovative sensor technology adoption. Each new biosensor category that requires clinical evidence demonstration before FDA clearance creates development investment whose recovery requires premium pricing that creates adoption barriers in cost-sensitive healthcare procurement contexts.

Connected medical sensor’s data security vulnerability creates HIPAA compliance requirements whose implementation adds system cost and complexity. Each patient data breach incident involving connected medical devices creates reputational risk that moderates healthcare institution adoption of networked sensor systems whose security management requirement creates additional IT infrastructure investment.

Opportunities: Implantable continuous monitoring biosensors and AI diagnostic sensor analytics

Implantable continuous monitoring biosensors for long-term glucose, cardiac biomarker, and drug level monitoring represent the most commercially transformative next-generation medical sensor opportunity. Each implantable biosensor that achieves multi-year continuous measurement creates patient preference over repeated blood draw or external sensor replacement, creating premium procedural and device procurement whose clinical value sustains above-external-sensor pricing.

AI diagnostic sensor analytics platforms that transform continuous physiological sensor data into early disease detection, deterioration prediction, and treatment response assessment create premium software value whose diagnostic intelligence creates clinical outcome improvement whose measurement sustains institutional procurement investment.

Recent Developments:

-

2024: Abbott Laboratories launched the Lingo continuous glucose monitor and continuous ketone monitor in 2024 as over-the-counter wearable biosensors for non-diabetic wellness users, expanding clinical CGM technology into the mainstream consumer metabolic health optimization market.

-

2024: Dexcom launched the Dexcom G7 continuous glucose monitor in 2024 with 60% smaller form factor, 30-minute warmup, and Apple Watch integration, expanding CGM accessibility to pre-diabetic and wellness monitoring demographics through pharmacy OTC availability.

-

2024: Medtronic launched the Guardian 4 CGM sensor in 2024 with extended 7-day wear, factory calibration eliminating fingerstick requirements, and enhanced SmartGuard automated insulin delivery integration creating closed-loop CGM accuracy whose performance improvement sustains Type 1 diabetes management market leadership.

Medical Sensors Market Key Players:

-

Abbott Laboratories (FreeStyle Libre/Lingo)

-

Medtronic PLC (Guardian CGM/CardioMEMS)

-

Dexcom Inc.

-

Siemens Healthineers AG

-

Koninklijke Philips N.V.

-

GE Healthcare

-

Honeywell International Inc.

-

Texas Instruments Inc.

-

STMicroelectronics N.V.

-

Becton, Dickinson and Company

-

Boston Scientific Corporation

-

Analog Devices Inc.

-

TE Connectivity Ltd.

-

Sensata Technologies Inc.

-

Amphenol Corporation

-

NXP Semiconductors N.V.

-

Sensirion AG

-

Masimo Corporation

-

Natus Medical Inc.

-

Nonin Medical Inc.

Medical Sensors Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 61.45 Billion |

| Market Size by 2035 | USD 356.01 Billion |

| CAGR | CAGR of 19.22% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Sensor Type (Biosensors, Image Sensors/Medical Imaging, Temperature Sensors, Pressure Sensors, Flow Sensors, Motion/Inertial Sensors, Others) • by Application (Surgical, Diagnostics, Monitoring & Therapeutic, Patient Safety) • by End User (Hospitals & Clinics, Home Healthcare, Diagnostic Laboratories, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Abbott Laboratories, Medtronic PLC, Dexcom Inc., Siemens Healthineers AG, Koninklijke Philips N.V., GE Healthcare, Honeywell International Inc., Texas Instruments Inc., STMicroelectronics N.V., Becton, Dickinson and Company, Boston Scientific Corporation, Analog Devices Inc., TE Connectivity Ltd., Sensata Technologies Inc., Amphenol Corporation, NXP Semiconductors N.V., Sensirion AG, Masimo Corporation, Natus Medical Inc., Nonin Medical Inc. |

Frequently Asked Questions

The Medical Sensors Market is expected to grow at a CAGR of 19.22% from 2026 to 2035.

The Medical Sensors Market was valued at USD 61.45 Billion in 2025.

Increasing use of medical sensors in wearable devices, remote monitoring, and home healthcare solutions, alongside demand for high-precision real-time monitoring driving advancements in sensor performance, miniaturization, and energy efficiency with enhanced IoT, 5G, and cloud interoperability.

Biosensors dominated the Medical Sensors Market with 42.6% share in 2025 as confirmed by SNS Insider, while Image Sensors is anticipated to exhibit the fastest CAGR.

Hospitals & Clinics dominated the Medical Sensors Market with 60.8% share in 2025, while Home Healthcare is expected to grow at the highest CAGR as confirmed by SNS Insider.

Get in Touch