Menopause Treatment Market Report Scope & Overview:

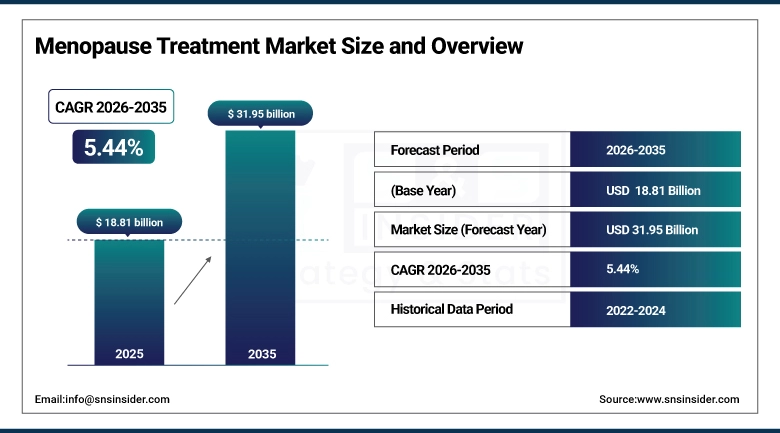

The Menopause Treatment Market was valued at USD 18.81 billion in 2025 and is expected to reach USD 31.95 billion by 2035, growing at a CAGR of 5.44% from 2026–2035.

The global Menopause Treatment Market is undergoing a profound transformation driven by the convergence of unprecedented demographic pressures, accelerating pharmaceutical innovation, and a fundamental societal shift in how menopause is perceived, discussed, and medically managed. By 2030, more than 1.2 billion women globally are projected to have reached menopausal or postmenopausal age, representing a patient population larger than any chronic disease category and creating an enormous, sustained commercial opportunity for pharmaceutical companies, digital health platforms, and wellness brands that can serve the diverse symptom relief, bone health, cardiovascular protection, and quality-of-life needs of this global demographic. The market encompasses hormonal therapies including estrogen-only preparations and combined estrogen-progesterone formulations delivered through oral tablets, transdermal patches, gels, sprays, vaginal rings, and injectable preparations; non-hormonal pharmaceutical therapies including the newly approved NK3 receptor antagonist fezolinetant, SSRI and SNRI antidepressants prescribed for vasomotor symptom management, and gabapentinoids for sleep and mood disturbances; and the large and growing dietary supplement category encompassing phytoestrogens, black cohosh, red clover, soy isoflavones, and targeted nutraceutical formulations. Shifting societal conversations driven by celebrity advocates, social media menopause communities, and physician education campaigns are reducing the stigma that historically caused women to endure menopausal symptoms without seeking medical treatment, creating structural demand growth that will persist through the forecast period as each successive cohort of women enters menopause with higher treatment-seeking rates than the generation before them.

The 5.44% Compound Annual Growth Rate (CAGR) of the menopause treatment market in the period from 2026 to 2035 is influenced by constant and consistent structural demand growth fueled by demographic necessity on the one hand and the rapid pharmaceutical innovation pipeline that is offering women more choices of treatment besides the disputed estrogen therapy, HRT, that many women refrain from because of the danger of contracting breast cancer. This is clearly depicted in the October 2024 FDA approval for Bayer AG to submit their New Drug Application (NDA) for elinzanetant after the success of three Phase III OASIS trials aimed at gaining approval by July 2025 under PDUFA.

Market Size and Forecast

-

Market Size in 2025: USD 18.81 Billion

-

Market Size by 2035: USD 31.95 Billion

-

CAGR: 5.44% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Menopause Treatment Market - Request Free Sample Report

Menopause Treatment Market Trends

-

Rapid commercial advancement of NK3 receptor antagonist therapies including fezolinetant (already approved and commercially launched as Veozah by Pfizer in 2023) and elinzanetant (under FDA review in 2025) that address vasomotor symptoms through a non-hormonal mechanism, providing the first pharmacologically novel non-hormonal treatment class for hot flashes since SSRIs were first used off-label for this indication decades ago.

-

Growing integration of digital health platforms and menopause-focused apps including Menopause Care, Peanut, and Flash co into menopause management pathways, enabling symptom tracking, telehealth prescription access, personalised lifestyle recommendations, and peer community support that improve treatment adherence and patient outcomes.

-

Rising adoption of bioidentical hormone therapy preparations including compounded bioidentical hormones and FDA-approved bioidentical products, driven by patient preference for hormones molecularly identical to endogenous hormones perceived as more natural and potentially safer than conventional synthetic hormone formulations.

-

Growing employer recognition of menopause as a workplace health issue, with major corporations introducing menopause support benefits including specialist clinical consultation access, symptom management products, and flexible working accommodations that are expanding the institutional demand base for menopause treatment programmes beyond individual out-of-pocket expenditure.

-

Accelerating adoption of telehealth menopause specialty services enabling women to access expert menopause clinical consultation and prescription therapy without the geographic barriers of traditional specialist referral, particularly benefiting women in rural and underserved communities where menopause-literate physicians are scarce.

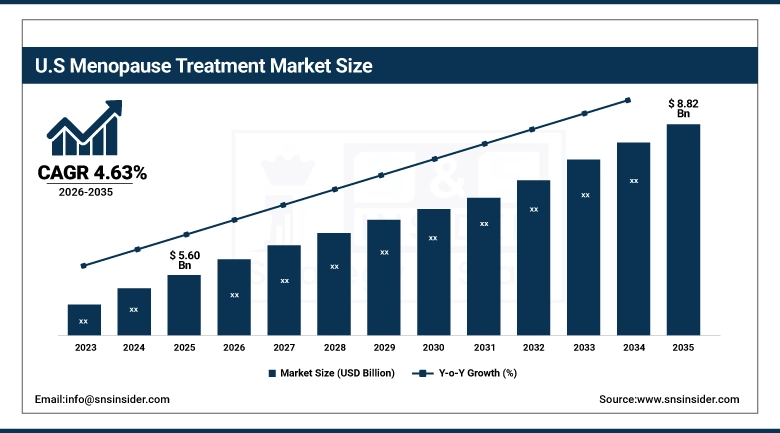

The U.S. Menopause Treatment Market was valued at USD 5.60 billion in 2025 and is expected to reach USD 8.82 billion by 2035, growing at a CAGR of 4.63% during 2026–2035.

The United States represents the world's largest menopause treatment market by revenue, driven by approximately 6,000 new women entering menopause daily, a well-developed pharmaceutical market with the broadest approved treatment portfolio globally, and a rapidly maturing menopause-focused healthcare ecosystem encompassing specialist menopause clinics, telehealth platforms, and employer health benefit programmes. U.S. market development has been accelerated by the 2023 FDA approval and commercial launch of fezolinetant (Veozah) by Pfizer, the first FDA-approved non-hormonal NK3 receptor antagonist for moderate to severe vasomotor symptoms, which has opened a new premium non-hormonal pharmaceutical segment and validated commercial interest in the menopause treatment category beyond conventional HRT. The presence of leading pharmaceutical companies including Pfizer, Organon, Amneal, AbbVie, and Bayer alongside a thriving specialty menopause telehealth sector provides the full treatment spectrum from prescription therapies through OTC supplements that U.S. women increasingly access through digital health platforms.

The October 2024 FDA acceptance of Bayer's NDA for elinzanetant backed by positive Phase III OASIS study outcomes, combined with the global debut regulatory authorisation of a novel non-hormonal menopause treatment that represents a landmark first approval in this category, confirm that the pharmaceutical innovation pipeline for menopause treatment is entering its most productive regulatory approval period in the market's history. The sequence of new non-hormonal therapy approvals, followed by anticipated biosimilar and generic HRT market expansion reducing treatment costs, will collectively drive U.S. menopause treatment market growth across both premium and accessible price segments through the 2026 to 2035 forecast period.

Menopause Treatment Market Segment Analysis

-

According to Treatment Type, Dietary Supplements and Herbal Remedies dominated with the largest market share in 2025 driven by widespread consumer adoption of phytoestrogen, black cohosh, and targeted nutraceutical formulations as first-line or complementary symptom management; Non-Hormonal Therapies are the fastest-growing treatment type driven by newly approved NK3 receptor antagonists and expanding SSRI and SNRI prescribing for menopause management.

-

In terms of Route of Administration, Oral dominated with the largest share in 2025 as the most widely prescribed and consumer-preferred administration format for both pharmaceutical and supplement therapies; Topical and Transdermal is the fastest-growing route driven by growing physician and patient preference for patch and gel hormone delivery that avoids first-pass hepatic metabolism.

-

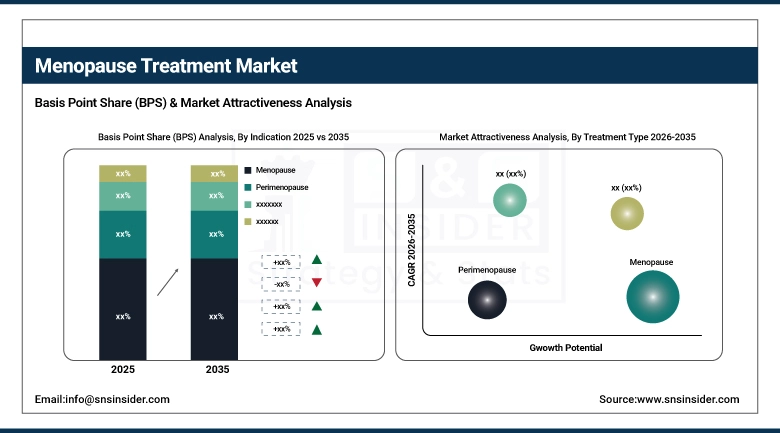

By Indication, Menopause dominated with the largest revenue share in 2025 as the primary treatment indication period; Postmenopause is a significant and growing segment driven by bone health, cardiovascular protection, and genitourinary syndrome of menopause management needs.

-

By Distribution Channel, Drug Stores and Retail Pharmacies dominated with approximately 42% of revenues in 2025 driven by high consumer trust, wide product availability, and pharmacist guidance access; Online Pharmacies are the fastest-growing channel through expanding e-prescription platforms, DTC supplement subscriptions, and telehealth prescription fulfilment.

By Treatment Type: Dietary Supplements dominate, Non-Hormonal Therapies grow fastest

Dietary Supplements and Herbal Remedies retained the dominant treatment type position in the Menopause Treatment Market in 2025, reflecting the enormous and diverse global consumer market for menopausal symptom relief products positioned outside the prescription pharmaceutical pathway. Phytoestrogen-containing products including soy isoflavone supplements, red clover extracts, and standardised black cohosh formulations are the most commercially significant supplement categories, collectively consumed by tens of millions of women globally seeking natural, accessible, and affordable approaches to managing hot flashes, night sweats, mood fluctuations, and sleep disturbance. The dietary supplement category's commercial dominance is sustained by its regulatory accessibility without prescription requirement, its cultural acceptability across diverse global markets including Asia Pacific where traditional herbal medicine is deeply embedded in healthcare culture, and its broad retail availability through pharmacies, health food stores, and online channels.

Non-Hormonal Therapies represent the fastest-growing treatment type through 2035, driven by the landmark approval of fezolinetant (Veozah) in 2023 as the first NK3 receptor antagonist specifically approved for moderate to severe vasomotor symptoms in menopausal women, opening a premium pharmaceutical category that addresses the estimated 40 to 50% of postmenopausal women who cannot or prefer not to use hormonal therapies due to breast cancer history, thromboembolic risk factors, or personal preference. The pharmaceutical innovation pipeline for non-hormonal menopause treatment is the most active in the market's history, with elinzanetant under FDA review in 2025 and multiple additional NK3 receptor antagonist and opioid receptor modulator programmes in Phase 2 and Phase 3 development that will create a competitive non-hormonal pharmaceutical market segment sustaining premium pricing and revenue growth through the forecast period.

By Route of Administration: Oral dominates, Topical and Transdermal grows fastest

Oral administration retained the dominant route of administration position in 2025, encompassing the widest range of menopause treatment forms including hormone replacement therapy tablets, NK3 receptor antagonist capsules, SSRI and SNRI prescription medications, and the extensive dietary supplement oral dosage form category of capsules, softgels, and functional food formats. Oral dosage forms benefit from patient familiarity, ease of use without clinical assistance, the full range of existing pharmacy dispensing infrastructure, and the straightforward dose escalation and de-escalation capability that menopause treatment management requires as symptom burden fluctuates across the perimenopause and early menopause periods.

Topical and Transdermal therapies are the fastest-growing route of administration, driven by growing physician and patient appreciation of the pharmacokinetic advantages of transdermal hormone delivery over oral hormone replacement therapy. Transdermal estrogen delivered through patches, gels, sprays, and emulsions avoids first-pass hepatic metabolism, resulting in lower circulating estrogen doses that achieve equivalent symptom relief to oral preparations, potentially with more favourable cardiovascular risk profiles including lower venous thromboembolism risk relative to oral conjugated estrogen preparations. The growing availability of body-identical transdermal estradiol gel and patch preparations, combined with micronized progesterone capsules that provide the full transdermal-oral combination therapy preferred by many menopause specialists, is driving transdermal therapy's market share growth among prescription hormone therapy users.

By Indication: Menopause dominates, Postmenopause grows alongside

The Menopause indication retained the dominant position in the Menopause Treatment Market in 2025, reflecting the clinical reality that symptomatic burden is typically greatest during the menopausal transition when vasomotor symptom frequency and severity peak, and treatment initiation rates are highest as women experience the most immediate and disruptive symptom impact. Hot flashes, night sweats, sleep disturbance, mood changes, and cognitive fogginess during menopause create the most compelling immediate quality-of-life impairment that drives women to seek medical consultation and treatment, sustaining the Menopause indication's commercial dominance in treatment prescription and supplement purchase.

Postmenopause represents a growing and commercially significant indication category, driven by the long-term health management needs that extend well beyond the acute vasomotor symptom phase of menopause into the decades of postmenopausal life where genitourinary syndrome of menopause, osteoporosis progression, cardiovascular risk management, and cognitive health maintenance create sustained demand for ongoing therapeutic intervention. The genitourinary syndrome of menopause, encompassing vaginal dryness, urinary urgency, and dyspareunia, is underdiagnosed and undertreated despite affecting the majority of postmenopausal women, representing a major market expansion opportunity as awareness campaigns and improved diagnostic practices progressively increase treatment-seeking rates for this prevalent and quality-of-life-impairing condition.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~83% |

|

Europe |

United Kingdom |

~28% |

|

Asia Pacific |

Japan |

~30% |

|

Middle East & Africa |

UAE |

~27% |

|

Latin America |

Brazil |

~44% |

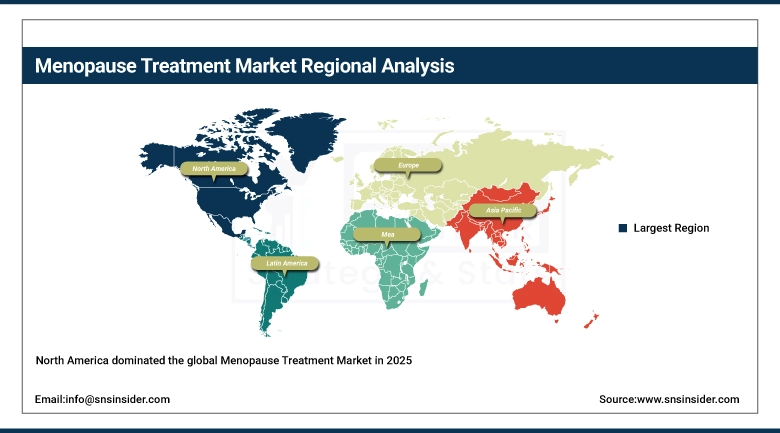

North America Menopause Treatment Market Insights

North America dominated the global Menopause Treatment Market in 2025, led by the United States which accounts for over 75% of North American revenues through its advanced healthcare infrastructure, broad portfolio of FDA-approved treatments, and the most developed physician awareness and patient advocacy ecosystem for menopause management globally. The U.S. market benefits from active pharmaceutical innovation including Pfizer's fezolinetant commercial programme, Bayer's elinzanetant regulatory submission, and multiple clinical development stage NK3 receptor antagonist programmes that will collectively expand the non-hormonal treatment market through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Menopause Treatment Market Insights

Asia Pacific is the fastest-growing regional Menopause Treatment Market, driven by rapidly aging female populations across Japan, China, South Korea, and India, improving access to women's health services, growing acceptance of modern treatments combined with traditional medicine, and increasing health awareness and urbanisation. Japan leads Asia Pacific through its advanced healthcare system, high geriatric female population proportion, and long-established cultural acceptance of phytoestrogen-rich traditional dietary practices that create a distinctive market for both pharmaceutical and botanical menopause treatments. China's growing disposable incomes and rapidly improving women's healthcare infrastructure are creating an expanding prescription menopause treatment market alongside strong traditional Chinese medicine utilisation.

Europe Menopause Treatment Market Insights

Europe represents a sophisticated menopause treatment market, shaped by NICE guidelines in the UK recommending HRT for appropriate candidates, German healthcare infrastructure enabling broad hormonal therapy access, and the active women's health advocacy community across Scandinavia driving policy change and clinical guideline evolution. The UK's NHS menopause service expansion, following the Government's Women's Health Strategy commitment to improve menopause care, is creating a significant market growth catalyst through improved diagnosis rates, standardised treatment pathways, and broader insurance coverage of HRT prescriptions.

Latin America and MEA Menopause Treatment Market Insights

Latin America and MEA are growing menopause treatment markets supported by improving women's healthcare access and rising health literacy. Brazil leads Latin American revenues through its large ageing female population and well-developed pharmaceutical market, while the UAE and Saudi Arabia lead MEA adoption through advanced private healthcare systems serving internationally educated women with strong health awareness. Supplement and botanical product markets are particularly significant in both regions as culturally accessible first-line options.

Menopause Treatment Market Growth Drivers:

-

Unprecedented global menopausal population growth and pharmaceutical innovation in non-hormonal treatment creating dual structural demand expansion

The primary structural growth drivers for the Menopause Treatment Market are the unprecedented demographic expansion of the global menopausal population toward 1.2 billion women by 2030 creating the largest-ever base of potential treatment recipients, combined with the most active pharmaceutical innovation pipeline in the market's history that is expanding beyond conventional HRT into novel non-hormonal mechanisms, personalised bioidentical hormone approaches, and digital health-enabled treatment management. Growing societal conversation around menopause, driven by high-profile celebrity advocacy and social media communities reducing the historic stigma that suppressed treatment-seeking, is simultaneously increasing the fraction of menopausal women who actively seek medical management compared to previous generations.

The global debut regulatory authorisation of a novel non-hormonal menopause treatment noted in SNS Insider's market intelligence, combined with the October 2024 FDA acceptance of Bayer's elinzanetant NDA backed by positive Phase III OASIS study outcomes, confirm that the regulatory and commercial momentum behind non-hormonal menopause pharmaceuticals is at an inflection point that will progressively convert the large unmet need population of women who avoid HRT into an addressable prescription pharmaceutical market. This market expansion from HRT to a broader pharmacological menu sustains the Menopause Treatment Market's reliable 5.44% CAGR through the 2026 to 2035 forecast period.

Menopause Treatment Market Restraints

-

HRT safety concerns from prior clinical studies limiting uptake, limited awareness in emerging markets, and high cost of novel prescription therapies restricting access

A significant restraint on the Menopause Treatment Market is the persistent physician and patient hesitancy toward hormone replacement therapy stemming from the 2002 Women's Health Initiative study that reported increased breast cancer and cardiovascular event risk in postmenopausal women taking combined estrogen-progestogen therapy, despite subsequent reanalysis demonstrating that the risks applied primarily to older postmenopausal women and that the risk-benefit balance is far more favourable for women beginning treatment at or near menopause onset. Limited physician education in menopause management across primary care in many markets means that women experiencing significant symptoms are often inadequately assessed and undertreated by clinicians without specialised menopause training. The premium pricing of newly approved non-hormonal therapies including fezolinetant at approximately USD 550 per month before insurance coverage creates access barriers for uninsured and underinsured women who cannot afford out-of-pocket pharmaceutical costs at this price level.

Menopause Treatment Market Opportunities

-

Menopause telehealth platform expansion, genitourinary syndrome treatment penetration improvement, and Asian market traditional-modern medicine integration

Menopause-focused telehealth platforms enabling women to access specialist clinical consultation, personalised treatment prescriptions, and ongoing symptom management support without geographic barriers represent the most scalable commercial opportunity for expanding menopause treatment penetration in markets where menopause-literate physicians are scarce. Genitourinary syndrome of menopause, affecting the majority of postmenopausal women but dramatically undertreated due to patient embarrassment and physician infrequency of assessment, represents a large addressable market that is progressively responding to awareness campaigns and improved diagnostic questioning in primary care consultations. Asian markets where traditional plant medicine and modern pharmaceutical treatments can be positioned as complementary rather than competing options represent high-growth market development opportunities for companies that can navigate cultural nuance in women's health communication.

Recent Developments:

-

October 2024: The U.S. FDA accepted Bayer's New Drug Application for elinzanetant, an NK3 receptor antagonist for moderate to severe vasomotor symptoms in menopause, backed by positive outcomes from three Phase III OASIS studies, with a July 2025 PDUFA review date.

-

March 2024: Theramex joined forces with ObsEva to market nolasiban, a novel oral treatment for fertility and hormone-related disorders, exemplifying the R&D pipeline broadening its scope across the women's reproductive health continuum.

-

2025: Pfizer continued expanding commercial access for fezolinetant (Veozah), the first FDA-approved non-hormonal NK3 receptor antagonist for moderate to severe vasomotor symptoms, through expanded insurance coverage negotiations and patient support programmes.

-

2025: Multiple major U.S. hospital networks completed expansion of integrated menopause specialist services, offering comprehensive symptom assessment, personalised treatment planning, and cognitive behavioral therapy alongside pharmacological options.

-

2025: Several European markets including France and Germany implemented improved reimbursement pathways for menopause specialist consultations and HRT prescriptions, addressing access inequity that previously required women to pay out-of-pocket for menopause care.

Menopause Treatment Market Key Players

-

Pfizer Inc.

-

Bayer AG

-

AbbVie Inc.

-

Organon and Co.

-

Amneal Pharmaceuticals LLC

-

Novo Nordisk AS

-

Teva Pharmaceutical Industries Ltd.

-

Theramex SAS

-

Hisamitsu Pharmaceutical Co. Inc.

-

Besins Healthcare

-

Shionogi and Co. Ltd.

-

TherapeuticsMD Inc.

-

Astellia (Mithra Pharmaceuticals SA)

-

Gedeon Richter plc

-

Procter and Gamble Co.

-

Nature's Way Products LLC

-

Metagenics Inc.

-

Garden of Life LLC

-

Solgar Inc.

-

Standard Process Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.81 Billion |

| Market Size by 2035 | USD 31.95 Billion |

| CAGR | CAGR of 5.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Hormonal Therapies, Non-Hormonal Therapies, Dietary Supplements and Herbal Remedies, Cognitive Behavioral Therapy and Lifestyle Interventions, Others) • By Route of Administration (Oral, Topical and Transdermal, Vaginal, Parenteral, Others) • By Indication (Perimenopause, Menopause, Postmenopause) • By Distribution Channel (Hospital Pharmacies, Drug Stores and Retail Pharmacies, Online Pharmacies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Pfizer Inc., Bayer AG, AbbVie Inc., Organon and Co., Amneal Pharmaceuticals LLC, Novo Nordisk AS, Teva Pharmaceutical Industries Ltd., Theramex SAS, Hisamitsu Pharmaceutical Co. Inc., Besins Healthcare, Shionogi and Co. Ltd., TherapeuticsMD Inc., Astellia (Mithra Pharmaceuticals SA), Gedeon Richter plc, Procter and Gamble Co., Nature's Way Products LLC, Metagenics Inc., Garden of Life LLC, Solgar Inc., Standard Process Inc. |

Frequently Asked Questions

Ans: The Menopause Treatment Market is expected to grow at a CAGR of 5.44% from 2026 to 2035.

Ans: The Menopause Treatment Market was valued at USD 18.81 billion in 2025.

Ans: The unprecedented demographic expansion of the global menopausal population toward 1.2 billion women by 2030, combined with the most active pharmaceutical innovation pipeline in the market's history including newly approved non-hormonal NK3 receptor antagonists, growing societal conversation reducing treatment-seeking stigma, and improving insurance coverage expanding access to evidence-based menopause therapies.

Ans: Dietary Supplements and Herbal Remedies dominated the market in 2025 with the largest revenue share, driven by the extensive global consumer market for phytoestrogen supplements, black cohosh, red clover, and targeted nutraceutical formulations accessed without prescription requirements through pharmacies, health food stores, and online channels by tens of millions of women globally.

Ans: North America dominated with the largest revenue share in 2025, led by the United States which accounted for over 75% of North American revenues through its advanced pharmaceutical market, the broadest FDA-approved treatment portfolio globally, and the most developed physician awareness and patient advocacy ecosystem for menopause management.

Get in Touch