Cellular Health Screening Market Report Scope & Overview:

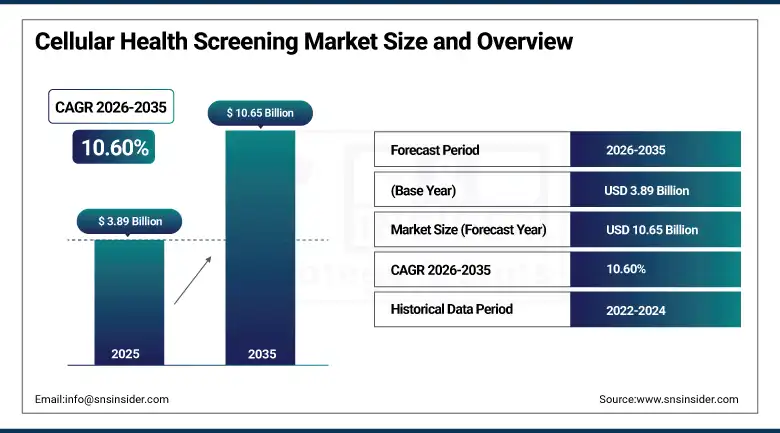

The Cellular Health Screening Market was valued at USD 3.89 Billion in 2025 and is expected to reach USD 10.65 Billion by 2035, growing at a CAGR of 10.60% from 2026–2035.

Cellular health screening market growth is driven by consumers' increased focus on personalized diagnostics and preventive care which drives changes in how they monitor biological aging, metabolism, and risk of diseases. Cellular health screening includes telomere length testing, micronutrients testing, and biomarkers panels which enable deeper insight into cellular aging and risks of chronic disease compared to regular clinical screening tests. The combination of wearables and cellular health screening transforms modern medicine in terms of continuous real-time tracking of critical health parameters, such as ECG, brain activity, and heart rate variability, beyond clinical setting. Higher expenditures on preventive diagnostics in healthcare, growing demands for instant and accurate point-of-care devices, as well as increasing awareness about personalized approaches among consumers fuel market growth above baseline level.

Genova Diagnostics introduced Fatty15 Test measuring pentadecanoic acid level to monitor cellular health in July 2024 with the assistance of Seraphina Therapeutics. This home test enables convenient monitoring of C15:0 levels contributing to overall cellular health. Fatty15 Test is specifically designed to help people deal with the problem known as Cellular Fragility Syndrome. Launch of this product illustrates current industry tendency towards biomarker testing at home for aging-related and metabolism purposes.

Market Size and Forecast

-

Market Size in 2026E: USD 4.30 Billion

-

Market Size by 2035: USD 10.65 Billion

-

CAGR: 10.60% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Cellular Health Screening Market - Request Free Sample Report

Cellular Health Screening Market Trends

-

Wearable device integration is enabling continuous, real-time tracking of cellular health metrics including ECG and heart rate variability.

-

Growing consumer demand for at-home testing kits is driving accessible, non-invasive cellular health screening adoption.

-

Rising healthcare spending on preventive diagnostics is accelerating early disease detection and personalized health management investment.

-

Telomere length and biological age testing adoption is expanding among health-conscious consumers seeking longevity insights.

-

Telemedicine integration with continuous health monitoring systems is enabling proactive chronic condition management for remote patients.

The U.S. Cellular Health Screening Market Outlook

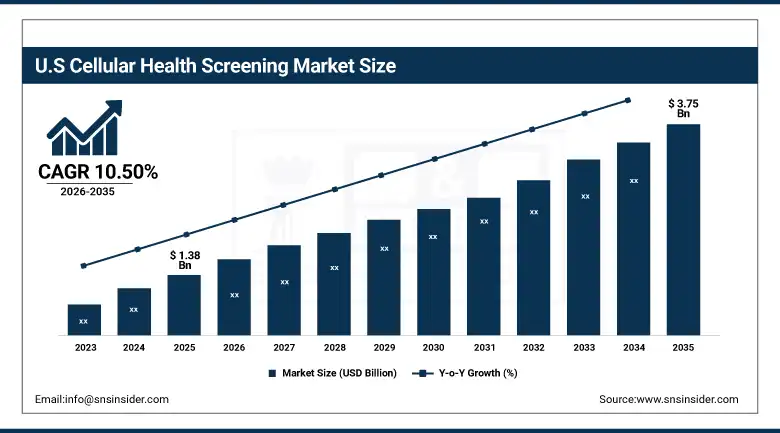

The U.S. Cellular Health Screening Market was valued at approximately USD 1.38 Billion in 2025 and is expected to reach approximately USD 3.75 Billion by 2035, growing at a CAGR of approximately 10.50%.

The US holds the position of leader in the North American revenue generated from cellular health screening on account of the high level of adoption of innovative technologies in healthcare, greater consumer awareness levels, and well-developed healthcare infrastructure in the country. The existence of prominent diagnostic companies such as Quest Diagnostics and LabCorp, as well as government programs encouraging preventive care, have led to a constant market growth. High demand for personalized and continuous monitoring screening methods, together with the rising number of cases of chronic diseases and aged population, stimulate domestic consumption of cellular health screening products.

The acquisition of select assets from BioReference Health’s diagnostics business by LabCorp took place in March 2024 and improved its laboratory testing services, providing greater access to clinical diagnostics and women’s health offerings in the United States. This purchase enhanced the testing capacity of LabCorp and allowed the company to handle the rising consumer and clinical demands for cellular health screening tests offered.

Cellular Health Screening Market Segment Analysis

-

By Sample Type, blood segment dominated the cellular health screening market with approximately 48% share in 2025, while the urine segment is the fastest growing driven by demand for non-invasive, affordable diagnostic approaches.

-

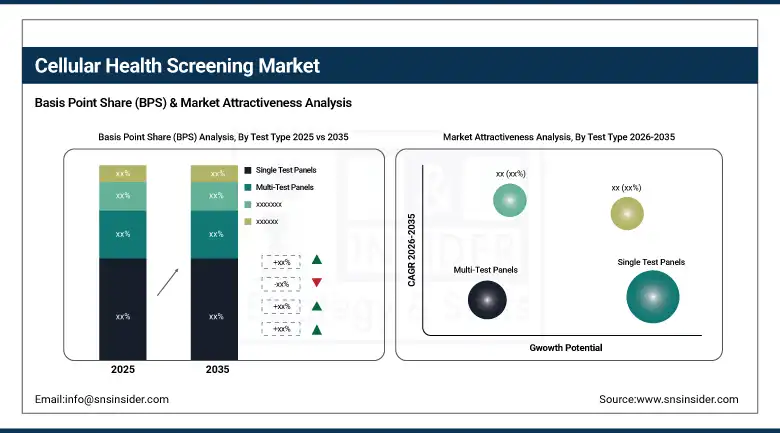

By Test Type, single test panels segment dominated the cellular health screening market with approximately 81% share in 2025, while the multi-test panels segment is the fastest growing driven by comprehensive preventive health diagnostics demand.

-

By Collection Site, the hospital segment dominated the cellular health screening market with the largest share in 2025, while the home segment is the fastest growing driven by rising consumer demand for convenient at-home diagnostics.

By Sample Type, blood dominates, urine grows fastest

The blood segment took the lead in terms of revenue share with around 48% in 2025. The major reason behind this trend is the usage of blood tests in early diagnosis and health evaluation. Blood screenings are highly popular across healthcare facilities and even at home because of their high level of accuracy, convenience, and the detailed analysis of different parameters, such as cholesterol, glucose, the state of the liver, as well as diseases, such as cancer, heart problems, and diabetes. Technological advancements made blood tests faster and cheaper; therefore, the popularity of this category among others can be explained by the high demand for blood tests that are easily performed in clinical settings as well as at home via portable health screening kits.

Among all other types, urine is predicted to exhibit the highest growth rate between 2026 and 2035, owing to the rising popularity of convenient and inexpensive diagnostic methods. Testing with urine samples can be done much more conveniently, without being too invasive, offering highly useful data that can be used to diagnose a number of conditions such as kidney diseases, diabetes, UTIs, metabolic issues and others. Since the technology has developed significantly over time, tests using urine samples have become much more precise and accurate, hence gaining increased popularity as a means of early detection.

By Test Type, single test panels dominate, multi-test panels grow fastest

Single Test Panels held the highest revenue share of about 81% in the cellular health screening market in 2025. Single test panels will remain the dominating revenue segment throughout the forecast period. The use of these types of tests matches the increasing demand for more straightforward and focused health tests that can deliver rapid results with ease. These types of tests are usually used to diagnose only one health marker or parameter, like cholesterol level, blood glucose, biomarker, etc., which increases efficiency and makes testing more convenient in the healthcare facilities. Single test panels are cheaper and semi-automated; they are usually done in routine testing or profiling of patients.

Multi-Test Panels are expected to be the fastest-growing segment from 2026 to 2035 due to their ability to conduct health screens simultaneously by using just one sample of blood or body tissue. This will significantly reduce costs involved and make the test process more efficient and quick. Multi-test panels provide comprehensive information about patients' health condition that allows detecting abnormalities and preventing diseases in their early stages, thus contributing to the overall preventive medicine sector development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Cellular Health Screening Market Insights

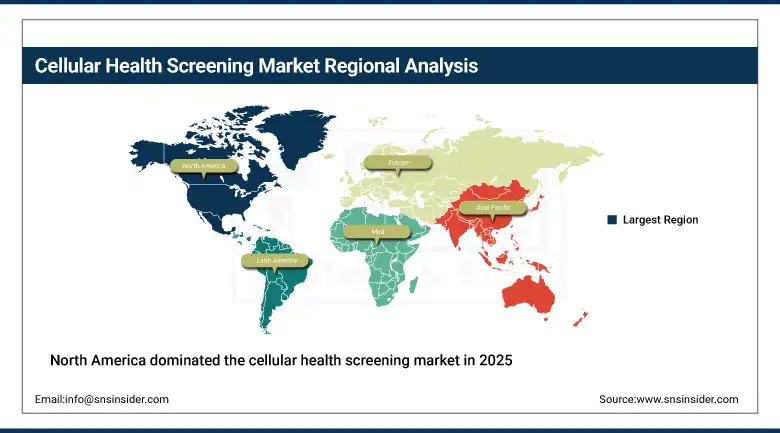

North America dominated the cellular health screening market in 2025, accounting for around 47% of the revenue share. The region’s dominance can be attributed to high adoption of advanced healthcare technologies, increasing consumer awareness, and robust healthcare infrastructure. The presence of leading diagnostic companies, coupled with government initiatives promoting preventive healthcare, has fostered sustained market growth.

The United States accounts for approximately 82.5% of North American revenues through Quest Diagnostics, Labcorp, and OPKO Health’s extensive testing infrastructure. Canada contributes supplementary revenues through its growing preventive healthcare investment and expanding adoption of personalised health screening among Canadian consumers and clinical institutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cellular Health Screening Market Insights

Europe is a significant cellular health screening market where strong consumer health consciousness and established clinical diagnostic infrastructure sustain steady demand. Germany accounts for approximately 22.4% of European revenues through Immundiagnostik AG’s telomere testing and immunodiagnostic product portfolio and the country’s advanced clinical laboratory network.

Spain’s Life Length telomere testing leadership, the United Kingdom’s growing direct-to-consumer diagnostics sector, and France’s preventive healthcare investment collectively sustain European market development. European consumer interest in biological age testing and longevity diagnostics is creating above-baseline demand for specialised cellular health screening panels.

Asia Pacific Cellular Health Screening Market Insights

Asia Pacific is the fastest-growing regional cellular health screening market, fueled by rapid developments in healthcare technology, growing awareness regarding preventive care, and increasing prevalence of chronic diseases. The growing middle class, coupled with advancements in healthcare infrastructure and government programmes promoting health awareness, is facilitating uptake across the region.

China accounts for approximately 44.8% of Asia Pacific revenues through its expanding diagnostic laboratory network and growing consumer interest in preventive health screening. India’s DNA Labs India and Japan’s advanced clinical diagnostics sector are driving rising need for economical, accessible, and personalized health diagnostics across the region.

MEA & Latin America Cellular Health Screening Market Insights

The UAE leads MEA revenues through its advanced healthcare infrastructure and growing consumer wellness sector investment. Saudi Arabia’s Vision 2030 healthcare transformation programme creates growing institutional demand for preventive diagnostic services across government and private healthcare providers.

Brazil leads Latin American revenues through its large private healthcare sector and growing consumer interest in personalized diagnostics. Mexico and Colombia contribute growing secondary demand through expanding private clinical laboratory networks and rising preventive healthcare investment.

Market Dynamics

Growth Drivers: Wearable device integration enabling continuous monitoring and rising preventive healthcare spending driving market expansion

The combination of wearable devices and cellular health screenings is revolutionizing the field of healthcare, as it allows for continual monitoring of health statistics in real-time. Thanks to recent technological advances in mobile computing and wearable devices, it is now possible for the user to monitor his or her cellular health and other important metrics, such as ECG readings, cognitive ability, and heart rate variability, outside conventional hospital settings. High levels of acceptance among pregnant women and people with cognitive disabilities have been observed; a survey has found that 91% of expecting women would use wearable ECG technology during their pregnancy.

There is an increasing trend towards investing in preventive diagnostics in the US, with estimated spending on it rising from USD 1.13 billion in 2023 to USD 2.78 billion by 2032. With increased interest worldwide towards preventive healthcare, it can be expected that the need for cellular health screening will increase in the years to come, especially considering that the convergence of multiple wearable devices produces greater results than the utilization of a single device.

Restraints: High device and testing costs limiting adoption among low-income populations and resource-constrained healthcare markets

The high costs associated with advanced wearable devices and diagnostic tests present a significant challenge to widespread adoption of cellular health screening, particularly for low-income populations. While wearable devices offer significant benefits such as continuous monitoring and real-time health data, their high initial cost, along with recurring expenses for diagnostic tests and remote monitoring programmes, can be a financial burden for many individuals. This makes it difficult for a large segment of the population to access these technologies, particularly in regions with limited healthcare resources.

For low-income groups, these financial barriers could prevent individuals from benefiting from the advanced health tracking capabilities that wearable devices offer, ultimately restricting overall market growth potential. As a result, the potential for market expansion remains limited in price-sensitive markets, and broader healthcare accessibility remains a persistent challenge that diagnostic companies and policymakers must address through cost reduction and insurance coverage expansion initiatives.

Opportunities: Cost-effectiveness improvements and remote monitoring expansion creating broader market accessibility opportunities

The growing demand for wearable health devices and remote monitoring solutions presents significant opportunities in the cellular health screening market. As production costs decrease, cost-effectiveness ratios for screening technologies including wearable telephonic cardiogram monitoring are improving, raising important questions about expanding access to such technology across demographics. More affordable alternatives such as pulse palpation and 12-lead ECG can extend coverage in low-resource environments, broadening the addressable market beyond premium wearable device segments.

Teenagers and young adults increasingly access telemedicine collection services through smartphones for remotely addressing acute and chronic conditions, while continuous health monitoring systems integrated with telehealth platforms open a pathway toward more proactive healthcare approaches for chronic conditions. This integration of remote diagnostics with telehealth infrastructure is improving patient outcomes while creating new commercial channels for cellular health screening providers beyond traditional clinical and laboratory settings.

Recent Developments:

-

2024: Genova Diagnostics launched its at-home Fatty15 Test to assess pentadecanoic acid levels for cellular health, developed in collaboration with Seraphina Therapeutics, offering an accessible solution for monitoring cellular fragility and metabolic health.

-

2024: Labcorp announced the acquisition of select assets from BioReference Health’s diagnostics business, enhancing its laboratory services network and expanding access to clinical diagnostics and women’s health services across the United States.

-

2023: SpectraCell Laboratories expanded its micronutrient and telomere testing panel offerings, enhancing personalized diagnostic capability for healthcare providers and consumers seeking comprehensive cellular health and nutritional status assessment.

Cellular Health Screening Market Key Players are:

-

Life Length S.L.

-

SpectraCell Laboratories Inc.

-

RepeatDx Inc.

-

Cell Science Systems Corp.

-

Quest Diagnostics Incorporated

-

Laboratory Corporation of America Holdings

-

OPKO Health Inc.

-

Genova Diagnostics Inc.

-

Immundiagnostik AG

-

DNA Labs India

-

BioReference Health LLC

-

Innovatics Laboratories Inc.

-

TruDiagnostic Inc.

-

Tally Health Inc.

-

Elysium Health Inc.

-

GlycanAge Ltd.

-

InsideTracker Inc.

Cellular Health Screening Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.89 Billion |

| Market Size by 2035 | USD 10.65 Billion |

| CAGR | CAGR of 10.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Test Type (Single Test Panels, Multi-Test Panels) • By Sample Type (Blood, Saliva, Serum, Urine) • By Collection Site (Home, Office, Hospital, Diagnostic Labs) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Length S.L., SpectraCell Laboratories Inc., RepeatDx Inc., Cell Science Systems Corp., Quest Diagnostics Incorporated, Laboratory Corporation of America Holdings, OPKO Health Inc., Genova Diagnostics Inc., Immundiagnostik AG, DNA Labs India, BioReference Health LLC, Innovatics Laboratories Inc., TruDiagnostic Inc., Tally Health Inc., Elysium Health Inc., GlycanAge Ltd., and InsideTracker Inc. |

Frequently Asked Questions

The Cellular Health Screening Market is expected to grow at a CAGR of 10.60% from 2026 to 2035.

The Cellular Health Screening Market was valued at USD 3.89 Billion in 2025.

Rising adoption of wearable devices enabling continuous health monitoring, increasing healthcare spending on preventive diagnostics, and growing consumer demand for personalized, at-home testing solutions are the primary growth factors.

The Blood segment dominated the Cellular Health Screening Market with approximately 48% share in 2025.

North America dominated the Cellular Health Screening Market with approximately 47% revenue share in 2025.

Get in Touch