Metallocene LDPE Market Report Scope & Overview:

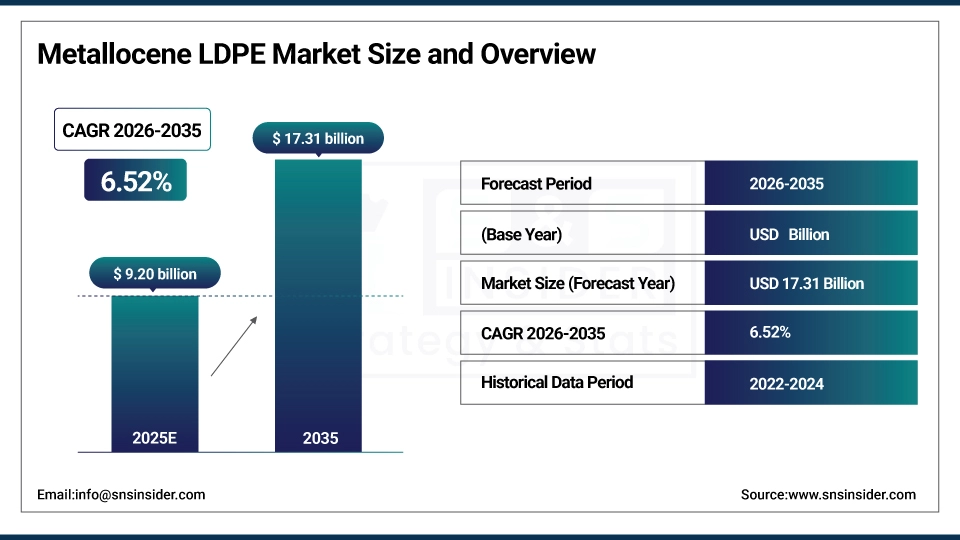

The Metallocene LDPE Market size was valued at USD 9.20 billion in 2025 and is expected to reach USD 17.31 billion by 2035, growing at a CAGR of 6.52% over the forecast period of 2026-2035.

High growth in the metallocene LDPE market is being propelled by the development of polymer processing technology, in flexible packaging films, industrial films, and where specialty polyethylene grades are being used to strengthen performance in mLLDPE films and flexible packaging. Recycling and biodegradability trends are increasing the need for sophisticated LDPE materials, contributing to metallocene LDPE market growth. For instance, ExxonMobil’s 2022 release of Exceed S polyethylene is the latest example of how metallocene LDPE suppliers drive innovation to enhance processability and toughness.

Metallocene LDPE Market Size and Forecast:

-

Market Size in 2025: USD 9.20 Billion

-

Market Size by 2035: USD 17.31 Billion

-

CAGR: 6.52% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Metallocene LDPE Market - Request Free Sample Report

Key trends in the Metallocene LDPE Market:

-

Growing demand for high-performance flexible packaging materials in food, beverage, and consumer goods industries due to superior clarity, toughness, and sealability.

-

Increasing adoption of metallocene LDPE in medical and pharmaceutical packaging, driven by rising hygiene standards and the need for contamination-resistant materials.

-

Shift toward lightweight and downgauged plastic films, as metallocene LDPE enables material reduction without compromising strength or durability.

-

Rising focus on sustainability, with manufacturers developing recyclable and mono-material packaging solutions using metallocene-based polyethylene.

-

Expansion of e-commerce and logistics sectors, boosting demand for stretch films, shrink films, and protective packaging made from metallocene LDPE.

-

Technological advancements in catalyst systems and polymerization processes, improving product consistency and performance characteristics.

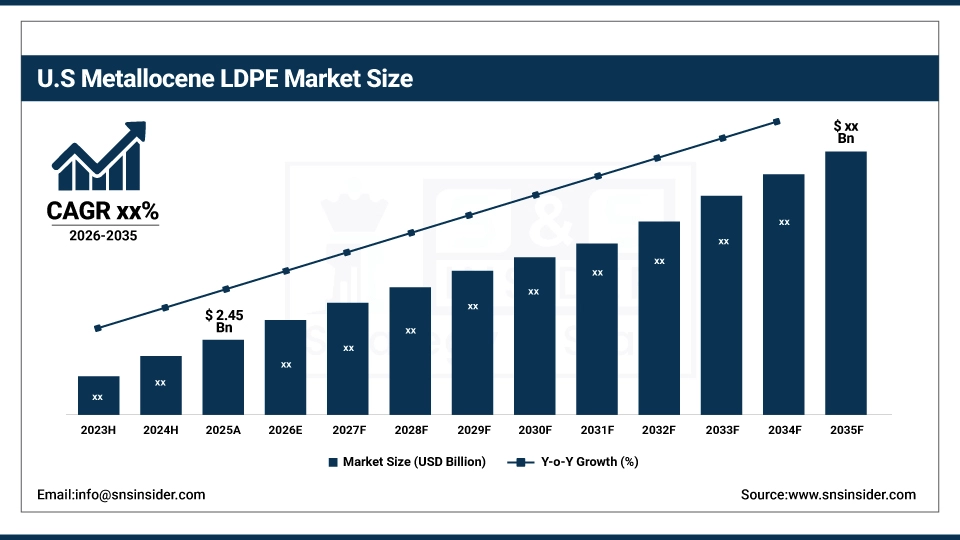

The U.S. metallocene LDPE market size was valued at approximately USD 2.45 billion in 2025 and is projected to witness steady growth through 2035, supported by strong demand from packaging, healthcare, and industrial applications. Increased emphasis on high-quality flexible packaging, coupled with innovations in sustainable polyethylene solutions, continues to drive market expansion across the country. Polyethylene and with it, metallocene LDPE market size, accounts for about 30% of Europe’s overall polymer requirements, according to Plastics Europe. These numbers illustrate the possible growth of the metallocene LDPE market size, as mono-material applications gain traction due to increasingly strict regulations.

Metallocene LDPE Market Drivers:

-

Enhanced Barrier Performance Enables High‑Value Flexible Packaging Applications

The growth of the Metallocene LDPE market is attributed to enhanced polymer processing technology that provides greater sealability and clarity for flexible packaging films and industrial films. One example is ExxonMobil’s ExceedS grades, which enable converters to produce more robust, thinner films with mLLDPE, but without compromising on performance. These specialty polyethylenes allow metallocene LDPE to gain market share by addressing consumer needs for shelf appeal and longevity. This is in line with general metallocene LDPE market dynamics in favor of lightweight, barrier packaging solutions, enabling growing consumer trends, and brands’ sustainability initiatives.

-

Regulatory Push for Recyclability Drives Adoption of Advanced LDPE Materials

Growing regulatory pressure to use recyclable and biodegradable packaging is influencing the demand for metallocene LDPE. LDPE (Resin Identification Code 4) has a 5.7% recycling rate in the U.S., as reported by the EPA. This space provides an opportunity for the mLDPE market as brands shift toward mono-material flexible packaging films. Metallocene LDPE manufacturers are adopting new LDPE materials to adhere to the latest quality standards that will further accelerate market share and enhance the growth of the metallocene LDPE market.

Metallocene LDPE Market Restraints:

-

Competition From mLLDPE Films and Other Polyolefins Impacts Market Share Potential

The metallocene LDPE market study also reveals intensifying competition from mLLDPE films and other polyolefins providing downgauging and cost advantages. Although there is a difference between clear and sealing properties between the new generations of LDPEs and the regular LDPEs, converters looking for an alternative to LDPE mLLDPE alternatives may become an issue for the metallocene LDPE market share. It is a pattern that curbs the growth of the metallocene LDPE market size, despite the technical advantages it offers, as brand owners and converters balance performance versus price and availability across the broader metallocene LDPE market.

Metallocene LDPE Market Segmentation Analysis:

By Catalyst Type

Zerconocene dominated the metallocene LDPE market in 2025 with a 45.5% share, on account of the catalyst, which helps in uniform polymer branching structure, hence thinner flexible packaging materials can be manufactured with higher tensile strength. This niche polyethylene allows for excellent downgauging without performance loss, which is why converters in packaging and industrial films prefer this formula to the American Chemistry Council. These metallocene LDPE market trends demonstrate increased demand for high-end LDPE with stronger metallocene LDPE market share and incentive for metallocene LDPE companies to innovate and upgrade for green flexible packaging.

Zerconocene is the fastest-growing catalyst type with a CAGR of 6.73%, on account of increasing demand for specialty polyethylene used in food and medical packaging applications, which ensure food safety and sanitation. According to the Flexible Packaging Association, converters continue to recognize the benefits of Zerconocene-catalyzed mLLDPE films for premium shelf appeal and robust sealing that improves product life on the shelf. Such developments in metallocene LDPE markets in turn exacerbate the metallocene LDPE market surge and augment metallocene LDPE market appeal in regulated industries that seek secure, sustainable, and innovative LDPE products.

By Application

Films dominated the metallocene LDPE market in 2025 with a 50.2% share as they are widely used in shrink films, stretch wraps, and agricultural covers. Light protective films are key to reducing food spoilage and waste, the U.S. Department of Agriculture says. These metallocene LDPE market trends are influencing specialty polyethylene demand for the clear, tough, flexible packaging films. This is helping extract products of metallocene LDPE to grow its share of the total metallocene LDPE market, driving the polymer processing technology in the next generation of LDPE materials for packaging benefits.

Sheets are the fastest-growing application segment with a CAGR of 7.61%, driven by the demand in foodservice, medical blister packs, and construction liners. Interest in recyclable rigid formats is growing, according to the National Association for PET Container Resources, which has been encouraging converters to adopt mLDPE sheets with formability and compliance. This metallocene LDPE market trend supports the growth of the metallocene LDPE market size, adding share to specialty polyethylene for long-lasting, eco-friendly packaging and industrial use.

By End-use Industry

Packaging dominated the metallocene LDPE market in 2025 with a 41.6% share, driven by the increasing demand for lightweight, durable, and flexible packaging films in retail and e-commerce. Mono-material solutions supporting recycling, along with the push for specialty polyethylene, continue to keep brands involved in design. These metallocene LDPE market trends help keep the metallocene LDPE market shares high and encourage metallocene LDPE manufacturers to work towards producing new & innovative LDPE materials inspired by the circular economy’s strategies to boost the metallocene LDPE market.

Food and beverages are the fastest-growing end-use industry with a CAGR of 7.05%, as there is an increasing demand for more protective, barrier packaging that can also be recycled from consumers wishing to purchase safer and fresher products. More stringent food-contact regulations of the U.S. Food and Drug Administration (FDA) encourage the use of mLLDPE films having excellent seal integrity. Such metallocene LDPE market trends strengthen the metallocene LDPE market and enlarge the metallocene LDPE market size, where specialty polyethylene fulfills new sustainable, compatible flexible packaging solutions.

Metallocene LDPE Market Regional Insights:

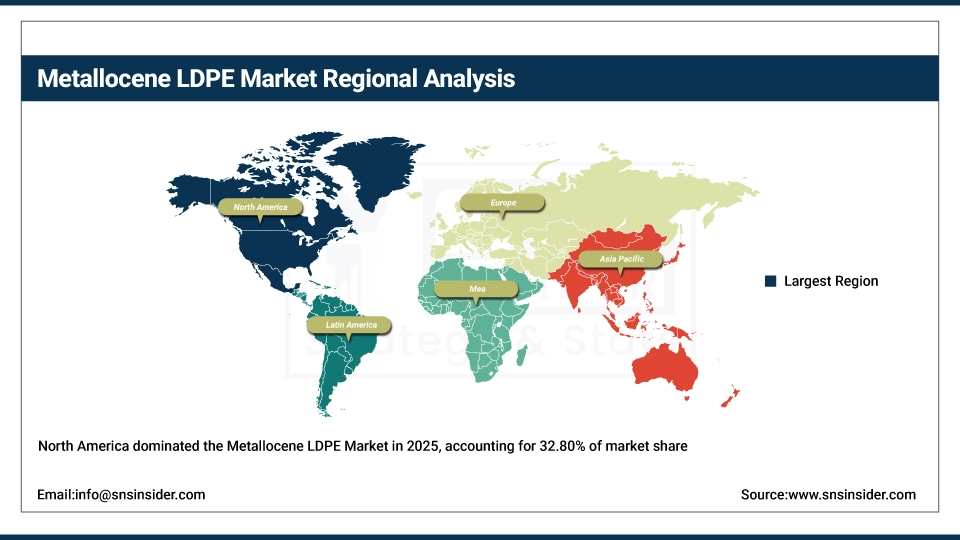

North America Dominates the Metallocene LDPE Market in 2024

The largest region for the metallocene LDPE market in 2024 was North America with a 32.80% market share, attributed to substantial investment made in polymer processing technology and recycling infrastructure and bio-degradation activities. Robust demand for speciality PE and higher performance LDPE grades in flexible packaging and industrial films provides ongoing support to regional leadership. Advanced LDPE materials are used more and more to fulfill performance and sustainability needs, per the American Chemistry Council.

Metallocene LDPE manufacturers are increasing their production capacities in the region to adhere to sustainability standards, and there are industry-led initiatives like the Sustainable Packaging Coalition’s FlexPack Recovery Challenge encouraging participation for better recycling solutions. These joint accomplishments greatly strengthen North America’s presence in the world of metallocene LDPE.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Leads the North American Metallocene LDPE Market

The United States dominates the North American metallocene LDPE market with a market size of USD 2.04 billion, projected to reach USD 3.35 billion by 2035, representing nearly 72% regional share. Growth is supported by leading production of mLLDPE films and widespread adoption of advanced LDPE materials in food packaging and retail applications.

Regulatory moves by the Environmental Protection Agency favoring recycling and biodegradable materials continue to bolster the use of specialty polyethylenes, as converters develop films that are thinner but stronger with more flex. Big producers including Butyl ExxonMobil beds Polymers and Dow Chemical have pumped money into high-tech polymer processing, giving the USA-based market a competitive edge as well as a strong sustainability story

Asia Pacific is the Fastest-Growing Metallocene LDPE Market

Asia Pacific is projected to be the fastest-growing region in the metallocene LDPE market from 2026 to 2035, registering the highest CAGR of 6.80%. Rapid growth is fueled by rising demand for flexible packaging films and industrial films in China and India.

The use of speciality polyethylene in ecofriendly packaging solution is being promoted by bodies like China Plastics Processing Industry Association where as Food and Beverage sector is growing rapidly in India thereby promoting better grades of LDPE and modern polymer processing technology. Together these trends drive the growth in market and market share of regional metallocene LDPE.

Europe Metallocene LDPE Market Insights

Europe was third leading metallocene LDPE market in 2025 contributing for a potential share with over 26.10% owing to the stringent environmental norms and early acceptance of advanced LDPE products. In the region, strong requirement from flexible packaging and industrial film applications in Germany and France are some of the factors driving regional growth, while meeting European chemical standards is a priority.

This approach appears to be increasingly common for metallocene LDPE and mLLDPE producers in Europe, where market trends are dominated by recycling solutions and biodegradable materials. This step is expected to strengthen long-term market competition and sustainability performance of Europe, thereby, consolidating its position in influencing the future of global metallocene low density polyethylene market.

Competitive Landscape of the Metallocene LDPE Market:

ExxonMobil

ExxonMobil is a world leader in metallocene polyethylene technology with its Exceed and Enable metallocene LEPE/LLDPE product families known throughout the industry. It specializes in high-performance flexible packaging films that are strong, clear and down gauge able. Its position in the metallocene LDPE market is pivotal, especially in food packaging and industrial films as well as mono-material solutions in response to sustainability trends.

-

March 2025: ExxonMobil started operations at a new linear LLDPE unit in Huizhou, China to strengthen supply of advanced metallocene polyethylene grades

Dow

Dow is a leading producer of metallocene LDPE under brands such as ELITE and INNATE, which are used in packaging, hygiene and industrial end use applications. Light weighting, improved seal performance and recyclability are focus of resin designing, company says. Dow is a leader in driving the increased adoption of sustainable packaging through innovative resin and catalyst solutions.

-

July 2024: Dow partnered with Mura Technology to scale chemical recycling of flexible packaging including metallocene LDPE, targeting 600,000 tons/year capacity to convert waste films into feedstock.

LyondellBasell

The metallocene LDPE is also an area of strength for LyondellBasell with proprietary Metocene catalyst technology. The company provides high performance polyethylene used primarily in flexible packaging and film applications. Its relative strength is the development and licensing of catalyst technology, which provides for consistent resin quality and performance.

-

March 2024: Completed acquisition of APK AG’s plastic recycling technology, enabling processing of multilayer films containing metallocene LDPE previously considered non-recyclable.

SABIC

SABIC is a world leader in providing metallocene LDPE resins for packaging, agriculture and industrial sectors. The company uses high-level polymer science to provide materials that have improved toughness and clarity, along with process-ability. SABIC’s robust world-class manufacturing footprint ensures reliable supply to high-growth regions.

-

January 2024: Expanded its TRUCIRCLE portfolio with metallocene LDPE grades containing up to 50% recycled content to support sustainability target

Metallocene LDPE Companies are:

-

ExxonMobil

-

Dow

-

SABIC

-

Borealis

-

INEOS

-

LG Chem

-

TotalEnergies

-

Chevron Phillips Chemical

-

Reliance Industries

-

Formosa Plastics

-

Westlake Corporation

-

QAPCO

-

Hanwha Solutions

-

PTT Global Chemical

-

Mitsui Chemicals

-

PetroChina

-

Sinopec

-

Versalis

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.20 billion |

| Market Size by 2035 | USD 17.31 billion |

| CAGR | CAGR of 6.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Catalyst Type (Zerconocene, Ferrocene, Tetanocene, Others) •By Application (Films, Sheets, Extrusion Coating, Injection Molding, Blow Molding, Wire & Cable Insulation, Others) •By End-use Industry (Packaging, Food and Beverages, Automotive, Building and Construction, Agriculture, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles |

ExxonMobil, Dow, LyondellBasell, SABIC, Borealis, INEOS, Braskem, LG Chem, TotalEnergies, Chevron Phillips Chemical, Reliance Industries, Formosa Plastics, Westlake Corporation, QAPCO, Hanwha Solutions, PTT Global Chemical, Mitsui Chemicals, PetroChina, Sinopec, Versalis |

Get in Touch