Metrology Equipment Market Report Scope & Overview:

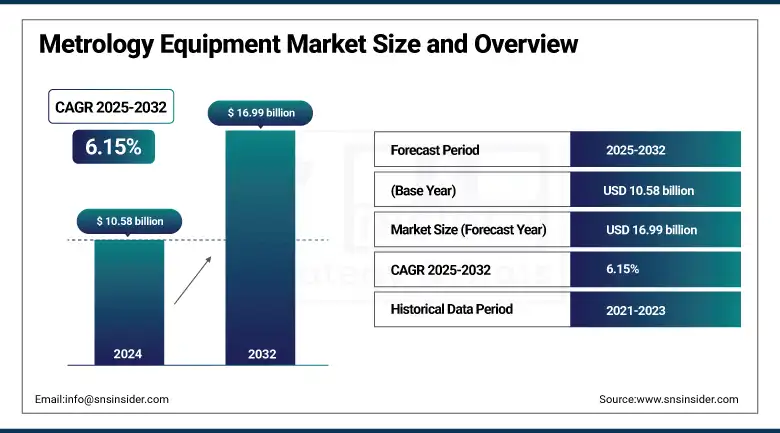

The Metrology Equipment Market size was valued at USD 10.58 billion in 2024 and is expected to reach USD 16.99 billion by 2032, growing at a CAGR of 6.15% over the forecast period of 2025-2032.

Metrology equipment market growth is attributed to the rising demand for precision measurement in advanced manufacturing and quality control applications for automotive, aerospace, electronics, and medical sectors. Market includes Coordinate Measuring Machines (CMMs), Optical Digitizers and Scanners (ODS), and X-ray & CT systems, which help perform precise dimensional analysis and defect detection. With the expansion of Industry 4.0, IoT, and automation, the operational capability of the equipment is also expanding while also providing real-time data. The metrology equipment market share is growing in areas investing in smart factories. Metrology equipment market analysis highlights the adoption of non-contact and AI-enabled solutions for enhanced productivity and quality assurance.

To Get more information On Metrology Equipment Market - Request Free Sample Report

“For instance, in May 2025, Hexagon conducted a high-speed and ultra-precise 3D inspection to address the pressing need for next-generation automation in manufacturing and quality control within the metrology equipment market.”

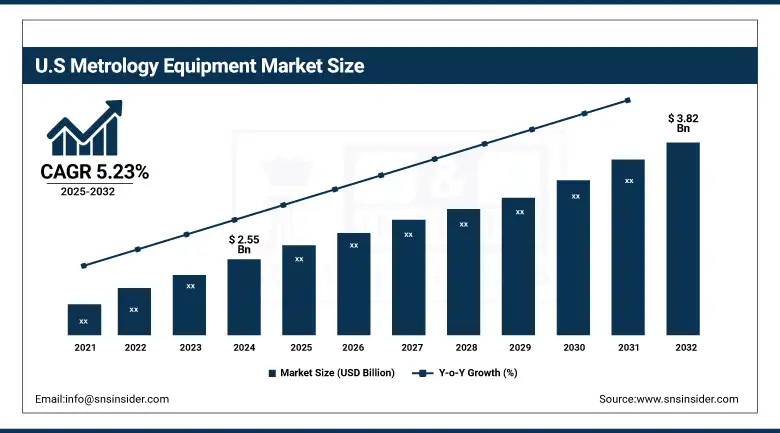

The U.S. metrology equipment market size was valued at USD 2.55 billion in 2024 and is expected to reach USD 3.82 billion by 2032, growing at a CAGR of 5.23% over the forecast period of 2025-2032.

High growth momentum in the metrology equipment market due to the automotive, aerospace, and semiconductor industries will boost growth in the U.S. metrology equipment market. The growing emphasis on precision engineering, automation, and quality control boosts the need for advanced measurement technologies. Domestic competitiveness and global influence of the market are also bolstered by government support for innovation and the growing adoption of smart factories.

Metrology Equipment Market Dynamics:

Drivers:

-

Rising Automation in Manufacturing Drives Demand for High-Precision Metrology Solutions Across Multiple Industrial Sectors

The rising automation proficiency in the manufacturing sector is primarily driving the metrology equipment market growth. With the growing initiative of Industry 4.0 in factories, manufacturers need measurement solutions that are real-time, precise, and consistent. Metrology equipment serves many automation functions, such as precise alignment, defect detection, part validation, and others. The automotive, electronics, and even aerospace sectors, in particular, need a great deal of advanced tool operation that can be easily integrated with the robotic systems. This is leading manufacturers to a new era of smart production lines where contactless metrology systems and inline, are increasingly in demand. The connectivity of the automation with quality control is a key driver changing the landscape of the market in multiple regions.

“In June 2024, the new multi-sensor measuring system from KEYENCE is intended to improve quality inspection in metrology thanks to its high-speed, high-precision measurements with fully automatic part recognition and minimal operator interaction.”

-

Growing Demand for Eco-Friendly Products in Various Industries Boosts the Adoption of Sustainable Metrology Solutions

Metrology equipment market trends are being shaped by sustainability goals across industries. Businesses are moving more toward eco-friendly production, such as reusable materials and energy-saving machinery. Such climate action fosters metrology systems that have the potential to minimize material use through measurement and optimized processes. Not only do modern instruments use less power and offer remote diagnostics, which helps minimize their environmental footprint. Such environmentally sustainable technologies are taking top priority as many manufacturing firms aim to meet regulations and the expectations of individual consumers. This trend of green innovation is forcing metrology suppliers to develop solutions that adhere to the circular economy model and enable sustainable industrial development.

Restraints:

-

High Initial Investment and Integration Cost Restrict Market Access for Small and Medium-Sized Manufacturers Globally

The escalating demand for precision measurement technologies globally continues to pose a major challenge for metrology equipment companies, due to the cost of advanced equipment. These sophisticated metrology systems can require millions of dollars in investment, highly trained operators, and be extremely time-consuming when trying to integrate into an existing manufacturing flow. Small and medium-sized enterprises (SME) are facing these financial and technical hurdles that slow or stop adoption. Moreover, operational expenses also come from continuous maintenance, calibration, and software upgrades. This has resulted in a two-fold phenomenon including a large number of smaller manufacturers have relied on outsourced services, or have delayed modernisation efforts, which in turn has restricted the ease of wider scalability of these tools in price-sensitive markets.

Metrology Equipment Market Segmentation Analysis:

By Type

In the metrology equipment market, the coordinate measuring machine (CMM) segment generated the highest revenue share of about 32.16% in 2024 and is expected to sustain its dominance over the forecast period due to early adoption for dimensional accuracy and geometric tolerancing in various industries. As they can measure almost any part, CMMS is a vital part of quality control processes, especially within the automotive and aerospace sectors, where such complex components need to be inspected. Due to their high accuracy/precision and ability to be automated, they remain a mainstay of Companies despite the ever-increasing competition in recent years from new optical technologies.

The optical digitizer and scanner (ODS) segment is expected to grow at the highest rate, with a CAGR of about 6.83% over 2025–2032, due to the significant demand for fast, contactless, and high-resolution inspection solutions. Such systems are mainly preferred in electronics and the consumer sector, as delicate and complicated components cannot be measured with contact. According to metrology equipment market analysis, a transition from time-consuming to quick and flexible inspection is being observed, which has led to increased uptake of ODS systems as an integral part of supporting real-time inspection and digitization in a smart manufacturing (SM) environment.

By End-Use

In 2024, the automotive segment accounted for the highest revenue share in the metrology equipment market, which is expected to experience high demand, owing to the rising requirement for high precision dimensional validation and surface finish inspection during vehicle manufacturing. Assembly lines are subject to stringent safety, quality, and regulatory standards requiring manufacturers to rely heavily on precision measurement instruments. Automated systems of metrology provide higher throughput, lesser rework, and improved quality of product, further enhancing the dominance of this segment in the industrial metrology equipment market, due to continued investments of OEMs and Tier 1 suppliers in advanced inspection technologies.

The electronics segment is expected to experience the highest growth rate of 23.8% over 2025–2032 since electronic components are critical and are becoming smaller in size, facility, and design, leading to a complex internal structure and requiring ultra-high-precision inspection tools. There is a broad and rapid increase in the need for non-destructive measurement systems that can work at the micro and nano levels. With these advancements in the global metrology equipment market, the evolution and development of electronics have led to the adoption of high-resolution optical systems and 3D scanning technologies that are capable of detecting defects in real-time, enabling targeted and timely solutions for the production of small and high-performance devices for consumer electronics, PCB manufacturing, and semiconductors.

Metrology Equipment Market Regional Outlook:

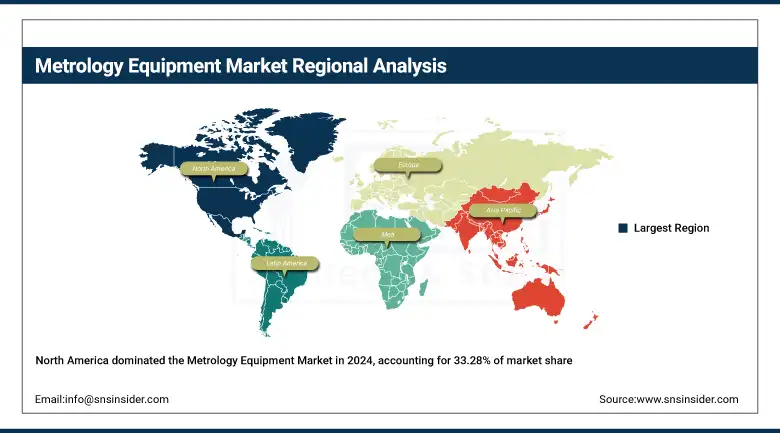

The North American region accounted for the highest revenue share of 33.28% in the metrology equipment market. The region enjoys early adopter advantages of automation and Industry 4.0 technologies and large investments in R&D from prominent Metrology Equipment Companies. Furthermore, the stringent quality control standards and regulatory compliance in the U.S. verticals propel the adoption of premium grade metrology solutions, thus backing the North America metrology market leadership in the global business landscape.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia-Pacific will grow at a steady CAGR of around 7.35% over 2025-2032 due to rapid industrialization, growth in automotive production, and an increase in consumer electronics manufacturing. Nations, such as China, Japan, South Korea, and India are pouring huge funds into smart factories and quality assurance technology. With high-growth economic regions having local and global manufacturers shifting their focus to expand their businesses, the Asia Pacific region is the fastest-growing region of the global metrology equipment market. The most common growth factors promoting the growth of this industry include an increase in demand for Precision Measurement Instruments in these high-growth economies.

Non-contact and automatic measurement technologies anticipate the growth of the European metrology equipment market. Germany tops the region, benefiting from the strength of its automotive and precision engineering sectors. For instance, the latest innovations comprise real-time inspection 3D scanning systems powered by AI. With stringent quality standards in place, the region continues to remain a hub for demand for precision metrology solutions.

Key Players in the Metrology Equipment Market are:

The major players operating in the market are Hexagon AB, Nikon Metrology NV (Nikon Corporation), ZEISS, KEYENCE CORPORATION, KLA Corporation, Mitutoyo America Corporation, Jenoptik, Renishaw plc, CREAFORM, and Metro.

Recent Developments:

-

February 2025 - ZEISS unveils cutting-edge metrology innovations at Live Tech Reveal 2025 in the U.S. and Canada, showcasing advanced AI-driven inspection systems and digital quality solutions for next-generation industrial applications.

-

October 2024 - Creaform launched enhanced HandySCAN 3D|MAX Series with improved accuracy, resolution, and speed, advancing large-part metrology for aerospace, automotive, and heavy industries, strengthening its position in the global metrology equipment market.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 10.58 Billion |

| Market Size by 2032 | USD 16.99 Billion |

| CAGR | CAGR of 6.15% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Coordinate Measuring Machine (CMM), Optical Digitizer and Scanner (ODS), X-ray and Computed Tomography (CT) Systems, Measuring Instruments, Form Measurement Equipment, Others) • By End Use (Manufacturing, Automotive, Aerospace, Electronics, Medical, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Hexagon AB, Nikon Metrology NV (Nikon Corporation), ZEISS, KEYENCE CORPORATION, KLA Corporation, Mitutoyo America Corporation, Jenoptik, Renishaw plc, CREAFORM, Metro |

Frequently Asked Questions

Ans: North America dominated the metrology equipment market in 2024.

Ans: The Coordinate Measuring Machine (CMM) segment dominated the metrology equipment market.

Ans: The major growth factor of the metrology equipment market is the increasing demand for precision measurement in advanced manufacturing and quality control across industries like automotive, aerospace, and electronics.

Ans: The metrology equipment market size was USD 10.58 billion in 2024 and is expected to reach USD 16.99 billion by 2032.

Ans: The metrology equipment market is expected to grow at a CAGR of 6.15% from 2024-2032.

Get in Touch