Military Software Market Report Scope & Overview:

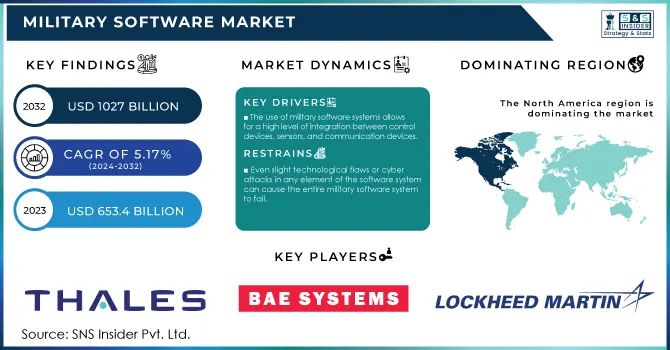

The Military Software Market Size was valued at USD 653.4 billion in 2023 and is projected to reach 1027 billion by the end of 2032, with a growing CAGR of 5.17% during the forecast period 2024-2032. Defense forces from throughout the world use varied software into weapons and other systems used on land, marine, aerial, and space platforms. The use of software in systems based on these platforms has allowed for the development of more efficient military systems that are less susceptible to human error. It has also resulted in higher synergy and improved battle system performance while requiring less maintenance. These military software applications include cybersecurity, logistics and transportation, target recognition, and battlefield healthcare. The use of military software systems allows for a high level of integration between control devices, sensors, and communication devices. This is a primary driving force in the market for military software systems.

To get more information on Military Software Market - Request Free Sample Report

Furthermore, developing technologies such as the Internet of Things and artificial intelligence, as well as its incorporation into military software systems, have enabled battlefield communication considerably faster and clearer than ever before. A slight technological glitch or a cyber-attack in any element of the software system might lead to the downfall of the entire Military software systems industry is the key constraint factor.

Military Software Market Dynamics

KEY DRIVERS

-

The use of military software systems allows for a high level of integration between control devices, sensors, and communication devices.

-

Emerging technologies such as the Internet of Things and artificial intelligence, as well as its incorporation into military software systems, have improved combat communication faster and clearer than ever before.

RESTRAINTS

-

Even slight technological flaws or cyber-attacks in any element of the software system can cause the entire military software system to fail.

OPPORTUNITIES

-

The market's constant need for novel items in all services creates a strong potential for profit.

THE IMPACT OF COVID-19

The COVID-19 epidemic has had a significant impact on the global market for military software.

The COVID-19 epidemic delayed economic growth in practically all major countries, causing changes in consumer purchasing habits.

National and international travel have been hampered as a result of the lockdown applied in many nations, which has greatly disrupted the supply chain of numerous sectors around the world, consequently increasing the supply-demand gap.

As a result, a lack of raw material supply is likely to slow the manufacturing pace of military software, severely impacting market growth.

However, the situation is expected to improve as governments around the world begin to reduce regulations for resuming corporate operations.

Raytheon has created a virtual software factory to help speed up the creation of military software and aid in the development of counter-threat capabilities for the armed forces. The software factory is made up of actual coding areas, Cloud-based tools, and software professionals. It will strive to give new capabilities to the military as rapidly as possible.

The virtual software factory was created in response to military commanders' calls for a shift in how software is generated, similar to how the consumer technology industry does it. The factory will enable the corporation to use modern software development approaches such as Agile and DevOps across all of its applications.

Air force, army, and navy are the main segments for application. The sector army will drive the market's expansion at the fastest rate. The new battleground necessitates flawless and unambiguous communication. The army sector uses ground-based communications to relay vital information, allowing army units to stay informed about the state of the conflict.

The US army is already planning to deploy cutting-edge software to improve communication. As military equipment becomes more advanced, the nay segment is likely to contribute to market expansion during the forecast period. During the forecast period, the section air force will expand significantly. The US Air Force has also created a new GPS signal that army leaders would find extremely useful. Military Software Industry Trends tend to accelerate market expansion.

Military Software Market Regional Analysis

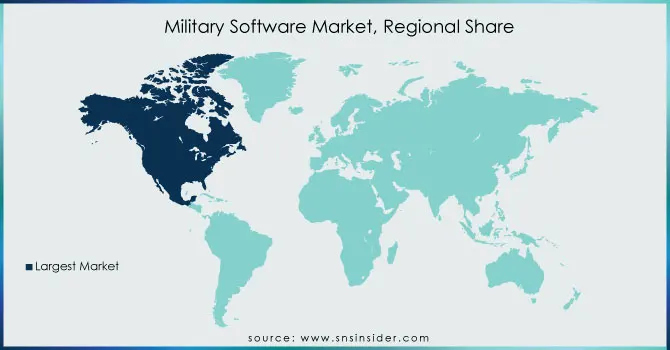

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa account for the majority of the military software market. North America has high-end main players, and technological innovation drives market expansion; as a result, it will control the military software market in 2023.

Because many military software suppliers are present in Europe, the military software market will rise. The continual terrorist attacks in China and India are driving market growth, which is expanding the Asia Pacific region's growth. It also increases military spending, which stimulates the expansion of the regional market.

Many significant firms are located in the Middle East and Asia, and as they invest in the military software business, the region's growth accelerates. The Brazilian army's requirement for increased border surveillance to defend the region will boost Latin American market growth. Military Software Market Forecast indicates that every region will have an impact on the market's growth.

Need any customization research on Military Software Market - Enquiry Now

KEY PLAYERS

The Key Players are Thales Group, IBM, Bae System, Soartech, Charles Corporation, Lockheed Martin, Raytheon Company, Northrop Grumman, General Dynamics, Nvidia & Other Players.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 653.4 Billion |

| Market Size by 2032 | US$ 1027 Billion |

| CAGR | CAGR of 5.17% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Learning & Intelligence, Advanced Computing, and AI Systems) • By Application (Information Processing and Cyber Security) • By Type (Command and Control, Military Messaging, Electronic Warfare) • By End Use (Army, Navy, Air Force) • By Platform (Land-based, air-based, naval) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thales Group, IBM, Bae System, Soartech, Charles Corporation, Lockheed Martin, Raytheon Company, Northrop Grumman, General Dynamics, Nvidia |

| DRIVERS | • The use of military software systems allows for a high level of integration between control devices, sensors, and communication devices. • Emerging technologies such as the Internet of Things and artificial intelligence, as well as its incorporation into military software systems, have improved combat communication faster and clearer than ever before. |

| RESTRAINTS | • Even slight technological flaws or cyber-attacks in any element of the software system can cause the entire military software system to fail. |

Get in Touch