Mini PCs Market Report Scope & Overview:

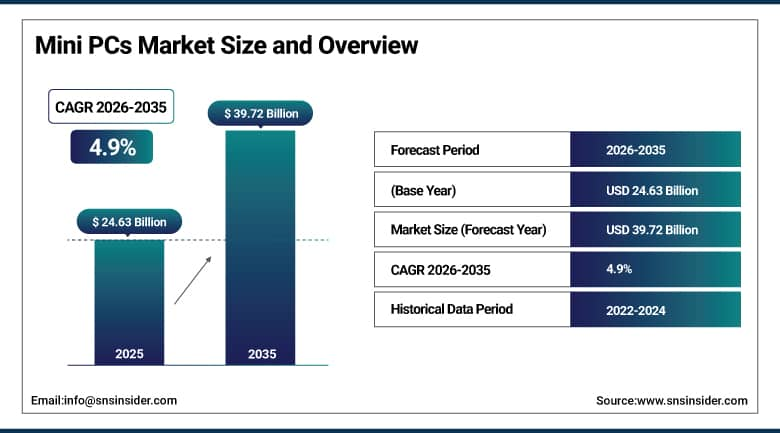

The Mini PCs Market was valued at USD 24.63 billion in 2025 and is expected to reach USD 39.72 billion by 2035, growing at a CAGR of 4.9% from 2026–2035.

The Mini PCs Market is seeing a paradigm shift propelled by the increasing worldwide demand for miniaturized, energy-efficient, and high-performing computing capabilities for an array of applications across various industries. Mini PCs, which are essentially small form factor computers that serve the same purpose as the standard tower desktop, have come a long way from being a product category limited to specific consumer use-cases to becoming advanced computing tools used in educational, healthcare, retail, corporate, digital signage, and automation settings. The capability of such devices to offer desktop-like computer processing within a small physical size while using much lesser energy than conventional tower desktops renders them ideal for space-limited and environmentally conscious deployment scenarios. Remote and hybrid working trends, ongoing digital transformation in enterprises and government agencies, along with breakthrough advances in processor design and manufacturing by Intel with its Core Ultra AI processors and AMD with its Ryzen series processors, has expanded the performance capabilities of mini PCs to match mainstream workstations.

Moreover, industry data consistently confirms that mini PCs are gaining significant adoption as a mainstream computing platform in edge computing deployments, IoT gateway applications, and AI-at-the-edge scenarios - where their compact size, low power consumption, and increasingly powerful integrated processing capabilities make them a compelling alternative to larger, more power-hungry computing architectures.

Mini PCs Market Size and Forecast

-

Market Size in 2025: USD 24.63 Billion

-

Market Size by 2035: USD 39.72 Billion

-

CAGR: 4.9% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Mini PCs Market - Request Free Sample Report

Mini PCs Market Trends

-

Increasing use of AI-enabled processors (Intel Core Ultra and AMD Ryzen AI) facilitating on-board AI inference for advanced generation mini PCs.

-

Convergence towards increased deployment of mini PCs in digital signage, kiosk, and interactive display setups due to their lower costs and 4K/8K content management support.

-

Increasing use of mini PCs as edge computing devices for IoT systems, smart manufacturing, and retail automation solutions.

-

Increasing prevalence of Wi-Fi 6E, Thunderbolt 4/5, and USB4 technologies for greater utility of mini PCs for professional multi-display and peripheral-intensive workflows.

-

Popularizing the use of power-efficient, low TDP mini PC platforms by enterprise IT departments in pursuit of sustainability goals within corporate data centers and offices.

-

Increased presence of mini PCs in the educational sector thanks to e-learning initiatives and government-funded program for subsidized computer device procurement.

-

Popularizing the use of mini gaming and media mini PCs, powered by dedicated GPUs, for home use and capture market share from traditional gaming desktops and media PCs.

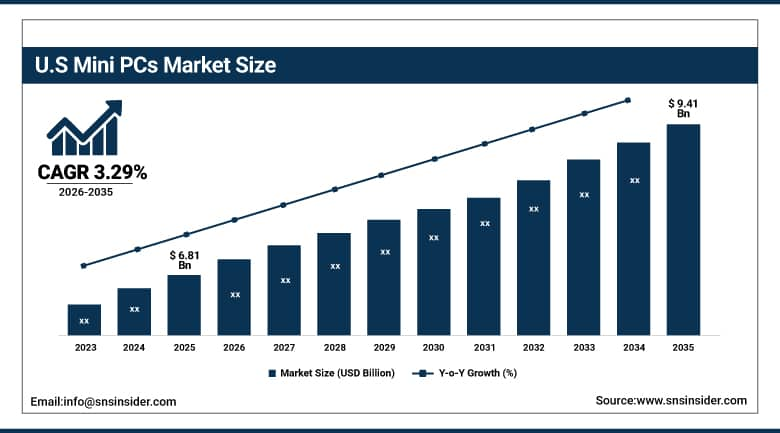

U.S. Mini PCs Market Size Outlook:

The U.S. was valued at USD 6.81 billion in 2025 and is expected to reach USD 9.41 billion by 2035, registering a CAGR of 3.29% during 2026–2035.

US is the dominant national market for Mini PCs around the globe, owing to its superior IT framework, extensive enterprise adoption of technology, and the existence of key players in the field such as Intel, HP Inc., Dell Technologies, and Apple. The continued growth in hybrid working models and the rapid replacement cycle of IT assets within organizations, facilitated by the shift from large legacy desktops to mini PCs, are the core drivers of demand. Enterprise IT teams have increasingly adopted mini PC solutions due to their low total cost of ownership, ease of implementation and management, and less power consumption than conventional tower desktop computers.

The educational sector in the US has become an important and expanding market vertical for mini-PCs, as district-wide technology initiatives utilize the devices for classroom and administration operations. Similarly, healthcare organizations have begun to leverage mini-PCs extensively for point-of-care workstations, radiology image viewing, and accessing electronic health records systems - all of which take advantage of the smaller form factor and consistent uptime offered by the platform.

Mini PCs Market Segment Insights

-

Based on Application, Home Entertainment accounted for the largest market share (~40%) in 2025; Digital Signage expected to be the fastest-growing segment with a CAGR of 6.05%.

-

Based on Industry Verticals, Consumer Electronics accounted for the largest market share (~34%) in 2025; Education segment expected to be the fastest-growing vertical (CAGR) driven by global ed-tech digitization.

-

Based on Component, Memory accounted for the largest revenue share in 2025; Processor segment expected to be the fastest-growing component (CAGR of 6.67%) driven by AI processor integration.

By Application, Home Entertainment segment dominates the Mini PCs Market, Digital Signage segment expected to grow fastest

The Home Entertainment category was dominant in the market for Mini PCs in 2025, taking up about 40 percent of the total sales value. Today, mini PCs have become the most sought-after devices to use as home entertainment media centers and living-room computing systems, replacing large set-top boxes, outmoded gaming devices, and tower computers with sleek machines that support 4K streaming, video playback on the local hard drive, gaming, and office-related functions. Products including Apple Mac Mini M4, the Intel NUC series successor models, and the ASUS Mini PC PN Series are some of the devices gaining immense popularity due to their performance, which is equivalent to or higher than the one offered by MacBook at a size that can fit into a person's palm.

The Digital Signage segment is projected to register the highest CAGR of 6.05% from 2026 to 2035. Mini PCs are rapidly becoming the preferred computing backbone for digital signage systems across airports, retail environments, hospitality venues, corporate lobbies, and transit hubs - replacing older, purpose-built signage players with general-purpose mini PC platforms that offer greater flexibility, remote management capability, and support for high-resolution and multi-screen content. HP Inc.'s Elite Slice and Dell's OptiPlex Micro are prominent examples of mini PC platforms specifically marketed for digital signage applications. As global digital-out-of-home (DOOH) advertising investments continue to scale and smart retail technologies proliferate, demand for mini PC-powered signage infrastructure is expected to grow substantially.

By Industry Verticals, Consumer Electronics segment dominates the Mini PCs Market, Education segment expected to grow fastest

The Consumer Electronics Vertical was the leading industry vertical in terms of the Mini PCs’ market share in 2025, accounting for about 34% of the total market revenues. The increased interest among consumers toward computing devices that integrate entertainment, gaming, and productivity functionalities within one efficient space has been driving consumer electronics demands towards mini PCs. Prominent brands such as Lenovo (ThinkCentre Neo Ultra, IdeaCentre Mini), ASUS (Mini PC PN Series), and Apple (Mac Mini) continue to expand their product lines through innovation and introduction of new artificial intelligence-powered mini PCs along with increased memory and better thermals, which helps the brands capture more consumer market shares.

Education vertical is anticipated to have the highest CAGR between 2026 and 2035 among all industry verticals. Digitization efforts backed by government intervention in the K-12 and higher education sectors, such as one-to-one computer initiatives in developing countries and IT upgrades in developed nations, will see a surge in demand for mini PCs in the education sector. Features like low energy consumption, robustness, ease of centralized management through MDM software, and affordable unit prices make mini PCs ideal candidates for educational deployment in large numbers.

By Component, Memory segment holds largest share in the Mini PCs Market, Processor segment expected to grow fastest

In 2025, the Memory category had the highest revenue share in the Mini PCs components market. Since end-users of mini PCs seek devices with multitasking abilities, capable of running intensive productivity applications, and enabling smooth content creation experiences, there is a gradual trend towards increased RAM offerings, where 16GB and 32GB DDR5 versions are increasingly commonplace on mid to premium range mini PCs. Upgrade cycles fueled by operating system upgrades and artificial intelligence application compatibility have also contributed to sustaining high demand for high capacity/high bandwidth memory.

The Processor segment is expected to record the fastest CAGR of 6.67% from 2026 to 2035, powered by the integration of AI-capable processors from Intel (Core Ultra Meteor Lake/Lunar Lake), AMD (Ryzen AI series), and Apple (M-series silicon) into successive generations of mini PC platforms. These next-generation processors incorporate dedicated neural processing units (NPUs) that enable on-device AI inferencing for tasks including real-time language processing, content generation, image recognition, and predictive analytics - dramatically expanding the functional capabilities of compact mini PC platforms. The processor innovation cycle is compressing performance gaps between mini PCs and full-size workstations, making the platform increasingly viable for professional-grade computing, software development, and creative applications.

Mini PCs Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~84% |

|

Europe |

Germany |

~28% |

|

Asia Pacific |

China |

~48% |

|

Middle East & Africa |

UAE |

~34% |

|

Latin America |

Brazil |

~51% |

North America Mini PCs Market Insights

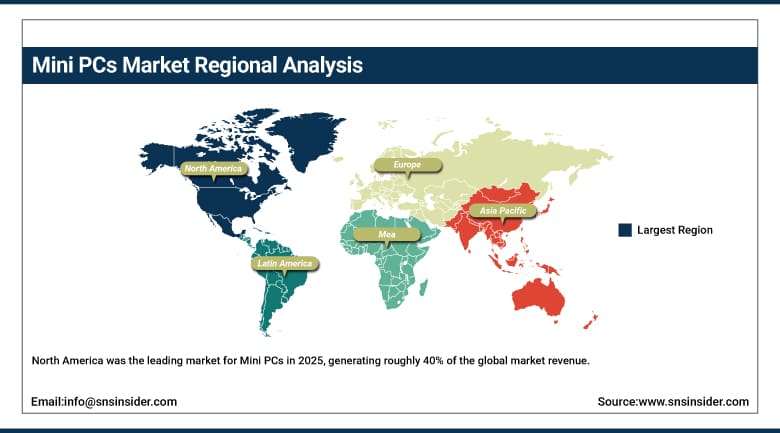

North America was the leading market for Mini PCs in 2025, generating roughly 40% of the global market revenue. The U.S. holds the distinction of being the biggest market among all countries in North America, aided by advanced enterprise technology adoption, robust information technology purchasing infrastructure, and the presence of global mini PC technology vendors such as Intel Corporation, HP Inc., Dell Technologies, and Apple. The major drivers behind the growth of demand in this region include an increase in hybrid working and distance learning trends, shorter enterprise IT refresh cycles, and increased use of mini PCs in the healthcare, retail, and digital signage sectors.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Mini PCs Market Insights

The Asia Pacific region is one of the fastest growing regional markets in terms of Mini PC demand, where growth is estimated at 6.66% during 2026 to 2035. The ongoing process of digitization in countries such as China, India, Japan, South Korea, and Southeast Asia has led to high-level growth in the demand for compact computer devices in sectors such as education, retail, business organizations, and industrial automation processes. Demand in the region is dominated by China, where leading regional manufacturers such as Hasee Computer and Lenovo dominate, along with a new wave of local manufacturers specializing in making cost-effective mini PCs.

Europe Mini PCs Market Insights

The Europe region had a considerable presence in the Mini PCs market during 2025, with Germany, the United Kingdom, and France being the top-performing countries in the regional market. The market demands are driven by robust institutional and business purchases due to IT upgrades and sustainability initiatives that promote efficient computing technologies. Data protection laws in Europe, including GDPR, are making companies inclined towards mini PC systems rather than cloud computing technologies due to their capability to process sensitive information within the company premises. Elitegroup Computer Systems (ECS), Acer, and Lenovo are some of the leading brands present across the Europe region.

Middle East & Africa and Latin America Mini PCs Market Insights

The mini PC market in Middle East & Africa and that of Latin America is at a relatively nascent stage but shows promising growth owing to factors like increasing digitalization, higher corporate IT spend, and growing demand for cost-effective computing in educational and public sectors. The UAE and Saudi Arabia are the key demand generators for the mini PC market in Middle East & Africa on the back of smart city technologies and government-led initiatives for digitization. The Brazilian market leads in Latin America because of high consumer electronics demand, increasing technology usage in retail, and deployment of digital signage.

Mini PCs Market Growth Drivers:

-

Increasing demand for space-efficient, high-performance computing devices across enterprise, education, and consumer segments

The main factor driving the growth of the Mini PCs industry is the continuous and expanding requirement for computing devices that can achieve high efficiency with minimum size, lower power usage, and low maintenance costs. The trend of utilizing mini PCs is growing within enterprises as part of the IT modernization and sustainability strategies by adopting mini PCs as an alternative to outdated desktop computers with reduced office energy usage up to 70% from normal desktops while maintaining their comparable or even higher processing efficiencies. In educational sectors, the trend of implementing technological advancements includes installing computing stations in classrooms based on mini PC systems.

Industry procurement data consistently confirms that mini PCs are gaining meaningful share in enterprise IT refresh cycles - a trend expected to accelerate as AI-capable mini PC platforms from Intel, AMD, and Apple deliver increasingly compelling performance-per-watt advantages over both traditional desktop towers and comparable notebook-class systems. The lower total cost of ownership, reduced IT management overhead via MDM integration, and extended product lifecycle of mini PCs are reinforcing enterprise purchasing decisions.

Mini PCs Market Restraints

-

Limited upgradability and thermal constraints relative to traditional desktop platforms restraining adoption in high-performance workloads

One of the key limitations of the Mini PCs market can be seen in the compromise of form factor and hardware scalability in the majority of mini PC offerings. In contrast to conventional desktop systems such as mid-towers and full towers, which provide users with an opportunity to replace their graphics cards, install more storage drives, and install expansion cards into the PCIe slots, most mini PC systems come with a very restrictive architecture which does not offer much flexibility in terms of hardware upgrades after purchase. This makes mini PCs less attractive to power users and professionals who may require GPU-accelerated computing for their work in areas such as 3D rendering, machine learning training, and CAD/CAM modeling.

Mini PCs Market Opportunities

-

Expanding opportunities in AI-at-the-edge, IoT gateway applications, and next-generation AI PC deployments

The convergence of mini PC hardware with AI processor capabilities and edge computing architectures represents one of the most compelling long-term growth opportunities for the market through 2035. As enterprises deploy distributed AI inference workloads closer to data sources - in factory floors, retail environments, hospitals, and smart city infrastructure - mini PCs equipped with dedicated NPUs and AI-accelerated SoCs are emerging as ideal edge computing nodes that balance processing capability, power efficiency, and deployment flexibility. The AI PC transition - driven by Microsoft's Copilot+ PC initiative and analogous AI integration programs from Apple, Intel, and AMD - is expected to drive a significant multi-year upgrade cycle as organizations and consumers migrate to AI-capable mini PC platforms. Additionally, the growing deployment of mini PCs as IoT gateway controllers, autonomous retail kiosk management systems, and digital health monitoring nodes in clinical environments is broadening the addressable market well beyond traditional computing use cases.

Recent Developments:

-

2026: Mini PC manufacturers accelerated the launch of Copilot+-certified AI PC platforms featuring Intel Lunar Lake and AMD Ryzen AI 300 series processors with on-device NPU capabilities. Apple expanded its Mac Mini lineup with an enhanced M4 Pro configuration targeting professional workstation users, while ASUS launched Arm-based mini PC platforms optimized for edge computing and IoT gateway deployments.

-

2025 (October): Lenovo introduced the ThinkCentre Neo Ultra Mini - a compact commercial mini PC powered by Intel Core Ultra processors with Intel vPro manageability technology - targeting enterprise IT deployments requiring centralized management, hardware-level security, and AI-accelerated productivity capabilities in a space-efficient form factor.

-

2025 (March): Apple launched an updated Mac Mini featuring M4 and M4 Pro chip configurations, delivering up to 3x CPU performance improvement over the previous M2 generation. The refreshed Mac Mini introduced Thunderbolt 5 connectivity and 16GB base memory configuration, significantly strengthening the platform's appeal for creative professionals, software developers, and AI/ML workload scenarios.

Mini PCs Market Key Players

-

Apple Inc.

-

Intel Corporation

-

HP Inc.

-

Dell Technologies Inc.

-

Lenovo Group Limited

-

ASUSTeK Computer Inc.

-

Acer Inc.

-

ASRock Inc.

-

Hasee Computer

-

Elitegroup Computer Systems (ECS)

-

MINISFORUM

-

GEEKOM

-

Beelink

-

Zotac Technology

-

MSI

Mini PCs Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 24.63 Billion |

| Market Size by 2035 | USD 39.72 Billion |

| CAGR | CAGR of 4.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Home Entertainment, Digital Signage, Others) • By Industry Verticals (Consumer Electronics, Retail, Manufacturing, Education, Others) • By Component (Processor, Memory, Storage, GPU, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Apple Inc., Intel Corporation, HP Inc., Dell Technologies Inc., Lenovo Group Limited, ASUSTeK Computer Inc., Acer Inc., ASRock Inc., Hasee Computer, Elitegroup, Computer Systems (ECS), MINISFORUM, GEEKOM, Beelink, Zotac Technology |

Frequently Asked Questions

The Mini PCs Market is expected to grow at a CAGR of 4.9% from 2026 to 2035.

The Mini PCs Market was valued at USD 24.63 billion in 2025.

The increasing global demand for space-efficient, high-performance, and energy-efficient computing devices across enterprise, education, healthcare, retail, and digital signage applications - amplified by the rise of hybrid work, digital transformation programs, and AI PC platform transitions.

The Home Entertainment segment dominated the Mini PCs Market in 2025, accounting for approximately 40% of total market revenue.

North America dominated the Mini PCs Market in 2025, holding approximately 40% of global market share, led by the United States - underpinned by mature IT infrastructure, high enterprise adoption rates, and the presence of leading mini PC technology companies.

Get in Touch