Mobile Artificial Intelligence Market Report Scope & Overview:

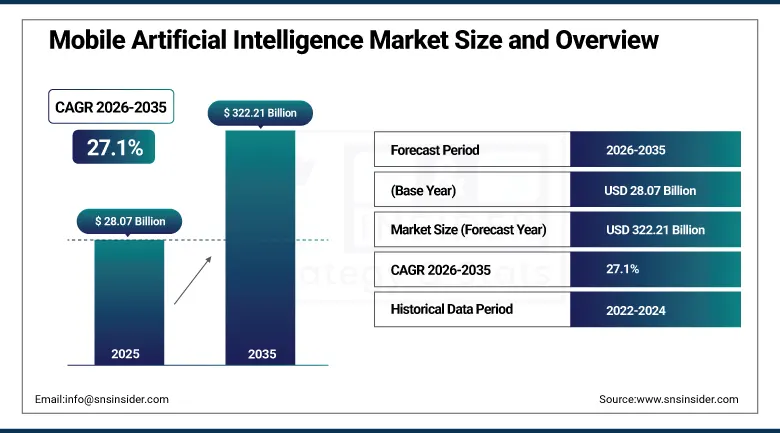

The Mobile Artificial Intelligence Market was valued at USD 28.07 Billion in 2025 and is expected to reach USD 322.21 Billion by 2035, growing at a CAGR of 27.1% from 2026 to 2035.

The Mobile Artificial Intelligence Market is expected to witness rapid growth on account of the adoption of AI-based smartphones, increasing need for customized user experience, and advancements in edge computing. The use of virtual assistants, image recognition, and predictive analysis in consumer devices and enterprise sectors is adding to the demand. The developments in machine learning and deep learning algorithms and the application of AI in mobile chipsets have enhanced the efficiency of processes and reduced the latency period. Increasing investments by major technology firms in AI-equipped mobile ecosystems are playing a vital role in driving the growth of the market.

According to Qualcomm Incorporated, its Snapdragon platforms power over 3 billion devices globally, with dedicated AI engines (Hexagon processors) enabling efficient on-device inference for imaging, voice processing, and predictive applications. Furthermore, the International Data Corporation (IDC) reports that AI-enabled smartphones are expected to account for more than 70% of global smartphone shipments by 2027, driven by the rapid integration of generative AI features and advancements in edge AI processing capabilities.

Market Size and Forecast

-

Market Size in 2026E: USD 35.67 Billion

-

Market Size by 2035: USD 322.21 Billion

-

CAGR: 27.1% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Mobile Artificial Intelligence Market - Request Free Sample Report

Mobile Artificial Intelligence Market Trends

-

Rising integration of AI-powered features in smartphones such as virtual assistants, image recognition, and real-time language translation driving market growth

-

Growing adoption of edge AI and on-device processing enabling faster performance, lower latency, and enhanced data privacy in mobile applications

-

Increasing use of AI in mobile photography, gaming, and augmented reality (AR) applications improving user experience and device capabilities

-

Expanding deployment of AI-enabled chipsets and neural processing units (NPUs) by semiconductor manufacturers enhancing computational efficiency in mobile devices

-

Continuous advancements in machine learning and deep learning algorithms supporting personalized user experiences, predictive analytics, and intelligent automation on mobile platforms

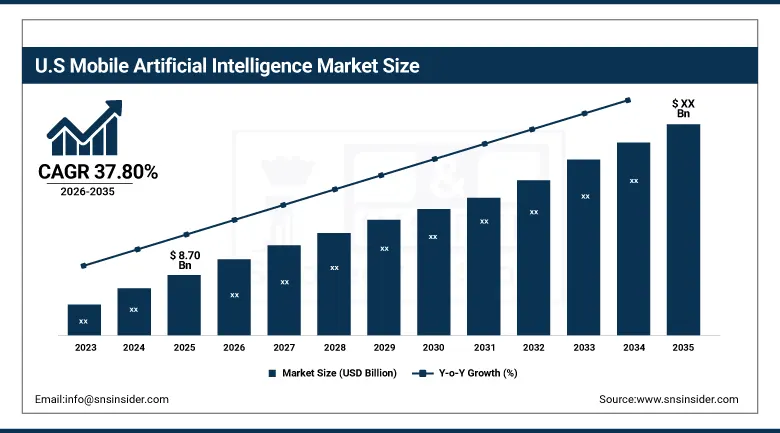

The U.S. Mobile Artificial Intelligence Market Outlook

The U.S. Mobile Artificial Intelligence Market was valued at approximately USD 8.70 Billion in 2025 and is expected to grow substantially through 2035 at a CAGR of approximately 37.80%.

The United States remains the global leader in mobile artificial intelligence owing to the presence of top technology companies in addition to high consumer penetration of advanced mobile devices which collectively support continuous innovation in mobile AI chipsets, applications, and platforms. Mobile artificial intelligence is revolutionizing several sectors from health care, retail to entertainment, automotive, and many others, and with rising demands for intelligent mobile solutions in conjunction with fast 5G and edge computing penetration, the U.S. mobile AI market will continue to grow through the forecast period.

In 2025, Apple continued advancing its proprietary Neural Engine architecture across its A-series and M-series chip families, enhancing on-device machine learning performance for features spanning Face ID authentication, computational photography, and natural language processing within its expanding device ecosystem.

Mobile Artificial Intelligence Market Segment Analysis

-

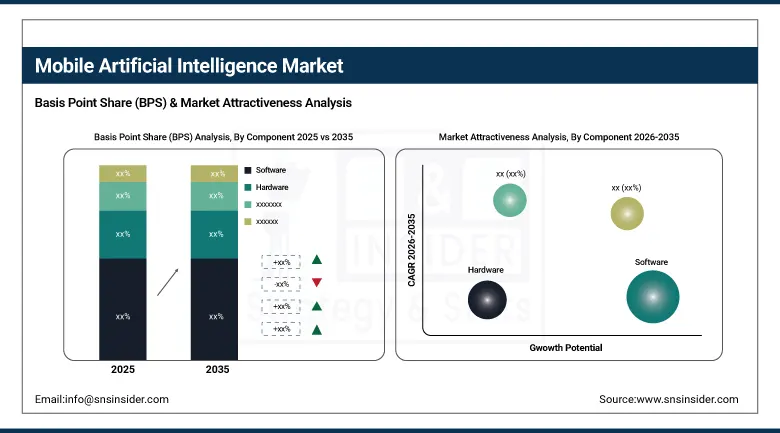

By Component, software segment dominated the Mobile Artificial Intelligence Market in 2025 with 60% share; services segment is the fastest growing segment.

-

By Technology, machine learning segment dominated the market in 2025 with 57% share; deep learning segment is the fastest growing segment.

-

By Application, virtual assistants segment dominated the market in 2025 with 38% share; predictive analytics segment is the fastest growing segment.

-

By End-User, consumer electronics segment dominated the market in 2025 with 42% share; healthcare segment is the fastest growing segment.

By Component, Software segment dominates the Mobile Artificial Intelligence Market, Services segment expected to grow fastest

The software segment dominated the Mobile Artificial Intelligence Market owing to its importance in enabling various artificial intelligence functions on mobile devices, including voice recognition, image processing, and predictive analysis. Increasing usage of AI-powered applications on mobile devices has been one of the major growth drivers for this market segment. Constant innovations in AI algorithms, cloud integration, and edge computing have made this segment even more crucial for intelligent mobile experiences.

The services segment is the fastest growing in the Mobile Artificial Intelligence Market owing to the increasing need for AI implementation, integration, and maintenance services in the mobile industry. Companies are turning to third-party assistance for AI model deployment, performance optimization, and management of data-driven applications. The increasing demand for AI consulting services, cloud AI services, and managed services is driving the rapid growth in the market.

By Technology, Machine Learning segment dominates the Mobile Artificial Intelligence Market, Deep Learning segment expected to grow fastest

The machine learning segment dominated the Mobile Artificial Intelligence Market owing to the importance of machine learning as an underlying technology for various AI-based mobile apps such as recommendation engines, voice assistants, and predictive typing. Its capacity to handle large volumes of data and learn from it makes this segment crucial for providing intelligence in mobile devices. Its popularity in the field of consumer electronics along with constant improvements in algorithms and on-device computing capability have strengthened the leading position of this segment in mobile AI technologies.

The deep learning segment is the fastest growing in the Mobile Artificial Intelligence Market as a result of higher effectiveness in performing complex tasks, including image recognition, natural language processing, and real-time analytics. With growing computing power of mobile devices and advances in architecture of neural networks, more use cases can be deployed. Growing need for highly accurate AI-powered applications in healthcare, automotive, and consumer electronics industries is fueling this trend.

By Application, Virtual Assistants segment dominates the Mobile Artificial Intelligence Market, Predictive Analytics segment expected to grow fastest

The virtual assistants segment dominated the Mobile Artificial Intelligence Market due to extensive usage of AI-based virtual assistants for performing tasks such as issuing commands using voices, searches, and automations in smart phones and devices. The capacity of providing enhanced user experience and real-time assistance is behind their mass adoption. The consistent development in natural language processing techniques and incorporation into mobile operating systems has made them as the most critical application of mobile AI.

The predictive analytics segment is the fastest growing in the Mobile Artificial Intelligence Market due to growing requirement for making decisions based on data analysis and personalized user experiences. Mobile applications are increasingly using predictive analysis tools for predicting the behavior of users and enhancing their performance. Increased usage in applications related to healthcare, finance, and retail applications along with developments in AI technology has contributed to their growth.

By End-User, Consumer Electronics segment dominates the Mobile Artificial Intelligence Market, Healthcare segment expected to grow fastest

The consumer electronics segment dominated the Mobile Artificial Intelligence Market owing to high use of AI-powered smartphones, tablets, smart speakers, and wearables. The increased consumer preference for intelligent applications like voice recognition, facial recognition, and recommendation engines has led to the adoption of the technology. In addition, constant innovations from device makers and the proliferation of smart devices have contributed to the dominance of the consumer electronics sector as the major end-user for mobile AI solutions.

The healthcare segment is the fastest growing in the Mobile Artificial Intelligence Market because of the increased use of mobile apps incorporating artificial intelligence technology in diagnostic activities, monitoring services, and patient care management. The increasing demand for personalized health care solutions, telemedicine, and health monitoring services is propelling the adoption of AI technology in the industry.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Mobile Artificial Intelligence Market Insights

North America Mobile Artificial Intelligence Market growth driven by strong AI R&D investments, technological advancements, and widespread adoption of AI-powered mobile devices across the region's technology-sophisticated consumer base. The presence of major AI chipset manufacturers including Qualcomm, Nvidia, Intel, and Apple has accelerated on-device AI development, boosting demand for AI-driven smartphones, wearables, and IoT applications, while the region's advanced 5G infrastructure has fuelled AI adoption in mobile applications enabling low-latency AI computing for AR/VR, gaming, and smart assistant applications.

The United States accounts for approximately 82.47% of regional revenue through its concentration of leading AI software development organisations including Google and Microsoft, whose continuous innovation in AI-powered applications sustains North America's commercial and technological leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Mobile Artificial Intelligence Market Insights

Europe held a significant share of global Mobile Artificial Intelligence revenues, with Germany expected to register particularly high growth rates within the European market driven by the country's strong automotive electronics and manufacturing sectors whose AI integration requirements span both consumer mobile devices and industrial AI applications. Germany accounts for approximately 28.47% of European revenues through its concentration of automotive manufacturing whose AI-enabled mobile and embedded systems applications create substantial regional demand, while stringent European regulations on data privacy and growing emphasis on AI ethics are influencing market dynamics across the broader European mobile AI ecosystem whose development increasingly emphasises privacy-preserving on-device processing architectures.

According to Eurostat, over 75% of individuals in the European Union use smartphones daily, creating a strong consumer base for mobile AI-powered applications such as virtual assistants, real-time translation tools, and predictive services.

Additionally, the European Commission supports AI development through its Digital Europe Programme, which allocates more than €7.5 billion toward strengthening AI, cloud computing, and edge infrastructure capabilities. These initiatives are fostering a favorable ecosystem for AI innovation, accelerating deployment of intelligent mobile applications and enhancing overall market growth across the region.

Asia Pacific Mobile Artificial Intelligence Market Insights

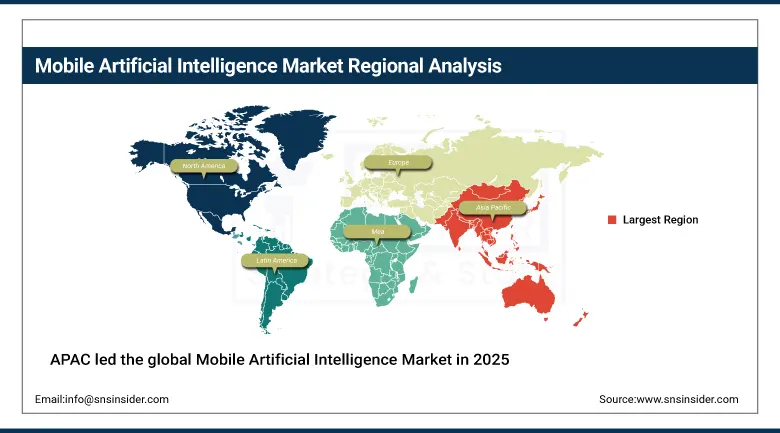

APAC led the global Mobile Artificial Intelligence Market in 2025, accounting for an estimated 40% share of total revenue. This dominance was driven by rapid smartphone penetration, strong semiconductor manufacturing capabilities, and widespread adoption of AI-enabled mobile applications across industries. Expanding investments in 5G infrastructure, edge AI processing, and digital ecosystems further strengthened regional leadership. Additionally, the presence of major consumer electronics manufacturers and growing demand for intelligent mobile services supported sustained market expansion throughout the year.

China accounts for approximately 38.47% of Asia Pacific revenues through its massive domestic smartphone market and growing semiconductor manufacturing capability, while smartphone usage incorporating AI processors is expected to continue increasing across China, Japan, India, and South Korea throughout the forecast period.

China’s Ministry of Industry and Information Technology reports that the country has shipped over 1 billion mobile phones annually in recent years, creating a vast installed base that significantly supports large-scale deployment and adoption of mobile AI applications.

MEA & Latin America Mobile Artificial Intelligence Market Insights

Middle East and Latin America are growing Mobile Artificial Intelligence markets where expanding smartphone penetration, growing 5G infrastructure investment, and increasing AI application adoption are creating increasing commercial demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its position as a regional technology hub whose advanced telecommunications infrastructure and high smartphone adoption rates create sophisticated mobile AI application demand. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large smartphone consumer base, growing technology sector investment, and increasing adoption of AI-powered mobile applications across both consumer and enterprise contexts.

Drivers: Advancing AI chipsets and rapid mobile AI app growth drive market expansion.

Unprecedented rates of growth of the mobile artificial intelligence market are achieved due to the convergence of semiconductor technology of chipsets that feature fast development at the level of increasingly fine nodes providing exponential improvement of AI performance per watt of energy used and the emergence of a wide array of new applications utilizing AI in mobile devices, whose requirements for computing power continuously grow the addressable market for mobile AI chips.

Mobile devices become increasingly equipped with facial recognition capabilities, voice assistants, augmented reality and other applications requiring continuous growth of chipsets and software demand that depends on each new level of AI technology embedded into smartphones by manufacturers. Moreover, the connection of 5G networks to edge AI computing opens the way to applications that were previously not viable due to limitations of older network technologies.

Restraints: Power constraints and privacy regulations limit deployment of mobile AI features.

Power consumption continues to be one of the main technical challenges for the implementation of advanced AI computations within mobile devices, due to the finite power supply and thermal management capability available, which pose an engineering challenge between advanced AI computations versus sustainable power usage that needs to be constantly managed by engineers through semiconductor manufacturing innovation and AI optimization.

The increasing amount of regulation regarding data protection in most of the major economies like the GDPR in Europe and many states in the USA results in difficulties in designing compliant and efficient mobile AI systems, which often process sensitive personal information such as biometric information, location information and behavioral patterns.

Opportunities: Generative AI and cross-industry adoption create major new commercial opportunities.

The implementation of generative AI capabilities right inside the mobile devices to be able to carry out large language models processes for personal assistants, content creation, and real-time translation without cloud connectivity requirements is a game-changing development in terms of product line expansion that is revolutionizing smartphone manufacturer competition strategy and consumer choices. The growing adoption of mobile AI technology in automotive electronics, medical diagnostic tools, and industrial robotics, leveraging the advancements already made in semiconductors and software development for smartphone usage, is a major growth opportunity whose potential addressable market goes far beyond conventional mobile device categories.

Recent Developments:

-

2025: Apple continued advancing its proprietary Neural Engine architecture across A-series and M-series chip families, enhancing on-device machine learning performance for Face ID, computational photography, and natural language processing within its expanding device ecosystem.

-

2024: Multiple leading semiconductor manufacturers including Qualcomm and MediaTek expanded their 7nm and finer fabrication AI chipset portfolios, delivering enhanced on-device generative AI capability for flagship and progressively mainstream smartphone tiers.

-

2023: Qualcomm Technologies announced the Snapdragon 7+ Gen 2 Mobile Platform, providing premium AI-enhanced experiences including advanced computational photography and high-speed connectivity capability for the expanding mid-tier premium smartphone segment.

Mobile Artificial Intelligence Market Key Players:

-

Apple Inc.

-

Google LLC

-

Samsung Electronics

-

Qualcomm Incorporated

-

Intel Corporation

-

Microsoft Corporation

-

Huawei Technologies Co., Ltd.

-

MediaTek Inc.

-

Amazon.com Inc.

-

IBM Corporation

-

Sony Group Corporation

-

Baidu Inc.

-

Alibaba Group Holding Limited

-

Advanced Micro Devices (AMD)

-

Arm Holdings

-

Synopsys Inc.

-

Samsung SDS

-

Lenovo Group Limited

Mobile Artificial Intelligence Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.07 Billion |

| Market Size by 2035 | USD 322.21 Billion |

| CAGR | CAGR of 27.1% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (RFID, GPS, Sensors) • By Product (Smart Collar, Smart Camera, Smart Harness and Vest, Others) • By Animal Type (Dogs, Cats, Other Animals) • By Application (Identification & Tracking, Behavior Monitoring & Control, Facilitation, Safety & Security, Medical Diagnosis & Treatment) • By Sales Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Apple Inc., Google LLC, Samsung Electronics, Qualcomm Incorporated, NVIDIA Corporation, Intel Corporation, Microsoft Corporation, Huawei Technologies Co., Ltd., MediaTek Inc., Amazon.com Inc., IBM Corporation, Sony Group Corporation, Baidu Inc., Alibaba Group Holding Limited, Tencent Holdings Ltd., Advanced Micro Devices (AMD), Arm Holdings, Synopsys Inc., Samsung SDS, Lenovo Group Limited |

Frequently Asked Questions

Advancing AI chips, 5G edge computing, generative AI apps, AR/VR growth, and federated learning drive mobile artificial intelligence market growth.

The Mobile Artificial Intelligence Market was valued at USD 28.07 Billion in 2025.

The Mobile Artificial Intelligence Market is expected to grow at a CAGR of 27.1% from 2026 to 2035.

The software segment dominated the Mobile Artificial Intelligence Market.

Asia Pacific dominated the Mobile Artificial Intelligence Market in 2025.

Get in Touch