Motor Lamination Market Report Scope & Overview:

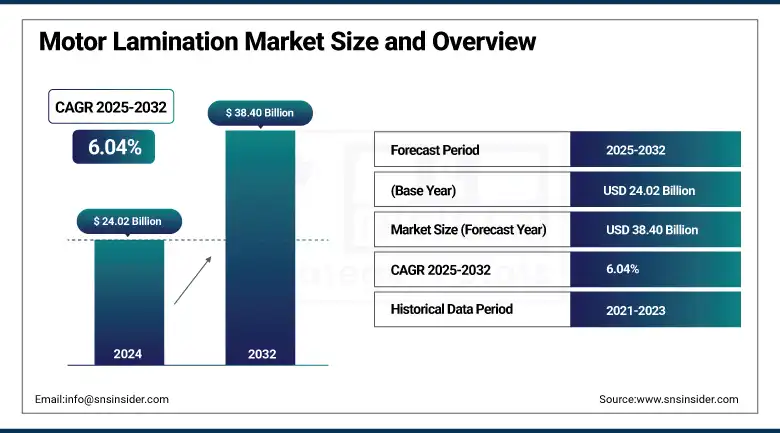

The motor lamination market size was valued at USD 24.02 billion in 2024 and is expected to reach USD 38.40 billion by 2032, growing at a CAGR of 6.04% over the forecast period of 2025-2032.

Motor lamination material market growth is driven by increasing demand for energy-efficient electric motors in various sectors such as electric vehicles, industrial automation, and renewable energy. Advanced materials, such as silicon steel, amorphous alloys, and Nanocrystalline compositions, improve magnetic properties and minimize core losses. The high-speed motors that are being accomplished using state-of-the-art lamination technology bring the capability of reaching as high as 100,000 rpm using commercial electric motor lamination technology. With developments in the manufacturing processes for electrical steels, such as laser cutting, precision stamping, and additive manufacturing, this can be complicated, and optimized cross-sections of electrical steel lamination can be made. The use of smarter technologies, such as the integration of IoT-enabled sensors, enhances real-time monitoring and predictive maintenance and, thus, increases reliability and efficiency amongst operations.

To Get more information On Motor Lamination Market - Request Free Sample Report

Another trend is towards sustainability, where manufacturers are using sustainable materials and processes to reduce their environmental footprint. These features lead to significant energy savings, with over 2,100 GWh per year in energy savings from improved lamination materials for the industrial sector and around 9,700 GWh in non-industrial applications, helping to create a more energy-efficient design. In the electric vehicle market, the increase in demand for compact, lightweight motors also raises the importance of new bonding methods and materials.

For Instance, EuroGroup Laminations, an Italian electric motor parts manufacturer, has formed a strategic partnership with China’s Hixih Rubber Industry Group to boost their presence in the Chinese electric vehicle market. They plan to set up a joint venture controlled by EuroGroup, including a new R&D center and a high-tech factory in Shandong province. This facility will focus on producing motor cores specifically for New Energy Vehicles, strengthening their foothold among local EV makers.

Motor Lamination Market Dynamics

Drivers

-

The global shift to electric mobility is fueling rapid growth in the motor lamination market as demand for efficient electric motors surges.

The ongoing global shift towards electric mobility is positively impacting the growth of the motor lamination market trends. The high performance and range potential of electric vehicles (EVs) stem from the efficiency characteristics of their electric motors. Motor laminations are key elements to minimizing energy losses, for example, eddy currents in the motor, and therefore improving efficiency and dependability. As the adoption of EVs spreads across the world, so does the urgent need for high-performance, high-grade laminations. Asia-Pacific is the pioneer of this transition, where nations like China and India are implementing the highest sales and infrastructure for EVs. By encouraging cleaner transportation and as emission regulations strengthen, electric motor demand will rise, and with it demand for motor laminations, influencing the trends of the motor lamination market in the upcoming years.

For Instance, Chinese automaker BYD sold more than 4.27 million vehicles, a large share of which were electric. The company is expected to reach 5.5 million vehicle sales in 2025. To support the rising adoption of electric vehicles, China is also enhancing its EV infrastructure by expanding the network of charging stations across the country.

Restraint

-

High Manufacturing Costs Hinder SME Competitiveness and Innovation in the Motor Lamination Market

The motor lamination market is restrained by its high manufacturing costs. Motor lamination production requires critical and really sophisticated technologies, electric steel properties, stamping, bonding and insulation. Typically, such high-level advanced manufacturing systems have high labour and maintenance initial costs that many SMEs find difficult to manage it. Additionally, the requirement of close tolerances, and customized designs in the motors are additional factors that add on to production complications and costs. Higher costs of labor and energy also add to the cost structure. Consequently, it deters many smaller manufacturers from competing so they are hindered in terms of scaling, expansion and future investment in innovation. Such cost barrier can eventually slow market growth and innovation penetration.

For instance, a stacked stator lamination welding machine can cost about USD 30,000, while stamping and notching machines may reach USD 50,000. These high upfront costs create financial pressure, especially for small and medium-sized manufacturers, limiting their ability to scale or adopt new technologies.

Motor Lamination Market Segmentation Outlook

By Technology

The stamping segment dominated the market and accounted for 42% of the motor lamination market share. Such a dominance can be attributed to the fact that stamping is the most efficient, inexpensive, and most extensively used production process in motor manufacturing. To minimize the energy losses and improve the performance of the motor, thin metal sheets need to be precisely shaped after stamping into the required lamination stacks. That reproducibility ensures high-quality lamination with great scale, which is why it's the go-to for manufacturers where high reliability and efficiency are needed. Finally, the well-developed infrastructure and long-established supply chains supporting stamping technology further solidify its dominant position in the market.

The Bonding segment is recognized as the fastest growing, owing to higher electrical performance and minimal energy losses that the bonding methods provide. Bonding is another benefit because it has stronger mechanical reliability and electrical insulation properties compared to conventional wire bonding, which makes it particularly appropriate for high-performance motor applications that require operational dependability and efficiency. Welding technology still resides in the market but is growing at a slower pace and has a lower market share than Stamping and Bonding as its advantages remain more limited and production remains more complex.

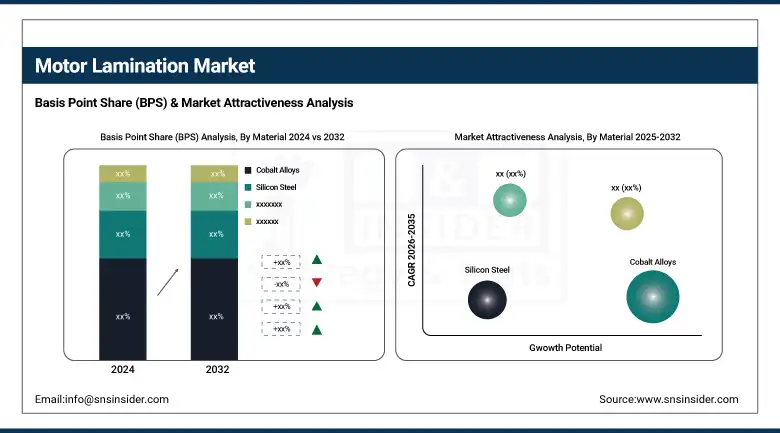

By Material

The motor lamination market is predominantly led by Cobalt Alloys, which hold a significant 38% market share in 2024. Cobalt's outstanding magnetic and corrosion-resistant properties contribute to this dominance, as does its ability to improve the efficiency and performance of motors. Due to these properties, cobalt alloys seem well-suited for use in high-performance electric motors, particularly in automotive and industrial applications where reliability and durability are of great importance. The rise of electric vehicles and other renewable energy solutions also drives the need for cobalt-based laminations. Cobalt alloys assist in decreasing the energy losses and better the life of the motor; therefore, these are favored among the manufacturers.

Cold-Rolled Lamination Steel is identified as the fastest-growing segment in the motor lamination market. It provides high strength, good surface finish, and dimensional accuracy, which makes it suitable for the quick manufacturing of the motor. The increase in demand for this segment results from the product's ability to minimize energy losses through higher conductivity magnetic flux, thus enhancing motor efficiency. Moreover, in automotive, industrial, and consumer electronics sectors, the increased share of electric motors with energy efficiency benefits has been forcing an increase in the demand for cold-rolled lamination steel.

By Application

The Electrical Stators/Rotors segment dominated the motor lamination market, capturing a significant 52% share in 2024. Stators and rotors have by far the most extensive applications in electric motors, which are used across a wide variety of industries, such as automotive, industrial machinery, and consumer electronics, resulting in this segment's dominance. These features are crucial for motor efficiency, performance, and lifespan, which increases the demand for quality motor laminations for this segment. Moreover, emerging automotive technologies such as electric vehicles and the increasing focus on energy-efficient motors additionally drive demand for high-performance stators and rotor laminations, in particular. The electrical stators/rotors segment remains one of the largest and most significant applications in the motor lamination market, especially as manufacturers strive to minimize energy loss and maximize motor reliability.

The transformers segment is the fastest-growing application in the motor lamination market owing to the demand for efficient and reliable power transmission and distribution systems globally. This is significant for the stability of the electrical grid and is a vital operation in the electrical grid, where transformers are employed to step voltage up and down for industry usage. Due to the increasing uptake of renewables, smart grids, and growth in electrical networks in developing areas, demand for better laminations for transformers has grown. These laminations offer reduction in core losses, preserving energy losses as well as in the vein of minimizing energy waste/ loss in energy per global goal. Furthermore, new designs and materials used for transformers are boosting this segment, thereby making it one of the key contributors to motor lamination market growth.

By End-Use

The Manufacturing segment dominated the motor lamination market, holding a substantial 54% market share in 2024. The high share of judgment is because of the wide adoption of motor laminations in many production purposes that require green & reliable electric principles. These laminations are widely used in manufacturing industries, which help to reduce energy losses, increase durability, and improve the performance of motors. This segment holds the leading position owing to the regular demand from end-use sectors, such as industrial machinery, automation, and heavy equipment.

The automotive segment is the fastest-growing in the motor lamination market due to the demand for electric vehicles (EVs) augmented by innovation in automotive technologies. In a drive to enhance energy efficiency and decrease emissions, automakers have turned to electric motors, which require high-quality motor laminations in quantities greater than ever. These lamination parts are essential parts for EV motors and hybrid vehicles, which can reduce energy loss, thus improving the working ability of motor properties. As well as government policies on cleaner transport technology and rising demand for e-cars and hybrid vehicles are also playing a role in pushing the growth in this sector.

Motor Lamination Market Regional Analysis

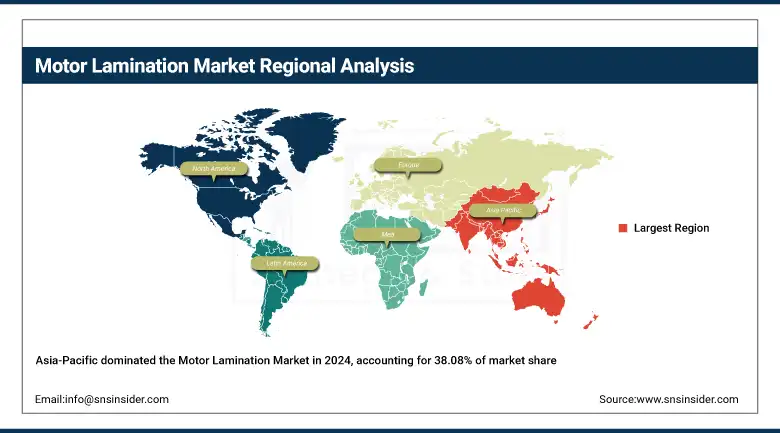

Asia-Pacific dominated the motor lamination market, holding a significant 38.08% share in 2024. Such leadership is powered by the fast growth of industry, the huge automotive market, and the growing need for electricity in the area. China, India, and Japan have a strong manufacturing base that supports the manufacture of motor laminations for automotive, industrial, and consumer applications. Moreover, various government programs supporting electrification and clean energy are also driving the growth of the market. Asia-Pacific is also the fastest-growing market, owing to its strong infrastructure and growing industrial activities. This growth can be attributed to the growing usage of electric motors in the automotive, industrial, and consumer sectors across the region. Asia-Pacific will continue to be at the forefront of market growth owing to an increase in demand, driven by strong government support concerning electrification projects, renewable energy projects, and an increase in industrial activity.

Get Customized Report as per Your Business Requirement - Enquiry Now

China is expected to grow notably due to the rapid expansion of the automotive and electrical machinery industries. China, the world's largest automotive market, is moving to electric vehicles, and that shifts demand for efficient motor laminations. Additionally, growing modernization of industrial as well as renewable energy propagation initiatives in the country fosters demand for advanced motor lamination technologies.

Europe holds a significant share of the motor lamination market, primarily driven by its well-established automotive and industrial sectors. With major automakers shifting to electric and hybrid vehicles, this region has a growing demand for quality motor laminations. The expanding industrial machinery and automation industries in Europe also provide demand for high-efficiency electric motors, bolstering market expansion. Market growth is also enabled by sustained research and development investments, strict environmental regulations that favor energy-efficient technologies, and government incentives for electrification. This combination of factors makes Europe a significant player in the global motor lamination market.

North America is experiencing steady growth in the motor lamination market, primarily driven by the increasing adoption of automotive electrification and advancements in the aerospace industry. Government incentives and tighter emission regulations are driving high-quality motor laminations demand for electric motors as the region is gaining a robust foothold in electric vehicles (EVs). Further, the ongoing technological advancements and lightweight yet efficient motor components in the aerospace sector are boosting market growth. Additionally, the increasing demand for industrial automation and investment in renewable energy projects are contributing to market growth. All in all, these aspects will guarantee constant growth and technological advancement in the North American motor lamination market.

Key Players in the Motor Lamination Market are

Motor Lamination Companies are Eurogroup S.P.A, Lake Air Companies, Lamination Specialties Incorporated, Partzsch Elektromotoren E.K., Pitti Laminations Ltd., Polaris Laser Laminations, LLC., R. Bourgeois, Tempel, Thomas Laminations, Hyundai Rotem Co.

Recent Development

-

In August 2024, EuroGroup Laminations S.p.A. formed a strategic alliance with China's Hixih Rubber Industry Group to create a joint venture dedicated to manufacturing motor cores for New Energy Vehicles in Shandong province.

-

In March 2024, Hyundai Rotem Co. introduced a state-of-the-art lamination press at its Dangjin facility specifically designed for electric vehicle motor cores. This advanced equipment significantly boosts the company's manufacturing capacity, enabling it to meet the growing demand for efficient and high-performance EV motors.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 24.02 Billion |

| Market Size by 2032 | USD 38.40 Billion |

| CAGR | CAGR of 6.04% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Welding, Bonding, Stamping) • By Material (Nickel Alloys, Cold-Rolled Lamination Steel, Cobalt Alloys, Silicon Steel) • By Application (Electrical Stators/Rotors, Magnetic Coils, Transformers) • By End Use (Automotive, Electronics, Manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Eurogroup S.P.A, Lake Air Companies, Lamination Specialties Incorporated, Partzsch Elektromotoren E.K., Pitti Laminations Ltd., Polaris Laser Laminations, LLC., R. Bourgeois, Tempel, Thomas Laminations, Hyundai Rotem Co. |

Frequently Asked Questions

The Asia-Pacific region dominated the Motor Lamination Market in 2024.

The “stamping” segment dominated the Motor Lamination Market.

The global shift to electric mobility is fueling rapid growth in the motor lamination market as demand for efficient electric motors surges.

The Motor Lamination Market was USD 24.02 billion in 2024 and is expected to reach USD 38.40 billion by 2032.

The Motor Lamination Market is expected to grow at a CAGR of 6.04% from 2025-2032.

Get in Touch