Air Separation Plant Market Report Scope & Overview:

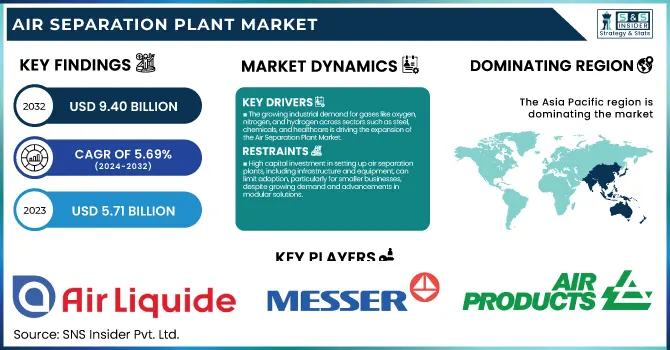

The Air Separation Plant Market Size was esteemed at USD 5.71 billion in 2023 and is supposed to arrive at USD 9.40 billion by 2032 with a growing CAGR of 5.69% over the forecast period 2024-2032.

This report offers a comprehensive analysis of production capacity, utilization rates, and maintenance metrics within the Air Separation Plant Market. It highlights technological adoption trends across different regions and examines the dynamics of global trade through export/import data. The report also looks into the impact of downtime on operational efficiency and cost management, providing a unique insight into market optimization. Trends show a growing focus on automation and energy-efficient solutions in the industry.

Air Separation Plant Market Size and Forecast

-

Market Size in 2023: USD 5.71 Billion

-

Market Size by 2032: USD 9.40 Billion

-

CAGR: 5.69% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2023

To Get more information on Air Separation Plant Market - Request Free Sample Report

Air Separation Plant Market Trends (with Statistics):

-

Rising demand for industrial gases in steel, chemicals, and healthcare is driving market growth, with global industrial gas consumption increasing at 6–8% annually.

-

Expansion of healthcare infrastructure and medical oxygen demand post-pandemic is supporting investments, with medical oxygen capacity rising by over 20% in developing regions.

-

Growing adoption of cryogenic air separation plants is strengthening large-scale production efficiency, accounting for more than 65% of total installed capacity globally.

-

Increasing investments in clean energy and hydrogen projects are boosting demand for high-purity oxygen and nitrogen, with hydrogen production capacity projected to grow at over 9% CAGR.

-

Emphasis on energy-efficient and modular air separation units (ASUs) is accelerating, reducing power consumption by 10–15% compared to conventional systems.

Air Separation Plant Market Dynamics

Drivers

-

The growing industrial demand for gases like oxygen, nitrogen, and hydrogen across sectors such as steel, chemicals, and healthcare is driving the expansion of the Air Separation Plant Market.

The growing industrial demand for gases such as oxygen, nitrogen, and hydrogen is a major driver of the Air Separation Plant Market. These gases are widely used in industries such as steel (for its properties), chemicals (for reactions), and healthcare (as medical treatments), with their applications including manufacturing, refining, and medical applications. Oxygen is needed in the steel industry to enhance combustion efficiency in blast furnaces, while nitrogen plays an important role in inerting and cooling applications. The growing demand for oxygen from the healthcare sector, especially after the pandemic, has also created demand. Moreover, moving beyond natural gas and towards clean energy technology such as hydrogen is witnessing significant traction in the transportation and energy generation industries, aiding the overall market growth. That growth is fueled by the demand for industrial gases because industrialization is quickly advancing in emerging economies. Market growth is also facilitated by trends like increased demand for sustainable energy solutions and advancements in air separation technologies that provide innovative and energy-efficient solutions for these industries.

Restraint

-

High capital investment in setting up air separation plants, including infrastructure and equipment, can limit adoption, particularly for smaller businesses, despite growing demand and advancements in modular solutions.

High capital investment is a significant restraint in the air separation plant market. As is common with production facilities, establishing such plants entails substantial capital expenditure, particularly for equipment like compressors, cryogenic units, and supporting infrastructure. Such high costs can be a barrier for smaller businesses or startups. Additionally, the expenditures are often associated with human resources and the continued upkeep that further increases operational costs. The market is expanding, however, due to the increasing rate of industrialization, the need for industrial gases, and technological advancements in air separation processes. As new market industries develop and require more efficient and sustainable solutions, suppliers are turning to innovations to help reduce costs and improve efficiency. Air separation trends are the growth of modular and compact air separation plants, providing more affordable air separation plant options for smaller more decentralized production that enables cross-industry adoption.

Opportunities

-

Small-scale and modular air separation systems offer flexible, cost-effective, and scalable solutions, driving growth in decentralized industrial operations and energy-efficient applications.

Small-scale and modular air separation systems are gaining traction in the Air Separation Plant market due to their flexibility and cost-effectiveness. As industries move more and more towards decentralized operations, these are a good way to avoid large-scale plants. They can be customized for smaller applications to help minimize capital outlay and operating costs but with high efficiency. Additionally, with the increasing emphasis on sustainability and energy efficiency, modular systems are in high demand, as they enable better resource utilization while reducing energy usage. Also, they are very scalable as their capacity can be expanded on demand without any kind of major infrastructure changes. Emerging markets are the leaders in this trend, as cost-effective and adaptable solutions are essential to their industrial growth. As air separation technology continues to advance, the market is expected to see a rise in innovation in modular systems that will make them even more energy-efficient and cost-effective, hence driving their adoption at a greater pace.

Challenges

-

Technological integration in air separation plants involves costly and complex upgrades to improve efficiency, with growing adoption driven by sustainability trends and energy demands.

Technological integration in air separation plants involves incorporating advanced, more efficient technologies into existing systems. While some of these upgrades can pay dividends in terms of improved plant performance, energy efficiency, and output, the task can prove difficult and costly. However, implementation of these newer technologies (membrane separation, pressure swing adsorption (PSA), and vacuum swing adsorption (VSA)) would need a significant investment in infrastructure, skilled labor, and a considerable amount of time for the optimization of these systems. Furthermore, retrofitting existing plants with cutting-edge technologies can be difficult as compatibility issues, operational interruptions, and the need for specialized equipment can pose obstacles. This complexity and high upfront cost can prevent a lot of operators from implementing these innovations in the short term. However, as energy efficiency becomes a greater priority in the context of sustainability goals, there is a clear and palpable movement toward adopting new technologies. But gradually, these innovations will incur significant growth in the market as they enhance cost-effectiveness by reducing operational expenses and the environmental footprint of air separation plants.

Air Separation Plant Market Segmentation Analysis

By Process

The Cryogenic segment dominated with a market share of over 65% in 2023. This process employs very low temperatures to fractionate air into its constituent gases, including nitrogen, oxygen, and argon, making it highly effective for bulk manufacture. The proven reliability and effectiveness of gas chromatography methods will ensure their continued widespread adoption, particularly in industries that require example high-purity gases for chemical, petrochemical, and energy processes. Cryogenic air separation plants are the preferred choice for large volumes and consistent gas purity for many critical industrial applications. Technological advancements coupled with consistent demand from the industrial sectors are anticipated to aid this dominance over the projected timeframe.

By Gas

The Nitrogen segment dominated with a market share of over 38% in 2023, due to its extensive use across various industries. Nitrogen is an important ingredient in many chemical productions, where it forms an inert atmosphere to prevent unwanted reactions. As a gas, nitrogen is often used in the food and beverage industry for food preservation and packaging, keeping foods fresh longer and extending shelf life. Moreover, manufacturing semiconductors and a controlled atmosphere in processes like soldering in electronics manufacturing are also some of the applications of nitrogen. The nitrogen segment is the largest and is the most widely used product segment in air separation plants, owing to the consistent demand for nitrogen from these industries during production as well as safety processes.

By End-Use

The Iron & Steel segment dominated with a market share of over 34% in 2023, due to its substantial demand for industrial gases like oxygen, nitrogen, and argon. In the production of steel, for example, these gases are of significant importance in such processes as blast furnace operation, electric arc furnaces, and steel refining. Oxygen is critical for burning and boosting the efficiency of steelmaking, while nitrogen is used to purge and generate inert environments. Due to the large amount of these gases used in the process of iron and steel production, this industry has become the largest consumer of products from air separation plants. Moreover, the increase in infrastructure and construction also drives the steel demand and leads to the continuing domination of the Iron & Steel category in the market.

Air Separation Plant Market Regional Outlook

Asia-Pacific region dominated with a market share of over 42% in 2023, because of rapid industrialization, especially in China, India, and Japan. Oxygen, nitrogen, and hydrogen are among the industrial gases that are in heavy demand in the region, driven by its growing manufacturing, steel production, and chemical sectors. Moreover, the increasing emphasis on healthcare, particularly in the wake of the pandemic, has also contributed to rising demand for the product in hospitals and medical centers thereby bolstering the market position. The region's overwhelming market share can be attributed to the rise of major infrastructure projects and burgeoning investments in the energy and steel production sectors. Furthermore, government initiatives to promote industrial growth along with policies to encourage their usage in countries such as China and India are further fueling the demand for advanced air separation technologies, allowing Asia-Pacific to maintain dominance in the market.

North America is the fastest-growing region in the Air Separation Plant Market, fueled by significant technological advancements and an increasing emphasis on energy efficiency. Demand for efficient and more sustainable air separation technologies is driven by the region’s strong industrial base (chemicals, healthcare, oil & gas). Furthermore, the increasing focus on hydrogen generation as a clean energy source is another primary driver influencing the market growth. The U.S. and Canada are placing large bets on their hydrogen infrastructure, which means there should be room for air separation plants that produce hydrogen by electrolysis and other methods. In addition, the use of advanced automation, IoT, and AI in the nutrition plants is increasing efficiency and minimising operational cost, which is expected to propel growth of the North America growth in the global market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Some of the major key players in the Air Separation Plant Market

-

Air Liquide S.A. (Oxygen, Nitrogen, Argon, Hydrogen)

-

Linde AG (Oxygen, Nitrogen, Argon, Carbon Dioxide)

-

Messer Group GmbH (Oxygen, Nitrogen, Argon, Hydrogen)

-

Air Products and Chemicals, Inc. (Oxygen, Nitrogen, Argon, Hydrogen, Helium)

-

E Taiyo Nippon Sanso Corporation (Oxygen, Nitrogen, Argon, Carbon Dioxide)

-

Praxair, Inc. (Oxygen, Nitrogen, Argon, Hydrogen)

-

Oxyplants (Oxygen, Nitrogen, Argon)

-

AMCS Corporation (Oxygen, Nitrogen, Argon, Hydrogen)

-

Enerflex Ltd (Oxygen, Nitrogen, Hydrogen, Helium)

-

Technex Ltd. (Oxygen, Nitrogen, Argon)

-

Atlas Copco (Nitrogen Generators, Oxygen Generators)

-

Airgas Inc. (Oxygen, Nitrogen, Argon, Helium)

-

Inox Air Products (Oxygen, Nitrogen, Argon, Hydrogen)

-

Southern Ionics (Oxygen, Nitrogen, Argon)

-

Worley (Oxygen, Nitrogen, Hydrogen, Helium)

-

Tianjin Tianhai (Oxygen, Nitrogen)

-

Cryogenic Equipment Manufacturing Company (Oxygen, Nitrogen, Argon)

-

Messer Group (Oxygen, Nitrogen, Argon, Hydrogen)

-

Gulf Cryo (Oxygen, Nitrogen, Argon, Hydrogen)

-

China National Petroleum Corporation (CNPC) (Oxygen, Nitrogen, Hydrogen)

Suppliers for (large-scale gas production and delivery systems, including innovative cryogenic technology) on Air Separation Plant Market

-

Air Liquide S.A.

-

Linde AG

-

Messer Group GmbH

-

Air Products and Chemicals, Inc.

-

E Taiyo Nippon Sanso Corporation

-

Praxair, Inc.

-

Oxyplants

-

AMCS Corporation

-

Enerflex Ltd

-

Technex Ltd.

Recent Development

In May 2023: Air Products and Chemicals Inc. entered into an investment agreement with the Government of the Republic of Uzbekistan and Uzbekneftegaz JSC to acquire, own, and manage an industrial gas complex.

In January 2024: EuroChem completed the construction of an air separation unit at Nevinnomysskiy. The unit, featuring over 1,000 tons of major process equipment delivered to Nevinnomysskiy Azot, produces gaseous oxygen, nitrogen, liquid oxygen, nitrogen, and argon, improving operational efficiency while minimizing environmental impact.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 5.71 Billion |

| Market Size by 2032 | USD 9.40 Billion |

| CAGR | CAGR of 5.69% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Process (Cryogenic, Non-cryogenic) • By Gas (Nitrogen, Oxygen, Argon, Others) • By End-use (Iron & Steel, Oil & Gas, Chemical, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Air Liquide S.A., Linde AG, Messer Group GmbH, Air Products and Chemicals, Inc., E Taiyo Nippon Sanso Corporation, Praxair, Inc., Oxyplants, AMCS Corporation, Enerflex Ltd, Technex Ltd., Atlas Copco, Airgas Inc., Inox Air Products, Southern Ionics, Worley, Tianjin Tianhai, Cryogenic Equipment Manufacturing Company, Messer Group, Gulf Cryo, China National Petroleum Corporation (CNPC). |

Frequently Asked Questions

Asia-Pacific dominated the Air Separation Plant Market in 2023

The “Cryogenic” segment dominated the Air Separation Plant Market.

The growing industrial demand for gases like oxygen, nitrogen, and hydrogen across sectors such as steel, chemicals, and healthcare is driving the expansion of the Air Separation Plant Market.

The Air Separation Plant Market was USD 5.71 billion in 2023 and is expected to Reach USD 9.40 billion by 2032.

The Air Separation Plant Market is expected to grow at a CAGR of 5.69% during 2024-2032.

Get in Touch