MulteFire Market Report Scope & Overview:

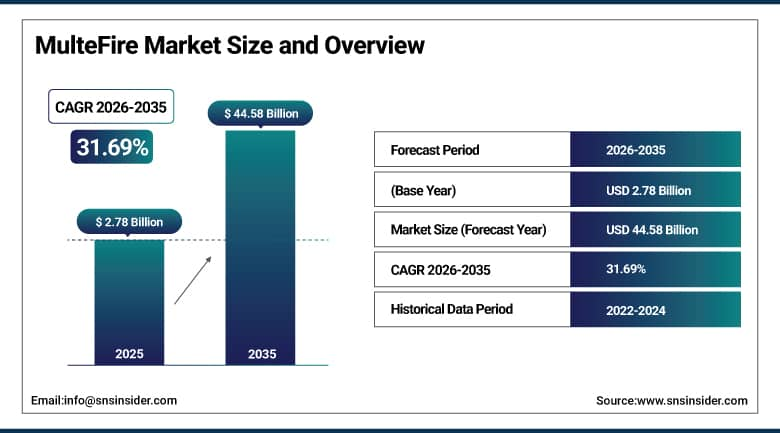

The MulteFire Market was valued at USD 2.78 Billion in 2025 and is expected to reach USD 44.58 Billion by 2035, growing at a CAGR of 31.69% from 2026 to 2035.

The global MulteFire market is experiencing exceptional and accelerating growth, driven by rising enterprise demand for private, secure, and high-reliability wireless connectivity that operates independently of public mobile network operators. The market is gaining strong momentum across manufacturing, logistics, energy, healthcare, and smart building sectors. Private LTE and MulteFire network deployments are replacing Wi-Fi in mission-critical industrial environments as businesses prioritize low-latency connectivity for industrial IoT automation, real-time machine monitoring, autonomous guided vehicle coordination, and seamless worker mobility. The MulteFire Alliance’s ecosystem development, spectrum regulatory improvements in CBRS-based shared spectrum in the U.S., and global expansion of unlicensed spectrum access are collectively creating the commercial and regulatory infrastructure.

In March 2024, Nokia launched its next-generation MulteFire small cell solution for industrial IoT applications, featuring enhanced interference management, improved spectral efficiency, and seamless integration with Nokia’s Digital Automation Cloud platform. The solution targets manufacturing plants, logistics hubs, and industrial campus environments whose critical automation workflows require LTE-grade connectivity reliability that conventional Wi-Fi cannot provide in dense machine and infrastructure environments.

Market Size and Forecast:

-

Market Size in 2026E: USD 3.66 Billion

-

Market Size by 2035: USD 44.58 Billion

-

CAGR: 31.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On MulteFire Market - Request Free Sample Report

MulteFire Market Trends:

-

CBRS-based private network deployments are accelerating MulteFire adoption across enterprise, industrial, and commercial environments.

-

AI-powered network management is improving interference mitigation, resource allocation, and overall MulteFire network performance.

-

Neutral host network models are gaining traction in airports, stadiums, campuses, and smart city projects.

-

Convergence with 5G NR-U is enabling migration from LTE-based MulteFire to advanced unlicensed 5G networks.

-

Expanding Industrial IoT device ecosystems are supporting broader deployment of MulteFire-enabled private wireless networks.

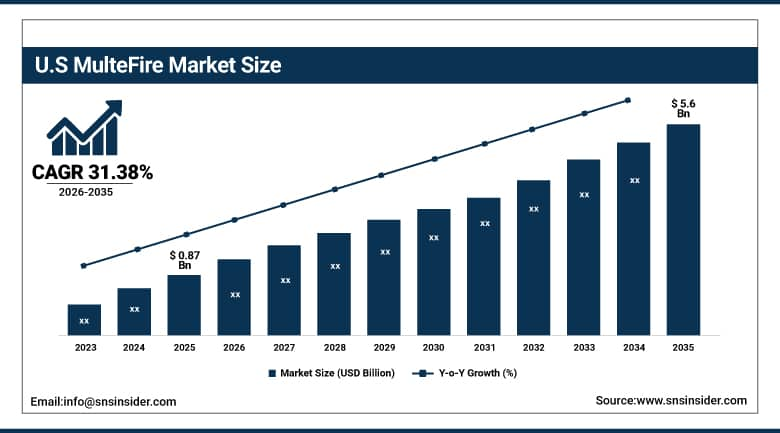

U.S. MulteFire Market Outlook:

The U.S. MulteFire Market was valued at approximately USD 0.87 Billion in 2025 and is expected to reach approximately USD 5.6 Billion by 2035, growing at a CAGR of approximately 31.38%.

The U.S. is the world’s most commercially significant MulteFire market, driven by the FCC’s Citizens Broadband Radio Service framework that provides a unique U.S.-specific shared spectrum access model enabling private LTE deployment without licensed spectrum, combined with rising demand for private LTE networks across manufacturing, logistics, healthcare, and enterprise IT networks. Qualcomm, Nokia, Ericsson, Cisco, CommScope, and Airspan Networks collectively define the domestic commercial landscape. Government support for smart manufacturing, semiconductor industry revitalization through the CHIPS Act creating new semiconductor fab private network requirements, and the extraordinary scale of U.S. enterprise IT modernization investment collectively sustain above-average domestic MulteFire market growth.

In 2024, Ericsson expanded its private network portfolio with enhanced CBRS-compatible solutions targeting U.S. industrial campus deployments, enabling enterprise customers to deploy private LTE networks in the 3.5 GHz CBRS band with enhanced quality of service guarantees, network slicing capability, and integration with enterprise IT infrastructure including ERP and manufacturing execution systems.

MulteFire Market Segment Analysis:

-

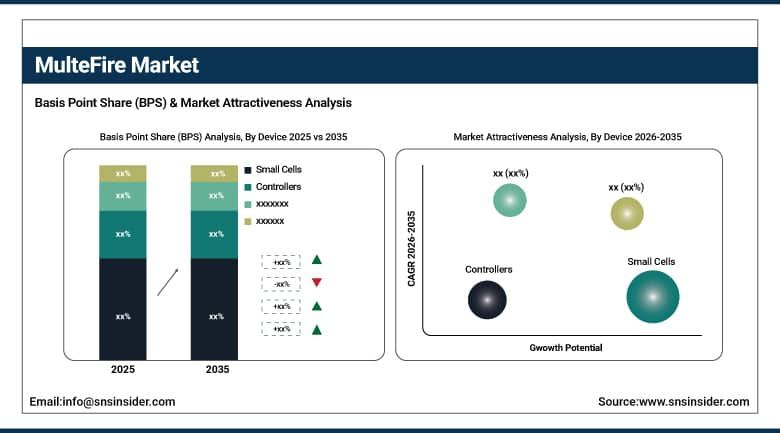

By Device, the small cells segment dominated the market with approximately 48% share in 2025, while the controllers segment is the fastest growing.

-

By Technology, the MulteFire 4g segment dominated the market with approximately 61% share in 2025, while the MulteFire 5g segment is the fastest growing.

-

By Deployment Mode, the private segment dominated the market with approximately 57% share in 2025, while the hybrid segment is the fastest growing.

-

By End User Vertical, the commercial & institutional buildings segment dominated the market with approximately 39% share in 2025, while the healthcare segment is the fastest growing.

By Device, small cells dominate, controllers grow fastest

Small cells retained the dominant device position with approximately 48% of the MulteFire market in 2025. The commercial primacy of small cells reflects their fundamental role as the radio access infrastructure on which MulteFire private network coverage depends, with each private network deployment requiring small cell installations that scale with coverage area and capacity requirements. The increasing adoption of MulteFire for private LTE networks across manufacturing, logistics, and enterprise sectors has directly driven small cell demand, with each new industrial private network deployment creating small cell hardware procurement proportional to facility scale.

Controllers are the fastest growing device segment because the growing complexity of multi-site enterprise private network management, the security orchestration requirements of industrial IoT networks, and the demand for AI-integrated analytics that provide intelligent network performance optimization collectively create above-average controller procurement growth. Each enterprise private MulteFire network whose scale exceeds a single-building deployment creates controller procurement whose commercial value grows with network complexity. The commercialization of cloud-native network controllers that enable central management of distributed MulteFire deployments across multiple factory or campus locations creates a premium controller product category whose advanced analytics and orchestration capability sustains pricing above commodity small cell hardware alternatives.

By End User, commercial buildings dominate, healthcare grows fastest

Commercial and institutional buildings retained the dominant end-user vertical position with approximately 39% of the MulteFire market in 2025. The commercial primacy of this vertical reflects the early adopter dynamic where enterprise campuses, government buildings, and educational institutions pioneered MulteFire deployment for its advantages in security, indoor connectivity reliability, and facility automation integration that public networks and Wi-Fi could not provide at equivalent performance. The inability of Wi-Fi to deliver LTE-grade mobility support, the interference vulnerability of dense Wi-Fi deployments in large commercial buildings, and MulteFire’s seamless handover support for mobile worker devices collectively create compelling commercial building private network investment.

Healthcare is the fastest growing end-user vertical because the extraordinary digital transformation of hospital and medical facility wireless infrastructure creates above-average MulteFire adoption growth from a segment whose specific requirements for security, reliability, and mobility performance exceed what shared public networks or conventional Wi-Fi can provide in dense clinical environments. Each hospital that deploys MulteFire for patient monitoring device connectivity, clinical staff communication, medical equipment tracking, and telemedicine infrastructure creates private network procurement whose compliance with HIPAA data security requirements and clinical workflow performance requirements creates premium specification investment.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

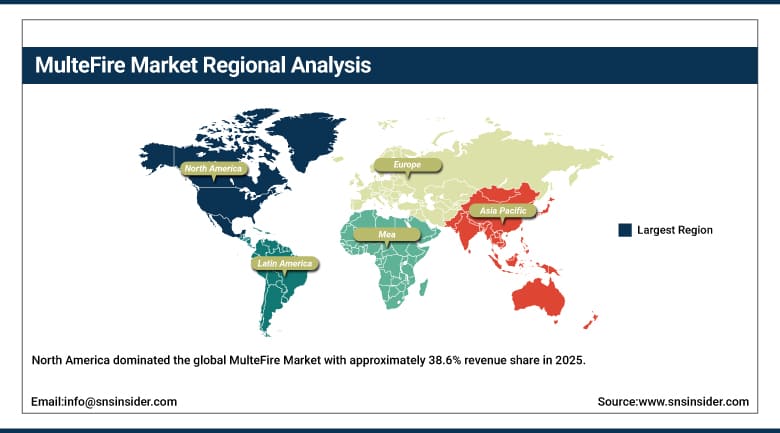

North America MulteFire Market Insights

North America dominated the global MulteFire Market with approximately 38.6% revenue share in 2025, driven by the FCC’s CBRS spectrum framework, early private LTE adoption across manufacturing and logistics, the presence of major technology companies including Qualcomm, Cisco, CommScope, and Airspan, and government investment in smart manufacturing and industrial IoT. The United States accounts for approximately 87.4% of North American revenues through its extraordinary CBRS deployment base and enterprise private network investment.

Canada contributes approximately 12.6% of North American revenues through its manufacturing sector’s industrial IoT investment, the growing enterprise campus private network adoption, and Innovation, Science and Economic Development Canada’s spectrum policy framework supporting shared and unlicensed spectrum use for industrial private networks.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe MulteFire Market Insights

Europe is a technically sophisticated MulteFire market where Germany’s industrial 5G and private network leadership, the EU’s shared spectrum framework, and the automotive and aerospace sectors’ smart manufacturing investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its manufacturing sector’s private network deployment, Nokia’s domestic enterprise sales, and the Bundeswehr’s connected defense infrastructure investment.

The United Kingdom, France, and Sweden are significant secondary markets where smart factory investment, Ericsson’s Swedish private network expertise, and Nokia’s Finnish operations create consistent MulteFire commercial activity. Europe’s regulatory frameworks around shared spectrum and industrial 5G trials provide the policy foundation for continued enterprise MulteFire adoption.

Asia Pacific MulteFire Market Insights

Asia Pacific is the fastest-growing regional market in the MulteFire Market, projected to expand at a CAGR of approximately 18.9% during 2026–2035, driven by China’s extraordinary industrial IoT investment and smart manufacturing programme, India’s growing manufacturing sector’s private network adoption, Japan’s Society 5.0 smart factory initiative, South Korea’s 5G private network deployment, and the extraordinary pace of urbanization creating smart city private network demand. China accounts for approximately 44.8% of Asia Pacific revenues through its government’s digital manufacturing investment, Huawei’s private network portfolio, and the extraordinary scale of Chinese smart factory programmes.

India represents the most commercially dynamic emerging market within Asia Pacific where the government’s PLI manufacturing incentive programmes, the growing smartphone and electronics manufacturing sector’s industrial IoT investment, and the telecom sector’s shared spectrum framework development create above-average MulteFire market growth.

MEA & Latin America MulteFire Market Insights

The UAE leads MEA revenues at approximately 31.2% through its smart city investment in Dubai and Abu Dhabi, NEOM’s industrial campus connectivity requirements, and the oil and gas sector’s industrial IoT private network deployment. Saudi Arabia’s Vision 2030 smart industry investment adds substantial complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its manufacturing sector’s private network adoption, the growing enterprise campus connectivity investment, and the oil and gas sector’s industrial wireless deployment. Mexico’s manufacturing sector and Colombia’s smart city investment collectively sustain regional market development through 2035.

Market Dynamics:

Growth Drivers: Industrial IoT expansion creating private network demand and spectrum regulatory improvements enabling operator-independent deployment

Industrial IoT expansion is the MulteFire market’s most commercially certain structural growth driver. Each manufacturing facility that automates production with IoT sensors, autonomous guided vehicles, collaborative robots, and real-time quality control systems creates wireless connectivity requirements whose reliability, latency, and security specifications exceed Wi-Fi’s capability in dense industrial environments. The manufacturing sector’s transition from reactive to predictive maintenance through continuous machine connectivity creates private network investment whose commercial justification grows with the operational downtime cost that wireless connectivity disruption creates.

Spectrum regulatory improvements enabling operator-independent private LTE deployment are simultaneously removing the most significant commercial adoption barrier. The FCC’s CBRS framework in the U.S., emerging shared spectrum frameworks in Europe and Asia Pacific, and the MulteFire Alliance’s ecosystem standardization collectively create the regulatory and technical foundation on which enterprise private network deployment proceeds without the operator dependency and licensing cost that traditional cellular private networks require.

Restraints: Limited ecosystem awareness and integration complexity with legacy industrial infrastructure

Limited awareness and technical understanding of MulteFire technology relative to more familiar Wi-Fi and Private 5G alternatives creates enterprise decision-making delays that moderate adoption pace in markets where IT procurement teams have established frameworks for evaluating conventional wireless alternatives but limited familiarity with MulteFire’s unique operator-independent private LTE value proposition. Each enterprise whose IT leadership requires extensive vendor education before MulteFire procurement creates sales cycle extension that moderates commercial adoption rate.

Integration complexity with legacy industrial infrastructure including OT networks, SCADA systems, and older manufacturing equipment creates deployment engineering challenges that require specialized systems integration expertise. Each industrial private network deployment that requires custom integration between MulteFire infrastructure and legacy manufacturing systems creates deployment cost that moderates procurement decision-making in cost-sensitive industrial environments.

Opportunities: Neutral host deployment model and 5G NR-U convergence

Neutral host deployment represents the most commercially scalable near-term opportunity whose shared private network infrastructure serving multiple tenants and operators creates per-deployment commercial value substantially exceeding single-tenant alternatives. Each stadium, airport, or smart city deployment that leverages neutral host MulteFire infrastructure to serve multiple MNOs and enterprise tenants simultaneously creates commercial relationships whose aggregate revenue exceeds single-operator site economics.

5G NR-U convergence represents the most commercially transformative longer-term opportunity whose MulteFire technology evolution toward 5G New Radio Unlicensed operation creates an upgrade pathway for enterprise private network customers seeking 5G performance in unlicensed spectrum without operator dependency. Each MulteFire customer whose business case includes future 5G NR-U upgrade capability creates procurement that values technology evolution continuity.

Recent Developments:

-

2026: Nokia Corporation expanded its private wireless portfolio with enhanced private LTE and 5G solutions supporting industrial automation, smart manufacturing, and enterprise connectivity deployments.

-

2025: Hewlett Packard Enterprise (HPE) strengthened its private networking offerings by integrating Athonet technology into enterprise-grade private LTE and 5G platforms for industrial users.

-

2025: Celona, Inc. introduced advanced private wireless management capabilities featuring AI-driven network optimization and simplified deployment for enterprise campuses and industrial facilities.

-

2026: Qualcomm Technologies Inc. expanded support for private wireless and unlicensed spectrum applications through next-generation chipset platforms designed for industrial IoT and private network devices.

MulteFire Market Key Players are:

-

Nokia Corporation

-

Telefonaktiebolaget LM Ericsson

-

Qualcomm Technologies Inc.

-

Huawei Technologies Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

Intel Corporation

-

Cisco Systems, Inc.

-

CommScope, Inc.

-

Airspan Networks Holdings Inc.

-

Casa Systems, Inc.

-

Hewlett Packard Enterprise

-

Rakuten Symphony, Inc.

-

Redline Communications Group Inc.

-

ip.access Ltd.

-

Baicells Technologies Co., Ltd.

-

InterDigital, Inc.

-

Sony Corporation

-

Boingo Wireless, Inc.

-

Celona, Inc.

-

Betacom, Inc.

MulteFire Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.78 Billion |

| Market Size by 2035 | USD 44.58 Billion |

| CAGR | CAGR of 31.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device (Small Cells, Switches, Controllers) • By Technology (MulteFire 4G, MulteFire 5G, MulteFire Wi-Fi) • By Deployment Mode (Public, Private, Hybrid) • By End Use (Commercial & Institutional Buildings, Industrial Manufacturing, Transportation & Logistics, Healthcare, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nokia Corporation, Telefonaktiebolaget LM Ericsson, Qualcomm Technologies Inc., Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Intel Corporation, Cisco Systems, Inc., CommScope, Inc., Airspan Networks Holdings Inc., Casa Systems, Inc., Hewlett Packard Enterprise, Rakuten Symphony, Inc., Redline Communications Group Inc., ip.access Ltd., Baicells Technologies Co., Ltd., InterDigital, Inc., Sony Corporation, Boingo Wireless, Inc., Celona, Inc., Betacom, Inc. |

Frequently Asked Questions

Regulatory uncertainties and spectrum interference issues pose deployment challenges.

The MulteFire Market is expected to grow at a CAGR of 31.69% from 2026 to 2035.

The MulteFire Market was valued at USD 2.78 Billion in 2025.

Rising enterprise demand for private, secure, operator-independent wireless connectivity in industrial IoT environments, and spectrum regulatory improvements.

Small Cells dominated the MulteFire Market with approximately 48% share in 2025, while the Controllers segment is the fastest growing.

Get in Touch