Multi-Cancer Early Detection Market Report Scope & Overview:

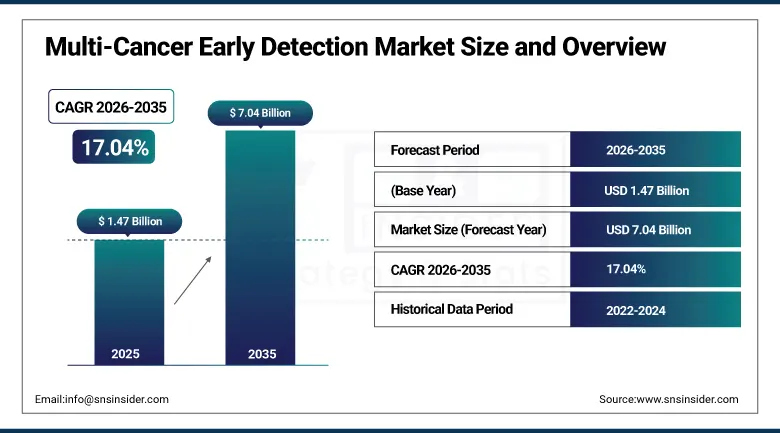

The Multi-Cancer Early Detection Market was valued at USD 1.47 Billion in 2025 and is expected to reach USD 7.04 Billion by 2035, growing at a CAGR of 17.04% from 2026 to 2035.

The global multi-cancer early detection market represents one of the most transformative emerging segments within preventive oncology. Multi-cancer early detection technologies use liquid biopsy techniques including circulating cell-free DNA methylation profiling, circulating tumor DNA fragment analysis, and multiomics biomarker panels. The market is propelled by the extraordinary convergence of genomics, artificial intelligence, and non-invasive diagnostics creating test accuracy improvements that are progressively building physician and patient confidence, rising cancer burden globally with the WHO estimating approximately 10 million cancer-related deaths annually, increasing emphasis on preventive healthcare and population-scale cancer screening, and the global policy priority of shifting cancer diagnosis from symptomatic late-stage presentation toward asymptomatic early-stage detection where survival rates are dramatically higher.

In May 2025, GRAIL formed a new collaboration with athenahealth to integrate its Galleri multi-cancer early detection test with Athena Coordinator Core, a service for streamlining laboratory order transmission and care coordination. The integration is supported by athenahealth's cloud-based electronic health record system Athena One, enabling primary care physicians to order Galleri testing through their existing clinical workflow without separate order entry systems, directly addressing the physician adoption barrier that order friction creates for novel screening tests whose commercial scaling requires seamless EHR integration.

Market Size and Forecast:

-

Market Size in 2026E: USD 1.72 Billion

-

Market Size by 2035: USD 7.04 Billion

-

CAGR: 17.04% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

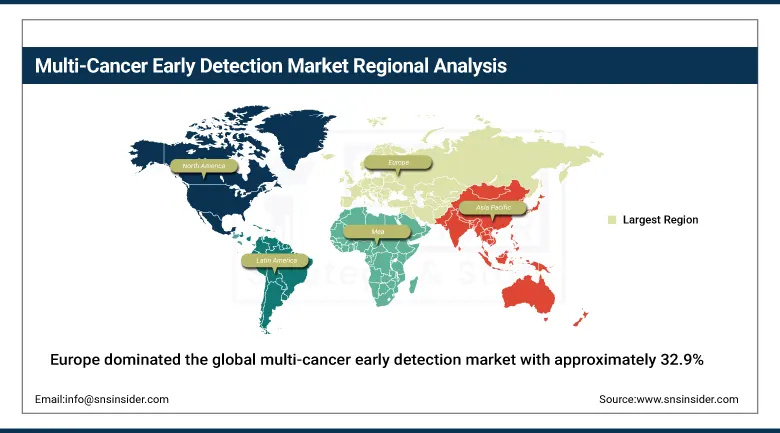

Largest Region: Europe

To Get more information On Multi-Cancer Early Detection Market - Request Free Sample Report

Multi-Cancer Early Detection Market Trends:

-

Methylation profiling is improving MCED test accuracy by enhancing cancer detection sensitivity and tissue-of-origin identification.

-

AI and machine learning integration with multiomics analysis is increasing the diagnostic accuracy of multi-cancer early detection tests.

-

Regulatory support through accelerated approval pathways is advancing the commercialization of next-generation MCED technologies.

-

Large-scale population screening studies are generating clinical evidence to support healthcare adoption and reimbursement decisions.

-

Direct-to-consumer access through concierge healthcare and telehealth platforms is expanding early adoption of MCED testing.

U.S. Multi-Cancer Early Detection Market Outlook:

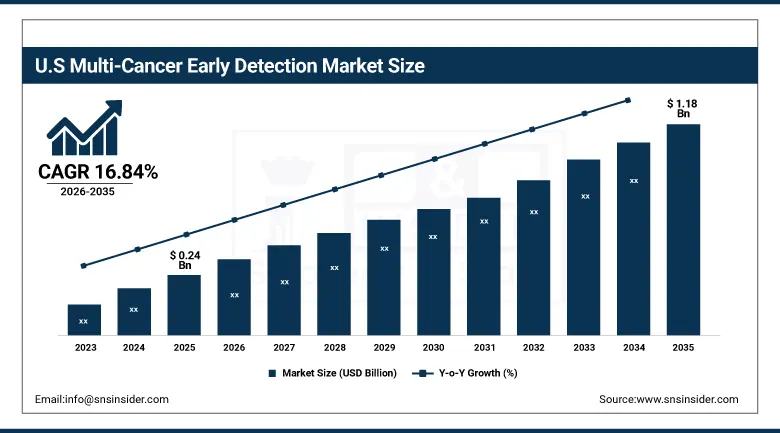

The U.S. Multi-Cancer Early Detection Market was valued at approximately USD 0.24 Billion in 2025 and is expected to reach approximately USD 1.18 Billion by 2035, growing at a CAGR of approximately 16.84%.

The US is the most important individual-country market among all countries in the MCED space due to greater investments in biotech and innovative policy-driven efforts, along with increasing focus on adoption of MCED testing into the practice of general health care check-ups. Galleri test by GRAIL, the pipeline MCED tests by Exact Sciences, Shield test by Guardant Health, and the multi-omics platform by Freenome together represent the MCED commercial development landscape in the domestic market. The inclusion of Clear Note Health's Advantest MCED test in NCI's Vanguard Study generates large-scale evidence in an effort funded by the government, thus ensuring scientific and commercial legitimacy.

In January 2025, Clear Note Health reported that the Advantest Multi-Cancer Detection Test had been selected for the NCI’s Vanguard Study by the National Cancer Institute. The NCI Vanguard Study is a large government-sponsored prospective study that aims to collect evidence on the performance of MCED tests in a real-world screening setting. Participation in the Vanguard Study leads to both funding and the development of a scientific validation database needed for regulatory and coverage decisions, providing an important commercial boost for Clear Note Health’s MCED test commercialization strategy.

Multi-Cancer Early Detection Market Segment Analysis:

-

By Type, the Epigenetic & Methylation Analysis segment dominated the Multi-Cancer Early Detection Market with approximately 39.8% share in 2025, while the Liquid Biopsy segment is the fastest growing.

-

By Cancer Type, the Lung Cancer segment dominated the Multi-Cancer Early Detection Market with approximately 31.6% share in 2025, while the Liver Cancer segment is the fastest growing.

-

By Application, the Screening segment dominated the Multi-Cancer Early Detection Market with approximately 42.7% share in 2025, while the Early Cancer Detection segment is the fastest growing.

-

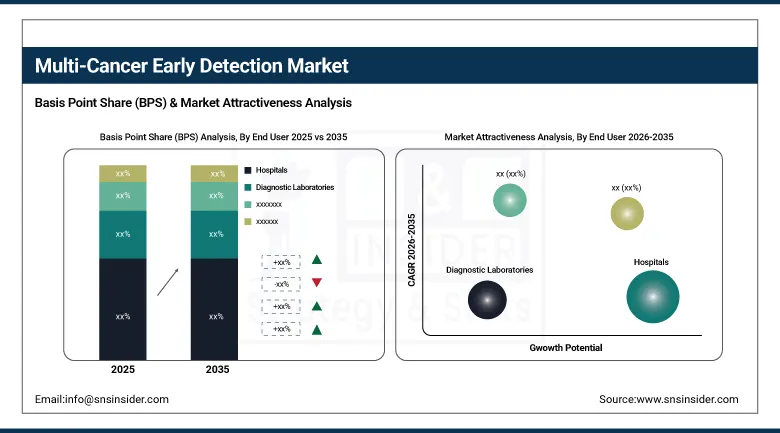

By End Use, the Hospitals segment dominated the Multi-Cancer Early Detection Market with approximately 46.9% share in 2025, while the Diagnostic Laboratories segment is the fastest growing.

By Type, gene panel and LDT dominates, liquid biopsy grows fastest

The epigenetic & methylation analysis segment dominated the market with approximately 39.8% share in 2025, owing to its superior ability to detect cancer-specific DNA methylation patterns across multiple cancer types at early stages. This technology offers high sensitivity and specificity while accurately identifying the tissue of origin, making it highly valuable for population-wide cancer screening programs. Growing clinical validation, increasing regulatory support, and the commercialization of methylation-based assays have accelerated adoption among healthcare providers and diagnostic laboratories. Leading companies continue to invest in advanced methylation profiling platforms, strengthening their role in precision oncology and supporting the segment’s dominant position in the global market.

Liquid biopsy is the fastest growing type because the convergence of technical performance improvements, consumer and physician awareness building through GRAIL’s commercial marketing, and the progressive building of clinical evidence from large-scale population screening trials creates adoption acceleration momentum. Each clinical trial result that demonstrates liquid biopsy MCED test sensitivity and specificity comparable to or exceeding existing standard-of-care single-cancer screening tests creates physician confidence that sustains adoption beyond early technology enthusiasts. Freenome’s USD 254 million February 2024 fundraise for multiomics MCED platform development, and Guardant Health’s Shield colorectal cancer screening test FDA clearance creating a regulatory precedent for blood-based cancer screening, collectively demonstrate the commercial investment sustaining liquid biopsy MCED development.

By End Use, hospitals dominate, diagnostic laboratories grow fastest

Hospitals retained the dominant end-use position with approximately 46.9% of the multi-cancer early detection market in 2025. Academic medical centers and comprehensive cancer centers represent the primary MCED commercial adoption setting because their patient population mix includes the cancer risk age groups for whom MCED testing is most clinically justified, their physician specialists include the oncologists and internists most familiar with cancer screening guideline evolution, and their integrated diagnostic and treatment infrastructure enables seamless follow-up workup for positive MCED screen results. GRAIL’s health system partnerships with major academic medical center networks and Exact Sciences’ hospital laboratory relationships collectively define the institutional channel that sustains hospital’s dominant end-use position.

Diagnostic laboratories are the fastest growing end use because the direct-to-consumer test access model for self-pay patients, outsourcing from smaller hospitals and primary care practices lacking internal MCED infrastructure, and specialist molecular diagnostic laboratory scale economics create above-average commercial volume growth outside hospital settings. Quest Diagnostics’ and LabCorp’s national laboratory network relationships with physician practices create a distribution channel for MCED test ordering that reaches the primary care physician population whose patient volume substantially exceeds specialist physician ordering volume, creating a commercial scale opportunity that compounds with primary care physician MCED awareness growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Multi-Cancer Early Detection Market Insights

North America is a rapidly growing multi-cancer early detection market where U.S. biotechnology investment, FDA regulatory pathway development, and GRAIL, Exact Sciences, Guardant Health, and Freenome's commercial development collectively define the global MCED innovation frontier. The United States accounts for approximately 87.4% of North American revenues through these commercial operations and the growing self-pay executive health and concierge medicine market for Galleri and similar premium-positioned MCED tests.

Canada contributes approximately 12.6% of North American revenues through its public health system's evaluation of MCED test integration into population cancer screening programmes, academic cancer research investment, and the growing private diagnostic laboratory sector's MCED test offering.

Europe Multi-Cancer Early Detection Market Insights

Europe dominated the global multi-cancer early detection market with approximately 32.9% of revenues in 2025, supported by favorable reimbursement policies in several markets, strong government-funded cancer research ecosystems, and the NHS-GRAIL Galleri trial's extraordinary 140,000-participant scale creating the largest MCED population screening evidence generation programme globally. Germany accounts for approximately 22.3% of European revenues through its oncology research investment, statutory health insurance system's preventive care coverage framework, and academic cancer center network.

The United Kingdom, France, and the Netherlands are significant secondary markets where the NHS England Galleri trial creates structured MCED testing volume, Institut Curie's French research investment, and the Dutch Cancer Institute's population screening research create consistent procurement. Europe’s generally favorable preventive screening coverage policies relative to U.S. Medicare create a reimbursement environment that sustains clinical adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Multi-Cancer Early Detection Market Insights

Asia Pacific multi-cancer early detection market is projected to grow at a CAGR of approximately 16.1% during 2026–2035, making it the fastest-growing regional market., driven by China's extraordinary government cancer prevention policy investment, Japan's advanced preventive healthcare adoption, South Korea's genomics innovation, and India's expanding molecular diagnostic infrastructure. China accounts for approximately 44.8% of Asia Pacific revenues through domestic MCED company development including AnchorDx, Burning Rock Biotech, and Singlera Genomics, combined with international company partnerships creating clinical validation and commercial deployment.

Japan represents a significant secondary market within Asia Pacific where the government's cancer screening programme evolution, the academic hospital network's advanced diagnostic adoption, and the technology sector's genomics investment create structured MCED market development. South Korea's Samsung Medical Center and Asan Medical Center create early adopter academic hospital deployment.

MEA & Latin America Multi-Cancer Early Detection Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through King Faisal Specialist Hospital's oncology innovation investment, Vision 2030's healthcare technology adoption, and the government's cancer prevention programme. The UAE's Cleveland Clinic Abu Dhabi and Mediclinic add complementary Gulf demand.

Brazil leads Latin American revenues at approximately 44.2% through its public oncology programme, INCA's cancer research, and the growing private diagnostic laboratory sector. Mexico's academic hospital network and Argentina's oncology research community collectively sustain regional market development through 2035.

Market Dynamics:

Growth Drivers: Rising cancer burden and AI-driven diagnostics

The extraordinary global cancer burden, with the WHO projecting cancer cases rising by approximately 60% over the next two decades from rising population aging and cancer risk factor exposure, is creating the most compelling public health motivation for population-scale MCED screening investment. Each country whose cancer mortality statistics demonstrate the disproportionate contribution of late-stage diagnosis to cancer deaths creates policy motivation for early detection investment whose commercial expression includes MCED programme evaluation and pilot deployment.

AI and machine learning diagnostic performance improvement is progressively addressing the sensitivity and specificity limitations that created physician hesitation about MCED clinical utility. Each published clinical study that demonstrates improved cancer signal detection sensitivity with reduced false positive rate sustains physician confidence building that is critical for broad-based MCED adoption beyond high-risk population targeting.

Restraints: Regulatory uncertainty and positive result follow-up

Regulatory pathway uncertainty for MCED tests, whose FDA clearance standard remains under development and whose clinical validation evidence requirements exceed traditional single-cancer screening test precedents, creates commercial launch timeline uncertainty that moderates healthcare system adoption investment. Each regulatory decision on MCED test evidentiary standards creates commercial implications for multiple developers whose product differentiation on sensitivity and specificity metrics depends on regulatory definition of acceptable performance thresholds.

Positive MCED result follow-up complexity creates a practical barrier to widespread deployment whose resolution requires healthcare system preparation for the diagnostic imaging, specialist consultation, and tissue biopsy workup cascade that a positive blood test result initiates. Each healthcare system whose diagnostic radiology and pathology capacity is insufficient to absorb the follow-up workup volume generated by population-scale MCED screening creates adoption restraint independent of test performance.

Opportunities: NHS trial data creating population screening integration

The NHS-GRAIL Galleri trial's 140,000-participant population-level evidence dataset represents the most commercially significant near-term opportunity whose publication will provide the real-world performance evidence that national health system payers globally require for coverage policy decision making. Each positive Galleri trial outcome metric that supports NHS England integration of MCED testing into national cancer screening programmes creates a commercially replicable population screening template that other national health systems can adopt.

Medicare coverage expansion for MCED testing represents the most commercially transformative U.S. market opportunity whose coverage of annual MCED testing for Medicare-eligible Americans aged 65 and above would create the largest single insurance coverage expansion in MCED market history. The USPSTF's evaluation process for MCED test evidence and CMS's coverage with evidence development pathway collectively create the regulatory and coverage policy milestones that sustain investor and commercial development confidence.

Recent Developments:

-

2026: GRAIL, Inc. expanded the clinical adoption of its Galleri® multi-cancer early detection test through new healthcare partnerships and additional real-world clinical evidence.

-

2025: Guardant Health, Inc. advanced its multi-cancer early detection research with expanded clinical validation of blood-based cancer screening technologies.

-

2025: Exact Sciences Corporation strengthened its MCED portfolio through continued development of next-generation liquid biopsy assays and expanded oncology diagnostic capabilities.

-

2026: Freenome Holdings, Inc. reported new AI-powered multiomics clinical study results supporting earlier detection of multiple cancer types using blood-based screening.

Multi-Cancer Early Detection Market key players are:

-

GRAIL, Inc. (Illumina)

-

Exact Sciences Corporation

-

Guardant Health, Inc.

-

Freenome Holdings, Inc.

-

Foundation Medicine, Inc.

-

AnchorDx Medical Co., Ltd.

-

Burning Rock Biotech Limited

-

Singlera Genomics Inc.

-

ClearNote Health

-

Laboratory for Advanced Medicine, Inc.

-

Natera, Inc.

-

Illumina, Inc.

-

Roche Diagnostics

-

Thermo Fisher Scientific Inc.

-

Abbott Laboratories

-

VolitionRx Limited

-

NeoGenomics Laboratories, Inc.

-

VESEN Inc.

-

ExactDx, Inc.

-

Harbinger Health, Inc.

Multi-Cancer Early Detection Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.47 Billion |

| Market Size by 2035 | USD 7.04 Billion |

| CAGR | CAGR of 17.04% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Liquid Biopsy, Genomic Analysis, Epigenetic & Methylation Analysis, Others) • By Cancer Type (Lung Cancer, Breast Cancer, Prostate Cancer, Liver Cancer, Others) • By Application (Screening, Early Cancer Detection, Risk Assessment, Recurrence Monitoring, Companion Diagnostics & Clinical Decision Support) • By End Use (Hospitals, Diagnostic Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GRAIL, Inc. (Illumina), Exact Sciences Corporation, Guardant Health, Inc., Freenome Holdings, Inc., Foundation Medicine, Inc., AnchorDx Medical Co., Ltd., Burning Rock Biotech Limited, Singlera Genomics Inc., ClearNote Health, Laboratory for Advanced Medicine, Inc., Natera, Inc., Illumina, Inc., Roche Diagnostics, Thermo Fisher Scientific Inc., Abbott Laboratories, VolitionRx Limited, NeoGenomics Laboratories, Inc., VESEN Inc., ExactDx, Inc., Harbinger Health, Inc. |

Frequently Asked Questions

The Multi-Cancer Early Detection Market is expected to grow at a CAGR of 17.04% from 2026 to 2035.

The Multi-Cancer Early Detection Market was valued at USD 1.47 Billion in 2025.

Rising global cancer burden creating public health motivation for population-scale early detection investment.

Epigenetic & Methylation Analysis dominated with approximately 88.8% share in 2025.

Europe dominated the Multi-Cancer Early Detection Market with approximately 32.9% of revenues in 2025.

Get in Touch