Multi-Tenant Data Center Market Report Scope & Overview:

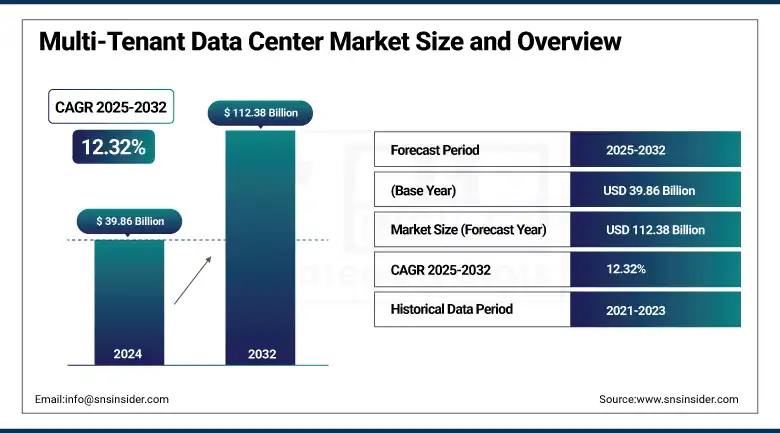

Multi-Tenant Data Center Market size was valued at USD 39.86 billion in 2024 and is anticipated to reach USD 112.38 billion by 2032, growing at a CAGR of 12.32% during 2025-2032.

The Multi-Tenant Data Center Market growth is attributed to the growing demand for cloud services, data storage, and the requirement for a rapidly scalable and agile IT infrastructure across numerous sectors. The market is growing as a result of the demand for secure, affordable, and scalable solutions. The growth of the multi-tenant data center market is also influenced by the adoption of IoT technologies, digital transformation, and an increase in data generation.

For instance, around 402.74 million terabytes of information was generated per day in 2024, and it is expected that around 147 zettabytes of information will be generated in 2025, further boosting the growing need for multi-tenant data center infrastructure.

To Get more information On Multi-Tenant Data Center Market - Request Free Sample Report

As per a research, 90% of the global companies report missing crucial storage features including high availability and tamperproof protection, and 54% opt for central or decentralized data centers over public cloud storage. Addition, around 69% of the market players are planning to incorporate AI capabilities in their storage infrastructure for efficiency and automation.

For instance, in 2024, Iron Mountain expanded its data center capacity in Virginia by more than 350 megawatts, bringing its total planned global capacity to over 1.2 gigawatts demonstrating robust industry investment in multi-tenant infrastructure.

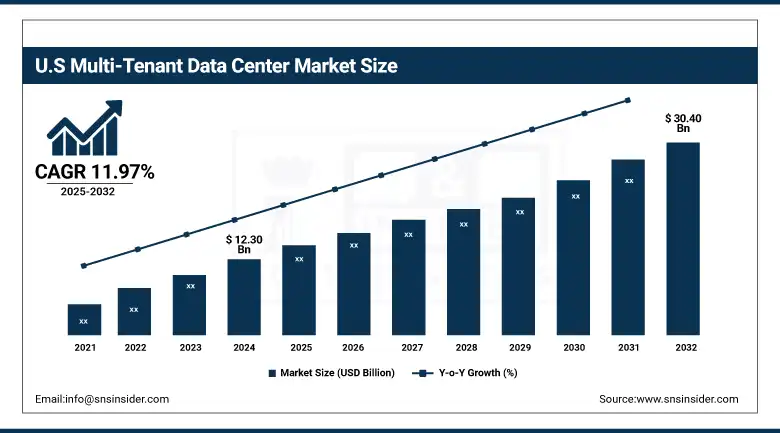

The U.S. multi-tenant data center market size accounted for a valuation of USD 12.30 billion in 2024 and is predicted to grow at a valuation of USD 30.40 billion by 2032, expanding at a CAGR of 11.97% during 2025-2032.

The U.S. multi-tenant data center market is growing due to the high demand for big data, colocation services, and cloud computing globally. During the digital transformation of businesses that have adopted IoT and AI-based technologies, requirements for scalable, secure, and efficient data centers boost market expansion and growth.

In 2024, Equinix has announced a joint venture with GIC and CPP Investments to invest over USD 15 billion in expanding its xScale data center program across the U.S. This initiative aims to address the growing demand for AI and cloud services by adding more than 1.5 gigawatts of capacity.

In 2024, Equinix and PGIM Real Estate launched a USD 600 million joint venture to develop the first xScale data center in the U.S. Located in Silicon Valley, the facility is set to be completed by Q2 2024.

Multi-Tenant Data Center Market Dynamics:

Drivers:

-

Cloud Adoption Boosts the Demand for Scalable and Cost-Efficient Multi-Tenant Data Center Infrastructure Across Industries Globally

Cloud computing is accelerating growth of multi-tenant data centers as organizations demand scalable and economical data storage solutions. With cloud infrastructures, operations are simplified, so are flexibility, and capital outlay has a minimum with these. Multi-tenant data centers offer companies the ability to scale without the high capital expenditure since they share resources. Increased usage of Software-as-a-Service (SaaS) and platform services further fuels demand, enabling ongoing market expansion for scalable, secure, and efficient data center solutions in industries of all sizes.

According to Google Cloud, in 2023, 41.4% of IT leaders increased their use of cloud-based services and products, 33.4% planned to migrate from legacy enterprise software to cloud-based tools, and over 50% of organizations were hiring or retraining staff to better optimize cloud spending highlighting the accelerating shift toward cloud adoption.

According to Research, in 2024, Amazon Web Services (AWS) led the global cloud infrastructure market with a 30% share, followed by Microsoft Azure at 21% and Google Cloud at 12%.

Restraints:

-

Shared Infrastructure Heightens Security Risks and Threatens Sensitive Data Protection in Multi-Tenant Data Centers

The multi-tenant data center model based on shared infrastructure presents security issues that can possibly slow down market expansion. Since several organizations share physical hardware, the threat of data compromise and unauthorized entry is present. Even with sophisticated security solutions such as encryption, data and system isolation in such an environment is still challenging, particularly for financial and health organizations whose data has to be protected by stringent data protection laws. Organizations are likely to shy away from embracing multi-tenant data centers unless security issues are comprehensively addressed.

According to research, 74% of all breaches involve human error or misuse. The average data breach cost reached an all-time high of $4.88 million in 2024, marking a 10% increase from 2023. It takes an average of 204 days to identify and 73 days to contain a breach.

Opportunities:

-

IoT Growth Increases Need for High-Performance, Scalable Data Center Solutions to Support Real-Time Processing

Expansion in IoT technology is making a drastic impact on the multi-tenant data center industry. Organizations trust advanced data centers to offer secure storage, handling, and examination of the incredible volumes of information produced by IoT devices. Multitenant data centers offer high-performance scalable solutions to facilitate IoT applications, especially in industries where timely processing matters, like manufacturing, healthcare, and transportation.

According to research, 83% of healthcare organizations have adopted IoT technologies, leveraging real-time data for improved patient care and operational efficiency. Additionally, the number of IoT devices was recorded to be 15.9 billion in 2023.

Challenges:

-

Managing Operational Efficiency While Scaling Infrastructure Amid Surging Data Center Demand Remains a Persistent Challenge

Multi-tenant data centers struggle to maintain operational efficiency as they manage increasing resource demands. As the generation of data grows, the data centers have to scale infrastructure, power usage, and cooling systems. Avoiding inefficiencies while expanding is key, as inefficiency can affect operations, increase costs, and slow down services. Coping with these issues while satisfying customer demand is a continuous challenge for multi-tenant data center players.

According to Uptime Institute’s 2023 survey, cooling issues contribute to 13% of impactful outages, highlighting the critical need for efficient thermal management in data centers. Power remains the leading cause of impactful outages, accounting for 54% of such incidents.

Additionally, research from the International Energy Agency (IEA) shows that data centers account for around 1% of global energy use, emphasizing the importance of optimizing power usage and cooling systems.

Multi-Tenant Data Center Market Segmentation Analysis:

By Component

The Solutions segment dominated the Multi-Tenant Data Center Market with the highest revenue share of about 74% in 2024 due to its wide spectrum of offerings like cloud services, security solutions, and data storage, which are important for enterprises with large-scale infrastructure. Demand for multi-tenant data centers is rising, as enterprises increasingly depend upon these solutions to ensure scalability, flexibility, and operational efficiency.

The Services segment is expected to grow at the fastest CAGR of 13.71% over the forecasting period 2025-2032 due to the fact that firms are tending to give more importance to managed services, network optimization, and cybersecurity offerings. The boost towards outsourcing of IT functions as well as specifications for niche-level services like disaster recovery and analytics is driving growth in the segment.

By Type

The Retail Colocation segment led the Multi-Tenant Data Center Market with the largest revenue share of approximately 71% in 2024 owing to the fact that companies favor retail colocation as it is cost-saving and scalable. It enables companies to lease space and maintain their own equipment but utilize the data center's infrastructure, thus offering a versatile solution to different industries, particularly small and mid-sized organizations.

The Wholesale Colocation segment is anticipated to grow at the fastest CAGR of approximately 13.59% from 2025-2032, as more demand is expected from large companies and cloud providers that need huge space, power, and cooling capacities. With scaling up of businesses, they opt for wholesale colocation for the fact that it can take large, dedicated infrastructure which grants them more control and a lower-cost solution for massive operations.

By Enterprise Size

Large Enterprises segment dominated the Multi-Tenant Data Center Market with a highest revenue share of around 68% in 2024, as these enterprises require robust, secure, and scalable data infrastructure to manage vast amounts of data and transactions. They heavily depend on multi-tenant data centers due to their cost-effectiveness and flexibility, enabling them to scale operations without a high amount of investment in physical infrastructure.

The SME segment is expected to grow at the fastest CAGR of approximately 14.52% during 2025-2032, supported by mounting digital transformation activities and growing use of cloud-based solutions among small and medium enterprises. With SMEs looking to contain IT infrastructure costs while preserving flexibility and data protection, multi-tenant data centers provide an affordable, scalable option. Also, rising awareness and availability of advanced IT solutions are fueling demand in this segment.

By Industry vertical

The IT & Telecom industry led the Multi-Tenant Data Center Market Share of around 29% in 2024 due to the fact that these sectors demand a huge data processing and storage capacity to host their growing networks, services, and customer bases. Multi-tenant data centers supply the platform for telecommunication networks and IT services with scalable and secure options for handling sophisticated operations.

The Healthcare segment is expected to grow at the fastest CAGR of around 14.75% between 2025-2032, with the healthcare industry increasingly adopting digital health solutions like electronic health records (EHR), telemedicine, and cloud-based applications. The demand for scalable and secure data storage facilities for patient information and healthcare solutions will drive growth, as healthcare organizations look for data centers with compliance with regulations and high availability.

By Application

The Public Cloud segment dominated the Multi-Tenant Data Center Market with the highest revenue market share of nearly 62% in 2024, owing to the rising adoption of cloud environments among businesses owing to their scalability, cost-effectiveness, and agility. Public cloud services, provided by industry leaders like AWS, Google Cloud, and Microsoft Azure, are finding favor among businesses looking to outsource their data management and IT infrastructure needs.

The Private Cloud segment is growing at the fastest CAGR of approximately 13.69% over 2025-2032, driven by the increasing need for more security, compliance, and control of confidential data. Companies handling sensitive or regulatory-limited information, like in finance and healthcare, are increasingly choosing private cloud offerings, which ensure greater data privacy and security than public cloud offerings.

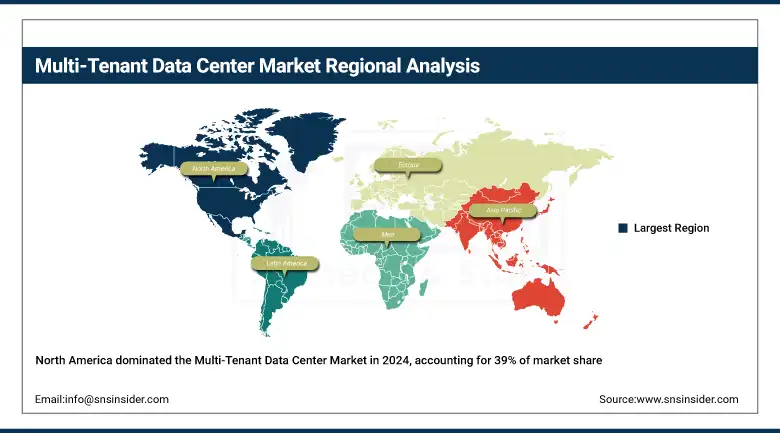

Regional Analysis:

North America dominated the Multi-Tenant Data Center Market with the highest revenue share of about 39% in 2024 due to the region's advanced IT infrastructure, high adoption of cloud computing, and strong presence of major tech companies. Growing demand from the IT, financial, and healthcare sectors for data storage facilities, colocation, and cloud computing solutions is fueling domination of the region, along with major investment towards building and upgrading data centers.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. led the Multi-Tenant Data Center Market with growing demand for cloud, strong infrastructure, and greater tech adoption.

Asia Pacific is also anticipated to expand at the fastest CAGR of 14.82% during 2025-2032 driven by the accelerated rate of digitalization and cloud service expansion in emerging markets such as China, India, and Southeast Asia. Increased usage of data, increased internet penetration, and entry of global players in the region to establish data centers are fueling its growth, as well as growing demand for cost-effective and scalable IT infrastructure solutions.

China led the Multi-Tenant Data Center Market in 2024 because of accelerated digital transformation, high demand for cloud services, and government encouragement for infrastructure development.

Europe has a strong presence in the Multi-Tenant Data Center Market due to its advanced digital infrastructure, high demand for data storage, robust data protection regulations, and growing adoption of cloud services across industries, driving market growth.

In Europe, Germany led the Multi-Tenant Data Center Market in 2024 because of its robust industrial base, high data center demand, and central location in Europe, making it a hub for cloud services and digital infrastructure.

Middle East & Africa and Latin America are increasingly present in the Multi-Tenant Data Center Market as a result of growing digitalization, rising cloud service demand, infrastructure investments, and the necessity for secure data storage and processing solutions.

Key Players:

Multi-Tenant Data Center Market Companies include Equinix Inc., Digital Realty, NTT Communications Corporation, IBM Corporation, Global Switch Ltd., CenturyLink Inc., Rackspace Inc., Iron Mountain, Telstra International, Eaton Corporation, AT&T, China Telecom, Cisco, DuPont Fabros, and Level 3 Communications.

Recent Developments:

-

In 2024, Lumen Technologies entered into a supply agreement with Corning for next-generation fiber-optic cables, reserving 10% of Corning's global fiber capacity over two years to support AI-enabled data centers and expand Lumen's intercity network.

-

In 2024, Iron Mountain expanded its planned data center capacity in Virginia by acquiring two development sites in Richmond and Manassas, adding over 350 megawatts of future capacity to support growing customer demand

-

In 2024, NTT Com's Osaka 7 Data Center received certification under the NVIDIA DGX-Ready Data Center program, validating its capability to support high-density AI workloads. The facility is part of NTT's Green Nexcenter initiative, focusing on energy efficiency and sustainability.

-

In 2023, Digital Realty and Blackstone announced a USD 7 billion joint venture to develop four hyperscale data center campuses across three metro areas in Europe and North America, expected to deliver approximately 500 megawatts of IT capacity.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 39.86 Billion |

| Market Size by 2032 | USD 112.38 Billion |

| CAGR | CAGR of 12.32% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Type (Retail Colocation, Wholesale Colocation) • By Enterprise Size (SME, Large Enterprises) • By Application (Public Cloud, Private Cloud) • By Industry Vertical (BFSI, Healthcare, Government & Defense, IT & Telecom, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Equinix Inc., Digital Realty, NTT Communications Corporation, IBM Corporation, Global Switch Ltd., CenturyLink Inc., Rackspace Inc., Iron Mountain, Telstra International, Eaton Corporation, AT&T, China Telecom, Cisco, DuPont Fabros, Level 3 Communications |

Frequently Asked Questions

The IT & Telecom sector led with a 29% market share due to its significant need for data processing and storage capacity for network services.

Retail Colocation led with a 71% market share, offering cost-effective and scalable solutions for businesses, especially small to mid-sized enterprises.

The Solutions segment dominated with a 74% market share due to cloud services, security solutions, and data storage offerings.

Growth is driven by cloud adoption, data storage, IT infrastructure needs, digital transformation, and IoT technology integration.

Multi-Tenant Data Center Market was valued at USD 39.86 billion in 2024 and is expected to reach USD 112.38 billion by 2032, growing at a CAGR of 12.32% from 2025-2032.

Get in Touch